Ratings and rankings: Voodoo or Science?

Abstract

Composite indicators aggregate a set of variables using weights which are understood to reflect the variables’ importance in the index. In this paper we propose to measure the importance of a given variable within existing composite indicators via Karl Pearson’s ‘correlation ratio’; we call this measure ‘main effect’. Because socio-economic variables are heteroskedastic and correlated, relative nominal weights are hardly ever found to match relative main effects; we propose to summarize their discrepancy with a divergence measure. We discuss to what extent the mapping from nominal weights to main effects can be inverted. This analysis is applied to six composite indicators, including the Human Development Index and two popular league tables of university performance. It is found that in many cases the declared importance of single indicators and their main effect are very different, and that the data correlation structure often prevents developers from obtaining the stated importance, even when modifying the nominal weights in the set of nonnegative numbers with unit sum.

keywords:

Composite indicators, linear aggregation, Pearson’s correlation ratio, modelling, weigths.1 Introduction

In social sciences, composite indicators aggregate individual variables with the aim to capture relevant, possibly latent, dimensions of reality such as a country’s competitiveness (World Economic Forum (2010)), the quality of its governance (Agrast et al. (2010)), the freedom of its press (Reporters Sans Frontieres (2011); Freedom House (2011)) or the efficiency of its universities or school system (Leckie and Goldstein (2009)). These measures have been termed ‘pragmatic’ (see Hand (2009), pp. 12-13), in that they answer a practical need to rate individual units (such as countries, universities, hospitals or teachers) for some assigned purpose.

Composite indicators (which are also referred to here as indices) have been increasingly adopted by many institutions, both for specific purposes (such as to determine eligibility for borrowing from international loan programs) and for providing a measurement basis for shaping broad policy debates, in particular in the public sector (Bird et al. (2005)). As a result, public interest in composite indicators has enjoyed a fivefold increase over the period : a search of ‘composite indicators’ on Google Scholar gave matches on October and at the time of the first version of this paper (December ).

Composite indicators are fraught with normative assumptions in variable selection and weighting. Here ‘normative’ is understood to be ‘related to and dependent upon a system of norms and values’. For example, the proponents of the Human Development Index (HDI) advocate replacing gross domestic product (GDP) per capita as a measure of the progress of societies with a combination of (i) GDP per capita (ii) education and (iii) life expectancy, see Ravallion (2010). Both the selection of these three specific dimensions and the choice of building the index by giving these dimensions equal importance are normative, see Stiglitz et al. (2009), p. 65. Composite indicators are thus often the subject of controversy, see Saltelli (2007), Hendrik et al. (2008).

The statistical analysis of composite indicators is essential to prevent media and stakeholders taking them at face value (see the recommendations in Organisation for Economic Co-operation and Development (2008)), possibly leading to questionable policy choices. For example, a policy maker might think of merging higher education institutions just because the most popular league table of universities puts a prize on larger universities, see Saisana et al. (2011).

Most existing composite indicators are linear, i.e. weighted arithmetic averages Organisation for Economic Co-operation and Development (2008). Linear aggregation rules have been criticized because weaknesses in some dimensions are compensated by strengths in other dimensions; this characteristic is called ‘compensatory’. Non-compensatory and non-linear aggregate ranking rules have been advocated by the literature on multicriteria decision making, see for example Billaut et al. (2010), Munda (2008), Munda and Nardo (2009), Balinski and Laraki (2010). In this paper we concentrate on linear aggregation, because of its widespread use.

In this paper we address the issue of measuring variable importance in existing composite indicators. As illustrated by a motivating example at the end of this section, nominal weights are not a measure of variable importance, although weights are assigned so as to reflect some stated target importance, and they are communicated as such. In linear aggregation, the ratio of two nominal weights gives the rate of substitutability between the two individual variables, see (Boyssou et al., 2006, Chapter 4), or Decancq and Lugo (2010), and hence can be used to reveal the target relative importance of individual indicators. This target importance can then be compared with ex-post measures of variables’ importance, such as the one presented in this paper.

We propose to measure the importance of a given variable via Karl Pearson’s ‘correlation ratio’, which is widely applied in global sensitivity analysis as a first-order sensitivity measure; we call this measure ‘main effect’. Main effects represent the expected relative variance reduction obtained in the output (the index) if a given input variable could be fixed (Saltelli and Tarantola (2002), see Section 3.1). They are based on the statistical modelling of the relation between the variable and the index.

This statistical modelling can be parametric or non-parametric; we compare a linear and a non-parametric alternative based on local-linear kernel smoothing. We apply the main effects approach to six composite indicators, including the HDI and two popular league tables of university performance. We find that in some cases, a linear model can give a reasonable estimate of the main effects, but in other cases the non-parametric fit must be preferred. Further, we find that nominal weights hardly ever coincide with main effects. We propose to summarize this deviation in a discrepancy statistic, which can be used by index developers and users alike to gauge the gap between the effective and the target importance of each variable.

We also pose the question of whether the target importance stated by the developers is actually attainable by appropriate choice of nominal weights; we call this the ‘inverse problem’. We find that in most instances the correlation structure prevents developers from obtaining the stated importance by changing the nominal weights within the set of nonnegative numbers with sum equal to 1. These findings may offer a useful insight to users and critics of an index, and a stimulus to its developers to try alternative, possibly non-compensatory, aggregation strategies.

Our proposed measure of importance is also in line with current practice in Sensitivity Analysis. Recently, some of the present authors proposed a global sensitivity analysis approach to test the robustness of a composite indicator, see Saisana et al. (2005, 2011); this approach performs an error propagation analysis of all sources of uncertainty which can affect the construction of a composite indicator. This analysis might be called ‘invasive’ in that it demands all sources of uncertainty to be modeled explicitly, e.g. by assuming alternative methods to impute missing values, different weights, different aggregation strategies; the method may also test the effect of including or excluding individual variables from the index.

In contrast, the approach suggested in this paper is non-invasive, because it does not require explicit modeling of uncertainties. The proposed measure also requires minimal assumptions, in the sense that it exists whenever second moments exist. Moreover, it takes the data correlation structure into account. When this analysis is performed by the developers themselves, it adds to the understanding – and ultimately to the quality, of the index. When performed ex-post by a third party on an already developed index, this procedure may reveal un-noticed features of the composite indicator.

The paper is organized as follows: the rest of Section 1 reports a motivating example and discusses related work. Section 2 describes linear composite indicators. Section 3 defines the main effects and discusses their estimation. It also defines a discrepancy statistic between main effects and nominal weights. Finally it discusses the inversion of the map from nominal weights to main effects. Section 4 presents detailed results for six indices: the 2009 Human Development Index (2009 HDI), the Academic Ranking of World Universities by Shanghai s Jiao Tong University (ARWU), the university ranking by the Times Higher Education Supplement (THES), the 2010 Human Development Index (2010 HDI), the Index of African Governance (IAG) and the Sustainable Society Index (SSI). Section 5 contains a discussion and conclusions. A solution to the inverse problem is reported in the Appendix.

1.1 Motivating example

In weighted arithmetic averages, nominal weights are communicated by developers and perceived by users as a form of judgement of the relative importance of the different variables, including the case of equal weights where all variables are assumed to be equally important. When using ‘budget allocation’, a strategy to assign weights, experts are given a number of tokens, say , and asked to apportion them to the variables composing the index, assigning more tokens to more important variables. This is a vivid example of how weights are perceived and used as measures of importance. However, the relative importance of variables depends on the characteristics of their distribution (after normalization) as well as their correlation structure, as we illustrate with the following example. This gives rise to a paradox, of weights being perceived by users as reflecting the importance of a variable, where this perception can be grossly off the mark.

Consider a University Dean who is asked to evaluate the performance of faculty members, giving equal importance to indicators of publications , of teaching and of office hours and administrative work . Hence she considers an equally-weighted index, , and she employs in order to measure the association between the index and each of the variables ex post.

