Weak Informativity and the Information in One Prior Relative to Another

Abstract

A question of some interest is how to characterize the amount of information that a prior puts into a statistical analysis. Rather than a general characterization, we provide an approach to characterizing the amount of information a prior puts into an analysis, when compared to another base prior. The base prior is considered to be the prior that best reflects the current available information. Our purpose then is to characterize priors that can be used as conservative inputs to an analysis relative to the base prior. The characterization that we provide is in terms of a priori measures of prior-data conflict.

doi:

10.1214/11-STS357keywords:

.and

1 Introduction

Suppose we have two proper priors and on a parameter space for a statistical model . A natural question to ask is: how do we compare the amount of information each of these priors puts into the problem? While there may seem to be natural intuitive ways to express this, such as prior variances, it seems difficult to characterize this precisely in general. For example, the consideration of several examples in Sections 3 and 4 makes it clear that using the variance of the prior is not appropriate for this task.

The motivation for this work comes from Gelman (2006) and Gelman et al. (2008), where the intuitively satisfying notion of weakly informative priors is introduced as a compromise between informative and noninformative priors. The basic idea is that we have a base prior , perhaps elicited, that we believe reflects our current information about , but we choose to be conservative in our inferences and select a prior that puts less information into the analysis. While it is common to take to be a noninformative prior, this can often produce difficulties when is improper, and even when is proper, it seems inappropriate, as it completely discards the information we have about as expressed in . In addition, we may find that a prior-data conflict exists with and so look for another prior that reflects at least some of the information that puts into an analysis, but avoids the conflict.

We note that our discussion here is only about how we should choose given that has already been chosen. Of course, the choice of is of central importance in a Bayesian analysis. Ideally, is chosen based on a clearly justified elicitation process, but we know that this is often not the case. In such a circumstance it makes sense to try and choose reasonably but then be deliberately less informative by choosing to be weakly informative with respect to . The point is to inspire confidence that our analysis is not highly dependent on information that may be unreliable. To do this, however, requires a definition of what it means for one prior to be weakly informative with respect to another and that is what this paper is about.

To implement the idea of weak informativity, we need a precise definition. We provide this in Section 2 and note that it involves the notion of prior-data conflict. Intuitively, a prior-data conflict occurs when the prior places the bulk of its mass where the likelihood is relatively low, as the likelihood is indicating that the true value of the parameter is in the tails of the prior. Our definition of weak informativity is then expressed by saying that is weakly informative relative to whenever produces fewer prior-data conflicts a priori than . This leads to a quantifiable expression of weak informativity that can be used to choose priors. In Section 3 we consider this definition in the context of several standard families of priors and it is seen to produce results that are intuitively reasonable. In Section 4 we consider applications of this concept in some data analysis problems. While our intuition about weak informativity is often borne out, we also find that in certain situations we have to be careful before calling a prior weakly informative.

First, however, we establish some notation and then review how we check for prior-data conflict. We suppose that , that is, each is absolutely continuous with respect to a support measure on the sample space , with the density denoted by . With this formulation a prior leads to a prior predictive probability measure on given by , where . If is a minimal sufficient statistic for , then it is well known that the posterior is the same whether we observe or . So we will denote the posterior by hereafter. Since is minimal sufficient, we know that the conditional distribution of given is independent of . We denote this conditional measure by . The joint distribution can then be factored as

where is the marginal prior predictive distribution of .

While much of Bayesian analysis focuses on the third factor in (1), there are also roles in a statistical analysis for and . As discussed in Evans and Moshonov (2006, 2007), is available for checking the sampling model, for example, if is a surprising value from this distribution, then we have evidence that the model is incorrect. Furthermore, it is argued that, if we conclude that we have no evidence against the model, then the factor is available for checking whether or not there is any prior-data conflict, and we do this by comparing the observed value of to . If we have no evidence against the model, and no evidence of prior-data conflict, then we can proceed to inferences about . Actually, the issues involved in model checking and checking for prior-data conflict are more involved than this (see, e.g., the cited references and Section 5), but (1) gives the basic idea that the full information, as expressed by the joint distribution of , splits into components, each of which is available for a specific purpose in a statistical analysis.

Accordingly, we restrict ourselves here, for any discussions concerning prior-data conflict, to working with . One issue that needs to be addressed is how one is to compare the observed value to . In essence, we need a measure of surprise and for this we use a -value. Effectively, we are in the situation where we have a value from a single fixed distribution and we need to specify the appropriate -value to use. In Evans and Moshonov (2006, 2007) the -value for checking for prior-data conflict is given by

| (2) |

where is the density of with respect to the volume measure on the range space for . In Evans and Jang (2011) it is proved that, for many of the models and priors used in statistical analyses, (2) converges almost surely, as the amount of data increases, to , where is the true value of . So (2) is assessing to what extent the true value is in the tails of the prior, or, equivalently, to what extent the prior information is in conflict with how the data is being generated.

A difficulty with (2) is that it is not generally invariant to the choice of the minimal sufficient statistic . A general invariant -value is developed in Evans and Jang (2010) for situations where we want to compare the observed value of a statistic to a fixed distribution. This requires that the model and satisfy some regularity conditions, for example, all spaces need to be locally Euclidean, support measures are given by volume measures on these spaces, and needs to be sufficiently smooth. A formal description of these conditions can be found in Tjur (1974) and it is noted that these hold for the typical statistical application. For example, these conditions are immediately satisfied in the discrete case. Furthermore, for continuous situations, with densities defined as limits, we get the usual expressions for densities. When applied to checking for prior-data conflict, this leads to using the invariant -value

| (3) |

where , is the volume measure on , and is the differential of . Note that gives the volume distortion produced by at . So is the density of with respect to the support measure given by times the volume measure on the range space for .

