A zero-sum game between a singular stochastic controller

and a discretionary stopper

Daniel Hernandez-Hernandezlabel=e1]dher@cimat.mx

[Robert S. Simonlabel=e2]r.s.simon@lse.ac.uk

[Mihail Zervoslabel=e3]mihalis.zervos@gmail.com

[

Centro de

Investigación en Matemáticas, London School of Economics and

London School of Economics

D. Hernandez-Hernandez

Centro de

Investigación en Matemáticas

Apartado Postal 402

Guanajuato GTO 36000

Mexico

R. S. Simon

M. Zervos

Department of Mathematics

London School of Economics

Houghton Street

London

WC2A 2AE

United Kingdom

E-mail:e3

(2015; 11 2012; 6 2013)

Abstract

We consider a stochastic differential equation that is controlled

by means of an additive finite-variation process.

A singular stochastic controller, who is a minimizer, determines

this finite-variation process, while a discretionary stopper, who

is a maximizer, chooses a stopping time at which the game

terminates.

We consider two closely related games that are differentiated

by whether the controller or the stopper has a first-move

advantage.

The games’ performance indices involve a running payoff as well

as a terminal payoff and penalize control effort expenditure.

We derive a set of variational inequalities that can fully

characterize the games’ value functions as well as yield

Markovian optimal strategies.

In particular, we derive the explicit solutions to two special

cases and we show that, in general, the games’ value functions

fail to be .

The nonuniqueness of the optimal strategy is an interesting

feature of the game in which the controller has the first-move

advantage.

91A15,

93E20,

60G40,

Zero-sum games,

singular stochastic control,

optimal stopping,

variational inequalities,

doi:

10.1214/13-AAP986

keywords:

[class=AMS]

keywords:

††volume: 25††issue: 1

,

and

1 Introduction

We consider a one-dimensional càglàd process

that satisfies the stochastic differential equation

(1)

where is a càglàd finite variation adapted process

such that , and is a standard one-dimensional

Brownian motion.

The games that we analyze involve a controller, who is a

minimizer and chooses a process , and a stopper, who

is a maximizer and chooses a stopping time .

The two agents share the same performance criterion, which

is given either by

(2)

or by

(3)

where is the total variation process of

and

(4)

for some positive functions .

The performance index reflects a situation where

the stopper has the “first-move advantage” relative to the

controller.

Indeed, if the controller makes a choice such that and the stopper chooses , then

.

On the other hand, the performance index reflects

a situation where the controller has the “first-move advantage”

relative to the stopper: if the controller makes a choice such

that , and the stopper chooses ,

then .

Given an initial condition , is an

optimal strategy if

(5)

for all admissible strategies , where “”

stands for either “” or “.”

If optimal strategies ,

exist for the two games for every initial condition

, then we define the games’ value functions by

(6)

respectively.

Zero-sum games involving a controller and a stopper were

originally studied by Maitra and Sudderth MS in a discrete

time setting.

Later, Karatzas and Sudderth KS derived the explicit

solution to a game in which the state process is a one-dimensional

diffusion with absorption at the endpoints of a bounded

interval, while, Weerasinghe W derived the explicit

solution to a similar game in which the controlled volatility

is allowed to vanish.

Karatzas and Zamfirescu KZ2 developed a martingale

approach to general controller and stopper games, while,

Bayraktar and Huang BH showed that the value function

of such games is the unique viscosity solution to an appropriate

Hamilton–Jacobi–Bellman equation if the state process is a

controlled multi-dimensional diffusion.

Further games involving control as well as discretionary stopping

have been studied by Hamadène and Lepeltier HL

and Hamadène H .

To a large extent, controller and stopper games have been

motivated by several applications in mathematical finance and

insurance, including the pricing and hedging of American

contingent claims (e.g., see Karatzas and Wang KW )

and the minimization of the lifetime ruin probability; for example,

see Bayraktar and Young BY .

Games such as the ones we study here arise in the context of

several applications.

To fix ideas, consider the singular stochastic control problem

that aims at minimizing the performance criterion

over all controlled processes subject to the dynamics

given by (1).

The solution to the special case of this problem that arises when

, , is a constant

and , for some , was derived

by Karatzas K and is characterized by a constant :

it is optimal to exercise minimal control so as to keep the

state process inside the range at all times.

The qualitative nature of such a solution has lead to the study

of several applications in which one wants to keep a state process

within an optimal range by means of singular stochastic control.

Such applications include: spaceship control (see Bather

and Chernoff BC who introduced singular stochastic

control) where, for example, represents the deviation of a satellite

from a given altitude and represents fuel expenditure;

the control of an exchange rate (see Miller and Zhang MZ )

or an inflation rate (see Chiarolla and Haussmann CH )

where, for example, models a rate or the fluctuations of a rate

around a target, and models the central bank’s cumulative

intervention efforts; the so-called goodwill problem

(see Jack, Jonhnson and Zervos JJZ ) where, for example,

is used to model the image that a product has in a

market, and represents the cumulative costs associated

with raising the product’s image, for example, through

advertising.111We have

included here only one indicative reference for each of the

areas mentioned because there is a rich literature

for each of them.

Any of the applications discussed in the previous paragraph

can give rise to a zero-sum game between a controller and

a stopper that are different incarnations of the same decision

maker.

Such games in which the players model competing

objectives of the same decision maker have attracted

considerable interest in the context of several applications.

For instance, they have been studied in the context

of robust optimization where “the agent maximizes utility by

his choice of control, while an evil agent minimizes utility by

his choice of perturbation” (Williams NW ), or

in the context of time-consistent optimization where

a decision maker’s problem is analyzed as a “game between

successive selves, each of whom can commit for an infinitesimally

small amount of time” (Ekeland, Mbodji and Pirvu EMP ).