We consider two different situations, which illustrate the influence of variances and of correlations of the variables on the performance of faculty members. In both situations, we let the variables , , be jointly normally distributed with mean zero. First assume that the variance of is equal to while and have unit variances, and that the variables are uncorrelated; the value 7 is chosen here in order to make the variance of equal to 1. We then find

which implies that the importance (as measured by ) of the variables and relative to is equal to . This shows how variances can greatly affect this measure of importance. We conclude that the Dean needs to do something about the indicators’ variances before computing the index.

Changing the weights from to , where and is the variance of would compensate for unequal variances; this corresponds to standardizing indicators before aggregation. In current practice, composite indicators builders prefer to normalise indicators before aggregation, for instance dividing by the highest score. Going back to the Dean’s example, the yearly number of administration hours can be divided by the total number of hours within a year, delivering as the fraction of administration hours. We remark that, in general, normalised scores present different variances.

Consider next the situation where , , are standardized, i.e. have all unit variances. Assume also that the correlations are all equal to zero, except . Simple algebra shows that

i.e. that the importance of indicators and is the same; this is a general property of standardized indicators. Note that the importance of indicators and is greater that the one of , because . Taking for instance , one finds

One may well imagine a faculty member looking at the relative importance of with respect to , complaining that research has become dispensable, because – although the index’s formula seems to suggest that all variables are equally important – in fact teaching is valued more than publications by a factor of 3. In this second situation, even if the Dean has standardized the variables measuring publications , teaching and administration , the last two have a higher influence on the faculty performance indicator due to their correlation.

This example describes different situations which generate the paradox. The occurrence of different variances is one such situation; this is a problem also in practice, because usually individual indicators are normalized to be between 0 and 1 or 0 and 100, and hence they have different variances in general. Also when correcting for different variances using standardized indicators, however, the paradox can be generated by correlations. This is of practical concern as well, because different individual indicators are usually correlated.

The paradox illustrated by the preceding example equally applies when the index’s architecture is made of pillars, each pillar aggregating a subset of variables. An hypothetical sustainability index could have environmental, economic, social and institutional pillars, and equal weights for these four pillars would flag the developers’ belief that these dimensions share the same importance. Still one of the four pillars with a weighting in principle of could contribute little or nothing to the index, e.g. because the variance of the pillar is comparatively small and/or the pillar is not correlated to the remaining three. A case study of this nature is discussed later in the present work.

1.2 Related work

The connection of the present paper with global sensitivity analysis has been discussed above. A related approach to measure variable importance in linear aggregations is the one of ‘effective weights’, introduced in the psychometric literature by Stanley and Wang (1968), Wang and Stanley (1970). The effective weight of a variable is defined as the covariance between and the composite indicator divided by its variance, i.e. . The same approach has been employed in recent literature in global sensitivity analysis, see e.g. Li et al. (2010).

Effective weights are, however, not necessarily positive, and hence they make an improper apportioning of the variance : cannot be interpreted as a ‘bit’ of variance. On the contrary, the measure of importance proposed in this paper (i.e. Pearson’s correlation ratio) is always positive and can be interpreted as the fractional reduction in the variance of the index that could be achieved (on average) if variable could be fixed. also fits into an ANOVA variance decomposition framework, see Saltelli (2002) for a discussion.

Moreover, effective weights assume that the dependence structure of the variables is fully captured by their covariance structure, as in linear regression. As we show in the following, the relation between the index and its components may well be nonlinear, and the measure of importance proposed in this paper extends to this case as well. The case-studies reported in Section 4 show that nonlinearity is often the rule rather than the exception. In the case of a linear relation between and , our measure reduces to , the square of , used in the example above; hence in this case, the present approach leads to a simple transformation of the effective weights.

For some indices, such as the Product Market Regulation Index (see Nicoletti et al. (2000)), Principal Component Analysis (PCA) has been used to select aggregation weights. PCA chooses weights that maximize (minimize) the variance of the index, and hence weights do not reflect the normative aspects of the definition of the index. Consequently, weights are difficult to interpret and to communicate, and as a result the use of PCA in this context is not widespread. The same Product Market Regulation Index moved from the use of PCA to a simpler and more transparent technique for linear aggregation after a statistical analysis of the implications of such a change Nardo (2009).

2 Weights and importance

Consider the case of a composite indicator calculated as a weighted arithmetic average of variables

| (1) |

where is the normalized score of individual (e.g., country) based on the value of variable , and is the nominal weight assigned to variable . The most common approach is to normalize original variables, see Bandura (2008), by the min-max normalisation method

| (2) |

where and are the upper and lower values respectively for the variable ; in this case all scores vary in . Here we indicate the transformation (2) as ‘normalisation’; the normalised variables in (2) are denoted as . We let and indicate their expectation and variance respectively. In the following, we replace and by and respectively, unless needed for clarity.

Observe that the normalisation (2) implies a fixed scale of the individual indicators; this is useful for instance for comparability in repeated waves of the same index. However, normalisation does not imply any standardization of different variables, which hence have different means and variances in general.

A popular alternative to the min-max normalization in (2) is given by standardization

| (3) |

where and are the mean and variances of the original variables . When standardized, all have the same mean and variance, , for all , removing one source of heterogeneity among variables. However, standardization does not affect the correlation structure of the variables (or ). Both transformations (2) and (3) are invariant to the choice of unit of measurement of , see (Hand, 2009, Chapter 1).

While standardization may appear a better approach than normalization, statistically, there are advantages and disadvantages of both. For example standardization may be expected not to work so well when the distribution is very skewed or long tailed. Moreover it does not enhance comparison across different waves of the same aggregate indicator over the years, if the mean and variances used in (3) change over time. Also one cannot achieve both standardization and normalization at the same time through a linear transformation of . This implies that index developers suffer the unwanted disadvantages of the chosen transformation.

Whatever the transformation, in the following we denote the column vector of scores of unit as and indicate by and the corresponding vector of means and the implied variance-covariance matrix. The weight, , attached to each variable, , in the aggregate is meant to appreciate the importance of that variable with respect to the concept being measured. The vector of weights is selected by developers on the basis of different strategies, be those statistical, such as PCA, or based on expert evaluation, such as analytic hierarchy process, see Saaty (1980, 1987).

In what follows we indicate by the target relative importance of indicators and . When this is not explicitly stated, the ratios can be taken to be the ‘revealed target relative importance’. In fact is a measure of the substitution effect between and , i.e. how much must be increased to offset or balance a unit decrease in , see Decancq and Lugo (2010). For simplicity of notation and without loss of generality, we assume that the maximal weight is assigned to indicator 1, i.e. that for , and we consider .

Note that the previous discussion applies to pillars as well as to individual variables, where a pillar is defined as an aggregated subset of variables, identified by the developers as representing a salient – possibly latent, or normative – dimension of the composite indicator.

3 Measuring importance

3.1 Measures of importance

In this paper we propose a variance-based measure of importance. We note that

| (4) |

where, if (3) is used, and the diagonal elements of are equal to 1; here we have dropped the subscript in for conciseness. In the following, we focus attention on the variance term.

Following Pearson (1905), we consider the question ‘what would be the average variance of , if variable were held fixed?’ This question leads to consider

where is defined as the vector containing all the variables in except variable . Owing to the well known identity

we can define the ratio of to as a measure of the relative reduction in variance of the composite indicator to be expected by fixing a variable, i.e.

| (5) |

The notation reflects the use of this measure as a first order sensitivity measure (also termed ‘main effect’) in sensitivity analysis, see Saltelli and Tarantola (2002). The notation reflects the original notation used in Pearson (1905); he called it ‘correlation ratio ’.

The conditional expectation in the numerator of (5) can be any nonlinear function of ; in fact , where the latter conditional expectations may be linear or nonlinear in . For the connection of to global sensitivity analysis see Saltelli et al. (2008).

In the special case of linear in , we find that reduces to , where is the product-moment correlation coefficient of the regression of on . In fact, it is well known that when is linear, i.e. , it coincides with the projection of on , which implies that , see e.g. Wooldridge (2010). Hence has the form and one finds .