In applications all models are effectively discrete, as we measure responses to some finite accuracy, and continuous models are viewed as being approximations. The use of (3), rather than (2), then expresses the fact that we do not want volume distortions induced by a transformation to affect our inferences. So we allocate this effect of the transformation with the support measure, rather than with the density, when computing the -value. In the discrete case, as well as when is linear, (2) and (3) give the same value and otherwise seem to give very similar values. Convergence of (3), to an invariant -value based on the prior, is established in Evans and Jang (2011). We use (3) throughout this paper but note that it is only in Section 3.3 where (3) differs from (2).

Our discussion here is based on a minimal sufficient statistic . We note that, except in mathematically pathological situations, such a statistic exists. It may be, however, that is high dimensional, for example, can be of the same dimension as the data. In such situations the dimensionality of the problem can often be reduced by examining components of the prior in a hierarchical fashion. For example, when the prior on is specified as , then and are checked separately and so the definition of weak informativity applies to each component separately. This is exemplified by the regression example of Section 4.2 where . More on checking the components of a prior can be found in Evans and Moshonov (2006). Furthermore, when ancillaries exist, it is necessary to condition on these when checking for prior-data conflict, as this variation has nothing to do with the prior. This results in a reduction of the dimension of the problem. The relevance of ancillarity to the problem of weakly informative priors is discussed in Section 5.

When choosing a prior it makes sense to consider the prior distribution of more than just the minimal sufficient statistic. For example, Chib and Ergashev (2009) consider the prior distribution of a somewhat complicated function of the parameters and data that has a real world interpretation. If this distribution produces values that seem reasonable in light of what is known, then this goes some distance toward justifying the prior. Also, the level of informativity of the prior can be judged by looking at the prior distribution of this quantity when that is possible. While this is certainly a reasonable approach to choosing , it does not supply us with a definition of weak informativity. For example, a prior can be chosen as discussed in Chib and Ergashev (2009), but then could be chosen to be weakly informative with respect to , to inspire confidence that conclusions drawn are not highly dependent on subjective appraisals.

As we will show, there will typically be many priors that are weakly informative with respect to a given base prior . The question then arises as to which we should use. This is partially answered in Section 2 where we show that the definition of weak informativity leads to a quantification of how much less informative is than . For example, we can choose in a family of priors to be 50% less informative than . Still, there may be many such and at this time we do not have a criterion that allows us to distinguish among such priors. For example, suppose the base prior is a normal prior for a location parameter. We can derive weakly informative priors with respect to such a prior in the family of normal priors (see Section 3.1) or in the family of priors (see Section 3.2). There is nothing in our developments that suggests that a weakly informative prior is to be preferred to a weakly informative normal prior or conversely. Such distinctions will have to be made based on other criteria.

2 Comparing Priors

There are a variety of measures of information used in statistics. Several measures have been based on the concept of entropy, for example, see Lindley (1956) and Bernardo (1979). While these measures have their virtues, we note that their coding theory interpretations can seem somewhat abstract in statistical contexts and they can suffer from nonexistence in certain problems. Also, Kass and Wasserman (1995) contain some discussion concerned with expressing the absolute information content of a prior in terms of additional sample values. Rather than adopting these approaches, we consider comparing priors based on their tendencies to produce prior-data conflicts. This formulation of the relative amount of information put into an analysis has a direct interpretation in terms of statistical consequences.

Suppose that an analyst has in mind a prior that they believe represents the information at hand concerning . The analyst, however, prefers to use a prior that is conservative, when compared to . In such a situation it seems reasonable to consider as a base prior and then compare all other priors to it. This idea comes from Gelman (2006) and leads to the notion of weakly informative priors.

Before we observe data we have no way of knowing if we will have a prior-data conflict. Accordingly, since the analyst has determined that best reflects the available information, it is reasonable to consider the prior distribution of when . Of course, this is effectively uniformly distributed [exactly so when has a continuous distribution when ] and this expresses the fact that all the information about assessing whether or not a prior-data conflict exists is contained in the -value, with no need to compare the -value to its distribution.

Consider now, however, the distribution of which is used to check whether or not there is prior-data conflict with respect to . Given that we have identified that a priori the appropriate distribution of is , at least for inferences about an unobserved value, then is not uniformly distributed. In fact, from the distribution of we can obtain an intuitively reasonable idea of what it means for a prior to be weakly informative relative to . Suppose that the prior distribution of clusters around 1. This implies that, if we were to use as the prior when is appropriate, then there is a small prior probability that a prior-data conflict would arise. Similarly, if the prior distribution of clusters around 0, then there is a large prior probability that a prior-data conflict would arise. If one prior distribution results in a larger prior probability of there being a prior-data conflict than another, then it seems reasonable to say that the first prior is more informative than the second. In fact, a completely noninformative prior should never produce prior-data conflicts.

So we compare the distribution of when , to the distribution of when , and do this in a way that is relevant to the prior probability of obtaining a prior-data conflict. One approach to this comparison is to select a -quantile of the distribution of , and then compute the probability

| (4) |

The value is presumably some cutoff, dependent on the application, where we will consider that evidence of a prior-data conflict exists whenever. Of course, if has a continuous distribution when , then . Our basic criterion for the weak informativity of relative to will then be that (4) is less than or equal to . This implies that the prior probability of obtaining a prior-data conflict under is no greater than when is used, at least when we have identified as our correct prior.

