Parameter estimation of a Lévy copula of a discretely observed bivariate compound Poisson process with an application to operational risk modelling

Abstract

A method is developed to estimate the parameters of a Lévy copula of a discretely observed bivariate compound Poisson process without knowledge of common shocks. The method is tested in a small sample simulation study. Also, the method is applied to a real data set and a goodness of fit test is developed. With the methodology of this work, the Lévy copula becomes a realistic tool of the advanced measurement approach of operational risk.

1 Introduction

The multivariate compound Poisson process is an intuitively appealing and natural model for operational risk and insurance claim modelling. The model is intuitively appealing because dependencies between different loss categories are caused by common shocks that apply to multiple loss categories simultaneously. For example, in operational risk modelling, failure of an IT system is a common shock that causes losses in multiple lines of business. The multivariate compound Poisson process is a natural model for the following two reasons. First, as a Lévy process, it is easily applied to any time horizon of interest. Second, because a redesign of loss categories results in a loss process that is again multivariate compound Poisson, the nature of the model does not depend on the level of granularity (Böcker and Klüppelberg, 2008).

A multivariate compound Poisson process can be specified in terms of univariate compound Poisson processes and a Lévy copula (Cont and Tankov, 2004). In essence, a Lévy copula provides the relationship between the Lévy measure of a multivariate Lévy process and the Lévy measures of its marginal processes. The Lévy copula allows for a parsimonious bottom-up modelling with compound Poisson processes. In case of two loss categories, for example, parameterization with a Clayton Lévy copula requires two marginal frequencies, two marginal jump size distributions and one Lévy copula parameter. In contrast, parameterization without a Lévy copula requires three frequencies (corresponding to losses of the first category only, losses of the second category only and common shocks that apply to both categories), two univariate jump size distributions (corresponding to losses of one of the two categories only) and, finally, one bivariate jump size distribution (corresponding to the common shocks).

The parameters of a Lévy copula of a multivariate compound Poisson process can be estimated if the process is either observed continuously (such that common shocks can be identified) or observed discretely with knowledge about all jump sizes and the common shocks. These two cases have been studied by Esmaeili and Klüppelberg (2010) for a bivariate compound Poisson process (the continuous observation is mimicked in a simulation study, while the discrete observation corresponds to a real data set of insurance claims). The objective of this work is to develop a method to estimate the parameters of a Lévy copula of a bivariate compound Poisson process in case the process is observed discretely with knowledge about all jump sizes, but without knowledge of which jumps stem from common shocks. This situation is relevant to operational risk modelling in which all material losses are registered, but common shocks are typically unknown. With the methodology developed here, the Lévy copula becomes a realistic tool of the advanced measurement approach of operational risk.

The outline of this paper is as follows. In Section 2, we discuss the bivariate compound Poisson process in terms of its common shock representation and Lévy measure. This prepares the ground for the two-dimensional Lévy copula of Section 3. In Section 4, the new estimation method of the discretely observed bivariate compound Poisson process is presented. The method is tested in a simulation study in Section 5 and applied to a real data set in Section 6. In Section 6, we also develop a goodness of fit test for the Lévy copula. Finally, we conclude in Section 7.

2 The bivariate compound Poisson process

A bivariate compound Poisson process is defined on a filtered probability space as

| (1) |

where is a Poisson process with intensity and is a sequence of iid -dimensional random vectors. The process and the sequence are statistically independent. By construction, given any , the increment is independent of and has the same distribution as . The probability distribution of is such that , which means that a jump of almost surely manifests itself in a jump of at least one of the components of .

2.1 The Lévy-Itô decomposition

The Lévy-Itô decomposition of takes the form

| (2) |

where is the Poisson random measure. With the help of the Lévy-Itô decomposition, we find that has common shock representation

| (3) |

where

| (4) |

| (5) |

and

| (6) |

The processes , and do not jump simultaneously and are statistically independent (Sato, 1999). The processes and are called the independent parts of . Conversely, the process is called the dependent part of and corresponds to the common shocks.