A further special case corresponds to linear and made of uncorrelated components. We find and so . The main difference between the uncorrelated and the correlated case is that in the former because , while for the latter might well exceed one, see e.g. Saltelli and Tarantola (2002). We note that in general can still be high also when is low, e.g. in case of a non-monotonic U-shaped relationship for . Hence in general needs to be estimated in a nonparametric way, see Section 3.2.

As these special cases illustrate, is quadratic measure in terms of the weights for linear aggregation schemes (1); this follows from its definition as a variance-based measure. The main effect is an appealing measure of importance of a variable (be it indicator or pillar) for several reasons:

-

•

it offers a precise definition of importance of a variable, that is ‘the expected fractional reduction in variance of the composite indicator that would be obtained if that variable could be fixed’;

-

•

it can be applied when relationships between the index and its components are linear or nonlinear. Such nonlinearity may be the effect of nonlinear aggregation (e.g. Condorcet-like, see Munda (2008)) and/or of nonlinear relationships among the single variables. It can be used regardless of the degree of correlation between variables. Unlike the Pearson or Spearman correlation coefficients, it is not constrained by assumptions of linearity or monotonicity;

-

•

it is not invasive, that is no changes are made to the composite indicator or to the correlation structure of the indicators, unlike e.g. the error propagation analysis presented in Saisana et al. (2005). While the error propagation can be considered as a stress test of the index, the present approach is a test of its internal coherence.

3.2 Estimating main effects

In this subsection we consider estimating the main effects and focus on the 2009 HDI to illustrate our approach. In Section 4 we describe the six case-studies of our approach in detail.

In sensitivity analysis, the estimation of is an active research field. can be estimated from design points: Sobol’ (1993); Saltelli (2002); Saltelli et al. (2010); Fourier analysis: Tarantola et al. (2006); Plischke (2010); Xu and Gertner (2011), or others. Many nonparametric estimators can be used to estimate , such as State Dependent Regression: Ratto et al. (2007); Ratto and Pagano (2010).

In the present work we employ a nonparametric, local-linear, kernel regression to estimate , and then use it in (5) to estimate , replacing the variances in the numerator and denominator with the corresponding sample variances, i.e. using , where , , and is the estimate of .

Local linear kernel estimators achieve automatic boundary corrections and enjoy some typical optimal properties, that are superior to Nadaraya-Watson kernel estimators, see Ruppert and Wand (1994) and reference therein. As a result, local linear kernel smoother are often considered the standard nonparametric regression method, see e.g. Bowman and Azzalini (1997).

The local linear nonparametric kernel regression is indexed by a bandwidth parameter , which is usually held constant across the range of value for . For large , the local linear nonparametric kernel regression converges to the linear least squares fit. This allows us to interpret as the deviation from linearity; it suggests that we investigate the sensitivity of the estimation of to variation in the bandwidth parameter . In order to make this dependence explicit we write to indicate the value of obtained by a local-linear kernel regression with bandwidth parameter . In the application we use a Gaussian kernel.

The choice of the smoothing parameter can be based either on cross-validation (CV) principles (see Bowman and Azzalini (1997)) or on plug-in choices for the smoothing parameter, such as the ones proposed in Ruppert et al. (1995). We describe these approaches in turn, starting with cross validation. Let indicate the local linear nonparametric kernel estimate for at based on all observations, and let be the same applied to all data points except for the one with index ; then the least-squares Cross Validation criterion for variable is defined as

The optimal value for the CV criterion is given by the bandwidth corresponding to the minimum of . In practice, a grid of possible values for is considered, and the minimum of the function is found numerically. In the application we chose the grid of values as follows: we defined a regular grid of 50 values for in the range from 0.1 to 5. The values for were then obtained as , for index-specific constants and ; the resulting set of values in this grid is denoted in what follows.

The default values for indices with range from 0 to 10 or 100 were , , so that ; for indices with range from 0 to 1, (namely 2009 and 2010 HDI ), we chose , , so that . In some cases CV attains its minimum at the right end of the grid ; This happened both for ARWU and THES, see Table 1, as well as for IAG and SSI, see Table 3, where the digits in braces refer to the subscript of the variables. In these cases, in practice, a linear regression fit would not be worse than the fit of the local linear kernel estimator, according to the CV criterion.

In the implementation of the CV criterion, when a local linear kernel regression implied a row of the smoothing matrix with numerical ‘divisions by zero’, we replaced it with a local mean (Nadaraya-Watson) estimator. When also the latter would imply numerical divisions by zero, we replaced the row of the smoothing matrix with a sample leave-one-out mean.

An alternative choice of bandwidth is given by plug-in-rules. One popular choice is given by the ‘direct plug-in’ selector introduced by Ruppert et al. (1995), which minimizes the Asymptotic Mean Integrated Squared Error for the local linear Gaussian kernel smoother, on the basis of the following preliminary estimators. Let , where is the -th derivative of . The range of is partitioned into blocks and a quartic is fitted on each block. Using this estimation, an estimate for is found, along with an estimator for the error variance . These estimates are then used to obtain a plug-in bandwidth , which is used in a local cubic fit to estimate and to obtain a different plug-in bandwidth . The bandwidth is then used in a final local linear kernel smoother to estimate , which is fed into the final formula for , along with the previous estimate of . The choice of , the number of blocks, is obtained minimizing Mallow’s criterion over the set , where .

In the application we chose as suggested by Ruppert et al. (1995); in case of numerical instabilities, we decreased to 4. Moreover we performed an -trimming in the estimation of and with . Because the choice of bandwidth can be affected by values at the end of the -range, we only considered pairs of observations for which in the choice of bandwidth, both for the criterion and the criterion.

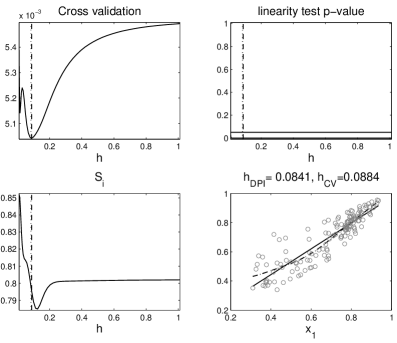

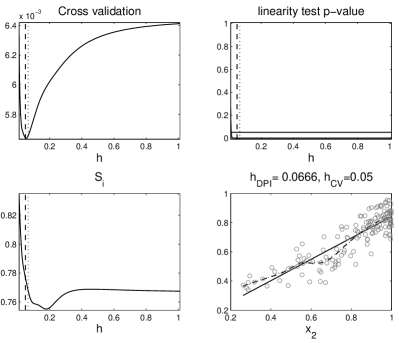

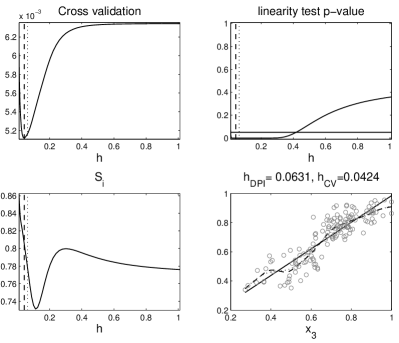

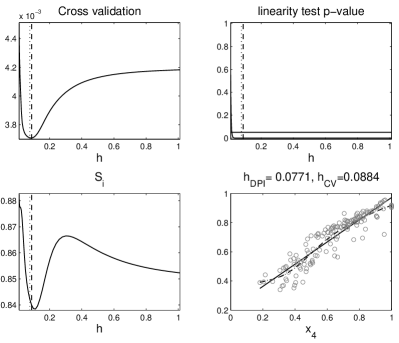

The resulting choice of bandwidth was sometimes very close to , as in the case for the 2009 HDI, which is depicted in Fig. 1-4, where each figure refers to one of the four indicators used in the construction of the 2009 HDI. Fig. 1 refers to the indicator (life expectancy), and contains four panels, which report – counterclockwise from upper-right – the -value of the linearity test introduced below, the cross validation criterion , the measure and the regression cross plot. The first 3 graphs show functions of the bandwidth parameter , while the final one has the values of on the horizonal axis. Fig. 2-4 have the same format, and refer to indicators and .