In what follows, we focus on one of the applications of the

games that we study (several others arising in the context

of the ones discussed in the previous paragraph can be

developed following similar arguments).

Consider a central bank that intervenes to keep fluctuations

of an exchange rate within an optimal range.

At any time, the central bank could be confronted with the

costs of their policy, in particular, with the demand that

its board should be replaced.

In this context, the controller can represent the central bank’s

targeting efforts, while the stopper can represent a

political veto on their policy.

In abstract terms, such a problem can be viewed as one of

optimization by a single agent.

However, its analysis and solution requires its formulation

as a zero-sum game.

Indeed, the conflicting natures of such a decision maker’s

objectives do not really allow for them to be addressed

by solving a (one-player) stochastic optimization problem.

For instance, the solution to the one-player problem derived by

Davis and Zervos DZ94 , which is akin to the special

case we solve in Section 5, involves markedly

different optimal strategies that would be absurd in the context

of an applications such as the one we discuss here.

In particular, the controller tries to minimize, for example, the

performance index given by (3).

From the controller’s perspective, penalizes large

fluctuations of the targeted rate for choices such as

, for some , as well as

the expenditure of intervention effort.

On the other hand, the stopper tries to maximize the same

performance criterion because large values of

indicate that intervention is “expensive,” namely,

unsustainable.

From the stopper’s perspective, the choice of the reward

function can be used to further quantify the bank’s reluctance

to intervene, for example, in situations where the rate assumes values

way off the target.

Furthermore, the choice of rather than

can be associated with a central bank that is more, rather

than less, keen to intervene.

The development of a theory for zero-sum games such

as the ones we study can therefore provide a useful

analytic tool to decision makers such as a central bank

in their considerations on whether and how to optimally

target a state process such as an exchange rate.

Such analytic tools can be most valuable because getting

a policy wrong can have rather extreme economic

and political consequences.

For instance, one can recall the UK’s crash out of the

European Exchange Rate Mechanism (ERM) in 1992.

The games that we study here are the very first ones involving

singular stochastic control and discretionary stopping.

Combining the intuition underlying the solution of standard

singular stochastic control problems and standard optimal

stopping problems by means of variational inequalities (e.g.,

see Karatzas K and Peskir and Shiryaev PS ,

resp.), we derive a system of inequalities that can fully

characterize the value function .

We further show that these inequalities can also characterize

the value function as well as an optimal strategy.

Surprisingly, we have not seen a way to combine all of them

into a single equation.

Our main results include the proof of a verification theorem

that establishes sufficient conditions for a solution to these

inequalities to identify with the value function and yield

the value function as well as an optimal strategy, which

we fully characterize.

In this context, we also show that the two games we consider

share the same optimal strategy, and we prove that

The nonuniqueness of the optimal strategy when the

controller has the first-move advantage is an interesting

result that arises from our analysis; see Remark 1

at the end of Section 4.

We then derive the explicit solutions to two special cases.

The first one is the special case that arises if is a

standard Brownian motion, and , are quadratics.

In this case, the value function is , but the

regularity of the value function may fail at a couple

of points.

The second special case is a simpler example revealing

that both of the value functions and may fail to be

at certain points and showing that the optimal strategy

may take qualitatively different form, depending on

parameter values.

The paper is organized as follows.

Notation and assumptions are described in Section 2,

while, a heuristic derivation of the system of inequalities

characterizing the solution to the two games is developed

in Section 3 (see Definition 1).

In Section 4, the main results of the paper, namely, a

verification theorem (Theorem 1) and the

construction of the optimal controlled process associated

with a function satisfying the requirements of Definition 1

(Lemma 1) are proved.

In Sections 5 and 6, the explicit

solutions to two nontrivial special cases are derived.

2 Notation and assumptions

We fix a filtered probability space satisfying

the usual conditions and carrying a standard one-dimensional

-Brownian motion .

We denote by the set of all -stopping

times and by the family of all -adapted

finite-variation càglàd processes such that .

Every process admits the decomposition

where

, are -adapted

finite-variation càglàd processes such that

has continuous sample paths,

where for .

Given such a decomposition, there exist -adapted

continuous processes ,

such that

where is the total variation

process of .

The following assumption that we make implies that, given

any , (1) has a unique strong solution;

see Protter P , Theorem V.7.

Assumption 1.

The functions

satisfy

for some constant , and

for all , for some constant .

We also make the following assumption on the data of the

reward functionals defined by (2)–(4).

Assumption 2.

The functions are

continuous, and there exists a constant

such that for all .

It is worth noting at this point that, given ,

we may have , for some .

In such a case, the reward functionals given by

(2)–(3) are well defined but may take the

value .

3 Heuristic derivation of variational inequalities for the value function

Before addressing the game, we consider the optimization

problems faced by the two players in the absence of

competition.

To this end, we consider any bounded interval , we denote by (resp.,

) the first hitting time of

(resp., ), and we fix any constants

.

Given an initial condition , a controller is concerned with solving the singular

stochastic control problem whose value function is given by

(7)

In the presence of Assumptions 1 and 2,

is with absolutely continuous

first derivative and identifies with the solution to the

variational inequality

with boundary conditions

where the operator is defined by

(8)

see Sun S , Theorem 3.2.

In this case, it is optimal to exercise minimal action so

that the state process is kept outside the interior

of the set

Given an initial condition , a stopper faces the discretionary stopping

problem whose value function is given by

(9)

where is the solution to (1) for .

In this case, Assumptions 1 and 2

ensure that is the difference of two

convex functions and identifies with the solution, in an

appropriate distributional sense, to the variational inequality

with boundary conditions

where is defined by (8); see Lamberton and

Zervos LZ , Theorems 12 and 13.