2.2 The Lévy-Khinchin representation and the Lévy measure

The Lévy-Khinchin representation of the characteristic function of can be determined from Eq. (2) with the exponential formula for Poisson random measures (Cont and Tankov, 2004). The representation takes the form

| (7) |

where and the Lévy measure

| (8) |

gives the expected number of jumps per unit of time in each Borel set of . The processes and are independent if and only if the support of is contained in the set (Cont and Tankov, 2004). In this case, and do not jump simultaneously almost surely and the Lévy-Khinchin representation factorizes as

| (9) |

On the other hand, the processes and are defined to be comonotonic if their jump sizes and , respectively, are elements of an increasing set of , see (Cont and Tankov, 2004). Any two elements and of satisfy or for all . An example of an increasing set is . The requirement means that by observing one of the processes or , the other process can be constructed exactly with a positive dependence. In case of comonotonic and , the Lévy measure is concentrated on .

In terms of , and , Eq. (7) takes the form

| (10) |

where we have used that , and are independent. The Lévy-Khinchin representation of the characteristic functions of , and can be determined from their Lévy-Itô decompositions in the same way as Eq. (7) is determined from Eq. (2). The Lévy measures of and are given by, respectively,

| (11) |

where is a Borel set of . The Levy measure of takes the form

| (12) |

where the sets and are defined as

| (13) |

To conclude our discussion of the bivariate compound Poisson process , we consider its components for a Lévy measure that is not necessarily concentrated on or an increasing set . The process is compound Poisson (Cont and Tankov, 2004) and by setting in Eq. (10), we find that the characteristic function of takes the form

| (14) |

From Eq. (14), it follows that the Lévy measure of is given by

| (15) |

If the measure is concentrated on , then and if it is concentrated on (such as on an increasing set ), then . In general, is a combination of and cf. Eq. (15). In the same way, is compound Poisson with Lévy measure

| (16) |

3 The Lévy copula

We consider a bivariate compound Poisson process with positive jumps. This means that the Lévy measure is concentrated on rather than on . The assumption of positive jumps is reasonable in the context of operational risk modelling and restricts our discussion of Lévy copulas to positive Lévy copulas.

3.1 The positive Lévy copula and Sklar’s theorem

A two-dimensional positive Lévy copula is a 2-increasing grounded function with uniform margins. The 2-increasing property means that for any and with and , we have

| (17) |

The grounded property means that if and/or . Finally, margins are defined as and , and the positive Lévy copula is such that and .

In the same way as a distributional copula connects marginal distribution functions to a joint distribution function, the Lévy copula connects marginal tail integrals to a tail integral. For a two-dimensional Lévy process with positive jumps, the tail integral is defined as

| (18) |

and the marginal tail integrals are defined as

| (19) |

The following theorem due to Cont and Tankov (2004) is a version of Sklar’s theorem for Lévy copulas.

Theorem 1

Let be a two-dimensional Lévy process with positive jumps having tail integral and marginal tail integrals and . There exists a two-dimensional positive Lévy copula which characterizes the dependence structure of , that is, for all , ,

| (20) |

If and are continuous, this Lévy copula is unique. Otherwise it is unique on .

Conversely, let and be two one-dimensional Lévy processes with positive jumps having tail integrals and and let be a two-dimensional positive Lévy copula. Then there exsists a two-dimensional Lévy process with Lévy copula and marginal tail integrals and . Its tail integral is given by Eq. (20).

The definition of the tail integral and its marginal tail integrals imply that and . The singularity at zero is necessary to correctly account for jumps of the independent parts and . Consider, for example, on the one hand

| (21) |

and, on the other hand

| (22) |

The difference

| (23) |

for between the tail integrals of Eqs. (21) and (22) corresponds to the tail integral of . If would have been defined as , the difference of the tail integrals vanishes and does not jump almost surely.

3.2 Construction of positive Lévy copulas

In case of independent and , the Lévy measure is concentrated on the set and the tail integral takes the form

| (24) |

With the help of Eq. (20), we find that the independence Lévy copula is given by

| (25) |

In case of comonotonic and , the Lévy measure is concentrated on an increasing set and the tail integral takes the form

| (26) |

which implies that the comonotonic Lévy copula is given by

| (27) |

A Lévy copula with a dependence that is between and can be constructed in several ways, such as by an approach similar to the construction of Archimedean distributional copulas (Cont and Tankov, 2004). Given a strictly decreasing convex function such that and , a positive two-dimensional Archimedean Lévy copula is defined as

| (28) |

For with , one obtains the Clayton Lévy copula

| (29) |

The Clayton Lévy copula includes the independence Lévy copula and the comonotonic Lévy copula in the limits and , respectively.