Definition 1.

If (4) is less than or equal to , then is weakly informative relative to at level . If is weakly informative relative to at level for every , then is uniformly weakly informative relative to at level . If is weakly informative relative to at level for every , then is uniformly weakly informative relative to .

Typically we would like to choose a prior that is uniformly weakly informative with respect to . This still requires us to select a prior from this class, however, and for this we must choose a level .

Once we have selected , the degree of weak informativity of a prior relative to can be assessed by comparing to via the ratio

| (5) |

If is weakly informative relative to at level , then (5) tells us the proportion of fewer prior-data conflicts we can expect a priori when using rather than . Thus, (5) provides a measure of how much less informative is than at level . So, for example, we might ask for a prior that is uniformly weakly informative with respect to and then, for a particular , select a prior in this class such that (5) equals 50%.

As we will see in the examples, it makes sense to talk of one prior being asymptotically weakly informative at level with respect to another prior in the sense that (4) is bounded above by in the limit as the amount of data increases. In several cases this simplifies matters considerably, as an asymptotically weakly informative prior is easy to find and may still be weakly informative for finite amounts of data.

While (4) seems difficult to work with, the following result is proved in the Appendix and gives a simpler expression.

Lemma 1.

Suppose has a continuous distribution under for . Then there exists such that , and is weakly informative at level relative to whenever . Furthermore, is uniformly weakly informative relative to if and only if for every .

Note that the equivalent condition for uniform weak informativity in Lemma 1 says that the probability content, under , in the “tails” (regions of low density) of the density is always bounded above by the probability content under . So puts more probability content into these tails than and this can be taken as an indication that is more dispersed than . Lemma 1 typically applies when we are dealing with continuous distributions on . It can also be shown that has a continuous distribution under if and only if has a continuous distribution under .

3 Deriving Weakly Informative Priors

We consider several examples of families of priors that arise in applications. These examples support our definition of weak informativity and also lead to some insights into choosing priors. The results obtained for the examples in this section are combined in Section 4.2 to give results for a practically meaningful context.

We first note that, while we could consider comparing arbitrary priors to , we want to reflect at least some of the information expressed in . The simplest expression of this is to require that have the same, or nearly the same, location as . This restriction simplifies the analysis and seems natural.

3.1 Comparing Normal Priors

Suppose we have a sample from a distribution where is unknown. Then is minimal sufficient and since is linear, there is constant volume distortion and so this can be ignored. Suppose that the prior on is a distribution with and known. We then have that is the distribution. Now suppose that is a distribution with known. Then is the distribution and

where denotes the distribution function. Now under we have that . Therefore,

We see immediately that (3.1) will be less than if and only if . In other words, will be uniformly weakly informative relative to if and only if is more diffuse than . Note that converges to 0 as to reflect noninformativity. Also, as , then (3.1) increases to . So we could ignore and choose conservatively based on this limit, to obtain an asymptotically uniformly weakly informative prior, as we know this value of will also be weakly informative for finite .

If we specify that we want (5) to equal , then (3.1) implies that . Such a choice will give a proportion fewer prior-data conflicts at level than the base prior. This decreases to as and so the more data we have the less extra variance we need for for weak informativity.

We can generalize this to with given by . Note we have that is the distribution. It is then easy to see that and

Note that (3.1) increases to the probability that , when , as . This probability can be easily computed via simulation.

The following result is proved in the Appendix.

Theorem 1.

For a sample of from the statistical model , a prior is uniformly weakly informative relative to a prior if and only if is positive semidefinite.

The necessary part of Theorem 1 is much more difficult than the case and shows that we cannot have a prior uniformly weakly informative relative to a prior unless . It follows from Theorem 1 that a prior is uniformly weakly informative relative to a prior if and only if a prior is uniformly weakly informative relative to a prior for every .

For the choice of we have that, if and are arbitrary positive definite matrices, then whenever where denotes the th ordered eigenvalue of . Note that this condition does not require that the have the same eigenvectors. When they do have the same eigenvectors, so is the spectral decomposition of , then whenever for .

3.2 Comparing a Prior with a Normal Prior

It is not uncommon to find priors being substituted for normal priors on location parameters. Suppose is a sample from a distribution where is unknown. We take to be a distribution and to be a distribution, that is, denotes the distribution of with distributed as a 1-dimensional distribution with degrees of freedom. We then want to determine and so that the prior is weakly informative relative to the normal prior.

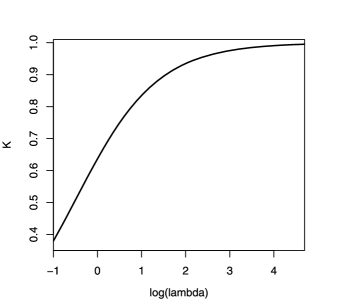

We consider first the limiting case as . The limiting prior predictive distribution of the minimal sufficient statistic is while converges in distribution to where is the distribution function of an distribution. This implies that (4) converges to and this is less than or equal to if and only if . So to have that is asymptotically weakly informative relative to at level , we must choose large enough. Clearly we have that is asymptotically uniformly weakly informative relative to if and only if

In Figure 1 we have plotted against .

