Multiple break detection in the correlation structure of random variables

Abstract

Correlations between random variables play an important role in applications, e.g. in financial analysis. More precisely, accurate estimates of the correlation between financial returns are crucial in portfolio management. In particular, in periods of financial crisis, extreme movements in asset prices are found to be more highly correlated than small movements. It is precisely under these conditions that investors are extremely concerned about changes on correlations. A binary segmentation procedure to detect the number and position of multiple change points in the correlation structure of random variables is proposed. The procedure assumes that expectations and variances are constant and that there are sudden shifts in the correlations. It is shown analytically that the proposed algorithm asymptotically gives the correct number of change points and the change points are consistently estimated. It is also shown by simulation studies and by an empirical application that the algorithm yields reasonable results.

Keywords: Binary segmentation; Correlations; CUSUM statistics; Financial returns; Multiple change point detection.

1 Introduction and Summary

There is much empirical evidence that the correlation structure of financial returns of all sorts cannot be assumed to be constant over time, see e.g. Krishan et al. (2009). Especially in times of crisis, correlation often increases, a phenomenon which is referred to as “Diversification Meltdown” (Campbell et al., 2008). Wied, Krämer and Dehling (2012) propose a CUSUM type procedure along the lines of Ploberger et al. (1989) to formally test if correlations between random variables remain constant over time. However, with this approach the practitioner is only able to see if there is a change or not; he cannot determine where a possible change occurs or how many changes there are.

The present paper fills this gap by proposing an algorithm based on the correlation constancy test to estimate both the number and the timing of possible change points. For this purpose, we adapt a method for the estimation of multiple breaks from Vostrikova (1981) which has been implemented in various problems by Inclán and Tiao (1994), Bai (1997), Bai and Perron (1998), Andreou and Ghysels (2002), Gooijer (2006), Galeano (2007) and Galeano and Tsay (2010), among others. The segmentation algorithm proceeds as follows: First, we determine the “dominating” change point and decide if this point is statistically significant. Then, we split the series in two parts and again test for possible change points in each part of the series. The procedure stops if we do not find any new change point any more. In this paper, we will analytically show that the algorithm asymptotically gives the correct number of change points and that - finitely many - change points are consistently estimated. Furthermore, we show that the algorithm gives reasonable results in finite samples and in an empirical application.

The rest of the paper is organized as follows. Section 2 introduces the proposed procedure. Section 3 derives the asymptotic properties of the procedure. Sections 4 and 5 present some simulation studies and a real data application and Section 6 provides some conclusions. All proofs are presented in the Appendix.

2 An algorithm for the determination of change points

In this section, we present the algorithm for the detection of change points in the correlation structure of bivariate random variables. To be more precise, let be a sequence of bivariate random variables with finite first four moments and let be the observation period. Denoting the correlation between and by

Wied et al. (2012) propose a test for the problem

which uses the test statistic

| (1) |

where is the empirical correlation up to time , for and is a normalizing constant which is described in Appendix A.1. Wied et al. (2012) show that the asymptotic null distribution of is the supremum over the absolute value of a standard Brownian bridge. The present paper employs this test to estimate the timings and the number of possible change points.

We assume that there is a finite number of change points. However, the number, location and size of the change points are unknown. Wied et al. (2012) allow for some fluctuations in the first and second moments under the null hypothesis, compare their assumption (A4). The variance fluctuations may be slightly stronger if the variances behave similarly, but it has to be stressed that no arbitrary fluctuations are allowed. In fact, in both settings, the variance shifts vanish with increasing sample size. For this reason and for ease of exposition, we focus on the case where expectations and variances are constant under the alternative. It would be possible to extend the framework to slightly changing expectations and variances as described in the previous paragraph, but this would only affect the proofs, not the procedure itself. Note that stationary GARCH models are included in our setup as the unconditional variances are constant here. We investigate in our simulation study how the procedure behaves in finite samples in the presence of GARCH effects (volatility clustering) or shifts in the mean.

The formal assumption is:

Assumption 1.

Under the alternative, expectations and variances are constant and equal to finite numbers and , the second cross moment changes from to . The function is a step function with a finite number of steps , i.e. there is a partition and there are second cross moment levels such that

and . The quantities , and do not depend on .

The function specifies the timing and the size of the changes in correlation. Since this is a step function, we consider sudden changes in the correlation (or more specific the covariance) and do not consider smooth changes.

Our goal is to estimate , and . To this end, we propose a binary segmentation algorithm. The main idea is to isolate each change point in different time intervals by splitting the two series into two parts once a change point is found. Then, the search of a new change point is repeated in both sections. The proposed procedure for detecting correlation changes essentially relies on the intuitive estimator of the change point fraction. To that purpose, we rewrite the test statistic (1) as

with (where is the floor function) and estimate the timing of the break by with and . Here and in the following, we restrict the values for which the is calculated to multiples of and, for uniqueness, then choose the smallest of these values. Note that is calculated from all observations. In the next steps of the algorithm, we just consider the observations in the relevant part of the sample and we call the corresponding “target function” , where, for and ,

Here, , (where and stands for maximum and minimum, respectively) and denotes the empirical correlation coefficient calculated from data point to data point . Moreover, is the variance estimator from Appendix A.1 calculated from the data from to . Then the timing of break is estimated by

| (2) |

with .