In this case, the optimal stopping time

identifies with the first hitting time of the so-called stopping

region

namely, .

Now, we consider the game where the controller has

the “first-move advantage” relative to the stopper, and we

assume that there exists a Markovian optimal

strategy for the sake of the discussion

in this section.

We expect that this optimal strategy involves the

same tactics as the ones we have discussed above.

From the perspective of the controller, the state space

splits into a control region and a

waiting region .

Accordingly, should involve minimal action to

keep the state process in the closure of the waiting region

for as long as the stopper

does not terminate the game.

Similarly, from the perspective of the stopper, the state

space splits into a stopping region

and a waiting region ,

and is the first hitting time of .

Inside any bounded interval , the

requirement that should satisfy (5)

suggests that should identify with

defined by (3) for

and .

Therefore, we expect that should satisfy

(10)

Inside any bounded interval , the

requirement that should satisfy (5)

suggests that should identify with

defined by (3) for

and .

Therefore, we expect that should satisfy

(11)

To couple variational inequalities (10) and

(11), we consider four possibilities.

The region where both players should

wait is associated with the inequalities

(12)

Inside the set

where the stopper should wait, whereas,

the controller should act, we expect that

(13)

Inside the part of the state space where

the controller would rather wait if the stopper deviated

from the optimal strategy and did not terminate the

game, we expect that

(14)

Finally, the region in which

the stopper should terminate the game should the controller

deviate from the optimal strategy and did not act, we expect that

(15)

These inequalities give rise to the following definition.

Here, as well as in the rest of the paper, we denote by

and the interior and the closure of a set , respectively.

Definition 1.

A candidate for the value function is a continuous

function that is with absolutely

continuous first derivative inside ,

where is a finite set, satisfies

and has the following properties, where

{longlist}

[(III)]

Each of the sets , and

is a finite union of intervals, and

.

satisfies

If we denote by [resp., ] the left-hand

(resp., right-hand) derivative of at ,

then

for all .

In the following definition, we introduce some terminology

we are going to use.

Definition 2.

Given a function satisfying the conditions of Definition 1,

we call the regions , and

waiting, control and stopping, respectively.

Also, we call reflecting all finite boundary points of

such that

for all sufficiently small, and repelling

all other finite boundary points of .

It is worth noting that requirement (III) of Definition 1

implies that all points in are repelling.

The special case that we solve in Section 5

involves only reflecting boundary points.

On the other hand, the special case that we solve in

Section 6 involves repelling as well as

reflecting points and .

4 A verification theorem

Before addressing the main result on this section, namely

Theorem 1, we consider the following result,

which is concerned with the construction of the process

that is part of the optimal strategy associated with

a given function satisfying the requirements of

Definition 1.

The main idea of its proof is to paste solutions to (1)

that are reflecting in appropriate boundary points.

Lemma 1

Consider a function that satisfies

the conditions of Definition 1.

There exists a controlled process

such that

Given a finite interval and a controlled process

, suppose that there exists a point and an -stopping time with

such that the solution to (1) is such

that on the event .

On the probability space , where

is the filtration defined by and is

the conditional probability measure

that has Radon–Nikodym derivative with respect to given by

the process defined by is a standard -Brownian

motion that is independent of ; see Revuz

and Yor RY , Exercise IV.3.21.

In this context, there exist -adapted continuous

processes and such that is a

finite variation process,

(21)

see El Karoui and Chaleyat-Maurel EC and

Schmidt Sc .

Since is an -stopping time,

and for all ,

see Revuz and Yor RY , Propositions V.1.4, V.1.5.

Similarly we can see, for example, that

In view of this observation, we can see that, if we define

Using the same arguments and references, we can show that,

given an interval , a point , a controlled process and an

-stopping time such that the solution to (1)

is such that on the event ,

there exist processes and

satisfying (1) and such that

(24)

(25)

(26)

Similarly, given an interval , a

point , a controlled

process and an -stopping time

such that the solution to (1) is such that

on the event , there

exist processes and

satisfying (1) and such that

(27)

(28)

(29)

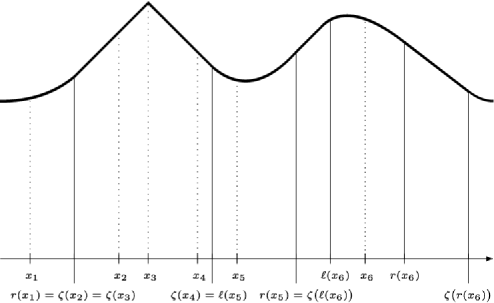

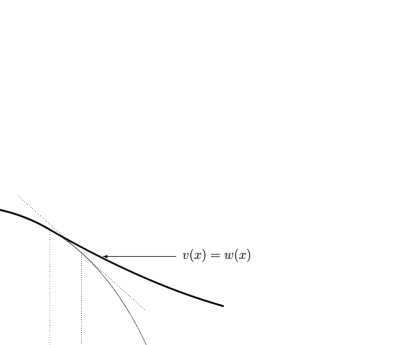

Figure 1: Illustration of

the functions , , appearing

in the proof of Lemma 1. The vertical

solid lines also demarcate the region .

Given a function that satisfies the requirements of

Definition 1, we now use the notation and the

terminology introduced by Definitions 1

and 2 to iteratively construct a process

such that (1)–(1)

hold true by means of the constructions above.

To this end, we introduce the following notation,

which is illustrated by Figure 1.

If and

, then we recall that we use

[resp., ] to denote the left-hand (resp., the

right-hand) first derivative of at , we define

and we note that because is

real-valued.