Since , we require that for a Cauchy prior to be uniformly weakly informative with respect to a prior.A prior has variance . If we choose so that the variance is , then . Since this is less than , this prior is not uniformly weakly informative. A prior has to have variance at least equal to if we want it to be uniformly weakly informative relative to a prior. This is somewhat surprising and undoubtedly is caused by the peakedness of the distribution. Note that as , so this increase in variance, for the prior over the normal prior, decreases as we increase the degrees of freedom.

The situation for finite is covered by the following result proved in the Appendix.

Theorem 2.

For a sample of from the statistical model , a prior is uniformly weakly informative relative to a prior whenever , where is the unique solution of with the density. Further, increases to

| (8) |

as and so a prior is asymptotically uniformly weakly informative if and only if is greater than or equal to (8).

Theorem 2 establishes that we can conservatively use (8) to select a uniformly weakly informative prior.

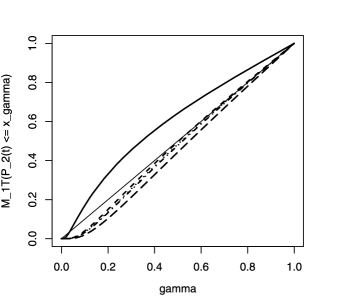

In Figure 2 we have plotted the value of (4) that arises with priors, where is chosen in a variety of ways, together with the 45-degree line. A uniformly weakly informative prior will have (4) always below the 45-degree line, while a uniformly weakly informative prior at level will have (4) below the 45-degree line to the left of and possibly above to the right of . For example, when , then the prior and the prior have the same variance. We see that this prior is only uniformly weakly informative at level and is not uniformly weakly informative.

Note that (5) converges to as , and setting this equal to implies that which converges, as , to the result we obtained in Section 3.1. So when and , we must have .

Our analysis indicates that one has to be careful about the scaling of the prior if we want to say that the prior is less informative than a normal prior, at least when we want uniform weak informativity.

Consider now comparing a multivariate prior to a multivariate normal prior. Let denote the -dimensional distribution given by , where is a square root of the positive definite matrix and has a -dimensional distribution with degrees of freedom. This is somewhat more complicated than the normal case, but we prove the following result in the Appendix which provides sufficient conditions for the asymptotic uniform weak informativity.

Theorem 3.

When sampling from the statistical model , a prior is asymptotically uniformly weakly informative relative to a prior whenever is positive semidefinite, where .

In contrast with Theorem 1, we do not have an equivalent characterization of the uniform weak informativity of multivariate priors in terms of the marginal priors of . For example, when , then and when , then for all . Therefore, for all does not imply that is positive semidefinite, for example, take .

For the choice of we have that, if and are arbitrary positive definite matrices, then whenever . When the have the same eigenvectors, then whenever for .

3.3 Comparing Inverse Gamma Priors

Suppose now that we have a sample from a distribution where is unknown. Then is minimal sufficient and . Now suppose that we take to be an inverse gamma prior on , namely, . From this we get that and, since , which implies

We want to investigate the weak informativity of a prior relative to a prior. For finite this is a difficult problem, so we simplify this by considering only the asymptotic case. When the prior is , then, as , we have that , that is, in the limit.Therefore, and we want to determine conditions on so that .

While results can be obtained for this problem, it is still rather difficult. It is greatly simplified, however, if we impose a natural restriction on . In particular, we want the location of the bulk of the mass for to be located roughly in the same place as the bulk of the mass for . Accordingly, we could require the priors to have the same means or modes, but, as it turns out, the constraint that requires the modes of the functions to be the same greatly simplifies the analysis. Actually, converges to 0, but the ’s cancel in the inequalities defining and so we can define which has its mode at . Therefore, we must have so that lies on the line through the points and . We prove the following result in the Appendix.

Theorem 4.

Suppose we use a prior on when sampling from the statistical model . Then a prior on , with , is asymptotically weakly informative relative to the prior whenever and or, equivalently, whenever and .

Of particular interest here is that we cannot reduce the rate parameter arbitrarily close to 0 and be guaranteed asymptotic weak informativity.

4 Applications

We consider now some applications of determining weakly informative priors.

4.1 Weakly Informative Beta Priors for the Binomial

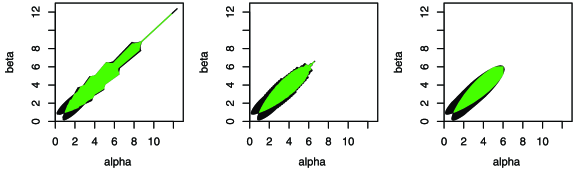

Suppose that and . This implies that and from this we can compute (4) for various choices of .

As a specific example, suppose that , the base prior is given by , and we take so that . As alternatives to this base prior, we consider priors. In Figure 3 we have plotted all the corresponding to distributions that are weakly informative with respect to the distribution at level , together with the subset of all corresponding to distributions that are uniformly weakly informative relative to the distribution. The graph on the left corresponds to , the middle graph corresponds to , and the graph on the right corresponds to . The plot for shows some anomalous effects due to the discreteness of the prior predictive distributions and these effects disappear as increases. In such an application we may choose to restrict to symmetric priors, as this fixes the primary location of the prior mass. For example, when , a prior for satisfying is uniformly weakly informative with respect to the prior and we see that values of are eliminated as increases.

4.2 Weakly Informative Priors for the Normal Regression Model

Consider the situation where , is of rank and are unknown. Therefore, with and . Suppose we have elicited a prior on given by , and . We now find a prior that is asymptotically uniformly weakly informative relative to this choice. For this we consider gamma priors for and priors for given . For the asymptotics we suppose that as .