Tables 1 and 3 report the selected values of and for the 2009 HDI and for the other 5 indices, described in detail in Section 4. It can be seen that the values of sometimes differed from by several orders of magnitude.

As in many other contexts, in the estimation of main effects the linear case is a relevant reference model, and one would like to address inference on and on the possible linearity of jointly. To this end we implemented the test for linearity proposed in Bowman and Azzalini (1997, Chapter 5). The fit of the linear kernel smoother can be represented as , where the matrix depends on all values , . A test of linearity can be based on the statistic, , that compares the residual sum of squares under the linearity assumption with the one corresponding to the local linear kernel smoother . Letting indicate the value of the statistic, the -value of the test is computed as the probability that where is a vector of independent standard Gaussian random variables and with , and equal to the linear regression design matrix, with first column equal to the constant vector and the second column equal to the values of , .

Bowman and Azzalini (1997) suggest approximating the quantiles of the quadratic form with the distribution of , where , and are obtained by matching moments of the quadratic form and the distribution; here represents a distribution with degrees of freedom. We implemented this approximation; the upper right panels in Fig. 1-4 report the resulting -values of the test as a function of for the 2009 HDI. It can be seen for some variable the test rejects the linearity hypothesis for all values of in the grid , and for some other pairs the test rejects only for a subset of . In a few other pairs, the test never rejects for all . Results for the linearity test are reported in Tables 1 and 3 for selected values of , both the 2009 HDI and for 5 other indices, described in detail in Section 4.

To show sensitivity of the main effects to the smoothing parameter , we also computed the index as a function of . We also recorded the min and max values obtained for varying in ; we denote these values as , . We report the plot of as a function of in the lower left panels of Fig. 1-4.

3.3 Comparing weights and main effects

In this section we compare revealed or target relative importance measures with the relative main effects . First notice that, in the independent case, , so that . When the variables are standardized, all and hence . The relative main effects do not reduce to , except in the homoskedastic case () when the nominal weights are equal, (), so that . In the general case, depends on and in a more complicated way, and hence there is no reason, a priori, to expect to coincide with .

One can compare how the effective relative importance deviates from the (revealed) target relative importance ; to this end we define the maximal discrepancy statistic as

| (6) |

In the case of revealed target relative importance, recall that is assumed to be the highest nominal weight . In the case when more than one variable has maximum weight equal to , we selected as reference variable the one with maximum value for with , i.e. where is the DPI bandwidth choice for indicator .

The higher the value of , the more discrepancy there is between relative target importance and the corresponding relative main effects. In we have chosen to capture the discrepancy by focusing on the maximal deviation; alternatively one can consider any absolute power mean, -divergence function or distance between the (un-normalized) distributions and . For simplicity, in the following we indicate these distributions used in the comparison as and .

Because depends on the choice of bandwidth parameters in the estimation of , we also calculated bounds on the variation of obtained by varying . Specifically, we computed comparing with choosing as either equal to or , considering all possible combinations. For instance, with , we considered , , and . Within the distribution of values of obtained in this way, we recorded the minimum and the maximum, denoted as . Table 5 reports the for equal to and in the linear case, along with the values , , which provide a measure of sensitivity of with respect to the choice of bandwidth .

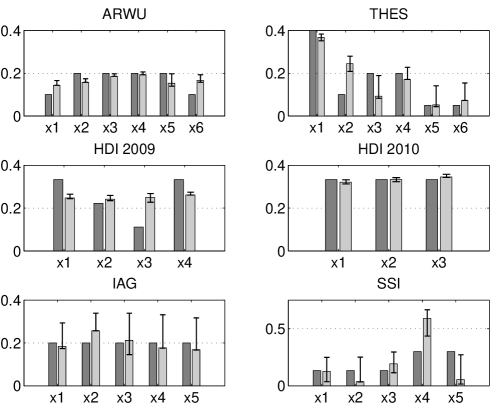

To compare the values with the weights graphically, in Fig 5 we re-scale the values to have sum equal to one, considering with , which we call ‘normalized ’. In order to visualise bounds for , we plot bars with endpoints equal to and ; these bars inform on the sensitivity of with respect to the variation of the bandwidth parameter .

3.4 Reverse-engineering the weights

This section discusses when it is possible to find nominal weights that imply pre-determined, given values for the relative main effects ; here we indicate the target relative importance to differentiate it from of the previous sections. This reverse-engineering exercise can help developers of composite indicators to anticipate criticism by enquiring if the stated relative importance of pillars or indicators is actually attainable.

For the purpose of this inversion, we consider the case of linear in ; in this case coincides with , the square of Pearson’s product moment correlation coefficients between and . The linear case can be seen as a first order approximation to the nonlinear general case; this choice is motivated by the fact that one can find an exact solution to the inversion problem of the map from to when one allows weights also to be negative. One expects that the reverse-engineering formula in the linear case to be indicative of the one based on a non-linear approach, where the latter would be computationally more demanding.

We wish to find a value for the vector of nominal weights such that equals pre-selected target values , for . We call this the ‘inverse problem’. The weights are chosen to sum to 1, but they are allowed also to be negative; this choice makes the inverse problem solvable, and in the Appendix we show that it has a unique solution, given by

| (7) |

where is a vector with -th entry equal to and is a -vector of ones.

Because the solution to this inverse problem is unique, if some of the weights in (7) are negative, it means that a solution to the inverse problem with all positive weights does not exist, and hence the targets are not attainable, owing to the data covariance structure. This can help designers to re-formulate their targets to make them attainable, and the stakeholders involved in the use of the composite indicator to evaluate wether the individual indicators can have the stated importance by an appropriate choice of weights.

2008 ARWU Alumni winning Nobel 0.88 3.43 0.71 198 Staff winning Nobel 0.59 3.13 0.27 135 Highly cited res. 0.00 1.15 0.00 424 Art. in Nature and Science 9.05 0.00 1.78 0.00 494 Art. in Science and Social CI 2.94 0.00 2.26 0.00 503 Academic perf. (size adj) 1.74 0.00 2.12 0.00 503 2008 THES Academic review 4.46 0.00 1.74 0.00 400 Recruiter review 5.81 0.00 2.62 0.00 400 Teacher/Student ratio 4.46 0.07 4.76 0.08 399 Citations per faculty 0.04 2.44 0.20 400 International staff 6.81 0.04 2.97 0.22 398 International students 0.18 4.13 0.65 399 2009 HDI Life expectancy 0.09 0.00 0.08 0.00 142 Adult literacy 0.05 0.00 0.07 0.00 142 Enrolment in education 0.04 0.00 0.06 0.00 142 GDP per capita 0.09 0.00 0.08 0.00 142

4 Case studies

In this section we apply the statistical analysis that was described in Section 3 to the six composite indicators. In Section 4.1 we consider the three indices for which aggregation was performed at indicator level and in Section 4.2 we consider the three indices for which aggregation was performed at the pillar level.

4.1 Importance at the indicator level

We consider the Human Development Index (HDI) and two well known composite indicators of university performance: the Academic Ranking of World Universities by Shanghai’s Jiao Tong University (ARWU) and the one associated to the UK’s Times Higher Education Supplement (THES).