3.3 Dependence implied by the Lévy copula

The bivariate compound Poisson process is fully determined by the Lévy measures , and . Given a Lévy copula , these measures can be expressed in terms of the Lévy measures and . All Lévy measures are defined in the same way as in Section 2, but now is concentrated on . The relation between the measures , and on the one hand, and the measures and on the other, is established in Appendix A. In this Section, for later purposes, the relation between the measures is expressed in terms of frequencies and jump size distributions.

The frequencies and of, respectively, and are given by

| (30) |

where

| (31) |

denote the frequencies of, respectively, , and . In terms of the Lévy copula, takes the form

| (32) |

The survival function of is defined as

| (33) |

where . In terms of the Lévy copula, takes the form

| (34) |

where denotes the survival function of . The distribution function of is related to by

| (35) |

Similarly, the distribution function of is given by . At this point, we have related to , , and . In the same way, the distribution function of is related to , , and the distribution function of . In terms of the survival functions

| (36) |

the relation takes the form

| (37) |

Finally, the joint survival function of is defined as

| (38) |

where . In terms of the Lévy copula, takes the form

| (39) |

The distribution function of is related to by

| (40) |

3.4 Examples of implied dependence

A distributional survival copula of satisfies

| (41) |

where

| (42) |

We assume here that and are continuous, which implies that is unique. For the Clayton Lévy copula (29), substituting

| (43) |

in the left- and right-hand side of Eq. (41) gives

| (44) |

which is the distributional Clayton copula. The distributional copula of takes the form

| (45) |

which collapses to for and to for . The frequency implied by the Clayton Lévy copula takes the form

| (46) |

which collapses to zero for and to for . In summary, for , the Clayton Lévy copula implies and independent components of , while, for , it implies and comonotonic components of .

As a second example, we consider the pure common shock Lévy copula defined by Avanzi et al. (2011) as

| (47) |

For the pure common shock Lévy copula, substituting

| (48) |

in the left- and right-hand side of Eq. (41) gives

| (49) |

which implies that the components of are independent. The frequency implied by the pure common shock Lévy copula takes the form

| (50) |

which equals zero if and if . In summary, the dependence implied by the pure common shock Lévy copula is between frequencies only.

4 Observation scheme and maximum likelihood estimation

We consider a sample of jumps of a positive bivariate compound Poisson process discretely observed up to time . The observation scheme is such that all jump sizes are observed, but it is not known which jumps stem from common shocks. We consider a partition of in intervals of equal length. The partition is chosen such that jumps of separate intervals can realistically be assumed not to stem from common shocks. In the context of operational risk modelling, with either being a month or a quarter, this is the observation scheme typically assumed in the advanced measurement approach.

The objective of this work is to estimate the parameters of the Lévy copula in the observation scheme described above. A possible solution is to construct a likelihood function based on all possible combinations of jumps within each interval. If, within a certain interval, there are jumps within loss category one and jumps within loss category two, one can distinguish between possibilities for the number of common jumps . Given a certain , there are

possibilities of distributing the common jumps over the observed jump sizes. Due to the large number of possibilities, a likelihood function based on all combinations of jumps is not feasible. An alternative approach is to construct a likelihood function based on the number of jumps and the expected jump sizes within the intervals. This approach, however, is also not feasible because the convolutions involved typically have no closed-form expressions. In the method proposed here, we use a sample consisting of the number of jumps and the maximum jump sizes within the intervals. For such a sample, we derive a closed-form likelihood function. Alternatively, a closed-form likelihood function based on the minimum jump sizes can also derived. In the context of operational risk modelling, however, one can expect the likelihood function based on maximum losses to me more variable with respect to model parameters than the likelihood function based on minimum losses.

4.1 Discrete processes for maximum likelihood estimation

We consider a partition of , where , and for all . The discrete process is defined as

| (51) |

where

| (52) |

The random vector is independent of and has the same distribution for all . In the same way as , we define the discrete processes and based on and , respectively. These processes have the same properties as , but, in contrast to , they cannot be observed. The processes and are independent. Also, the components of are independent.