As discussed in Evans and Moshonov (2006, 2007), it seems that the most sensible way to check for prior-data conflict here is to first check the prior on , based on the prior predictive distribution of . If no prior-data conflict is found at this stage, then we check the prior on based on the conditional prior predictive for given , as is ancillary for . Such an approach provides more information concerning where a prior-data conflict exists than simply checking the whole prior via (3).

So we consider first obtaining an asymptotically uniformly weakly informative prior for . We have that and so, as in Section 3.3, when , the limiting prior predictive distribution of is as . Furthermore, when , then . Therefore, the limiting value of (4) in this case is the same as that discussed in Section 3.3 and Theorem 4 applies to obtain a prior asymptotically uniformly weakly informative relative to the prior.

If we consider as an arbitrary fixed value from its prior predictive distribution, then, when , the conditional prior predictive distribution of given converges to the distribution. Furthermore, when , the conditional prior predictive distribution of given converges to the distribution. So we can apply Lemma 1 to these limiting distributions. It is then clear that the comparison is covered by Theorem 3, as the limiting prior predictives are of the same form. Therefore, the prior is asymptotically uniformly weakly informative relative to the prior whenever or, equivalently, whenever where is defined in Theorem 3. Note that this condition does not depend on . Also, as , we can use Theorem 2 to obtain that a prior is asymptotically uniformly weakly informative relative to the prior whenever .

4.3 Weakly Informative Priors for Logistic Regression

Supposing we have a single binary valued response variable and quantitative predictors , we observe at settings of the predictor variables and have observations at the th setting of the predictors. The logistic regression model then says that where for and and the are unknown real values. For simplicity, we will assume no is zero. For this model , with , is a minimal sufficient statistic. For the base prior we suppose that is the product of independent priors on the ’s and we consider the problem of finding a prior that is weakly informative relative to . For example, we could take to be a product of priors and to be a product of priors and choose the so that weak informativity is obtained. Note that since is discrete we can use (2) in our computations.

As we will see, it is not the case that choosing the very large relative to the will necessarily make weakly informative relative to . In fact, there is only a finite range of values where weak informativity will obtain.

While this can be demonstrated analytically, the argument is somewhat technical and it is perhaps easier to see this in an example. The following bioassay data are from Racine et al. (1986) and were also analyzed in Gelman et al. (2008). These data arise from an experiment where 20 animals were exposed to four doses of a toxin and the number of deaths recorded (Table 1).

| Dose (gml) | Number of animals | Number of deaths |

|---|---|---|

| 0.422 | 5 | 0 |

| 0.744 | 5 | 1 |

| 0.948 | 5 | 3 |

| 2.069 | 5 | 5 |

Following Gelman et al. (2008), we took to be the variable formed by calculating the logarithm of dose and then standardizing to make the mean of equal to 0 and its standard deviation equal to 12. Gelman et al. (2008) placed independent Cauchy priors on the regression coefficients, namely, independent of .

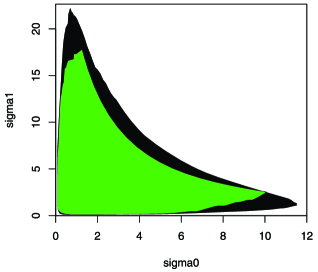

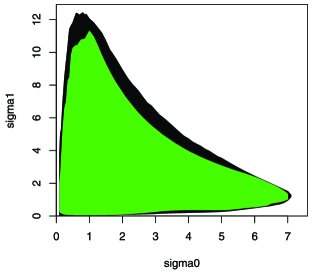

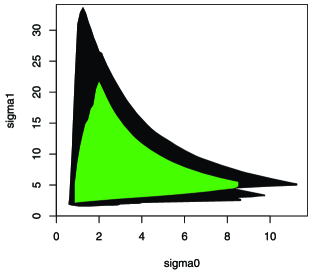

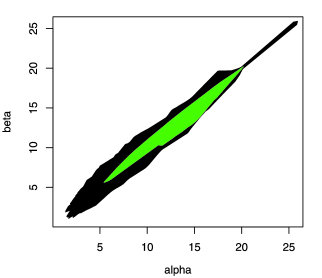

We consider four possible scenarios for the investigation of weak informativity at level and uniform weak informativity. In Figure 4(a) we compare priors with the prior . The entire region gives the values corresponding to priors that are weakly informative at level , while the lighter subregion gives the values corresponding to priors that are uniformly weakly informative. Note that some of the irregularity in the plots is caused by the fact that the prior predictive distributions of are discrete. The three remaining plots are similar where in Figure 4(b) and , in Figure 4(c) and , and in Figure 4(d) and . Note that these plots only depend on the data through the values of .

|

|

| (a) | (b) |

|

|

| (c) | (d) |

We see clearly from these plots that increasing the scaling on any of the does not necessarily lead to weak informativity and in fact inevitably destroys it. Furthermore, a smaller scaling on a parameter can lead to uniform weak informativity. These plots underscore how our intuition does not work very well with the logistic regression model, as it is not clear how priors on the ultimately translate to priors on the . In fact, it can be proven that, if we put independent priors on the , fix all the scalings but one, and let that scaling grow arbitrarily large, then the prior predictive distribution of converges to a distribution concentrated on two points, for example, when the scaling on increases these points are given by , and this is definitely not desirable. This partially explains the results obtained.