Basically, this means that we always look for the time point at which the test statistic (1) (calculated from data in a particular interval) takes its maximum and divide by . Note that for and .

The formal algorithm proceeds as follows:

-

1.

Let and be the observed series. Obtain the test statistic . There are two possibilities:

-

(a)

If the test statistic is statistically significant, i.e., if , where is the asymptotic critical value for a given upper tail probability, then a correlation change is announced. Let be the break point estimator from (2) and go to step 2.

-

(b)

If the test statistic is not statistically significant, the algorithm stops.

-

(a)

-

2.

Let be the change points in increasing order already found in previous iterations. Repeat step 1 for every segment until

where is the value of the statistic calculated from the data from to , for , taking and .

-

3.

Let be the detected change points. If , refine the estimate of the location of the change points by calculating the statistic from the data from to , for , where and . If any of the change points is not statistically significant, delete it from the list, and repeat this step.

-

4.

Finally, estimate the correlation between and in each segment separately with the usual Bravais-Pearson correlation coefficient.

The key point of the proposed procedure is that it detects a single change point in each iteration, which may not be the most efficient way to detect correlation changes when multiple changes exist. However, our theoretical results show that the procedure consistently detects the true change points. Moreover, the proposed procedure works well in small samples in terms of detection of the true number of changes as shown in the Monte Carlo experiments of Section 4.

Step 3 is meant to refine the estimation of the change points. Note that in this step, the procedure computes the value of the statistics in intervals that are only affected by the presence of a single change point, which is not guaranteed in step 2.

In a sense, the main objective of the proposed procedure is to identify issues which require further attention. For instance, if the number of change points detected is large compared to the sample size, then a piecewise constant correlation may not be a good description of the true correlation between the two series.

Although we later prove that we can consistently estimate the correct number of change points even if the critical value is the same in each step of the procedure, we proceed differently in practice with finite samples. Using the same critical level in steps 2 and 3 may lead to over-estimation of the number of change points, because more tests are performed in each iteration as the number of detected change points increases and the type I errors accumulate (remember that the decision of the tests basically determine the number of change points). So, to avoid this multiple-test problem we require that the type I errors used depend on the number of change points already detected by the algorithm. To be more precisely, if is a fixed initial type I error for step 1 such as , we use the critical value after detecting the -th change point. Here, is such that . This leads to , so for example to and for . This choice of keeps the same significance level constant for all tests. In fact, for the asymptotic result concerning the number of break points (Theorem 2), the initial type I error would have to converge to zero, but in finite samples, seems to be an acceptable choice. Moreover, in practice, we use the quantiles of the distribution of the supremum of the absolute value of a standard Brownian bridge (the limit distribution of the correlation test statistic under the null hypothesis) in order to apply the procedure. The explicit form of this distribution function can be found in Billingsley (1968), p. 85. For example, for the critical value is .

3 Asymptotic results

In this section, we show that our algorithm asymptotically gives correct solutions. To this end, we impose another assumption which guarantees that we do not have two or more change points with “equal form”, i.e. we assume that there are always change points which dominate the rest.

Assumption 2.

Let be arbitrary. The function from Assumption 1 is such that the function with

is either constant or has a unique maximum.

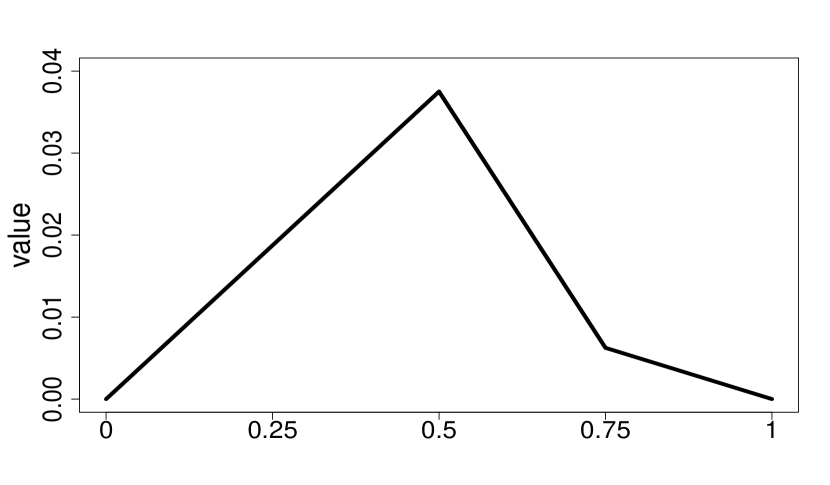

A dominating change point is then defined as in a given interval . For ease of exposition, we do not mention the dependence of from and which should become clear from the context. We illustrate Assumption 2 in the case of the example

| (3) |

In the interval for example, we have

so has a unique maximum at , i.e. the point with the “strongest” correlation change, see also Figure 1.