On the other hand, given any , we define

with the usual conventions that and .

The algorithm that we now develop terminates after finite

iterations because each of the sets ,

is a finite union of intervals.

STEP 0: Initialization.

We consider the following four possibilities that can happen,

depending on the initial condition of (1):

If and

(e.g., see the

points , , in Figure 1), then we define

for all .

If we denote by the corresponding solution to

(1), and we set , then has a single

jump at time ,

In this case, if .

If and , which is the

case if ,

then we define , we denote by the

corresponding solution to (1), and we let .

If ,

and either of , is reflecting (e.g., see

the points , in Figure 1), then we

define , we denote by the

corresponding solution to (1), and we set .

If ,

,

and both , are repelling if finite

(e.g., see the point in Figure 1), then we

consider the -stopping times

in which expression, we define [resp., ] arbitrarily

if [resp., ].

If we denote by the corresponding solution to

(1), and we set ,

then has a single jump at the -stopping

time ,

In this case, we may have

but and for all .

STEP 1: Induction hypothesis.

We assume that we have determined an -stopping

time , and we have constructed a process such that, if we denote by the

associated solution to (1), then (1)–(1)

are satisfied for , in place of ,

and for all instead of all positive .

Also, we assume that, if ,

then one of the following two possibilities occur:

{longlist}[(II)]

there exists a point such that on the event ;

there exist points , and events

forming a partition of

such that ,

on the event and at

least one of , is finite and

reflecting, for .

Step 0 provides such a construction for .

In particular, the last possibility there gives rise to

Case (II) for

On the other hand, the second possibility there is

such that , while the

remaining two possibilities give rise to Case (I).

STEP 2.

If , then define ,

and stop.

Otherwise, we proceed to the next step.

STEP 3.

We address the situation arising in the context

of Case (II) of Step 1; the analysis regarding Case (I)

is simpler and follows exactly the same steps.

To this end, we first consider the -stopping

time , and we note that

on the event .

We are faced with the following possible cases.

If both of , are finite and reflecting,

then we appeal to the construction associated with

(22)–(4) for , , and to obtain processes

, that are equal to ,

up to time and satisfy (4) for all .

We then define

The result of this construction is such that

on the event

, which puts us in the

context of Case (I) of Step 1.

If is finite and reflecting and [resp., and

is finite and reflecting], then we proceed in the same

way using the construction associated with

(24)–(25) [resp., (27)–(28)].

If is finite and reflecting and

is finite and repelling, then we consider (24)–(25)

and, as above, we construct processes ,

that are equal to , up to time

and satisfy (25) for all .

We then consider the -stopping time and the process

given by

we denote by the associated solution to

(1), and we define

In this case, we may have but

and for all .

Finally, if is finite and repelling, and

is finite and reflecting, then we are faced

with a construction that is symmetric to the very last

one using (27)–(28).

STEP 4.

Go back to Step 2.

We now prove the main result of the section.

It is worth noting that we can relax significantly assumptions

(34)–(35).

However, we have opted against any such relaxation because

(a) this would require a considerable amount of extra arguments

of a technical nature that would obscure the main ideas of the

proof, and (b) (34)–(35) are

plainly satisfied in the special cases that we explicitly solve

in Sections 5 and 6.

Theorem 1

Consider a function that satisfies the

conditions of Definition 1, let be

the control strategy constructed in Lemma 1,

let be the associated solution to (1) and define

(32)

Also, given any , define

where is the associated solution to (1), and note

that .

In this context, the following statements are true:

{longlist}[(III)]

If satisfies (35), then

[resp., ] is an optimal strategy for the game

with performance criterion given by (2) [resp., (3)]

and and are the value functions of the two games.

{pf}

Given a function satisfying the conditions of

Definition 1, we denote by the unique,

Lebesgue-a.e., first derivative of in , and we define , arbitrarily

for in the finite set .

In view of (1), we can use Itô’s formula and the

integration by parts formula to calculate

It follows that, given any finite -stopping time

,

(37)

Similarly, we can calculate

(38)

Combining (4) with (1) and

the facts that for all and

Lebesgue-a.e. in , we can see

that, given any and any -stopping

time ,

(39)

the last inequality following thanks to (32).

These inequalities and the positivity of , imply

that the stopped process

is a supermartingale and .

Therefore, we can take expectations in (4)

and pass to the limit using Fatou’s

lemma to obtain the inequality .

With reasoning similar to (4), we derive

the inequality ,

and (I) follows.

To prove (II), we consider the -stopping time

defined by (1) with instead of

, and we note that

Combining this observation and the definition of

with the facts that for all

and for all , we can see that

In view of these observations, (4) and the fact

that Lebesgue-a.e. in , we can

see that, given any ,

If we denote by a localizing sequence

for the stopped local martingale such that

for all , then we can see that

these identities imply that

In view of (34) and Assumption 2,

we can pass to the limit as using the

monotone and the dominated convergence theorems to

obtain .

To establish Part (III), we consider any admissible and we note that (4) remains true with

, instead of , if is replaced

by because .

Also, we note that

(40)

In view of the facts that for all and for all , we can see that this observation and the definition

of imply that

Combining these observations with the fact that

Lebesgue-a.e. inside

,

we can see that (4) implies that, given any ,

where is defined as in (36).

If is a localizing sequence for the stopped local

martingale such that for all

, then these inequalities imply that

In view of (35) and Assumption 2,

we can pass to the limit as using the

monotone and the dominated convergence theorems to obtain

.

In general, the inequality may be

strict because, for example, we may have and .

In such a case, the set may not be empty, but it is finite.

Therefore, we can use Itô’s formula to derive (4)

with , instead of , and with replacing .