The discrete process is defined as

| (53) |

where the continuous process counts the number of jumps of . The random variable has decomposition

| (54) |

where

| (55) |

Here, the continuous processes and count the number of jumps of and , respectively. The random vector is independent of and has the same distribution for all . In the same way as , we define the discrete process based on . The process is the discrete process corresponding to . The processes and have the same properties as , but, in contrast to , they cannot be observed. The processes and are independent. Also, the components of are independent.

4.2 The likelihood function

Realizations of the process are collected in an matrix such that is a realization of . Similarly, the matrix holds realizations of . The likelihood function corresponding to and takes the form

| (56) |

where denotes the likelihood function of the -th row of and . The entries of and consist of , , the parameters of , the parameters of and, finally, the parameters of the Lévy copula . The function in Eq. (56) has no discrete time label because the distributions of the random vectors do not depend on time. The likelihood function factorizes cf. (56) because random vectors of different discrete time points are independent. The function takes the form

| (57) |

Here, the function is defined as

| (58) |

where we have used that

| (59) |

The functions and with are assumed to be differentiable with respect to the first and second entry, respectively. The functions with are assumed to be continuously differentiable of second order. As we will see later, these assumptions hold if and are continuously differentiable and the Lévy copula is continuously differentiable of second order on .

To find an explicit expression for , we need to calculate and to calculate the conditional probability appearing in Eq. (58). Because , and are statistically independent Poisson random variables with frequencies , and , respectively, we find

| (60) |

The conditional probability appearing in is given by

| (61) |

The conditional probability appearing in with takes the form

| (62) |

where we have used

| (63) |

and the independence of and from and . In terms of the distribution function of defined by Eqs. (34) and (35), Eq. (62) becomes

| (64) |

where we have used that the jump sizes of are iid. The conditional probability appearing in with is treated similarly. Finally, we consider a conditional probability appearing in with . Making use of the independence of the processes , and , we find

| (65) |

where is the distribution function of defined by Eqs. (36) and (37), and is the distribution function of defined by Eqs. (39) and (40).

Substituting the conditional probabilities of Eqs. (61,64,65) in Eq. (58) and subsequently substituting the resulting expression of in Eq. (57), gives

| (66) |

where and are the probability density functions corresponding to, respectively, and . From Eqs. (34) and (35), we find

| (67) |

where is the probability density function corresponding to and is the survival function of . The density exists because and are differentiable. Similarly, from Eqs. (36) and (37), we find

| (68) |

where is the probability density function corresponding to and is the survival function of . The double derivative in the likelihood takes the form

| (69) |

where

| (70) |

From Eqs. (39) and (40), we find

| (71) |

Similarly, takes the form

| (72) |

Finally, the density is given by

| (73) |

The double derivative of Eq. (69) is continuous if and are continuously differentiable, and the Lévy copula is continuously differentiable of second order on . The likelihood function (and thereby ) is now completely specified in terms of the marginal frequencies, the marginal jump size distribution functions and the Lévy copula. In the limit of continuous observation (), the likelihood converges to the likelihood derived by Esmaeili and Klüppelberg (2010).

4.3 Maximizing the likelihood function

The parameters of the process can be estimated by maximizing the likelihood function with respect to all its entries simultaneously. Alternatively, the likelihood function can be maximized with an approach similar to the inference functions for margins (IFM) approach of distributional copulas (Joe and Xu, 1996). The IFM method consists of two steps. In the first step, the parameters of with are estimated by maximizing the marginal likelihood function

| (74) |

where is the vector of jumps of within . In the second step, the estimates of the marginal parameters are substituted in and the resulting likelihood function is maximized with respect to the Lévy copula parameters. The IFM approach seems particularly suitable in the observation scheme of this work because the method makes use of all jump sizes (rather than the maximum jump sizes and the number of jumps in the intervals) in estimating the marginal parameters.

