title\setkomafontsection\setkomafontsubsection\setkomafontsubsubsection

Pricing and Valuation under the

Real-World Measure

Abstract

In general it is not clear which kind of information is supposed to be used for calculating the fair value of a contingent claim. Even if the information is specified, it is not guaranteed that the fair value is uniquely determined by the given information. A further problem is that asset prices are typically expressed in terms of a risk-neutral measure. This makes it difficult to transfer the fundamental results of financial mathematics to econometrics. I show that the aforementioned problems evaporate if the financial market is complete and sensitive. In this case, after an appropriate choice of the numéraire, the discounted price processes turn out to be uniformly integrable martingales under the real-world measure. This leads to a Law of One Price and a simple real-world valuation formula in a model-independent framework where the number of assets as well as the lifetime of the market can be finite or infinite.

Keywords: Arbitrage, complete market, complex market, efficient market, enlargement of filtrations, Fundamental Theorem of Asset Pricing, growth-optimal portfolio, immersion, numéraire portfolio, pricing, sensitive market, valuation.

JEL Subject Classification: G12, G14.

1 Motivation

The central motivation of this work is to clarify the economic conditions under which the discounted price processes in a financial market are martingales under the physical measure and not only under an equivalent martingale measure . This martingale property is strongly connected to Samuelson’s Martingale Hypothesis, which is also formulated in terms of instead of (Samuelson, 1965). A substantial difference between Samuelson’s approach and the methodological framework chosen in this work is that the desired martingale property is derived without any requirement on the interest and risk attitude of the market participants. The underlying probabilistic assumptions are minimal. In this model-independent framework, I try to build a bridge between the fundamental results of financial mathematics in terms of “” and the broad field of econometrics, which requires the “.”

Let F be any flow of information that encompasses the evolution E of asset prices in a complete financial market. The main result of this work can be stated as follows:

If the market is sensitive to F, there exists a normalized E-predictable trading strategy that can be chosen as a numéraire such that each discounted price process is a uniformly integrable -martingale with respect to F.

Conversely, choose any normalized E-predictable trading strategy as a numéraire. If each discounted price process is a uniformly integrable -martingale with respect to F, the market is sensitive to F.

In either case, the chosen numéraire is the unique growth-optimal portfolio with respect to F, and is the unique equivalent measure under which the discounted price process is a uniformly integrable martingale with respect to F.

In the following, every financial market is said to be simple if and only if it contains a finite number of assets. By contrast, it is said to be complex if and only if the number of assets is infinite. The main result solves a fundamental problem which frequently occurs in the context of pricing and valuation both in simple and complex financial markets. This problem is threefold:

-

(i)

The set of equivalent martingale measures depends on the given information flow. Hence, there are many possibilities to represent the asset prices and to calculate the fair value of a contingent claim. This leads to the following question:

Does it pay to strive for more information or is it better to renounce searching altogether and to use the information we already have?

-

(ii)

Even if we specify the flow of information, the set of equivalent martingale measures typically contains a multitude of elements. In this case, it is still not clear which one to choose and then the fair value of a contingent claim is not uniquely determined by the given information. Hence, we might ask:

Which economic condition guarantees that the set of equivalent martingale measures is a singleton given the specified flow of information?

-

(iii)

Given a unique equivalent martingale measure for the specified flow of information, it is not always clear how to use this measure in empirical applications, especially if the market is complex. Therefore, the last question is:

Under which circumstances is it possible to represent asset prices and calculate the fair value of any contingent claim in terms of instead of ?

These issues are highly relevant both from a theoretical and a practical perspective. Albeit the given exposition is rigorous in a mathematical sense, most of the presented results have a clear economic content. In particular, the results developed in this work fit harmonically into different coexistent branches of financial mathematics and finance theory. I hope that their practical implications are substantial. The industry still keeps inventing complicated financial instruments, which is a permanent challenge for the quant. This work shall provide a universal approach for assessing the fair value of a contingent claim, which might be considered helpful for the practitioner.

The main result of this work requires a complete financial market. Unfortunately, the classic notion of market completeness has got a bad reputation. In simple financial markets, i.e., if the number of assets is finite, the assumption of market completeness is very restrictive. In the continuous-time framework, only a small number of models are known to be complete, e.g., Bachelier’s Brownian-motion model, the Black-Scholes model, the compensated Poisson process, and Azéma martingales (Cox and Ross, 1976, Harrison and Pliska, 1981, Jarrow and Protter, 2008). For this reason, many alternative approaches have been proposed during the last decades. In particular, the concept of market completeness has been adopted to complex financial markets, i.e., to markets with an infinite number of assets (see, e.g., Artzner and Heath, 1995, Bättig and Jarrow, 1999, Delbaen, 1992, Jarrow and Madan, 1999, Jarrow et al., 1999).111For a nice overview of those contributions see Biagini (2010). On the one hand, this essentially relaxes the notion of market completeness, but on the other hand market complexity sets higher standards for the underlying economy. In view of the vast amount of financial instruments and the increasing globalization of financial markets, complexity can be regarded as an acceptable assumption, at least for every well-developed economy.