Combining this result with the observations that

we can derive the inequality as above.

Finally, Part (IV) follows immediately from Parts (I)–(III).

Remark 1.

An inspection of the proof of Theorem 1

reveals that the optimal strategy of the game

where the controller has the first-move advantage is highly

nonunique.

Indeed, in the presence of (35), , where is any

-stopping time such that ,

in particular, , is also an optimal strategy.

It is worth noting that a similar observation cannot be made

for the game where the stopper has the first-move

advantage.

Both of the special cases considered in the following two

sections provide cases illustrating this situation; see

Propositions 4, 5,

7 and 8.

5 The explicit solution to a special case with quadratic

reward functions

We now derive the explicit solution to the special case of

the general problem that arises when

for some constants and

.

In our analysis, we exploit the symmetry around

the origin that the problem has, we consider only

sets such that

and we denote

.

Also, we recall that the general solution to the ODE

is given by

for some constants .

In the special case that we consider in this section, the

controller should exert effort to keep the state process

close to the origin.

On the other hand, the stopper should terminate the game

if the state process is sufficiently far from the origin.

In view of these observations, we derive optimal strategies

by considering functions satisfying the requirements of

Definition 1 that are associated with the regions

(41)

for some constants ; see

Definition 1.

In particular, we derive three qualitatively different cases

that are characterized by the relations ,

or , depending on

parameter values; see Figures 2–4 as well as

Remark 2.

In this context,

Theorem 1 implies that the associated optimal

strategies can be described informally as follows.

The controlled process has an initial jump equal

to [resp., ] if the initial condition

of (1) is such that (resp., ).

Beyond time 0, is such that the associated

solution to (1) is reflecting in in the positive

direction and in in the negative direction.

On the other hand, the optimal stopping times ,

are the first hitting times of

as defined by (1).

In view of these observations, we focus on the construction

of the function satisfying the requirements of

Definition 1 in what follows.

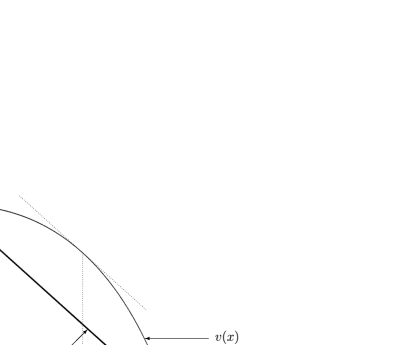

Figure 2: The functions

and in the context of Proposition 2

().

In the first case that we consider, identifies with the value

function of the singular stochastic control problem that arises

if the stopper never terminates the game (see Figure 2).

In particular, we look for a solution to the variational inequality

(42)

of the form

(43)

The requirement that should be along the

free-boundary point , which is associated with the

so-called “principle of smooth fit” of singular stochastic

control, implies that the parameter should be given by

(44)

while should satisfy

(45)

We also define to be the unique solution to

the equation

(46)

We prove the following result, as well as the other ones

we consider in this section, in Appendix I.

Proposition 2

Equation (45) has a unique solution ,

which is strictly greater than ,

while equation (46) has a unique solution

.

Furthermore, if and only if

in which case, and the

function defined by (43) for , given by

(44), satisfies the conditions of Definition 1; see

Figure 2 for a depiction of the value functions

and .

We next consider the possibility that the value function of the

game where the stopper has the “first-move advantage” identifies

with the value function of the optimal stopping problem that

arises if the controller never acts; see Figure 3.

Figure 3: The functions

and in the context of Proposition 3

().

In this case, we look for a solution to the variational inequality

of the form

(48)

The requirement that should be along the

free-boundary point , which is associated with

the so-called “principle of smooth fit” of optimal stopping,

implies that the parameter should be given by

(49)

while should satisfy

(50)

In this context, the function defined by

(51)

provides an appropriate choice for a function satisfying the

requirements of Definition 1 as long as .

Proposition 3

Suppose that .

Equation (50) has a unique solution ,

which is strictly greater than .

This solution is less than or equal to if

and only if

(52)

in which case, the function defined by (51)

for , given by (49), satisfies the requirements

of Definition 1; see Figure 3 for a depiction of the

value functions and .

The third case that we consider “bridges” the previous

two and is characterized by the fact that the

free-boundary points , may coincide

in a generic way.

In particular, we look for a function satisfying the

requirements of Definition 1 that is given by

(53)

for some , and satisfies

(54)

see Figure 4.

The requirements that should satisfy (54)

and be at imply that the parameter

should be given by

(55)

while the free-boundary point should satisfy

(56)

Proposition 4

Suppose that and .

Figure 4: The functions

and in the context of Propositions 4

and 5 ().

If the parameters are such that (57) is true,

then the function defined by (53) for , given

by (55), satisfies the conditions of Definition 1

if and only if

(59)

On the other hand, if the parameters are such that

(58) is true, then

if and only if

(60)

in which case, the function defined by (53) for

, given by (55), satisfies the conditions of

Definition 1; see Figure 4 for a depiction of the

value functions and .

The results that we have established thus far involve

mutually exclusive conditions on the problem data.

To exhaust all possible parameter values, we need to

consider the following result that is associated with

the regions

(61)

which are consistent with (41) for , and the proof of which

is straightforward.

Proposition 5

Suppose that and .

The function defined by

(62)

is a function that satisfies the requirements of

Definition 1.

Remark 2.

Suppose that .

The conditions differentiating between the different cases

we have considered are mutually exclusive and exhaustive

in the sense that they cover the entire range of possible

parameter values.

To see this claim, we define

and

(63)

In view of the implications

we can see that the following table summarizes the conditions

of Propositions 2, 3,

4 and 5:

then , and we are in the context of

Proposition 2 if

then ,

, and we are in the

context of Proposition 3 if

then ,

, and we are in the context

of Proposition 4, while if

then , and we

are again in the context of Proposition 4.