Figure 1 about here

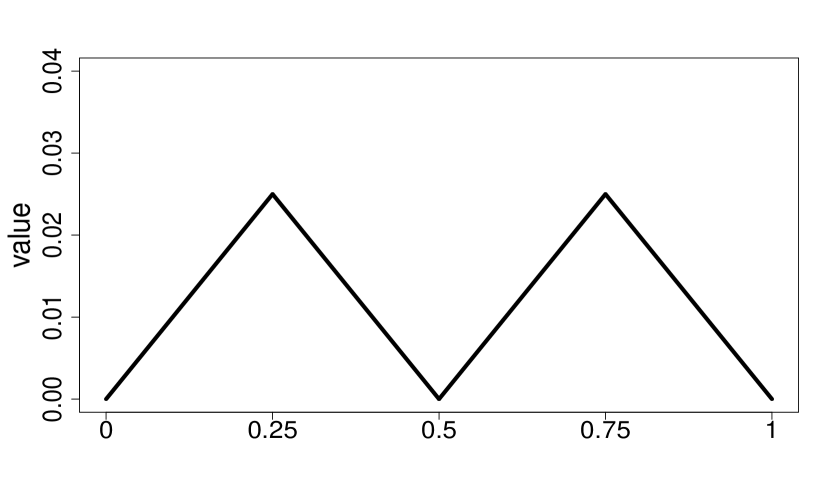

In general, the size and the position of the change decide if it is dominant or not. Assumption 2 is violated if the correlation changes are equal at symmetric time points, e.g. when

| (4) |

Here, we have

so has two non-unique maxima at and , see also Figure 2.

Figure 2 about here

Moreover, we need a rather technical assumption regarding the normalizing constant .

Assumption 3.

Consider an arbitrary interval with and let be the estimator from Appendix A.1 calculated from data from to . Then, under the alternative, converges to a real number .

For the interval , this assumption is for example fulfilled in a simple model with a bivariate normal distribution, serial independence, constant expectations , constant variances and a change in the covariance in the middle of the sample from to . In this case, it is easy to see that is equal to with

and . So, is equal to and this is a real positive number e.g. for .

Moreover, we need two assumptions concerning bounded moments and serial dependence.

Assumption 4.

The -th absolute moments of the components of are uniformly bounded for some .

Assumption 5.

The following theorem shows that the change point estimator (2) is consistent if it is known a priori that there is a change point in a given interval.

Theorem 1.

While also of interest on its own, this theorem is mainly needed for the next one which provides the convergence of the algorithm. Note that, as we just use a law of large numbers and no (functional) central limit theorem in the proof of this theorem, we just need a little bit more than finite second moments. This is different in the following theorem yielding consistency of the number of change points. Here, we need stronger assumptions to guarantee that the test statistic behaves well in the case of no correlation change. These assumptions are basically similar to the assumptions (A1), (A2) and (A3) in Wied et al. (2012).

Assumption 6.

Consider an arbitrary interval with . For it holds under the null which is a finite and positively definite matrix.

Assumption 7.

The -th absolute moments of the components of are uniformly bounded for some .

Assumption 8.

The following theorem also requires an additional assumption on the critical values . While we argued in the preceding section that we have to adjust the value for finite due to multiple testing problems, we need another kind of assumption for the asymptotics as . This assumption is basically the same as in Bai (1997), Proposition 11.

Assumption 9.

The critical values used in the algorithm obey the condition

and for .

The assumption rules out choosing an initial type I error such as for all because the initial type I error must converge to . However, it is legitimate using a fixed type I error in finite samples if we consider an upper bound for . The initial type I error then corresponds to , see the discussion before Section 3. Note that the level adjustment discussed in the previous section basically fits into this setting because is a fixed number not depending on . This guarantees that the critical values do not become too large so that the -condition is not violated.

Theorem 2.

Finally, in this section, we want to address the case in which the correlation shifts tend to zero with rate as the sample size increases such that in Assumption 1 we replace by . In this setting, Wied et al. (2012) provide local power results (compare their Theorem 2). We do not have consistency to the true break point any more, but the change point estimator converges to a non-degenerated random variable as the next theorem shows.

Theorem 3.

Let Assumptions 1 (with replaced by ), 6, 7 and 8 be true and let there be at least one break point in a given interval with . Then it holds for the change point estimator (2) that

where is a constant depending on the data generating process formally defined in the proof, is from Assumption 2 and is a one-dimensional standard Brownian motion.

Note that under our local alternatives, the limit matrix from Assumption 6 is equal to the corresponding limit matrix under the null. Second, note that, for and , the quantity

is a one-dimensional standard Brownian bridge. Third, note that, although the quantity appears in the limit process, we do not need Assumption 2 for this theorem. In fact, the (formerly assumed to be existing) unique maximum of does not appear in the limit random variable from Theorem 3.

4 Monte Carlo experiments

This section presents several Monte Carlo experiments to gain insight into the finite sample performance of the proposed procedure. We study several aspects, including the size (probability of a type I error) of the procedure, its power in correct detection of the changes and its ability to accurately identify the location of the change points. For that, we consider two different scenarios. The first one based on a vector autoregression (VAR) model, which is widely used for many economic time series, and the second one based on a dynamic conditional correlation (DCC) model, which is widely used for financial returns.

For the first scenario, initially we check the size (probability of a type I error) of the procedure which can be equivalently considered as the accuracy of the estimator of the number of change points if the true value is zero. To this purpose, we consider a vector autoregression of order 1 given by:

where are iid bivariate Gaussian distributed with zero mean and correlation parameter . Three values of the correlation parameter are considered, and . Three values of the parameter are considered, , and , to represent the case where and are close to non-stationary. Sample sizes are , , , and . Table 1 gives the results based on replications and an initial nominal significant level of . From this table, it seems that the type I error of the proposed procedure (the accuracy of the estimator of the number of change points if the true value is zero) is very close to the initial nominal level even with the smallest sample size. Therefore, overestimation does not appear to be an issue for the proposed procedure in this situation if there are no changes in the correlation.