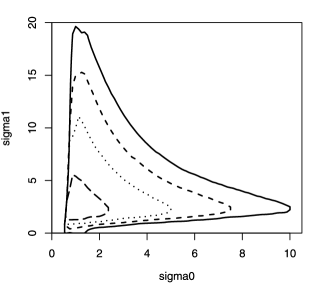

Of some interest is how much reduction we actually get, via (5), when we employ a weakly informative prior. In Figure 5 we have plotted contours of the choices of that give 0%, 25%, 50% and 75% reduction in prior-data conflicts for the case where and when (this corresponds to ). Note that a substantial reduction can be obtained.

We can also consider fixing one of the scalings and seeing how much reduction we obtain when varying the other. For example, when we fix we find that the maximum reduction is obtained when is close to 2.2628, while if we fix , then the maximum reduction is obtained when is close to 0.875.

It makes sense in any application to check to see if any prior-data conflict exists with respect to the base prior. If there is no prior-data conflict, this increases our confidence that the weakly informative prior is indeed putting less information into the analysis. This is assessed generally using (3), although (2) suffices in this example. When , then (2) equals and when (the prior used in Gelman et al., 2008), then (2) equals , so in neither case is there any evidence of prior-data conflict.

5 Refinements Based Upon Ancillarity

Consider an ancillary statistic that is a function of the minimal sufficient statistic, say, . The variation due to is independent of and so should be removed from the -value (3) when checking for prior-data conflict. Removing this variation is equivalent to conditioning on and so we replace (3) by

| (9) |

that is, we use the conditional prior predictive given the ancillary . To remove the maximal amount of ancillary variation, we must have that is a maximal ancillary. Therefore, (4) becomes

| (10) |

that is, we have replaced by and by.

We note that the approach discussed in Section 2 works whenever is a complete minimal sufficient statistic. This is a consequence of Basu’s Theorem, as, in such a case, any ancillary is statistically independent of and so conditioning on such an ancillary is irrelevant. This is the case for the examples in Sections 3 and 4.

One problem with ancillaries is that multiple maximal ancillaries may exist. When ancillaries are used for frequentist inferences about via conditioning, this poses a problem because it is not clear which maximal ancillary to use and confidence regions depend on the maximal ancillary chosen. For checking for prior-data conflict via (9), however, this does not pose a problem. This is because we simply get different checks depending on which maximal ancillary we condition on. For example, if conditioning on maximal ancillary does not lead to prior-data conflict, but conditioning on maximal ancillary does, then we have evidence against no prior-data conflict existing.

Similarly, when we go to use (10), we can also simply look at the effect of each maximal ancillary on the analysis and make our assessment about based on this. For example, we can use the maximum value of (10) over all maximal ancillaries to assess whether or not is weakly informative relative to . When this maximum is small, we conclude that we have a small prior probability of finding evidence against the null hypothesis of no prior-data conflict when using . We illustrate this via an example.

Example 1.

Suppose that we have a sample of from the distribution where is unknown. Then the counts constitute a minimal sufficient statistic and is ancillary, as is . Then is given by independent of , giving

We then have two 1-dimensional distributions and to use for checking for prior-data conflict. A similar result holds for the conditional distribution given .

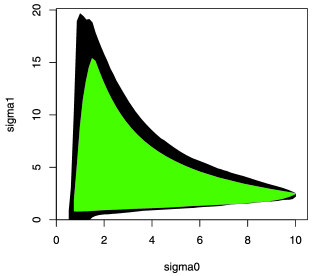

For example, suppose is a distribution on , so the prior concentrates about , and for a sample of we have that and . In Figure 6 we have plotted all the values of that correspond to a prior that is weakly informative relative to the prior at level , as well as those that are uniformly weakly informative. So for each such we have that (10) is less than or equal to 0.05 for both and .

6 Conclusions

We have developed an approach to measuring the amount of information a prior puts into a statistical analysis relative to another base prior. This base prior can be considered as the prior that best reflects current information and our goal is to determine a prior that is weakly informative with respect to it. Our measure is in terms of the prior predictive probability, using the base prior, of obtaining a prior-data conflict. This was applied in several examples where the approach is seen to give intuitively reasonable results. The examples chosen here focused on commonly used prior families. In several cases these were conjugate families, although there is no special advantage computationally to conjugacy in this context.

As noted in several examples, we need to be careful when we conceive of a prior being weakly informative relative to another. Ultimately this concept needs to be made precise and we feel our definition is a reasonable proposal. The definition has intuitive support, in terms of avoiding prior-data conflicts, and provides a quantifiable criterion that can be used to select priors.

In any application we should still check for prior-data conflict for the base prior using (3). If prior-data conflict is found, a substitute prior that is weakly informative relative to the base prior can then be selected and a check made for prior-data conflict with respect to the new prior. While selecting the prior based on the observed data is not ideal, this process at least seems defensible from a logical perspective. For example, the new prior still incorporates some of the information from the base prior and is not entirely driven by the data. Certainly, in the end it seems preferable to base an analysis on a prior for which a prior-data conflict does not exist. Of course, we must still report the original conflict and how this was resolved.

We have restricted our discussion here to proper priors. The concept of weak informativity is obviously related to the idea of noninformativity and improper priors. Certainly any prior that has a claim to being noninformative should not lead to prior-data conflict. At this time, however, there is no precise definition of what a noninformative prior is, whereas we have provided a definition of a weakly informative prior. In the examples of Section 3.1 and 3.2 we see that if the spread of is made large enough, then is uniformly weakly informative with respect to the base prior. This suggests that the flat improper prior, which is Jeffreys’ prior for this problem, can be thought of as always being uniformly weakly informative. The logistic regression example of Section 4.3 suggests caution, however, in interpreting increased diffuseness as a characterization of weak informativity. In the binomial example of Section 4.1 the uniform prior is always weakly informative with respect to the base prior, while the (Jeffreys’) prior is not. Further work is required for a full examination of the relationships among the concepts of prior-data conflict, noninformativity and weak informativity.