6 A special case with value functions that are not

We now solve the special case of the general problem that arises

when

for some constants .

In this context, the controller has no incentive to exert any

control action other than to counter the stopper’s action

because .

We therefore solve the problem by first viewing the game

from the stopper’s perspective.

Also, we exploit the problem’s symmetry around the origin

in the same way as in the previous section.

We first consider the possibility that a function satisfying

the requirements of Definition 1 identifies with the value

function of the optimal stopping problem that arises if the

controller never takes any action.

To this end, we look for a solution to the variational inequality

of the form

(64)

for some constants and .

A function of this form is associated with the regions

(65)

and is depicted by Figure 5.

To determine the constant and the free-boundary point

, we appeal to the so-called “principle of smooth-fit”

of optimal stopping.

We therefore require that is at and

to obtain

(66)

In this case, Theorem 1 implies that the

associated optimal strategy can be described informally

as follows.

The controller should never act (i.e., ), while the

stopper should terminate the game as soon as the state

process takes values in

(i.e., is the first hitting time of

).

Figure 5: The functions

and in the context of Proposition 6.

We prove the following result, as well as the other ones

we consider in this section, in Appendix II.

Proposition 6

The function defined by (64) for , given by (66) satisfies the

requirements of Definition 1 if and only if

(67)

see Figure 5 for a depiction of the value functions

and .

If the problem data is such that (67) is not true,

then we consider the possibility that an optimal

strategy is characterized by a function satisfying the

requirements of Definition 1 that is associated

with the regions

for some , and is depicted by

Figure 6.

In particular, we consider the function

(69)

The requirement that should be continuous at

yields

(70)

while, the requirement that should be along

, , implies that

(71)

Figure 6: The functions

and in the context of Proposition 7.

In view of Theorem 1, we can describe

informally the associated optimal strategy as follows.

If the initial condition of (1) belongs to

, then the controller should wait

until the uncontrolled state process hits , at which time, the controller should apply an impulse

to instantaneously reposition the state process at

or , whichever point is closest.

As soon as the state process takes values in (resp., ), the

controller should exert minimal effort to reflect the state

process in in the negative direction (resp., in

in the positive direction).

Figure 7: The functions

and in the context of Proposition 8.

On the other hand, the stopper should terminate

the game as soon as the state process takes values

in .

Proposition 7

The point defined by (71) is

strictly greater than , and there

exists satisfying (70)

if and only if

(72)

in which case, .

If the problem data satisfy these inequalities, then the

function defined by (69), for , given by (71), satisfies the

conditions of Definition 1; see Figure 6 for a

depiction of the value functions and .

The final possibility that may arise is associated with the

regions

(73)

for some , and is depicted by

Figure 7.

In this case, a function satisfying the requirements of

Definition 1 is given by

(74)

The constant and the free-boundary point

are characterized by the requirement that should be

along , , and are given by (71).

In this case, Theorem 1 implies that the

associated optimal strategy can be described informally

as follows.

The controlled process has an initial jump equal

to [resp., ] if the initial condition

of (1) is such that

(resp., ).

Beyond time 0, is such that the associated

solution to (1) is reflecting in in the negative

direction if and in in the

positive direction if .

On the other hand, the stopping time is the first hitting time of .

Proposition 8

The function defined by (69) for ,

given by (71)

satisfies the conditions of Definition 1

if and only if

(75)

see Figure 7 for a depiction of the value functions

and .

Proof of Proposition 2

It is straightforward to see that equation (45) has

a unique solution and that this solution is strictly

greater than .

In particular, we can verify that

(76)

For this value of and for given by (44),

the function defined by (43) is and satisfies

the variational inequality (42) because

(77)

To see (77), we first note that for all

, which implies that the restriction of

in is strictly decreasing.

Combining this observation with the identities

we can see that for all .

It follows that is an even convex function, which, combined

with the identities and , implies (77).

The definition and the continuity of imply that

, for .

Combining this observation with the inequality for all ,

which follows from the fact that ,

we can see that (79) is true.

To see that equation (46) has a unique solution

, we define .

In view of the calculations

we can see that either is convex, or there exists

such that for

all and for all .

In the first case, for all , while,

in the second case, there exists such that

for all and

for all because .

In either case, we can see that the equation has a unique solution because

To show that the point defined by (46)

is strictly greater than if and only if (2) is true,

we note that the linearity of in implies that

there exists such that (46) is

true if and only if .

In particular, if such exists, then .

Using the definition (43) of , we calculate

If , then this identity implies trivially

that

(80)

Similarly, if and , then

(80) is true.

On the other hand, if ,

then (80) is true if and only if because the function is strictly decreasing in .

Therefore, if , then (80)

is true if and only if the very last inequality in (2) holds

true, thanks to (76).

It follows that the equation has a unique

solution if and only if

(2) is true.

Finally, it is straightforward to check that, if (2) is

true, then is associated with the regions , ,

and ,

and satisfies all of the conditions required by

Definition 1.

implies that the right-hand side of (50) defines a strictly

decreasing function on .

Combining this observation with the fact that is a strictly

increasing function, we can see that (50) has a

unique solution and that this solution is strictly

greater than .

In particular, we can see that

(81)

which implies that the solution of (50) is

less than or equal to if and only if the

inequalities in (52) are true.

In what follows, we assume that the problem data satisfy

(52), in which case, is associated with the

regions , , and .

We will show that satisfies all of the conditions in

Definition 1 if and only if we prove that

(82)

(83)

Inequality (82) follows immediately from the

convexity of and the fact that .