Table 1 about here

Next, we analyze the power of our procedure when there is a single change point in the series. The Monte Carlo setup is similar to the one described above, but the series are generated with a single change point in the correlation. Three locations of the change point are considered, , and . The change is such that is initially and then changes to , to represent a big change, to , to represent a small change, or to , to represent a moderate change. Tables 2, 3 and 4 show the relative frequency detection of zero, one and more than one changes. It is seen that the procedure performs quite well in detecting a single change point if the size of the change is moderate and large, with many cases over correct detection. However, if the size of the change is small, then the power is small. Second, as the sample size increases and the size of the change gets larger, the procedure works better. However, the magnitudes of the exception are small in general. Third, when the sample size of the change is small, the probability of under-detection may be large. Fourth, the location of the change point does not strongly affect the detection frequency of the procedure when the sample size is large. However, if the sample size is small then the procedure detects more frequently the change point at the middle of the series. Finally, in most cases, the percentage of false detection is smaller than the nominal . In particular, the frequency of over-detection is small unless the two series are close to nonstationarity. On the other hand, Table 5 shows the median and mean absolute deviation of the change point estimators in each case. The median of the estimates are quite close to the true change point locations. Note that the larger the size of the change, the better is the location estimated.

Next, we conduct another Monte Carlo experiment to study the power of the proposed procedure for detecting two change points. In this case, the location of the change points are and , respectively. Three situations are considered. First, the changes are such that the correlation of the series before the first change point is , then changes to , and, finally, changes to at the second change point. Second, the correlation of the series before the first change point is , then changes to , and, finally, changes to at the second change point. Third, the correlation of the series before the first change point is , then changes to , and, finally, changes to at the second change point. It is important to note that the first and the third of the situations do not fulfill Assumption 1. However, we consider these situations in order to show that, even if there is not a dominating change point, the procedure appears to perform well in these situations. Indeed, the results suggest that the procedure consistently estimates the number of change points even if Assumption 1 does not hold. Table 6 shows the relative frequency detection of zero, one, two and more than two changes. As in the case of a single change point, the proposed procedure works reasonably well, especially when the sample size is large or the size of the correlation change is large. In addition, the procedure does not overestimate the number of change points. It may underestimate the number of change points, however. The underestimation can be serious when the sample size is small, say , which indicates that the procedure has to be applied with care for small sample size. Finally, the percentage of false change points detected in both cases, one and two change points, is smaller than the nominal in almost all the cases. On the other hand, Table 7 shows the median and mean absolute deviation of the estimates of the change point locations. Note that the medians of the estimates are quite close to the true ones. Again, it appears that the larger is the size of the change, the better is the location estimated.

To finish with the VAR(1) model, we repeat the previous experiment when there are two change points in the correlation of the series plus two change points in the mean of the series. The Monte Carlo setup is similar to the one described above, but the mean of the series pass from to . The results are shown in Tables 8 and 9. We deduce from these results that the inclusion of changes in the mean additionally to changes in the correlation does not affect importantly the results of the procedure. Note however that the size of the fluctuation test is usually affected by mean changes: If the correlation is constant and if there are mean changes, the empirical size is typically higher than the nominal size. Detailed results are available upon request.

For the second scenario, more appropriate for financial returns, initially we check the size (probability of a type I error) of the procedure which can be equivalently considered as the accuracy of the estimator of the number of change points if the true value is zero. To this purpose, we consider a dynamic conditional correlation model as in Tse and Tsui (2002) given by:

where

with and are the individual volatilities of and respectively, driven by univariate GARCH models, and:

is the conditional correlation between and , , is the matrix of ones and are iid bivariate standard Gaussian distributed. Three values of the correlation parameter are considered, , and , to represent the cases where and are uncorrelated and have medium and high unconditional correlation, respectively. Sample sizes are , , , and that represent usual sample sizes in financial returns. Table 10 shows the relative frequency detection of zero and more than zero changes based on replications and an initial nominal significant level of . From this table, as in the VAR(1) case, it seems that the type I error of the proposed procedure is very close to the initial nominal level.

Table 10 about here

Next, we analyze the power of our procedure when there is a single change point in the series. The Monte Carlo setup is similar to the one described above, but the series are generated with a single change point in the correlation. Three locations of the change point are considered, , and . The change is such that the correlation of the series is and then changes to , or , that represent a small, moderate and high correlation change, respectively. Table 11 shows the relative frequency detection of zero, one and more than one changes. The results appear to confirm the conclusions given in the case of the VAR(1) model. Consequently, note that conditional variances and correlations does not appear to affect the power of the procedure for detecting one change point in the correlation structure of the two series. In particular, note that even a small change can be reasonably well detected by the procedure. On the other hand, Table 12 shows the median and mean absolute deviation of the change point estimators in each case and appears to confirm that the larger the size of the change, the better is the location estimated.