5 A simulation study

The quality of the estimation method of Section 4 is tested in a bootstrap analysis. The analysis consists of sampling many times from on a period and estimating its parameters. The marginal jump size distribution function with is given by

| (75) |

and dependence is introduced by the Clayton Lévy copula of Eq. (29). The process is thus described by five parameters (the marginal frequencies and , the parameters and of the marginal jump size distribution functions and the parameter of the Lévy copula). Given the parameters of the process, the sampling algorithm consists of the following steps:

-

•

Draw and from a Poisson distribution with frequency and , respectively.

-

•

Draw from a Poisson distribution with frequency .

-

•

Draw times from a uniform distribution. The resulting draws are the jump times of . The jump times of are determined similarly.

-

•

Draw times from a uniform distribution and apply the inverse of to each draw. The resulting numbers are the jump sizes of . The jump sizes of are determined similarly.

-

•

Draw times from a uniform distribution and apply the inverse of the marginal distribution function defined as to each draw. The resulting numbers with are the jump sizes of . (Note that the marginal distribution function defined here has one entry. In contrast, the function defined in Eq. (70) with two entries denotes the partial derivative of with respect to the first entry. We will use to denote both functions. The number of entries indicates to which function it refers.)

-

•

Draw times from a uniform distribution. The resulting draws are denoted by with . Apply the inverse of the distribution function , where , to for all . The resulting numbers with are the jump sizes of .

In the last step, we have used that

| (76) |

The algorithm to sample from is the same as the one used by Esmaeili and Klüppelberg (2010) apart from the step where and are drawn. ( These authors first draw , and and then calculate and as and . This method may accidentally work, but it could result in negative and .) To prepare a sample to which we can apply the methods of Section 4, we perform the following steps

-

•

Divide the observation period in intervals of equal length and determine and for all . This results in an matrix of maximum jump sizes. Also determine and for all . This results in an matrix of number of jumps.

-

•

Determine the vector of all jump sizes of on . Similarly, determine the vector of all jump sizes of . (The vectors and are used in the IFM approach.)

The algorithm described above is repeated many times and based on each , , and , the parameters of are estimated. Statistics of the resulting bootstrap estimates are given in Tables I and II for the IFM approach and in Table III for maximum likelihood estimation. From Table I, we find that the difference between the bootstrap mean and the true value of is within a standard error of the mean (bootstrap standard deviation divided by 10). This indicates that the estimate of with the IFM approach is unbiased for the process under study and . From Table II, we find that the estimate of remains unbiased for other values of and . Also, for a fixed value of , the bootstrap standard deviation is seen to be approximately proportional to , which means that the relative precision of the estimate of does not depend on . From Table III, we find that the difference between the bootstrap mean and the true value of is within a standard error of the mean (bootstrap standard deviation divided by ). This indicates that the maximum likelihood estimate of is unbiased for the process under study and . Similarly, from Tables I and III, estimates of the parameters of the marginal processes are seen to be unbiased in both methods. In terms of the bootstrap standard deviations, however, the IFM approach provides estimates of a slightly better quality.

| value | 1000 | 1000 | 1 | 1 | 1 |

|---|---|---|---|---|---|

| bootstrap mean | 1004 | 999 | 0.999 | 1.002 | 1.007 |

| bootstrap standard deviation | 33 | 36 | 0.032 | 0.031 | 0.114 |

| value | bootstrap mean | bootstrap standard deviation | |

|---|---|---|---|

| 50 | 1 | 0.989 | 0.143 |

| 50 | 5 | 4.999 | 0.543 |

| 100 | 1 | 1.007 | 0.114 |

| 100 | 5 | 5.006 | 0.417 |

| value | 1000 | 1000 | 1 | 1 | 1 |

|---|---|---|---|---|---|

| bootstrap mean | 1004 | 997 | 0.993 | 0.994 | 0.992 |

| bootstrap standard deviation | 37 | 39 | 0.036 | 0.042 | 0.113 |

6 A real data analysis

We apply the methodology developed in Section 4 to the Danish fire loss data set publicly available at http://www.ma.hw.ac.uk/~mcneil. The data set consists of fire insurance data divided into loss of building, loss of content and loss of profit. Common shocks are known in this data set and a Lévy copula has already been fitted to the data based on the likelihood function of continuous observation (Esmaeili and Klüppelberg, 2010). To mimick an actual loss data set faced by banks in operational risk modelling, we consider a monthly observation and remove common shock information within months.