Inequality (83) is equivalent to

(85)

where

Since , (85) is plainly true

for all .

On the other hand, we can use (I)

to calculate

because .

This inequality is indeed true because , and (I)

follows.

{pf*}

Proof of Proposition 4

If we denote by the right-hand side of (56),

then we can check that

(86)

and

If , then these calculations

imply that

Combining these inequalities with the observations that

and the fact that the restriction of in is

strictly concave, we can see that equation (56)

has a unique solution , which satisfies

(57).

In particular, we can see that

imply that equation (56) has a unique solution

satisfying (58).

In particular, we can see that

We will show that the function satisfies all of the

requirements of Definition 1 if and only if we prove

that

(88)

If the parameters are such that (58) is

true, then this inequality follows immediately from the

boundary conditions ,

and the fact that is convex, which is true because

.

If the parameters are such that (57) is

true, then .

In this case, for all , which

implies that is strictly decreasing in .

Combining this observation with the fact that is

an even function, we can see that (88) is true

if and only if ,

which is equivalent to .

In view of (I) and the fact that

, we can see that this indeed the case if

and only if (59) is true.

Proof of Proposition 6

In view of (65), we will prove that satisfies

the conditions of Definition 1 if we show that

(89)

(90)

and

Inequality (90) follows immediately by the facts

that is at and the restriction of in

is strictly convex.

Inequality (II) is equivalent to for all , which is true

because .

Finally, inequality (89) is true if and only if

because the restriction of in

has a global minimum at .

Combining this observation with the identity and (66), we can see

that (89) is satisfied if and only if (67)

true.

{pf*}

Proof of Proposition 7

It is a matter of straightforward algebra to verify that if and only if the first inequality in

(72) is true, which we assume in what follows.

Similarly, it is a matter of algebraic manipulations to show

that the constant on the left-hand side of (72) is

strictly less than the constant on the right-hand side of

(72).

Combining the inequality

with the strict concavity of the function , we can see that there exists

such that the function defined by (69) is continuous

and for all if and only if , which is equivalent to the second

inequality in (72).

We now assume that the problem data is such that

(72) is true.

In view of the arguments above and (6), we

will prove that satisfies the requirements of Definition 1

if we show that

(92)

(93)

and

The inequalities (92) and (93) follow

immediately by the facts that is at ,

the restriction of

in is strictly convex and .

Finally, the inequality (II) is equivalent to for all , which is

plainly true because .

{pf*}

Proof of Proposition 8

The inequality for all

that characterizes the region is true if and only if , which is equivalent to (75).

Otherwise, the proof of this result is very similar to the

proof of Proposition 7.

References

(1){bincollection}[mr]

\bauthor\bsnmBather, \bfnmJohn\binitsJ. and \bauthor\bsnmChernoff, \bfnmHerman\binitsH.

(\byear1967).

\btitleSequential decisions in the control of a spaceship.

In \bbooktitleProc. Fifth Berkeley Sympos. Mathematical

Statistics and Probability (Berkeley, Calif., 1965/66), Vol.

III: Physical Sciences

\bpages181–207.

\bpublisherUniv. California Press,

\blocationBerkeley, CA.

\bidmr=0224218

\bptokimsref\endbibitem

(2){barticle}[auto:STB—2014/02/12—14:17:21]

\bauthor\bsnmBayraktar, \bfnmE.\binitsE. and \bauthor\bsnmHuang, \bfnmY.-J.\binitsY.-J.

(\byear2012).

\btitleOn the multi-dimensional controller and stopper games.

\bjournalSIAM J. Control Optim.

\bvolume51

\bpages1263–1297.

\bidmr=3036989

\bptokimsref\endbibitem

(3){barticle}[mr]

\bauthor\bsnmBayraktar, \bfnmErhan\binitsE. and \bauthor\bsnmYoung, \bfnmVirginia R.\binitsV. R.

(\byear2011).

\btitleProving regularity of the minimal probability of ruin via a

game of stopping and control.

\bjournalFinance Stoch.

\bvolume15

\bpages785–818.

\biddoi=10.1007/s00780-011-0160-1, issn=0949-2984, mr=2863643

\bptokimsref\endbibitem

(4){barticle}[mr]

\bauthor\bsnmChiarolla, \bfnmMaria B.\binitsM. B. and \bauthor\bsnmHaussmann, \bfnmUlrich G.\binitsU. G.

(\byear1998).

\btitleOptimal control of inflation: A central bank problem.

\bjournalSIAM J. Control Optim.

\bvolume36

\bpages1099–1132 (electronic).

\biddoi=10.1137/S036301299630495X, issn=0363-0129, mr=1613921

\bptokimsref\endbibitem

(5){barticle}[mr]

\bauthor\bsnmDavis, \bfnmM. H. A.\binitsM. H. A. and \bauthor\bsnmZervos, \bfnmM.\binitsM.

(\byear1994).

\btitleA problem of singular stochastic control with discretionary stopping.

\bjournalAnn. Appl. Probab.

\bvolume4

\bpages226–240.

\bidissn=1050-5164, mr=1258182

\bptokimsref\endbibitem

(6){barticle}[mr]

\bauthor\bsnmEkeland, \bfnmIvar\binitsI.,

\bauthor\bsnmMbodji, \bfnmOumar\binitsO. and \bauthor\bsnmPirvu, \bfnmTraian A.\binitsT. A.

(\byear2012).

\btitleTime-consistent portfolio management.

\bjournalSIAM J. Financial Math.

\bvolume3

\bpages1–32.