Finally, we conduct a Monte Carlo experiment to study the power of the proposed procedure for detecting two change points for the DCC model. As in the VAR(1) case, the location of the change points are and . Three situations are considered. First, the changes are such that the correlation of the series before the first change point is , then changes to , and, finally, changes to at the second change point. Second, the correlation of the series before the first change point is , then changes to , and, finally, changes to at the second change point. Third, the correlation of the series before the first change point is , then changes to , and, finally, changes to at the second change point. Again, it is important to note that the first situation does not fulfill Assumption 1, but we include it to show that even if there is not a dominating change point, the procedure appears to perform well. Table 13 shows the relative frequency detection of zero, one, two and more than two changes. As in the VAR(1) case, the proposed procedure works reasonably well, especially when the sample size is large or the size of the correlation change is large. In particular, note that the procedure does not overestimate the number of change points and that it may underestimate the number of change points only when both the size of the changes and the sample size are small. On the other hand, Table 14 shows the median and mean absolute deviation of the estimates of the change point locations leading to similar conclusions as before.

5 Application

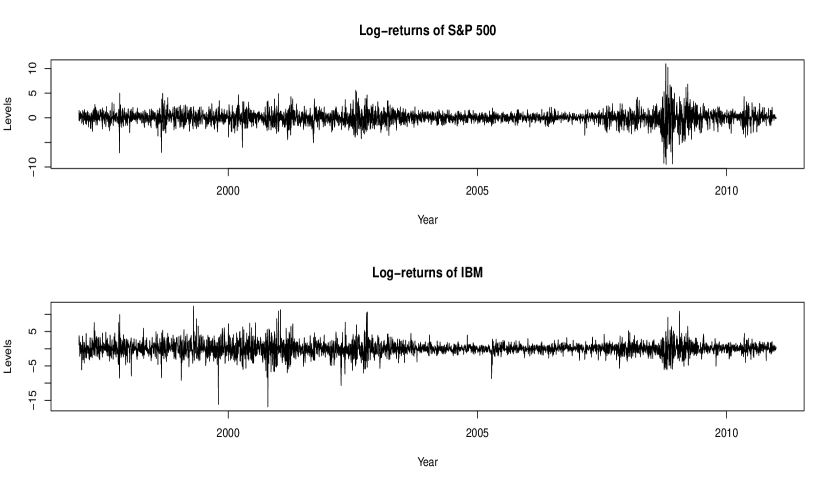

This section looks for changes in the correlation structure of the log-return series of the Standard & Poors 500 Index and the IBM stock from January 2, 1997 to December 31, 2010 consisting of data points. Both log-returns series are plotted in Figure 3, which shows different volatility periods. The empirical full sample correlation is . The autocorrelation functions of the log-returns show some minor serial dependence, while the autocorrelation functions of the squared log-returns reveals considerable serial dependence, as usual in stock market returns.