2008 ARWU Alumni winning Nobel 0.10 0.64 0.65 0.67 0.65 0.76 Staff winning Nobel 0.20 0.72 0.72 0.73 0.72 0.80 Highly cited res. 0.20 0.81 0.85 0.87 0.85 0.90 Art. in Nature and Science 0.20 0.87 0.88 0.88 0.88 0.94 Art. in Science and Social CI 0.20 0.63 0.70 0.70 0.64 0.90 Academic perf. (size adj) 0.10 0.71 0.76 0.75 0.72 0.88 2008 THES Academic review 0.40 0.77 0.81 0.82 0.78 0.85 Recruiter review 0.10 0.45 0.54 0.54 0.46 0.62 Teacher/Student ratio 0.20 0.19 0.21 0.20 0.18 0.42 Citations per faculty 0.20 0.38 0.38 0.41 0.38 0.50 International staff 0.05 0.10 0.12 0.12 0.10 0.31 International students 0.05 0.16 0.16 0.17 0.16 0.34 2009 HDI Life expectancy 0.33 0.80 0.80 0.80 0.78 0.85 Adult literacy 0.22 0.77 0.78 0.77 0.76 0.83 Enrolment in education 0.11 0.77 0.81 0.78 0.73 0.86 GDP per capita 0.33 0.85 0.84 0.84 0.84 0.88

University Ranking

The ARWU, Center for World-Class Universities (2008), summarizes quality of education, quality of faculty, research output and academic performance of world universities using six indicators: the number of alumni of an institution having won Nobel Prizes or Fields Medals (weight of 10%), the number of Nobel or Fields laureates among the staff of an institution (weight of 20%), the number of highly cited researchers (weight of 20%), the number of articles published in Nature or Science, Science Citation Index Expanded and Social Sciences Citation Index (weight of 40%), and finally the academic performance measured as the weighted average of the above five indicators divided by the number of full-time equivalent academic staff (weight of 10%). The raw data are normalized by assigning to the best performing institution a score of 100 and all other institutions receiving a score relative to the leader. The ARWU score is a weighted average of the six normalized indicators, which is finally re-scaled to a maximum of 100. The six indicators have moderate to strong correlations in the range from 0.48 to 0.87 and an average bivariate correlation of 0.68.

The THES, Times Higher Education Supplement (2008), summarizes university features related to research quality, graduate employability, international orientation and teaching quality using six indicators: the opinion of academics on which institutions they consider to be the best in the relevant field of expertise (weight of 40%), the number of papers published and citations received by research staff (weight of 20%), the opinion of employers about the universities from which they would prefer to recruit graduates (weight of 10%), the percentage of overseas staff at the university (weight of 5%), the percentage of overseas students (weight of 5%), and finally the ratio between the full-time equivalent faculty and the number of students enrolled at the university (weight of 20%). Raw data are standardized. The standardized indicator scores are then scaled by dividing by the best score. The THES score is the weighted average of the six normalized indicators, which is finally re-scaled to a maximum of 100. The six indicators have very low to moderate correlations that range from 0.01 to 0.64 and a low average bivariate correlation of 0.24.

Results for ARWU and THES are given in Tables 1-2 and 5. The first two panels of Table 1 provide the bandwidth selection results for ARWU and THES; the corresponding panels of Table 2 give estimates of the importance measure for different choices of bandwidth. The first two lines in Table 5 give the maximum discrepancy statistic for ARWU and THES. Finally the two upper graphs in Fig. 5 summarize the comparison between target and actual relative importance of indicators. For ARWU the main effects are more similar to each other than the nominal weights, i.e. ranging between and (normalised values to unit sum, cross validation estimates) when weights should either be or .

The situation is worse for THES, where the combined importance of peer review based variables (recruiters and academia) appears larger than stipulated by developers, indirectly supporting the hypothesis of linguistic bias at times addressed to this measure (see e.g. Saisana et al. (2011) for a review). Further for THES the ‘teachers to student ratio’, a key variable aimed at capturing the teaching dimension, is much less important than it should be when comparing normalized (, cross validation estimate) with the nominal weight ().

Overall, there is more discrepancy between the nominal weights assigned to the six indicators and their respective main effects in THES () than in ARWU (), cross validation estimates. Comparing this result with the conclusions in Saisana et al. (2011), we can see the value-added of the present measure of importance. In that paper we could not draw a judgement about the relative quality of THES with respect to ARWU. The main effects used here allow us to say that – leaving aside the different normative frameworks about which no statistical inference can be made – ARWU is statistically more consistent with its declared targets than THES.

When considering the sensitivity of values to the choice of bandwidths , one can see that the range is slightly shorter for ARWU () than for THES (); this implies that ARWU is slightly less sensitive than THES to the choice of bandwidths . Note however that the two ranges overlap, so that there are choice of bandwidths for which the ordering of values is reversed. This, however, does not happen at the values and .

The hypothesis of linearity is not rejected for two indicators for ARWU and for four indicators for THES, when evaluating the tests at and . The two indicators for ARWU are those with the highest proportion of values equal to 0, which were discarded in the choice of bandwidth; the number of valid cases are 198 and 135 respectively. This may reflect the fact that it is more difficult to reject linearity with smaller samples. The indicators used in THES instead do not have so many zero values; also here however, one finds that is approximately linear for 4 indicators.

2010 HDI Life expectancy 0.08 0.00 0.07 0.00 169 Education 0.02 0.09 0.06 0.21 169 GDP per capita 0.05 0.00 0.06 0.00 169 IAG Safety and security 17.69 0.15 3.31 0.45 53 rule of law and corruption 0.30 4.75 0.94 53 part. and human rights 4.89 0.08 2.85 0.41 53 Sust. economic opportunity 22.14 0.09 4.21 0.51 53 Human development 0.17 3.42 0.87 53 SSI Personal development 0.69 0.00 0.37 0.00 151 Healthy environment 0.41 0.49 0.69 151 Well-balanced society 0.69 0.00 0.42 0.01 151 Sustainable use of resources 0.30 0.00 0.30 0.00 150 Sustainable World 0.86 0.00 0.38 0.01 151

The Human Development Index 2009

The HDI, see United Nations Development Programme (2009), summarizes human development in countries based on four indicators: a long healthy life measured by life expectancy at birth (weight of 1/3), knowledge measured by adult literacy rate (weight of 2/9) and combined primary, secondary and tertiary gross enrollment ratio (weight of 1/9), and a decent standard of living measured by the GDP per capita (weight of 1/3). Raw data in the four indicators are normalized by using the min-max approach to be in [0, 1]. The 2009 HDI score is the weighted average of the four normalized indicators. Because data on Adult literacy rate was missing for several countries, we analyzed data only for the countries without missing data; this gave a total of 142 countries. The four indicators present strong correlations that range from 0.70 to 0.81 and an average bivariate correlation of 0.74.

Nominal weights and estimates of the main effects are given in the last panel of Table 2, while the choice of bandwidth is given in Table 1. The maximum discrepancy is given in Table 5 and a graphical comparison of nominal weights and estimates of the main effects is provided in Fig. 5. Table 1 reports evidence on the choice of bandwidth and the -values for the linearity test, at the values and of the smoothing parameter .

Both the main effects and the Pearson correlation coefficients reveal a relatively balanced impact of the four indicators ‘life expectancy’, ‘GDP per capita’, ‘enrolment in education’, and ‘adult literacy’ on the variance of the HDI scores, with the adult literacy being slightly less important. It would seem that HDI depends more equally from its four variables than the weights assigned by the developers would imply. For example, if one could fix adult literacy the variance of the HDI scores would on average be reduced by (CV estimate), whereas by fixing the most influential indicator, GDP per capita, the variance reduction would be on average.

One might suspect that it was precisely the developers’ intention, when assigning nominal weights and to these two variables respectively, to make them equally important on the basis of the measure; however this is is not stated explicitly in the index documentation report United Nations Development Programme (2009). Overall, there is considerable discrepancy between the nominal weights assigned to the four indicators and their respective main effects in 2009 HDI ().

The analysis of the 2009 HDI illustrates vividly that assigning unequal weights to the indicators is not a sufficient condition to ensure unequal importance. Although the 2009 HDI developers assigned weights varying between and , all four indicators are roughly equally important. The scatterplots in Fig. 1-4 help visualize the situation. In cases like this, where the variables are strongly and roughly equally correlated with the overall index, each of them ranks the countries roughly equally, and the weights are little more than cosmetic.

4.2 Importance at the pillar level

The issue of weighting is particularly fraught with normative implications in the case of pillars. As mentioned above, pillars in composite indicators are often given equal weights on the ground that each pillar represents an important – possibly normative – dimension which could not and should not be seen to have more or less weight than the stipulated fraction. The discrepancy measure presented here can be of particular relevance and interest to gauge the quality of a composite indicator with respect to this important assumption. Here we consider the 2010 version of the HDI, the Index of African Governance (IAG) and the Sustainable Society Index (SSI).