\biddoi=10.1137/100810034, issn=1945-497X, mr=2968026

\bptokimsref\endbibitem

(7){barticle}[auto:STB—2014/02/12—14:17:21]

\bauthor\bsnmEl Karoui, \bfnmN.\binitsN. and \bauthor\bsnmChaleyat-Maurel, \bfnmM.\binitsM.

(\byear1978).

\btitleUn problème de réflexion et ses applications au temps

local at aux equations différentielles stochastiques sur , cas continu.

\bjournalAstérisque

\bvolume52-53

\bpages117–144.

\bptokimsref\endbibitem

(8){barticle}[mr]

\bauthor\bsnmHamadène, \bfnmS.\binitsS.

(\byear2006).

\btitleMixed zero-sum stochastic differential game and American

game options.

\bjournalSIAM J. Control Optim.

\bvolume45

\bpages496–518.

\biddoi=10.1137/S036301290444280X, issn=0363-0129, mr=2246087

\bptokimsref\endbibitem

(9){barticle}[mr]

\bauthor\bsnmHamadène, \bfnmS.\binitsS. and \bauthor\bsnmLepeltier, \bfnmJ.-P.\binitsJ.-P.

(\byear2000).

\btitleReflected BSDEs and mixed game problem.

\bjournalStochastic Process. Appl.

\bvolume85

\bpages177–188.

\biddoi=10.1016/S0304-4149(99)00072-1, issn=0304-4149, mr=1731020

\bptokimsref\endbibitem

(10){barticle}[mr]

\bauthor\bsnmJack, \bfnmAndrew\binitsA.,

\bauthor\bsnmJohnson, \bfnmTimothy C.\binitsT. C. and \bauthor\bsnmZervos, \bfnmMihail\binitsM.

(\byear2008).

\btitleA singular control model with application to the goodwill problem.

\bjournalStochastic Process. Appl.

\bvolume118

\bpages2098–2124.

\biddoi=10.1016/j.spa.2008.01.001, issn=0304-4149, mr=2462291

\bptokimsref\endbibitem

(11){barticle}[mr]

\bauthor\bsnmKaratzas, \bfnmIoannis\binitsI.

(\byear1983).

\btitleA class of singular stochastic control problems.

\bjournalAdv. in Appl. Probab.

\bvolume15

\bpages225–254.

\biddoi=10.2307/1426435, issn=0001-8678, mr=0698818

\bptokimsref\endbibitem

(12){barticle}[mr]

\bauthor\bsnmKaratzas, \bfnmIoannis\binitsI. and \bauthor\bsnmSudderth, \bfnmWilliam D.\binitsW. D.

(\byear2001).

\btitleThe controller-and-stopper game for a linear diffusion.

\bjournalAnn. Probab.

\bvolume29

\bpages1111–1127.

\biddoi=10.1214/aop/1015345598, issn=0091-1798, mr=1872738

\bptokimsref\endbibitem

(13){barticle}[mr]

\bauthor\bsnmKaratzas, \bfnmI.\binitsI. and \bauthor\bsnmWang, \bfnmH.\binitsH.

(\byear2000).

\btitleA barrier option of American type.

\bjournalAppl. Math. Optim.

\bvolume42

\bpages259–279.

\biddoi=10.1007/s002450010013, issn=0095-4616, mr=1795611

\bptokimsref\endbibitem

(14){barticle}[mr]

\bauthor\bsnmKaratzas, \bfnmIoannis\binitsI. and \bauthor\bsnmZamfirescu, \bfnmIngrid-Mona\binitsI.-M.

(\byear2008).

\btitleMartingale approach to stochastic differential games of

control and stopping.

\bjournalAnn. Probab.

\bvolume36

\bpages1495–1527.

\biddoi=10.1214/07-AOP367, issn=0091-1798, mr=2435857

\bptokimsref\endbibitem

(15){barticle}[mr]

\bauthor\bsnmLamberton, \bfnmDamien\binitsD. and \bauthor\bsnmZervos, \bfnmMihail\binitsM.

(\byear2013).

\btitleOn the optimal stopping of a one-dimensional diffusion.

\bjournalElectron. J. Probab.

\bvolume18

\bpages49.

\biddoi=10.1214/EJP.v18-2182, issn=1083-6489, mr=3035762

\bptokimsref\endbibitem

(16){bincollection}[mr]

\bauthor\bsnmMaitra, \bfnmAshok P.\binitsA. P. and \bauthor\bsnmSudderth, \bfnmWilliam D.\binitsW. D.

(\byear1996).

\btitleThe gambler and the stopper.

In \bbooktitleStatistics, Probability and Game Theory

(\beditorT. S. Ferguson, L. S. Shapley and J. B. MacQueen, eds.).

\bseriesInstitute of Mathematical Statistics Lecture

Notes—Monograph Series

\bvolume30

\bpages191–208.

\bpublisherIMS,

\blocationHayward, CA.

\biddoi=10.1214/lnms/1215453573, mr=1481781

\bptokimsref\endbibitem

(17){barticle}[auto:STB—2014/02/12—14:17:21]

\bauthor\bsnmMiller, \bfnmM.\binitsM. and \bauthor\bsnmZhang, \bfnmL.\binitsL.

(\byear1996).

\btitleOptimal target zones: How an exchange rate mechanism can

improve upon discretion.

\bjournalJ. Econom. Dynam. Control

\bvolume20

\bpages1641–1660.

\bptokimsref\endbibitem

(18){bbook}[mr]

\bauthor\bsnmPeskir, \bfnmGoran\binitsG. and \bauthor\bsnmShiryaev, \bfnmAlbert\binitsA.

(\byear2006).

\btitleOptimal Stopping and Free-Boundary Problems.

\bpublisherBirkhäuser,

\blocationBasel.

\bidmr=2256030

\bptokimsref\endbibitem