Figure 3 about here

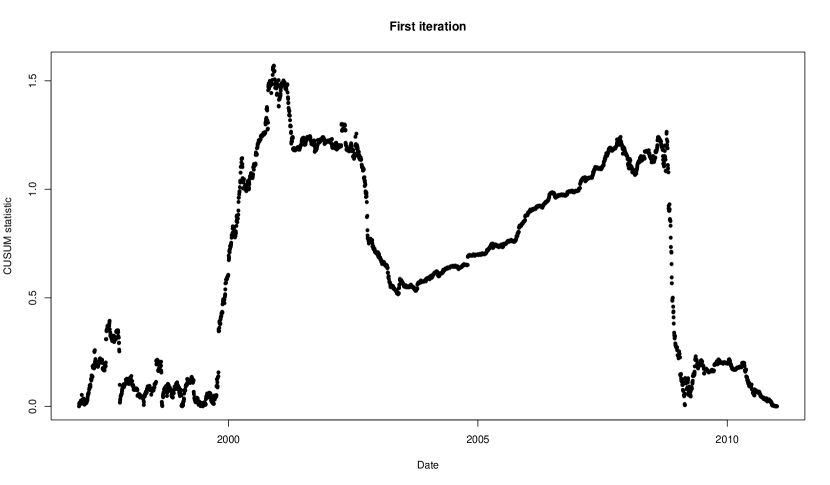

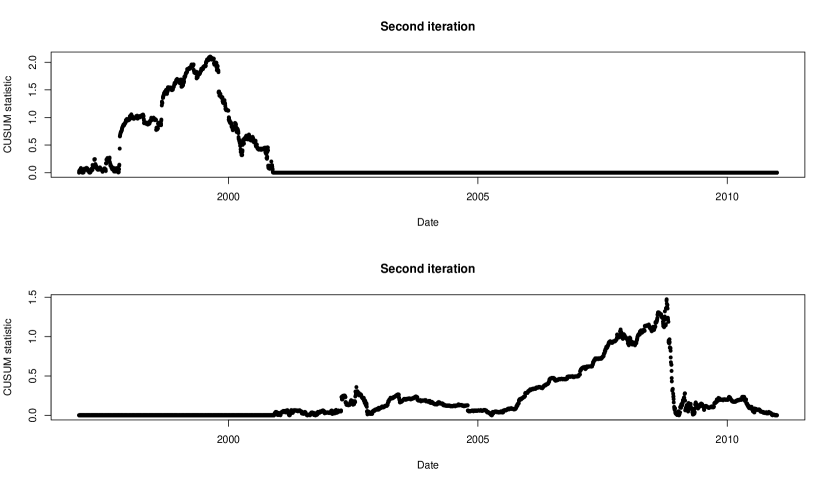

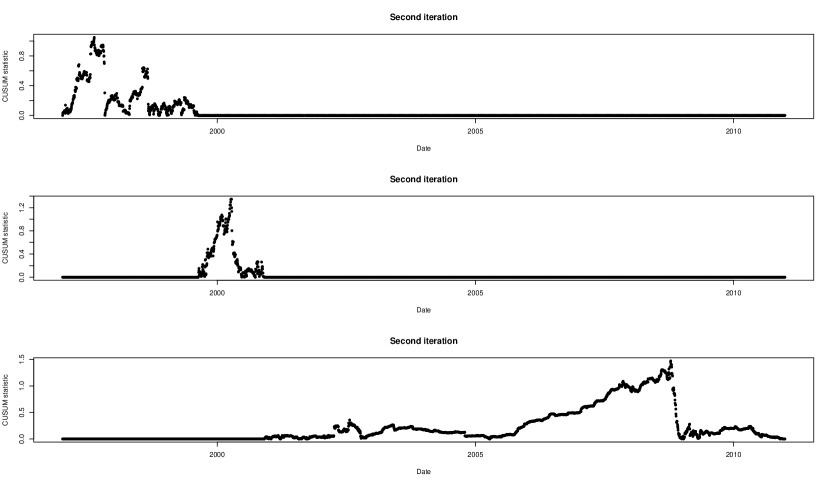

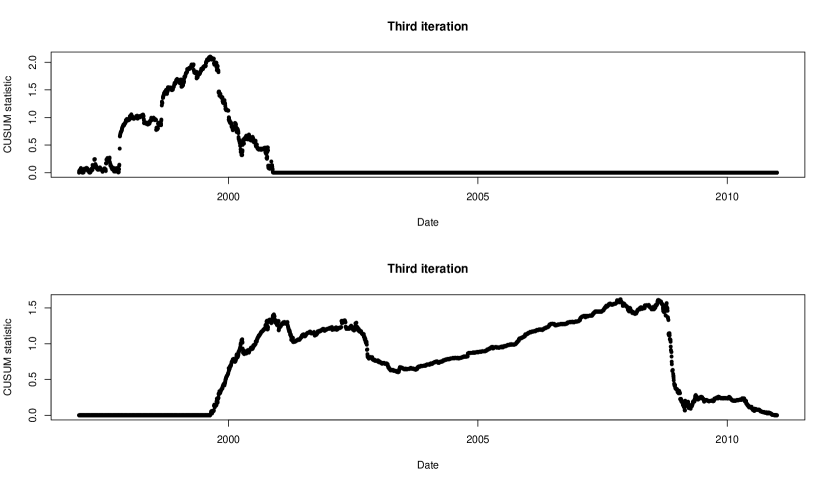

Next, we apply the proposed segmentation procedure of Section 2 to detect correlation changes for the log-returns of the S&P 500 and IBM stock assets. Table 15 and Figures 4, 5, 6 and 7 show the iterations taken by the procedure. Similar to the simulation experiments of Section 4, we start with the asymptotic critical value at the 5% significance level. In the first iteration, the procedure detects a change in the correlation at time point (November 29, 2000). Indeed, as shown in Figure 4 there are two local modes of the CUSUM statistic. The value of the test statistic (1) is , which is statistically significant at the level. Following the proposed procedure, we split the series into two subperiods and look for changes in the subintervals and , respectively. In the first subinterval (see Figure 5), the procedure detects a change at time point (August 19, 1999). The value of the test statistic is . Then, we split the subinterval into two subintervals and look for changes in the subintervals , and (see Figure 6). No more changes were found in these three subintervals. Then, we pass to step 3 and refine the search. For that we estimate the location of the change points in the intervals and , respectively. In the first subinterval (see Figure 7), as in the previous step, the procedure detects a change at time point (August 19, 1999) and the value of the test statistic is . On the other hand, in the second subinterval (see Figure 7), as in the previous step, the procedure detects a change at time point (November 12, 2007) and the value of the test statistic is . These are the finally estimated change points.

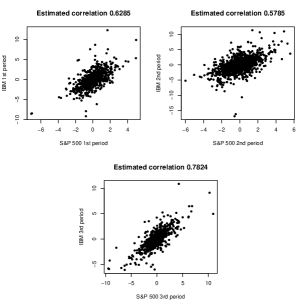

The empirical correlation coefficients in the three subintervals are , and , respectively, indicating that the correlation shifted to a smaller value after the first change point and to a higher value after the second change point. Figure 8 shows the scatterplots of the two log-returns indexes at three different subperiods. It is interesting to see that the dates of the detected change points fare well with well known financial facts. The period starting at till the end of is a period of economic growth in the U.S. economy in which the inflation was under control and the unemployment rate dropped to below . This is a period with high increases in the stock markets. However, the collapse of the dot-com bubble started at the end of the 1990s and the beginning of the 2000s, and the market gave back around the of the growth obtained in the 1990s. However, note that, contrarily to the diversification meltdown theory, the correlation did not increase during the dot-com bubble crisis. The third estimated change point roughly corresponds to the beginning of the Global Financial Crisis around the end of 2007, which is considered by many economists the worst financial crisis since the Great Depression of the 1930s. The reduction of interest rates leads to several consequent issues starting with the easiness of obtaining credit, leading to sub-prime lending, so that an increased debt burden, and finally a liquidity shortfall in the banking system. This resulted in the collapse of well known financial institutions such as Lehman Brothers, Merrill Lynch, Washington Mutual, Wachovia, and AIG, among others, the bailout of banks by national governments such as Bear Stearns, Citigroup, Bank of America and Northern Rock, among others, and great loses in stock markets around the world. In this case, the Global Financial Crisis produced an increase in the correlation between both log-returns. Of course, it is important to note that these economic interpretations are mere speculations. These comments only point out that, for this particular example, the proposed detection procedure in Section 2 identifies changes in the correlation structure that fare well with well known events affecting the U.S. financial market.