2010 HDI Life expectancy 0.33 0.82 0.84 0.84 0.81 0.86 Education 0.33 0.86 0.87 0.86 0.84 0.89 GDP per capita 0.33 0.90 0.90 0.90 0.89 0.93 IAG Safety and security 0.20 0.52 0.54 0.63 0.51 0.87 rule of law and corruption 0.20 0.77 0.76 0.78 0.76 1.00 part. and human rights 0.20 0.44 0.63 0.68 0.43 1.00 Sust. economic opportunity 0.20 0.52 0.52 0.56 0.52 0.98 Human development 0.20 0.50 0.50 0.55 0.49 0.94 SSI Personal development 0.13 0.05 0.14 0.17 0.04 0.27 Healthy environment 0.13 0.04 0.04 0.07 0.04 0.27 Well-balanced society 0.13 0.13 0.21 0.21 0.12 0.32 Sustainable use of resources 0.30 0.48 0.64 0.64 0.47 0.72 Sustainable World 0.30 0.02 0.06 0.10 0.02 0.29

The Human Development Index 2010

In this section we analyze the 2010 version of the HDI at the pillar level, covering 169 countries. From the methodological viewpoint the main novelty in this version of the index is the use of a geometric – as opposed to an arithmetic – mean, in the aggregation of the three pillars. The three pillars cover health (life expectancy at birth) , education and income (gross national income per capita) . Education is the combination of two variables, namely mean years of schooling and expected years of schooling, see United Nations Development Programme (2010). The HDI index is computed as

where all three dimensions have equal weights. The reason for this change of aggregation scheme is to introduce an element of ‘imperfect substitutability across all HDI dimensions’, i.e. to reduce the compensatory nature of the linear aggregation, see (United Nations Development Programme, 2010, p. 216).

ARWU 0.36 0.36 0.31 0.26 0.50 THES 0.41 0.42 0.34 0.29 0.55 2009 HDI 0.59 0.63 0.57 0.50 0.69 2010 HDI 0.06 0.07 0.09 0.03 0.13 IAG 0.29 0.34 0.42 0.13 0.57 SSI 0.85 0.91 0.95 0.38 0.98

Nominal weights and estimates of the main effects are given in the first panel of Table 4, while the choice of bandwidth is given in Table 3. The maximum discrepancy is given in row 4 of Table 5 and a graphical comparison of nominal weights and estimates of the main effects is provided in Fig. 5.

Overall, the HDI 2010 shows very little discrepancy between the goals of equal importance of the three pillars and the main effects. In fact all three pillars have similar impact on the index variance (roughly ). Hence, in this case the relative nominal weights are approximately equal to the relative impact of the pillars’ on the index variance. Such a correspondence is of value because it indicates than no pillar impacts too much or too little the variance of the index as compared to its ‘declared’ equal importance. Compared to the other examples discussed, the 2010 HDI is the most consistent in this respect (). The linearity tests reveal that the role of education is approximately linear within the index, despite the multiplicative aggregation scheme.

In order to assess the impact of the choice of the aggregation scheme on the index balance, we also perform a counterfactual analysis of the 2010 HDI using linear aggregation of the three dimensions. We find that this choice does not affect the relative importance of dimensions, as these have comparable variances and covariances. Hence the 2010 HDI would have been balanced also under a linear aggregation scheme. This, however, does not detract from the conceptual appeal of imperfect substitutability implicit in geometric aggregation.

Index of African Governance

The Index of African Governance was developed by the Harvard Kennedy School, see Rotberg and Gisselquist (2008); for a validation study see Saisana et al. (2009). In the 2008 version of the index, 48 African countries are ranked according to five-pillars: (i) Safety and Security, (ii) Rule of Law, Transparency, and Corruption, (iii) Participation and Human Rights, (iv) Sustainable Economic Opportunity, and (v) Human Development. The five pillars are described by fourteen sub-pillars that are in turn composed of indicators in total (in a mixture of qualitative and quantitative variables). Raw indicator data were normalized using the min-max method on a scale from to . The five pillar scores per country were calculated as the simple average of the normalized indicators. Finally, the IAG scores were calculated as the simple average of the five pillar scores. The five pillars have correlations that range from 0.096 to 0.76 and average bivariate correlation of 0.45. Three pairwise correlations (involving Participation and Human Rights and either Sustainable Economic Opportunity or Human Development or Safety & Security) are not statistically significant at the 5% level.

Nominal weights and main effects are given in Table 4 and in Fig. 5, while the choice of bandwidth is reported in Table 3 and the discrepancy statistics in Table 5. The main conclusions are summarized as follows: The IAG is a good example of the situation discussed in Section 1 whereby all pillars represent important normative elements which by design should be equally important in the developers’ intention. Overall the IAG appears to be balanced with respect to four pillars that have similar impact on the index variance (roughly ), but the fifth pillar on the Rule of Law is more influential than conceptualised (, cross validation estimate). The IAG has a maximal discrepancy statistic .

The linearity tests in Table 3 suggest that there is no statistical evidence against linearity for all the five indicators. Hence one could calculate here as .

Sustainable Society Index

The Sustainable Society Index (SSI) has been developed by the Sustainable Society Foundation for 151 countries and it is based on a definition of sustainability of the Brundtland Commission (van de Kerk and Manuel, 2008). Also in this example, the five pillars of the index represent normative dimensions which are, however, considered of different importance: Personal Development (weight of 1/7), Healthy Environment (1/7), Well-balanced Society (1/7), Sustainable Use of Resources (2/7), and Sustainable World (2/7). These five pillars are described by indicators. Raw indicator data were normalized using the min-max method on a scale from 0 to 10. The five pillars were calculated as the simple average of the normalized indicators. The SSI scores were calculated as the weighted average of the five pillar scores.

One can note that the linearity test suggests that for the second pillar ‘Healthy Environment’ there is no evidence against linearity of its relation to the SSI index. The five pillars have correlations that range from to , where negative correlations between pillars are generally undesired, as they suggest the presence of trade-offs between pillars (e.g. economic performance can only come with an environmental cost). Such trade-offs within index dimensions are a reminder of the danger of compensability between dimensions.

For the Sustainable Society Index, there are notable differences between declared and variance-based importance for the five pillars. The different association between a pillar and the overall index can also be grasped visually in Fig. 5. The two pillars on ‘Sustainable use of resources’ and on ‘Sustainable World’ are meant to be equally important accordingly to the nominal weights (2/7 each), while the main effects suggest that the variance reduction obtained by fixing the former is compared to merely by fixing the latter. This strong discrepancy is due to the significant negative correlations present among the SSI pillars. Overall, the level of maximal discrepancy of the SSI is the highest of the examples discussed (). The authors and the developers of the SSI have been communicating on this issue, and the 2010 version of the SSI index appears considerably improved, see http://www.ssfindex.com/ssi/.

4.3 Reverse-engineering the weights

Applying the reverse engineering exercise described in Section 3.4 and the Appendix to our test cases (except for the case of 2010 HDI that has low maximal discrepancy between relative weights and relative importance for the three pillars, and it is not obtained by the linear aggregation scheme (1)), we find that to achieve a relative impact of the indicators (or pillars) (as measured by the square of the Pearson correlation coefficient ) that equals the relative ‘declared’ importance of the indicators, negative nominal weights are involved in all studies except for the SSI. In the case of SSI, to guarantee that the two pillars on Sustainable Use of Resources and Sustainable World are twice as important as the other three pillars, the nominal weights to be assigned to them are Personal Development (weight of 0.19), Healthy Environment (0.16), Well-balanced Society (0.07), Sustainable Use of Resources (0.16), and Sustainable World (0.41). For all other cases, the data correlation structure does not allow the developers to achieve the stated relative importance by choosing positive weights.