Appendix

Proof of Lemma 1 We have that since has a continuous distribution under . Suppose has a point mass at when . The assumption implies. Then, pick so that and let . Then, has point mass at because .This is a contradiction and so has a continuous distribution when .

Let where and is the range space of . Then, and for all . Thus, we have that , , and is weakly informative at level relative to if and only if . The fact that implies the last statement.

Proof of Theorem 1 Suppose first that . We have that and so . This implies that (3.1) is less than and so the prior is uniformly weakly informative relative to the prior.

For the converse put . If , then for there exists such that which implies and so . This implies that and so and the result follows. If , then the same reasoning says that and (3.1) would be greater than if .

So we need only consider the case where , both have positive volumes, that is, we are supposing that neither nor is positive semidefinite and then will obtain a contradiction. Let and note that , since , that is, there are points in the interior of on the boundary of . Now put and note that has positive volume.

Let and . Then while . Since , we need only show that for all sufficiently small, to establish the result.

Let be such that is the density of . Then where . Note it is clear that and so and . Also, where . Therefore, as ,

since as and .

Proof of Theorem 2 First note that we can use (2) instead of (3) in this case as is constant in this case. We assume without loss of generality that

We first establish several useful technical results. If is a probability distribution that is unimodal and symmetric about 0, and denotes a density, we have that is unimodal and symmetric about 0. We have the following result.

Lemma .1.

If is a minimal sufficient statistic, is constant in , and are unimodal and symmetric about 0, the have continuous distributions when , and has a unique solution for then is uniformly weakly informative relative to .

By the unimodality and symmetryof , we must have that . We show for all because it is equivalent to being uniformly weakly informative relative to by Lemma 1. Let be the solution of on . From the unique solution assumption, for and for . For and for , . Thus, we are done.

We can apply Lemma .1 to comparing normal and priors when sampling from a normal.

Lemma .2.

Suppose we have a sample of from a location normal model, is a prior and is a prior. If , then is uniformly weakly informative relative to .

We have that and, using the representation of the distribution as a gamma mixture of normals, we write where is the density of distribution. By the symmetry of , is symmetric. Also, for and so . Thus, is decreasing on , that is, is unimodal. To show that is log-convex with respect to , we prove that . Note that ,

and so , where is the random variable having density . Thus, is log-convex in .

The functions and meet in at most two points on because is linear in and is convex in . Also, and share at least one point on because , and the following shows that for all large . Note first that if , then and . Then,

as .

The above conditions together imply that and meet in exactly one point on . Therefore, is uniformly weakly informative relative to by Lemma .1.

Since is strictly decreasing in , we see that is equivalent to where satisfies . This proves the first part of Theorem 2.

We also need the following results for the remaining parts of Theorem 2.

Lemma .3.

(i) increases as , (ii) as.

(i) We have and putting , we can write this as

| (1) |

Differentiating both sides of (1) with respect to , we have . If we let , then this integral can be written as the expectation

where the inequality follows via Jensen’s inequality. Hence, and so is an increasing function of because . This proves increases as .

(ii) It is easy to check that when and for . Let be a pair satisfying and (1). Then, for and as . Therefore,

and this proves (ii).

Lemma .4.

Suppose we have a sample of from a location normal model, is a prior and is a prior. Then is asymptotically uniformly weakly informative relative to if and only if .

Suppose that . Then by Lemma .3 for all and so is uniformly weakly informative with respect to for all . So (4) is bounded above by for all and so the limiting value of (4) is also bounded above by . This establishes that is asymptotically uniformly weakly informative relative to .

Suppose now that . Note that and . Therefore, we get . Let and . Then, on and. Hence, is not weakly informative relative to at level . Therefore, .

It is now immediate that and the proof of Theorem 2 is complete.

Proof of Theorem 3 Since the minimal sufficient statistic is linear, there is no volume distortion and we can use (2) instead of (3). The limiting prior predictive distribution of under is and under it is . It is easy to check that when and when . This implies that converges to , where is the distribution function of an distribution. Further, we have that (4) converges to .

Let for . By the continuity of as a function of , and the continuity of , there exists such that if and only if . Hence, is asymptotically uniformly weakly informative relative to if and only if for all by Lemma 1. Since is decreasing in , the set . So we must prove that for all .

The positive semidefiniteness of implies that is positive semidefinite. Then, for , that is, , we have . Thus, .

Now we prove a stronger inequality for all . Note that

and set . Then, and

Note that is equivalent to . Further recalling the definition of from the statement of the theorem,

The logarithm of given by is concave as a function of . Hence, has exactly two solutions: and . Because of its concavity, the function is positive on and negative on . This implies that is increasing on and decreasing on . Since and , the function is nonnegative, that is, for all . Thus, for all .

Proof of Theorem 4 Let . For , let be the two solutions of (one of the equals so . Note that if and only if and then as well. Then, and . Now . By Lemma 1 we have that uniform weak informativity is equivalent to for all and so we must prove that or for all . Since is implicitly a function of , it is equivalent to prove that for all . Using , we have that the derivatives of the two terms are given by

where . Then, recalling the definition of , we have that the ratio strictly decreases as increases from to when because , and is identically 1 when . Suppose then that so there is at most one value where and the derivative is 0. If , then for all and strictly decreases from . This cannot hold because as . Hence, and increases from near and decreases to as . Therefore, goes up from and down to as increases from to , and we have for all .