Figure 8 about here

6 Conclusions

In this paper, we have proposed a binary segmentation procedure for change points in the correlation structure of random variables. As far as we know, this is the first procedure for solving such a problem. The procedure is based on a CUSUM test statistic proposed by Wied et al. (2012). The asymptotic distribution of the test coincides with the one of the supremum of the absolute value of a standard Brownian bridge in the interval . We have shown that the proposed procedure consistently detects the true number and the location of the change points. Also, the finite sample properties of the procedure have been analyzed by the analysis of several simulation studies and the application of the procedure to a real data example. The empirical findings in the real data example suggest that the procedure detects changes in situations in which the relationship between financial returns may change due to financial crisis. Some care is necessary if the procedure is applied on datasets with small sample size.

A potential drawback of our procedure is the fact that it is designed for a bivariate vector only. Of course it is possible to consider each entry in a higher dimensional correlation matrix separately to determine whether there have been changes in the individual correlations. It might be an

interesting issue for further research to do this in a more sophisticated way. Moreover, it might be interesting to consider other methods of

detecting multiple breaks in correlation, for example a method building on the simultaneous method in Bai and

Perron (1998). This method would be quite

different as the break points would not be estimated step-by-step, but by performing one single minimization: Given a certain sum of squares and the

number of break points, one searches for the break points which minimize this sum. It would be interesting to see which procedure

provides advantages in which situation.

Acknowledgements: Financial support by MCI grants MTM2008-03010 and ECO2012-38442 and Deutsche Forschungsgemeinschaft (SFB 823, project A1) is gratefully acknowledged. We are grateful to the referees for helpful suggestions. The paper also benefitted a lot from detailed comments by Walter Krämer.

References

- Andreou and Ghysels (2002) Andreou, E. and E. Ghysels (2002): “Detecting multiple breaks in financial market volatility dynamics,” Journal of Applied Econometrics, 17(5), 579–600.

- Andrews (1993) Andrews, D. (1993): “Tests for parameter instability and structural change with unknown change point,” Econometrica, 61(4), 821–856.

- Bai (1997) Bai, J. (1997): “Estimating multiple breaks one at a time,” Econometric Theory, 13(3), 315–352.

- Bai and Perron (1998) Bai, J. and P. Perron (1998): “Estimating and testing linear models with multiple structural changes,” Econometrica, 66(1), 47–78.

- Billingsley (1968) Billingsley, P. (1968): Convergence of probability measures, Wiley, New York.

- Campbell et al. (2008) Campbell, R., C. Forbes, K. Koedijk, and P. Kofman (2008): “Increasing correlations or just fat tails?” Journal of Empirical Finance, 15, 287–309.

- Davidson (1994) Davidson, J. (1994): Stochastic limit theory: An introduction for econometricians, Oxford University Press.

- Galeano (2007) Galeano, P. (2007): “The use of cumulative sums for detection of changepoints in the rate parameter of a Poisson Process,” Computational Statistics and Data Analysis, 51(12), 6151–6165.

- Galeano and Tsay (2010) Galeano, P. and R. Tsay (2010): “Shifts in individual parameters of a GARCH model,” Journal of Financial Econometrics, 8(1), 122–153.

- Gooijer (2006) Gooijer, J. D. (2006): “Detecting change-points in multidimensional stochastic processes,” Computational Statistics and Data Analysis, 51(3), 1892–1903.

- Inclán and Tiao (1994) Inclán, C. and G. Tiao (1994): “Use of cumulative sums of squares for retrospective detection of changes of variance,” Journal of the American Statistical Association, 89(427), 913–923.

- Kim and Pollard (1990) Kim, J. and D. Pollard (1990): “Cube root asymptotics,” Annals of Statistics, 18(1), 191–219.

- Krishan et al. (2009) Krishan, C., R. Petkova, and P. Ritchken (2009): “Correlation risk,” Journal of Empirical Finance, 16(3), 353–367.

- Ploberger et al. (1989) Ploberger, W., W. Krämer, and K. Kontrus (1989): “A new test for structural stability in the linear regression model,” Journal of Econometrics, 40(2), 307–318.

- Tse and Tsui (2002) Tse, Y. and A. Tsui (2002): “A Multivariate Generalized Autoregressive Conditional Heteroscedasticity Model with Time-Varying Correlations,” Journal of Business and Economic Statistics, 20(3), 351–362.

- Vostrikova (1981) Vostrikova, L. (1981): “Detecting ’disorder’ in multidimensional random processes,” Soviet Mathematics Doklady, 24, 55–59.