5 Conclusions

According to many – including some of the authors of the Stiglitz report, see Stiglitz et al. (2009) – composite indicators have serious shortcomings. The debate among those who prize their pragmatic nature in relation to pragmatic problems, see Hand (2009), and those who consider them an aberration is unlikely to be settled soon, see Saltelli (2007) for a review of pros and cons. Still these measures are pervasive in the public discourse and represent perhaps the best known face of statistics in the eyes of the general public and media.

One might muse that what official statistics are to the consolidation of the

modern nation state, see Hacking (1990), composite indicators are to the

emergence of post-modernity, – meaning by this the philosophical critique

of the exact Science and rational knowledge programme of Descartes and

Galileo, see Toulmin (1990), p. 11-12. On a practical level, it is undeniable

that composite indicators give voice to a plurality of different actors and

normative views. The authors in Stiglitz

et al. (2009) remark (p. 65):

“The second [argument against composite indicators] is

a general criticism that is frequently addressed at composite indicators,

i.e. the arbitrary character of the procedures used to weight their various

components. (…) The problem is not that these weighting procedures are

hidden, non-transparent or non-replicable — they are often very explicitly

presented by the authors of the indices, and this is one of the strengths of

this literature. The problem is rather that their normative implications are

seldom made explicit or justified.”

The analysis of this paper shows that,

although the weighting

procedures are often very explicitly presented by the authors of the

indices, the implications of these are neither fully understood, nor

assessed in relation to the normative implications.

This paper proposes a variance-based tool to measure the internal discrepancy

of a composite indicator between target and effective importance.

Our main conclusions can be summarized as follows. For transparency and simplicity, composite indicators are most often built using linear aggregation procedures which are fraught with the difficulties described in the Introduction: practitioners know that weights cannot be used as importance, while they are precisely elicited as if they were. Weights are instead measures of substitutability in linear aggregation. The error is particularly severe when a variable’s weight substantially deviates from its relative strength in determining the ordering of the units (e.g. countries) being measured.

Pearson’s correlation ratio (or main effect) that is suggested in this paper is a suitable measure of importance of a variable (be it indicator or pillar) because: i) it offers a precise definition of importance (that is ‘the expected reduction in variance of the composite indicator that would be obtained if a variable could be fixed’), ii) it can be used regardless of the degree of correlation between variables, iii) it is model-free, in that it can be applied also in non-linear aggregations, and finally iv) it is not invasive, in that no changes are made to the composite indicator or to the correlation structure of the indicators.

Because of property i) and the fact that it takes the whole covariance structure into account, the main effect can also be useful to prioritise variables on which a country or university, or whatever units are being rated, could intervene to improve its overall score. Note that the indicator with highest main effect is not necessarily the one in which the country scores the worst.

The main effects approach can complement the techniques for robustness analysis applied to composite indicators thus far seen in the literature, see e.g. Saisana et al. (2005); Organisation for Economic Co-operation and Development (2008); Saisana et al. (2011). The approach described in this paper does not need an explicit modeling of error-propagation but it is simply based on the data as produced by developers.

The discrepancy statistic based on the absolute error between ratios of the main effects and of the corresponding target relative importance provides a pragmatic answer to the research question posed in this paper. Relative main effects are variance-based, and hence they are ratios of quadratic forms of nominal weights, while target relative importance are often deduced as ratios of nominal weights. Comparing them via the discrepancy statistic is a way to compare these two importance measures, one of which is stated ex-ante as a target and the other one that is computed ex-post; this allows to see how close the two measures are in practice.

The discrepancy statistic has been effective in the six examples discussed, in that it allowed an analytic judgement about the discrepancy in the assignment of the weights in two well known measures of higher education performance ( for THES versus for ARWU), two versions of a human development index ( for the 2009 HDI and for the 2010 HDI), one index of governance ( for the IAG) and one index of sustainability ( for the SSI).

Our reverse engineering analysis shows that in most cases it is not possible to find nominal weights that would give the desired importance to variables. This can be a useful piece of information to developers, and might induce a deeper reflection on the cost of the simplification achieved with linear aggregation. Developers could thus:

-

a)

avoid associating nominal weights with importance, but inform users of the relative importance of the variables or pillars, using statistics such as those presented in this paper;

-

b)

abstain from aggregating pillars when these display important trade offs which make it difficult to give them target weights in an aggregated index;

-

c)

reconsider the aggregation scheme, moving from the linear one (which is fully compensatory) to a partially- or fully-non-compensatory alternative, such as e.g. a Condorcet-like (or approximate Condorcet) approach, where weights would fully play their role as measure of importance, see Munda (2008);

-

d)

assess different weighting strategies, so as to select the one that leads to a minimum discrepancy statistic between target weights and variables importance.

Acknowledgement

We thank, without implicating, Beatrice d’Hombres, Giuseppe Munda, the Associate Editor and two Referees for useful comments. The views expressed are those of the authors and not of the European Commission or the University of Insubria.

Appendix - Solution to the inverse problem

In the linear case, the ratio equals the ratio of squares of Pearson’s correlation coefficients ; this is a function of and of the covariance matrix of . One finds , where is the -th column of the identity matrix of order and is the -th variance on the diagonal of . We wish to make equal to a pre-selected value for all :

| (8) |

and seeks to find a solution to this problem such that nominal weight to sum to 1, i.e.

| (9) |

We show that this solution is unique and it is given by (7) in the text, where is a vector with -th entry equal to and is a -vectors of ones.

Note that by construction . One has that (8) can be written as , or, setting , as . This shows that should be selected in the right null space of . We observe that

whose right null-space is one dimensional; moreover is spanned by . Hence for a nonzero or . Substituting this expression in (9), one finds , which implies . One hence concludes that the weights that satisfy (8) are given by (7), and that they are unique.

References

- Agrast et al. (2010) Agrast, M. D., J. C. Botero, and A. Ponce (2010). Rule of law index 2010. Technical report, World Justice Project, Washington, DC, http://worldjusticeproject.org/.

- Balinski and Laraki (2010) Balinski, M. and R. Laraki (2010). Majority Judgment. Measuring, ranking and electing. MIT Press.

- Bandura (2008) Bandura, R. (2008). A survey of composite indices measuring country performance: 2008 update. Technical report, United Nations Development Programme - Office of Development Studies, New York.

- Billaut et al. (2010) Billaut, J. C., D. Bouyssou, and P. Vincke (2010). Should you believe in the Shanghai ranking? Scientometrics 84, 237–263.

- Bird et al. (2005) Bird, S. M., D. Cox, V. T. Farewell, H. Goldstein, T. Holt, and P. C. Smith (2005). Performance indicators: good, bad, and ugly. J. R. Statist. Soc. A 168, 1–27.

- Bowman and Azzalini (1997) Bowman, A. W. and A. Azzalini (1997). Applied Smoothing Techniques for Data Analysis: A Kernel Approach with S-Plus Illustrations. Oxford: Clarendon Press.

- Boyssou et al. (2006) Boyssou, D., T. Marchant, M. Pirlot, and A. Tsoukiàs (2006). Evaluation and Decision Models with Multiple Criteria: Stepping Stones for the Analyst. Springer.

- Center for World-Class Universities (2008) Center for World-Class Universities (2008). Academic ranking of world universities - 2008. Technical report, Institute of Higher Education, Shanghai Jiao Tong University, China, http://www.arwu.org/.

- Decancq and Lugo (2010) Decancq, K. and M. Lugo (2012). Weights in multidimensional indices of well-being: An overview. Econometric Reviews in press, DOI: 10.1080/07474938.2012.690641.

- Freedom House (2011) Freedom House (2011). Freedom of the press 2011. Technical report, Freedom House, Wasghington DC, http://www.freedomhouse.org.

- Hacking (1990) Hacking, I. (1990). The Taming of Chance. Cambrige University Press.

- Hand (2009) Hand, D. (2009). Measurement Theory and Practice: The World Through Quantification. Wiley.

- Hendrik et al. (2008) Hendrik, W., C. Howard, and A. Maximilian (2008). Conwsequences of data error in aggregate indicators: Evidence from the human development index. Technical report, Department of Agricultral and Resource economics, UCB, UC Berkeley.

