Generating multivariate extreme value distributions

Helena Ferreira Department of Mathematics, University of Beira

Interior, Covilhã, Portugal

Abstract

We define in a probabilistic way a parametric family of multivariate extreme value distributions. We derive its copula, which is a mixture of several complete dependent copulas and total independent copulas, and the bivariate tail dependence and extremal coefficients. Based on the obtained results for these coefficients, we propose a method to built multivariate extreme value distributions with prescribed tail/extremal coefficients. We illustrate the results with examples of simulation of these distributions.

Keywords: multivariate extreme value theory, tail dependence, extremal

coefficients, simulation

1 Introduction

The construction of multivariate distributions has its motivation in Probability Theory, Biostatistics, Economics, and there is no need to demonstrate its importance nowadays. In particular, multivariate extreme value (MEV) distributions provide models for joint extreme events which require special care from practitioners since rare events can have serious natural and economic impact.

The MEV distributions composes an important class of positive dependent distributions with dependence in the extreme upper tails, with this property known as tail dependence ([14, 9]). A misleading evaluation of the dependence in the tails of a multivariate distribution may lead to an underestimation of risks from crises events ([2]).

The MEV distributions can be constructed through methods such as mixtures, stochastic representations and limits ([9]). They also can be obtained via copulas and suitable techniques of extra-parametrisation ([12, 7, 11, 6]).

The dependence structure of a MEV distribution is completely characterised by its dependence function ([14]). However this function cannot be easily inferred from data and simple dependence measures are welcome.

The most popular of the dependence measures for bivariate distributions are the upper tail dependence coefficient and the extremal coefficient , introduced far back in the sixties ([18, 19]), which determines each other in the extreme value distributions by the relation .

Our paper is a contribution for the main issue of the development of higher dimensional models capturing dependencies. This issue covers quite a large spectrum of techniques and applications where copulas become ladies of quality since they are able to yield any kind of dependence structure independently of marginal distributions. An application of copula functions is the simulation of multivariate distributions with dependent observations. By departing of the right copula or a mixture of copulas any dependence structure may be reached. For a review of different estimators, some model selection tests for copula functions and methods of its simulation see, for instance, [4, 8, 13]. However, in general copulas cannot be characterised in a simple way that provides a simple algorithm to simulate data.

How to get out of the way of selection of a candidate copula, its estimation and simulation of dependent random observations? One proposal is to estimate non-parametricaly the bivariate extremal dependences ([16, 5]) and to construct in a probabilistic way a multivariate extreme value distribution with these prescribed extremal dependences, which can be used to generate random observations.

Here we propose a method to built a MEV distribution with prescribed tail/extremal dependence coefficients.

To the best of our knowledge, the problem was treated by [1] for elliptical distributions and by [3] for the case where each bivariate tail dependence coefficient between the margins and has the representation , where and is the dimension of the random vector.

Our solution is of stochastic representation kind and can be used in practical problems where one needs to buil a stochastic model in a situation where the extremal dependence is known or estimated and the knowledge or estimates of marginal distributions are available.

A motivation for such approach can be the difficulty to choose or find an appropriate copula for the problem in hand or the fact that the choice of copulas does not inform explicitly about the strength of the dependence between the variables involved.

Another advantage of the method we propose is that we can take tail dependence/extremal coefficients not constant over time and build a more realistic time-varying parametric family of models.

The result shows that the MEV distributions are rich enough to encompass a large variability for bivariate dependence one would like to be able to handle.

2 A multivariate extreme value model

Let , , and , , be independent and unit Frechét variables and , nonnegative constants. For constant satisfying , consider the -dimensional random vector defined as

| (1) |

We will present in the next result the distribution of the random vector and its copula , where denotes the generalised inverse of the distribution function of , which is a mixture of several complete dependent copulas and total independent copulas.

Proposition 2.1.

The mixture model in (1) has multivariate extreme value distribution defined as

| (2) |

with its corresponding copula

| (3) |

Dem. By assuming , we can write from the definition of the model in (1), for each ,

| (4) |

The assumptions on the distributions of the variables and leads to the expression in (2) and, by changing to the variable we obtain the copula function which satisfies the max-statbility condition , for .

The tail dependence coefficient between and , measures the probability of occurring extreme values for one random variable given that another assumes an extreme value too and is defined as

| (5) |

where denotes the distribution function of . In our model, since has bivariate extreme value distribution, can be computed from the extremal coefficient of . This is defined by

| (6) |

where denotes the distribution function of . The value of doesn’t depend on and satisfies .

These dependence measures have extensions for -dimensional vectors with ( [16, 10, 5, 15]).

In the next result we compute for the model in (1) and show how such a model for prescribed can be constructed. In this way we provide a method for building new multivariate distributions and modelling dependence structures.

Proposition 2.2.

Dem. First we derive the diagonal of the bivariate copula of , . We have, by taking for in (3),

| (8) |

Therefore

| (9) |

which leads to the above presented value for .

Now, for (b), let be the symmetric tail dependence coefficients matrix of a random vector, where . Consider a model as in (1) with , , defined as following. Assume that when we don’t define the corresponding coefficient, , and . Let us consider

| (14) |

| (15) |

| (16) |

with if , if and .