- Wied et al. (2012) Wied, D., W. Krämer, and H. Dehling (2012): “Testing for a change in correlation at an unknown point in time using an extended functional delta method,” Econometric Theory, 28(3), 570–589.

Appendix A Appendix

A.1 The scalar from the test statistic (1)

The scalar from our test statistic based on all observations can be written as

where

and

This is the same expression as in Appendix A.1 in Wied

et al. (2012). The estimator based on the relevant sub-sample is basically calculated in the same way with the respective interval length taken into account.

A.2 Proof of theorems

Proof of Theorem 1

We consider the interval and consider . Denote

Let be the variance estimator from Appendix A.1 calculated from the observations to . It suffices to show consistency of with

because the difference between and is . We first show that converges in distribution to

uniformly in with a constant (where is the limit from under the alternative from Assumption 3). For this purpose, write

with and consider an arbitrary such that . We thus have

Straightforward calculations using the strong law of large numbers (Theorem 20.21 in Davidson, 1994), Slutzky’s theorem, the fact that

and the fact that yield

and

uniformly on .

Consider now the following functions:

As uniform almost sure convergence implies convergence in distribution, the previous results then imply that

for on and also

for rational . The convergence of on then follows from Theorem 4.2 in Billingsley (1968) if we can show that

for all . Note that the separability condition of this theorem is not necessary in our case, because for each interval , is always a random variable when is a right-continuous random function.

With Assumptions 2 and 3, has a unique maximum in the change point fraction.

Let the maximum of for (and as multiples of ). Since we get stochastic convergence of to (compare the argument in Bai and

Perron, 1998, p.77; also an application of the argmax continuous mapping theorem would be possible here).

Proof of Theorem 2

Theorem 1 implies

uniformly for if there is a change point in the interval . Denote the test statistic calculated from data from to . Since

we have

| (5) |

for any sequence if there is a change point in the interval . With this argument (which is partially similar to Corollary 2 in Andrews, 1993), one can adapt the proof of Proposition 11 of Bai (1997).

Consider the event . If the estimated number of change points is smaller than , there is at least one segment with and such that there is another change point . Denote the test statistic calculated from data from to . Since as with (5), we have as . Consider the event . For this event to be true, there must be a false rejection of the null hypothesis at a certain stage in the segmentation procedure. If are the true change points and are the corresponding consistent estimates, it holds

Let be the test statistic computed from data from to . Since under the null hypothesis , it holds

Consequently, for .

Combining the argumentation for the event with Theorem 1 yields the proposed consistency results and the proof is completed.

Proof of Theorem 3

As in the proof of Theorem 1, we derive the limit of . We make use of the fact that the quantitiy can be equivalently written as . This is important because we want to apply an argmax continuous mapping theorem later on which requires that the paths of the limit process almost surely have unique maxima.

In the first step, we adapt the proof of Theorem 2 in Wied et al. (2012) for the case that we consider the interval instead of the interval . The basic difference is that we do not consider the convergence of the process

with from Assumption 7 to a scaled Brownian motion for , but the convergence of the process

to for , which follows by the same functional central limit theorem as used in Wied et al. (2012). With this adaption, we transfer the proof of Theorem 2 in Wied et al. (2012) and get convergence of the process (with from the proof of Theorem 1) to the process

| (6) |

for . Here, , where is the limit of under the sequence of local alternatives that is equal to the limit of under the null hypothesis to which the local alternatives converge.

The result of the theorem then follows with the argmax continuous mapping theorem from Kim and Pollard (1990), Theorem 2.7. This theorem can be applied here because it follows with Lemma 2.6 in Kim and Pollard (1990) that with probability , every path of the Gaussian process 6 has a unique maximum.

Rel. freq. Rel. freq. Rel. freq. .949 .051 .952 .048 .925 .075 .949 .051 .947 .053 .954 .046 .945 .055 .943 .057 .945 .055 .953 .047 .955 .045 .946 .054 .948 .052 .953 .047 .950 .050 .932 .068 .969 .031 .939 .061 .958 .042 .963 .037 .958 .042 .955 .045 .958 .042 .970 .030 .962 .038 .957 .043 .953 .047 .954 .046 .956 .044 .962 .038 .786 .214 .798 .202 .791 .209 .830 .170 .841 .159 .832 .168 .839 .161 .851 .149 .867 .133 .886 .114 .857 .143 .859 .141 .885 .115 .884 .116 .900 .100

Rel. freq. Rel. freq. Rel. freq.

Rel. freq. Rel. freq. Rel. freq.

Rel. freq. Rel. freq. Rel. freq.

Rel. freq. Rel. freq. Rel. freq.

Rel. freq. Rel. freq. Rel. freq.

Rel. freq. Rel. freq. Rel. freq.

Rel. freq. Rel. freq. Rel. freq.

Rel. freq.

Step 1 Interval Change point Time point Date 1.5700 (*) 988 0.2804 November 29, 2000 Step 2 Interval Change point Time point Date 2.1009 (*) 664 0.1884 August 19, 1999 1.4745 2966 0.8417 October 14, 2008 1.0482 157 0.0446 August 14, 1997 1.3471 825 0.2341 April 7, 2000 1.4745 2966 0.8417 October 14, 2008 Step 3 Interval Change point Time point Date 2.1009 (*) 664 0.1884 August 19, 1999 1.6193 (*) 2734 0.7758 November 12, 2007