6.1 Description of the data and pre-processing

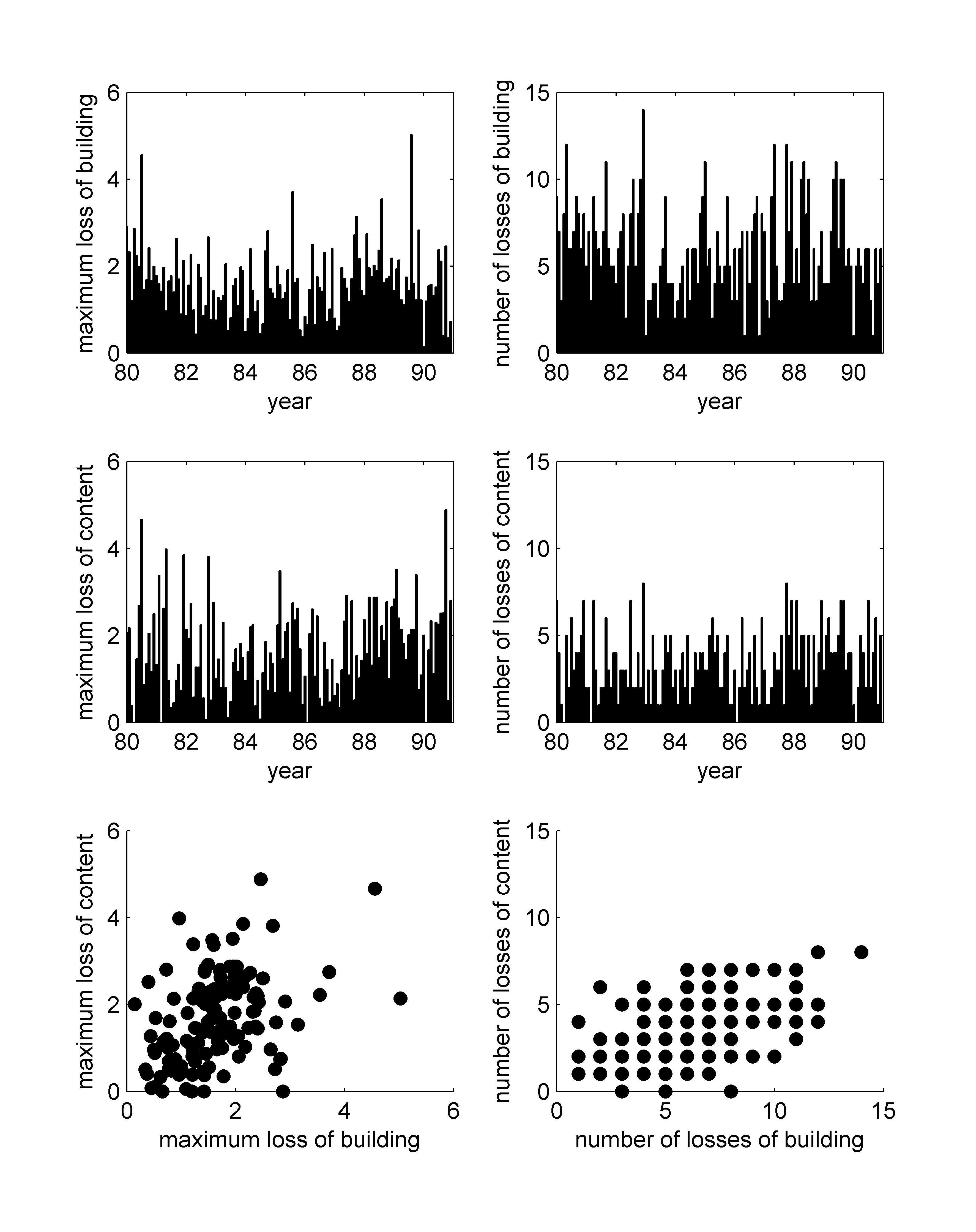

Details about the loss data set are described at its source http://www.ma.hw.ac.uk/~mcneil. The data set consists of 2167 fire loss events over the period 1980 up to 1990 (11 years). They have been adjusted for inflation and are given with respect to the year 1985 in millions of Danish Kroner. Each loss event is divided into a loss of building, a loss of content and a loss of profit. In order to make a comparison with the case of known common shocks studied by Esmaeili and Klüppelberg (2010), we apply the same pre-processing to the data. This means that the loss of profit is not taken into account because it rarely has a non-zero value. For the remaining two loss categories, we consider only losses exceeding a million Kroner and take the logarithm of these losses. The resulting data set consists of 940 transformed loss events.