Similarly, one can find a plethora of definitions of market efficiency (see, e.g., Fama, 1965, 1970, Fama et al., 1969, Latham, 1986, Malkiel, 1992, Samuelson, 1965). The classic approach to the Efficient-Market Hypothesis is based on the fair-game model (Fama, 1970). Unfortunately, this model suffers from a serious drawback, i.e., the joint-hypothesis problem (Campbell et al., 1997, Fama, 1991). For this reason, I rely on another concept which I call “market sensitivity.” A financial market is said to be sensitive to F if and only if E is -immersed in F. This is a rigorous definition of informational efficiency in terms of martingale theory. Put another way, in a sensitive market, the evolution of asset prices “fully reflects” or “rapidly adjusts to” the information flow F. In Section 4.2 I show that the concept of market sensitivity is intimately connected to different notions of the Efficient-Market Hypothesis. Nevertheless, sensitivity does not require that the market is a fair game and thus, in contrast to the classic approach to market efficiency, it does not suffer from the joint-hypothesis problem (see Section A.1).

A financial market is said to be arbitrage free if and only if there is no free lunch with vanishing risk (NFLVR) and no dominance (ND) with respect to the information flow F. Due to the 1st Fundamental Theorem of Asset Pricing (FTAP), the NFLVR condition alone only guarantees that there exists an equivalent probability measure such that each discounted price process is a local -martingale with respect to F (Delbaen and Schachermayer, 1994). Jarrow and Larsson (2012) prove that, in every simple market with finite lifetime, the additional ND condition turns the discounted price processes into -martingales with respect to F. Conversely, if a simple market with finite lifetime contains an equivalent martingale measure with respect to F, it must be arbitrage free. This result is referred to as the 3rd FTAP (Jarrow, 2012). In this work, I extend the 3rd FTAP to financial markets with infinite lifetime.

Modern approaches to the Efficient-Market Hypothesis focus on the absence of arbitrage (Jarrow and Larsson, 2012, Ross, 2005). In fact, Jarrow and Larsson (2012) show that NFLVR and ND together are necessary and sufficient for the existence of a pure exchange economy, with finite lifetime and a finite number of assets, where all subjects use the information flow F for their investment-consumption plans and the discounted price processes form an Arrow-Radner market equilibrium. This demonstrates that every simple market, with finite lifetime and symmetric information, that is considered “efficient” must be at least arbitrage free or, equivalently, the discounted price processes must be martingales with respect to F under any equivalent probability measure . Both the absence of arbitrage opportunities and the ability of asset prices to “fully reflect” or “rapidly adjust to” the information flow F are fundamental assumptions of neoclassical finance (Ross, 2005). These axioms turn out to be essential also for the theory presented in this work and so I use the following definition of market efficiency: A financial market is said to be efficient if and only if it is sensitive to F and contains a risk-neutral measure, i.e., an equivalent martingale measure with respect to F.222As a consequence of the extended version of the 3rd FTAP, which I present in this work, the discounted price processes are even assumed to be uniformly integrable martingales under .

The mathematical tools I use belong to martingale theory (Jacod and Shiryaev, 2003) and the key results stem from a discipline called “enlargement of filtrations,” developed by Yor and Jeulin (1978, 1985).333For a nice overview see Jeanblanc (2010, Ch. 2), which contains a comprehensive list of references on that topic. This is a popular instrument in modern finance and has often been applied in the recent literature, especially in the area of credit risk and insider trading (Amendinger, 1999, Bielecki and Rutkowski, 2002, Elliott et al., 2000, Kohatsu-Higa, 2007). The enlargement of filtration is typically done under some probability measure that is equivalent to . To the best of my knowledge, the question of market sensitivity, where we are mainly concerned with an enlargement under the physical measure, has not yet been investigated in the literature.

Since the 1st, 2nd, and 3rd FTAP (Delbaen and Schachermayer, 1994, 1998, Harrison and Pliska, 1981, 1983, Jarrow, 2012, Jarrow and Larsson, 2012) are essential in this methodological framework, they are briefly discussed in Section 3 and Section 4.1. Another essential branch of literature is related to the benchmark approach propagated by Platen and Heath (2006). This is based on the growth-optimal portfolio (GOP), which has been a subject of heated discussions (Christensen, 2005, MacLean et al., 2011). In fact, the benchmark approach goes back to Long (1990), who has introduced the notion of numéraire portfolio (NP). In Section 5, I give a short overview of the benchmark approach and explain the connection between the GOP and the NP.

The GOP plays a fundamental role in modern finance (Karatzas and Kardaras, 2007, MacLean et al., 2011, Platen and Heath, 2006). If the market contains no unbounded profit with bounded risk (NUPBR), the GOP can be used as an NP. Unfortunately, this leads only to a Law of Minimal Price. The question of how to obtain a Law of One Price, in the strict sense mentioned at the beginning of this introduction, has not yet been investigated in the literature. Section 6 contains the main result of this work. This can be put in a nutshell as follows:

Every complete and sensitive market contains a specific numéraire such that .