- Leckie and Goldstein (2009) Leckie, G. and H. Goldstein (2009). The limitations of using school league tables to inform school choice. J. R. Statist. Soc. A 172, 835–851.

- Li et al. (2010) Li, G., H. Rabitz, P. Yelvington, O. Oluwole, F. Bacon, C. Kolb, and J. Schoendorf (2010). Global sensitivity analysis for systems with independent and/or correlated inputs. Journal of Physical Chemistry 114,, 6022.

- Munda (2008) Munda, G. (2008). Social Multi-Criteria Evaluation for a Sustainable Economy. Berlin Heidelberg: Springer-Verlag.

- Munda and Nardo (2009) Munda, G. and M. Nardo (2009). Non-compensatory/non-linear composite indicators for ranking countries: a defensible setting. Applied Economics 41, 1513–1523.

- Nardo (2009) Nardo, M. (2009). Product market regulation: Robustness and critical assessment 1998-2003-2007 - How much confidence can we have on PMR ranking?, EUR 23667. Technical report, European Commission, JRC-IPSC, Ispra, Italy.

- Nicoletti et al. (2000) Nicoletti, G., S. Scarpetta, and O. Boylaud (2000). Summary indicators of product market regulation with an extension to employment protection legislation. Technical report, OECD, Economics department working papers No. 226, OECD Publishing. http://dx.doi.org/10.1787/215182844604.

- Organisation for Economic Co-operation and Development (2008) Organisation for Economic Co-operation and Development (2008). Handbook on Constructing Composite Indicators. Methodology and User guide. Paris: OECD.

- Pearson (1905) Pearson, K. (1905). On the General Theory of Skew Correlation and Non-linear Regression, volume XIV of Mathematical Contributions to the Theory of Evolution, Drapers’ Company Research Memoirs. Dulau & Co., London, Reprinted in: Early Statistical Papers, Cambridge University Press, Cambridge, UK, 1948.

- Plischke (2010) Plischke, E. (2010). An effective algorithm for computing global sensitivityindices (EASI). Reliability Engineering and System Safety 95, 354–360.

- Ratto and Pagano (2010) Ratto, M. and A. Pagano (2010). Using recursive algorithms for the efficient identification of smoothing spline ANOVA models. AStA Advances in Statistical Analysis 94, 367–388.

- Ratto et al. (2007) Ratto, M., A. Pagano, and P. Young (2007). State dependent parameter metamodelling and sensitivity analysis. Computer Physics Communications 177, 863–876.

- Ravallion (2010) Ravallion, M. (2010). Troubling tradeoffs in the human development index, policy research working paper 5484. Technical report, The World Bank, Development Research Group, Washington, DC.

- Reporters Sans Frontieres (2011) Reporters Sans Frontieres (2011). Press freedom index. Technical report, Reporters Without Borders, Paris http://en.rsf.org/press-freedom-index-2010,1034.html.

- Rotberg and Gisselquist (2008) Rotberg, R. and R. Gisselquist (2008). Strengthening african governance. ibrahim index of african governance: Results and rankings 2008. Technical report, Kennedy School of Government, Harward.

- Ruppert et al. (1995) Ruppert, A., S. J. Sheather, and M. P. Wand (1995). An effective bandwidth selector for local least squares regression. Journal of the American Statistical Association 90, 1257–1270.

- Ruppert and Wand (1994) Ruppert, D. and M. P. Wand (1994). Multivariate locally weighted least squares regression. The Annals of Statitics 22, 1346–1370.

- Saaty (1980) Saaty, T. (1980). The Analytic Hierarchy Process. McGraw-Hill, New York.

- Saaty (1987) Saaty, T. L. (1987). The analytic hierarchy process: what it is and how it is used. Mathematical Modelling 9, 161–176.

- Saisana et al. (2009) Saisana, M., P. Annoni, and M. Nardo (2009). A robust model to measure governance in African countries, EUR 23773. Technical report, European Commission, JRC-IPSC, Ispra, Italy.

- Saisana et al. (2011) Saisana, M., B. d’Hombres, and A. Saltelli (2011). Rickety numbers: Volatility of university rankings and policy implications. Research Policy 40, 165–177.

- Saisana et al. (2005) Saisana, M., A. Saltelli, and S. Tarantola (2005). Uncertainty and sensitivity analysis techniques as tools for the quality assessment of composite indicators. Journal of the Royal Statistical Society - A 168(2), 307–323.

- Saltelli (2002) Saltelli, A. (2002). Making best use of model valuations to compute sensitivity indices. Computer Physics Communications 145, 280–297.

- Saltelli (2007) Saltelli, A. (2007). Composite Indicators between analysis and advocacy. Social Indicators Research 81, 65–77.

- Saltelli et al. (2010) Saltelli, A., P. Annoni, I. Azzini, F. Campolongo, M. Ratto, and S. Tarantola (2010). Variance based sensitivity analysis of model output. design and estimator for the total sensitivity index. Computer Physics Communications 181, 259–270.

- Saltelli et al. (2008) Saltelli, A., M. Ratto, T. Andres, F. Campolongo, J. Cariboni, D. Gatelli, M. Saisana, and S. Tarantola (2008). Global Sensitivity Analysis - The Primer. John Wiley & Sons, Ltd.

- Saltelli and Tarantola (2002) Saltelli, A. and S. Tarantola (2002). On the relative importance of input factors in mathematical models: safety assessment for nuclear waste disposal. Journal of American Statistical Association 97, 702–709.

- Sobol’ (1993) Sobol’, I. (1993). Sensitivity analysis for non-linear mathematical models. Mathematical Modelling and Computational Experiment 1, 407–414. Translated from Russian: Sobol’, I. M., 1990, Sensitivity estimates for nonlinear mathematical models, Matematicheskoe Modelirovanie 2, 112-118.

- Stanley and Wang (1968) Stanley, J. and M. Wang (1968). Differential weighting: a survey of methods and empirical studies. Technical report, Johns Hopkins University, Baltimore.

- Stiglitz et al. (2009) Stiglitz, J. E., A. Sen, and J. Fitoussi (2009). Report by the commission on the measurement of economic performance and social progress. Technical report, www.stiglitz-sen-fitoussi.fr.

- Tarantola et al. (2006) Tarantola, S., D. Gatelli, and T. Mara (2006). Random balance designs for the estimation of first order global sensitivity indices. Reliability Engineering and System Safety 91(6), 717–727.

- Times Higher Education Supplement (2008) Times Higher Education Supplement (2008). World university rankings. Technical report, http://www.timeshighereducation.co.uk.

- Toulmin (1990) Toulmin, S. (1990). Cosmopolis - The hidden agenda of modernity. University of Chicago Press.

- United Nations Development Programme (2009) United Nations Development Programme (2009). Human development report 2009. Technical report, http://hdr.undp.org/en/reports/.

- United Nations Development Programme (2010) United Nations Development Programme (2010). Human development report 2010. Technical report, http://hdr.undp.org/en/reports/.

- van de Kerk and Manuel (2008) van de Kerk, G. and A. R. Manuel (2008). A comprehensive index for a sustainable society: The SSI, Sustainable Society Index. Journal of Ecological Economics 66, 228–242.

- Wang and Stanley (1970) Wang, M. W. and J. C. Stanley (1970). Differential weighting: a review of methods and empirical studies. Review of Educational Research 40(5), 663–705.

- Wooldridge (2010) Wooldridge, J. M. (2010). Econometric Analysis of Cross Section and Panel Data: Second Edition. The Mit Press.

- World Economic Forum (2010) World Economic Forum (2010). The Global Competitiveness Report 2010-2011. Technical report, World Economic Forum, http://www.weforum.org/.

- Xu and Gertner (2011) Xu, C. and G. Gertner (2011). Understanding and comparisons of different sampling approaches for the fourier amplitudes sensitivity test (fast). Computational Statistics and Data Analysis 55, 184–198.