We remark that and therefore the set in (17) will be empty for . Also, since , the sets in (14) will be empty for .

For sake of simplicity we can present the coefficients in a matrix as

By assuming if , we can verify that this choice of the coefficients for (1) leads to

| (17) |

and, for each pair ,

In fact, as we can seen in the proof, the model can be constructed for any

and therefore we have the next two particular cases.

Proposition 2.3.

(a) Given the set of tail dependence coefficients of a -dimensional random vector such that

, for each , there exists a random vector defined as in (1) with the same tail dependence coefficients.

(b) Given the set of tail dependence coefficients of a -dimensional random vector such that for each , there exists a random vector defined as in (1) with the same tail dependence coefficients.

3 Generating MEV distributions

Example 3.1.

Consider the model in (1) with , , , , , and . By applying the Proposition 1.2, we find the following tail dependence matrix

for the vector .

Example 3.2.

Let now

be the tail dependence coefficients matrix of a -dimensional random vector.

We chose

and, as in the proof of part (b) of the Proposition 1.2, we present the coefficients , , for along line of the matrix , , as follows

For this choice of , and , by applying the Proposition 1.1, we obtain a random vector with tail dependence coefficients matrix

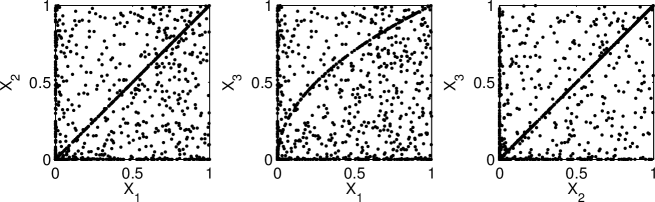

Example 3.3.

Let now

be the tail dependence coefficients matrix of a -dimensional random vector.

If we chose , the matrix of coefficients , ,

then, by applying Proposition 2.3, the model in (1) still has the given tail dependence coefficients matrix .

We simulated observations of leading to the following bivariate representations.

References

- [1] Brommundt, B. (2003) Estimating the value at risk by means of elliptical copulae. Diploma Thesis, Munich University of Technology.

- [2] Embrechts, P., McNeil, A., Straumann, D. (2002). Correlation and dependence in risk management: properties and pitfalls In: Risk Management: Value at Risk and Beyond, ed. M.A.H. Dempster, Cambridge University Press, Cambridge, pp. 176-223.

- [3] Falk, M. (2005) On the generation of a multivariate extreme value distribution with prescribed tail dependence parameter matrix. Statistics and Probability Letters, 2005, vol. 75, issue 4, pages 307-314.

- [4] Fermanian, J.-D., Radulović, D., Wegkamp, M. (2004). Weak convergence of empirical copula processes. Bernoulli 10(5), 847-860.

- [5] Ferreira, H. and Ferreira, M. (2011) Fragility Index of block tailed vectors. To appear in Journal of Statistical Planning and Inference. http://dx.doi.org/10.1016/j.jspi.2012.01.021

- [6] Ferreira, H. and Pereira, L. (2011) Generalized logistic model and its orthant tail dependence. Kybernetika, Vol. 47, No. 5, 732-739

- [7] Fisher, M. (2012) Multivariate copulae. In D. Kurowicka and H. Joe (Eds), Dependence modeling - Vine Copula Handbook. World Scientific Publishing.

- [8] Genest, C., Remillard, B. and Beaudoin, D. (2009) Goodness-of-fit tests for copulas: a review and a power study. Insurance: Mathematics and Economics 44, 199-213.

- [9] Joe, H. (1997). Multivariate Models and Dependence Concepts. Chapman & Hall, London.

- [10] Li, H. (2009). Orthant tail dependence of multivariate extreme value distributions, J. Multivariate Anal., 100(1), 243-256.

- [11] Liebscher, E. (2008) Construction of asymetric multivariate copulas, J. Multivariate Anal. 99(10), 2234Ð2250.

- [12] Nelsen, R.B. (2006). An Introduction to Copulas. Second Edition. Springer, New York.

- [13] Patton A. (2009) Copula-based models for financial time series. In T.G. Andersen, R.A. Davis, J.-P. Kreiss and T. Mikosch (Eds.), Handbook of Financial Time Series. Springer Verlag.

- [14] Resnick, S. (1987). Extreme Values, Regular Variation and Point Processes. Springer-Verlag, New York.

- [15] Schlather, M. and Tawn, J.A. (2002). Inequalities for the extremal coefficients of multivariate extreme value distributions. Extremes, 5(1), 87-102.

- [16] Schmidt, R., Stadtmüller, U. (2006). Nonparametric estimation of tail dependence, The Scandinavian Journal of Statistics 33, 307-335.

- [17] Smith, R.L. (1990). Max-stable processes and spatial extremes. Preprint, Univ. North Carolina, USA.

- [18] Sibuya, M. (1960). Bivariate extreme statistics. Ann. Inst. Statist. Math. 11, 195-210.

- [19] Tiago de Oliveira, J. (1962/63). Structure theory of bivariate extremes, extensions. Est. Mat., Estat. e Econ. 7, 165-195.