To prepare a sample for the discretely observed process under study in this work, we consider a monthly partition of the 11 years and determine the maximum loss and the number of losses for each month and each loss category. This results in a matrix of maximum losses and a matrix of number of losses. Details about the maximum losses and the number of losses are given in Figure 1. To prepare for the IFM approach, we construct the vectors and holding, respectively, all losses of building and all losses of content. The vector holds 782 losses and the vector holds 456 losses.

6.2 Marginal processes

We will estimate a Lévy copula with the IFM approach. This means that the parameters of the process of loss of building and the parameters of the process of loss of content are based on, respectively, and . We use the same marginal jump size distributions as Esmaeili and Klüppelberg (2010). These authors use a Weibull distribution function for the log-losses and study the quality of the fit in terms of QQ-plots. The Weibull distribution function of takes the form

| (77) |

where . By maximizing the marginal likelihood function , we find estimates of , and for . The estimates are listed in Table IV.

| estimate | 71.1 | 41.5 | 0.818 | 1.197 | 1.036 | 1.131 |

6.3 A goodness of fit test and selection of a Lévy copula

In the case of continuous observation or known common shocks, one can check if a Lévy copula provides a reasonable fit to the data by inspecting the goodness of fit of the implied distributional copula between the components of . For a Clayton Lévy copula, for example, the implied distributional copula is given by Eq. (45). The goodness of fit of a distributional copula can be assessed by transforming the correponding pseudo sample of probabilities to another sample of probabilities based on the copula (Breymann et al., 2010). If the copula provides a reasonable fit, the transformed probabilities are realizations of statistically independent uniform random variables. This can be tested by applying the inverse of the standard normal distribution function to the random variables and subsequently performing standard statistical tests.

In the discrete observation scheme discussed in this work, common shocks are unknown. In order to test the fit and select a reasonable Lévy copula, we construct a method similar to the goodness of fit test of distributional copulas. For this purpose, we define the distribution function as

| (78) |

For the -th time interval, the probability is calculated as

| (79) |

We calculate the distribution function as

| (80) |

The probability is calculated as

| (81) |

We select the rows of that correspond to the rows of of which both elements are non-zero. These rows correspond to the time intervals in which at least one loss is recorded in both loss categories. The selected rows are collected in a matrix with two columns. In case of the Danish fire loss data, is a matrix. If the data generating process is correctly specified, should be a realization of a random matrix with independent and uniform elements. To test this assumption, we translate into a matrix by

| (82) |

where denotes the standard normal distribution function. The matrix should have independent standard normal elements. For the Danish fire loss data, this is tested for the pure common shock Lévy copula and the Clayton Lévy copula. The results are listed in Table V. For the pure common shock Lévy copula, the estimated correlation coefficient between the columns of deviates from zero at the 0.01 level. This indicates that the pure common shock Lévy copula is probably not appropriate for the data set. In contrast, the Clayton Lévy copula provides a good fit. This is in line with the results of Esmaeili and Klüppelberg (2010).

| Lévy copula | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| pure common shock | 0.79 | 0.60 | -0.01 | -0.01 | 1.04 | 0.95 | 0.09 | 0.05 | 0.25 |

| (0.64) | (0.72) | (0.94) | (0.89) | (0.26) | (0.25) | (0.29) | (0.60) | (0.01) | |

| Clayton | 1.14 | 0.41 | -0.02 | -0.01 | 1.00 | 1.05 | 0.08 | 0.09 | -0.09 |

| (0.52) | (0.80) | (0.77) | (0.92) | (0.46) | (0.21) | (0.38) | (0.31) | (0.29) |