Acknowledgments

The authors thank the Editor, Associate Editor and referees for many helpful comments.

References

- Bernardo (1979) {barticle}[author] \bauthor\bsnmBernardo, \bfnmJose-M.\binitsJ.-M. (\byear1979). \btitleReference posterior distributions for Bayesian inference (with discussion). \bjournalJ. Roy. Statist. Soc. Ser. B \bvolume41 \bpages113–147. \bidmr=0547240 \endbibitem

- Chib and Ergashev (2009) {barticle}[author] \bauthor\bsnmChib, \bfnmSiddartha\binitsS. and \bauthor\bsnmErgashev, \bfnmBakhodir\binitsB. (\byear2009). \btitleAnalysis of multifactor affine yield curve models. \bjournalJ. Amer. Statist. Assoc. \bvolume104 \bpages1324–1337. \endbibitem

- Evans and Jang (2010) {barticle}[author] \bauthor\bsnmEvans, \bfnmMichael\binitsM. and \bauthor\bsnmJang, \bfnmGun Ho\binitsG. H. (\byear2010). \btitleInvariant -values for model checking. \bjournalAnn. Statist. \bvolume38 \bpages312–323. \bidmr=2589329 \endbibitem

- Evans and Jang (2011) {barticle}[author] \bauthor\bsnmEvans, \bfnmMichael\binitsM. and \bauthor\bsnmJang, \bfnmGun Ho\binitsG. H. (\byear2011). \btitleA limit result for the prior predictive applied to checking for prior-data conflict. \bjournalStatist. Probab. Lett. \bvolume81 \bpages1034–1038. \endbibitem

- Evans and Moshonov (2006) {barticle}[author] \bauthor\bsnmEvans, \bfnmMichael\binitsM. and \bauthor\bsnmMoshonov, \bfnmHadas\binitsH. (\byear2006). \btitleChecking for prior-data conflict. \bjournalBayesian Anal. \bvolume1 \bpages893–914. \bidmr=2282210 \endbibitem

- Evans and Moshonov (2007) {bincollection}[author] \bauthor\bsnmEvans, \bfnmMichael\binitsM. and \bauthor\bsnmMoshonov, \bfnmHadas\binitsH. (\byear2007). \btitleChecking for prior-data conflict with hierarchically specified priors. In \bbooktitleBayesian Statistics and Its Applications (\beditor\bfnmA. K.\binitsA. K. \bsnmUpadhyay, \beditor\bfnmU.\binitsU. \bsnmSingh and \beditor\bfnmD.\binitsD. \bsnmDey, eds.) \bpages145–159. \bpublisherAnamaya Publishers, \baddressNew Delhi. \endbibitem

- Gelman (2006) {barticle}[author] \bauthor\bsnmGelman, \bfnmAndrew\binitsA. (\byear2006). \btitlePrior distributions for variance parameters in hierarchical models. \bjournalBayesian Anal. \bvolume1 \bpages515–533. \bidmr=2221284 \endbibitem

- Gelman et al. (2008) {barticle}[author] \bauthor\bsnmGelman, \bfnmAndrew\binitsA., \bauthor\bsnmJakulin, \bfnmAleks\binitsA., \bauthor\bsnmPittau, \bfnmMaria Grazia\binitsM. G. and \bauthor\bsnmSu, \bfnmYu-Sung\binitsY.-S. (\byear2008). \btitleA weakly informative default prior distribution for logistic and other regression models. \bjournalAnn. Appl. Statist. \bvolume2 \bpages1360–1383. \bidmr=2655663 \endbibitem

- Kass and Wasserman (1995) {barticle}[author] \bauthor\bsnmKass, \bfnmRobert E.\binitsR. E. and \bauthor\bsnmWasserman, \bfnmLarry\binitsL. (\byear1995). \btitleA reference Bayesian test for nested hypotheses and its relationship to the Schwarz criterion. \bjournalJ. Amer. Statist. Assoc. \bvolume90 \bpages928–934. \bidmr=1354008 \endbibitem

- Lindley (1956) {barticle}[author] \bauthor\bsnmLindley, \bfnmD. V.\binitsD. V. (\byear1956). \btitleOn a measure of the information provided by an experiment. \bjournalAnn. Math. Statist. \bvolume27 \bpages986–1005. \bidmr=0083936 \endbibitem

- Racine et al. (1986) {barticle}[author] \bauthor\bsnmRacine, \bfnmA.\binitsA., \bauthor\bsnmGrieve, \bfnmA. P.\binitsA. P., \bauthor\bsnmFlühler, \bfnmH.\binitsH. and \bauthor\bsnmSmith, \bfnmA. F. M.\binitsA. F. M. (\byear1986). \btitleBayesian methods in practice: Experiences in the pharmaceutical industry (with discussion). \bjournalJ. Roy. Statist. Soc. Ser. C \bvolume35 \bpages93–150. \bidmr=0868007 \endbibitem

- Tjur (1974) {bmisc}[author] \bauthor\bsnmTjur, \bfnmT.\binitsT. (\byear1974). \bhowpublishedConditional Probability Models. Institute of Mathematical Statistics, Univ. Copenhagen, Copenhagen. \bidmr=0345151 \endbibitem