6.4 Estimation results

Based on the analysis of Section 6.3, we use a Clayton Lévy copula to fit the monthly Danish fire loss data. The parameters of the process are estimated with the IFM approach and the results are listed in Table VI. We also estimate with the IFM approach in case of known common shocks. This results in an estimate of 0.903, a bootstrap mean of 0.904 and a bootstrap standard deviation of 0.043. These bootstrap statistics are based on 100 bootstrap samples. As expected, the bootstrap standard deviation with unknown common shocks is larger than with known common shocks. The IFM estimate of 0.903 is close to the maximum likelihood estimate of 0.953 reported by Esmaeili and Klüppelberg (2010).

| estimate | 71.1 | 41.5 | 0.818 | 1.197 | 1.036 | 1.131 | 0.695 |

|---|---|---|---|---|---|---|---|

| bootstrap mean | 70.5 | 41.3 | 0.818 | 1.206 | 1.038 | 1.141 | 0.699 |

| bootstrap standard deviation | 2.6 | 2.1 | 0.024 | 0.034 | 0.047 | 0.046 | 0.092 |

7 Conclusions

In summary, we have developed a method to estimate a Lévy copula of a bivariate compound Poisson process in case the process is observed discretely with knowledge about all jump sizes, but without knowledge of which jumps stem from common shocks. The method is tested in a simulation study with a Clayton Lévy copula. The results indicate that the method is unbiased in small samples and that the bootstrap standard deviation of the Clayton Lévy copula parameter is approximately proportional to its bootstrap mean. A goodness of fit test for the Lévy copula is developed and applied to monthly log-losses of the Danish fire loss data set. The results indicate that the Clayton Lévy copula provides a good fit to the data set.

The method developed in this work is particularly useful in the context of operational risk modelling in which common shocks are typically unknown. To model dependencies between operational losses of different loss categories, the common practice in the banking industry is to use a distributional copula between either the number of losses or the aggregate losses within a certain time window. A disadvantage of this approach is that the distributional copula depends non-trivially on the length of the time window. If one has, for example, estimated a distributional copula between monthly losses, the distributional copula between yearly losses is typically unknown. A second disadvantage of the approach is that the nature of the model depends on the level of granularity. If one combines, for example, two loss categories connected by a distributional copula, the new loss category is typically not compound Poisson. These two issues are resolved by a multivariate compound Poisson process, which can be parsimoniously modelled with a Lévy copula in a bottom-up approach.

Appendix A Connection between Lévy measures

In this Appendix, we relate the Lévy measures , and to the Lévy measures , and the Lévy copula . On a Borel set with , the Lévy measure is given by

| (83) |

which is equivalent to

| (84) |

In terms of

| (85) |

and the Lévy copula, takes the form

| (86) |

Similarly, on a Borel set for , the measure takes the form

| (87) |

Finally, on a Borel set with , the measure is given by

| (88) |

References

- Avanzi et al. (2011) Avanzi, B., Cassar, L. C., and B. Wong, 2011, Modelling dependence in insurance claims processes with Lévy copulas, ASTIN Bulletin 41(2), 575-609.

- Böcker and Klüppelberg (2008) Böcker, K., and C. Klüppelberg, 2008, Modelling and measuring multivariate operational risk with Lévy copulas, The Journal of Operational Risk 3(2), 3-27.

- Breymann et al. (2010) Breymann, W., Dias, A., and P. Embrechts, 2010, Dependence structures for multivariate high-frequency data in finance, Quantitative Finance 3(1), 1-14.

- Cont and Tankov (2004) Cont, R., and P. Tankov, 2004, Financial Modelling with Jump Processes (Chapman & Hall/CRC, Boca Raton).

- Esmaeili and Klüppelberg (2010) Esmaeilli, H., and C. Klüppelberg, 2010, Parameter estimation of a bivariate compound Poisson process, Insurance: Mathematics and Economics 47(2), 224-233.

- Jarque and Bera (1980) Jarque, C. H., and A. K. Bera, 1980, Efficient tests for normality, homoscedasticity and serial independence of regression residuals, Economics Letters 6(3), 255-259.

- Joe and Xu (1996) Joe, H., and J. J. Xu, 1996, The estimation method of inference functions for margins for multivariate models, Technical Report no. 166, Department of Statistics, University of British Columbia.

- Sato (1999) Sato, K.-I., 1999, Lévy Processes and Infinitely Divisible Distributions (Cambridge University Press, Cambridge).