2 Preliminary Definitions and Assumptions

Let be a filtered probability space where the filtration is right-continuous and complete. It is implicitly assumed that forms the -algebra of the given probability space. Consider an asset universe with a finite or infinite number of primary assets. Let be the set of asset prices in at time . More precisely, it is supposed that is an F-adapted price process. Two assets are considered identical if and only if their price processes coincide almost surely. For notational convenience, I omit the subscript “” in every expression of the form “” if the index set is clear from the context.

The filtration F can be viewed as a cumulative flow of information evolving through time. Since is F-adapted, contains at least the price history at every time .444The fact that is F-adapted does not imply that each market participant has access to the information flow F. More precisely, denotes the -algebra generated by the price history in at time . It is supposed that is trivial, i.e., it contains only the -null and -one elements of . The evolution of asset prices is represented by , i.e., the natural filtration of the price process . A filtration is said to be a subfiltration if and only if , i.e., for all .

The notation “” means that the random quantity is -measurable, where is any sub--algebra of . Attributes that are ascribed to random quantities or stochastic processes are meant to hold almost surely. For example, the equality “” for any two random vectors and means that each component of equals the corresponding component of almost surely. Any inequality of the form “,” “,” “,” or “” is to be understood in the same sense. If is an -valued stochastic process, means that is almost surely (uniformly) bounded from below by . Moreover, two stochastic processes are considered identical if and only if they coincide (almost surely).

Now, choose an arbitrary asset as a numéraire and let be its price process. Every finite subset of that contains the chosen numéraire asset plus other assets is said to be a subuniverse.555In this work, the symbol “” stands for the set of positive integers, i.e., . This is symbolized by and denotes the corresponding vector of asset prices for all . It is assumed that is a positive F-adapted -valued semimartingale being right-continuous with left limits (càdlàg).666It is not assumed that is bounded or locally bounded. Also its left-continuous version, i.e., (with for ), is assumed to be positive.

The limit of , i.e., , exists and is finite. Moreover, it is assumed that . This general approach enables us to analyze markets with infinite lifetime. Markets with finite lifetime, e.g., the Black-Scholes model, can be considered a special case. This is simply done by assuming that for all , where is any fixed lifetime. Discrete-time financial markets are obtained in the same way, just by assuming that the filtration F is constant over the time intervals for , , and .

For notational convenience, but without loss of generality, it is supposed that for . I usually refer to the -valued process of discounted asset prices, i.e., with for all .777From Itô’s Lemma it follows that is a semimartingale and the product of two semimartingales is also a semimartingale. This means is an -valued semimartingale. Since and are assumed to be positive, we also have that . If I say that any statement is true for all , I mean that it is true for the discounted price process in each subuniverse . Similarly, a statement is true for all if and only if it is true for the nominal price process in every . All previous statements are supposed to be true for all and , respectively.

Every F-predictable -valued stochastic process with that is integrable with respect to the discounted price process is said to be a trading strategy. The discounted value of the strategy at every time is given by

where is the discounted initial value and represents the discounted gain of the strategy up to time .888Two strategies are considered identical if and only if their (discounted) value processes coincide. This means evolves from self-financing transactions between time and . The integral is to be understood in the sense of Jacod and Shiryaev (2003, p. 207), i.e., as a stochastic vector integral.999For this reason, the requirements on that are mentioned by Harrison and Pliska (1981) are too strict (Jarrow and Madan, 1991). See also Remark 1.3 in Biagini (2010).

The strategy is called admissible if and only if there exists a real number such that .101010According to Delbaen and Schachermayer (1994, Definition 2.7), the strategy is called “-admissible” if and only if for a given number but just “admissible” if and only if for some . The discounted initial value of , i.e., , need not be constant. If we add numéraire assets at , we obtain the strategy , which has a nonnegative discounted value process with for all . In the case we can divide by so as to obtain the strategy whose discounted value process starts at 1 and remains nonnegative. By choosing a sufficiently high number , we can even guarantee that both and its left-continuous version are positive. Each admissible strategy that leads to a positive discounted value process starting at 1, such that the left-continuous version of the discounted value process is positive, too, is said to be normalized.111111A normalized strategy is always 1-admissible by construction. Moreover, each normalized strategy is still normalized after any change of numéraire. A normalization just leads to an affine-linear transformation of the discounted value process of , which enables us to switch easily between the different no-arbitrage conditions explained in Section A.2.1. This general framework shall guarantee that the basic assumptions of the fundamental theorems of asset pricing and of the benchmark approach are satisfied (Delbaen and Schachermayer, 1994, 1998, Harrison and Pliska, 1981, 1983, Jarrow, 2012, Karatzas and Kardaras, 2007).

In this work, we are often concerned with an equivalent martingale measure (EMM), an equivalent local martingale measure (ELMM) or an equivalent uniformly integrable martingale measure (EUIMM). A probability measure is said to be an E(L)MM with respect to F if and only if

-

(i)

is equivalent to on and

-

(ii)

every discounted price process is a (local) -martingale with respect to F.

The equivalence between and on is denoted by . Further, () is the set of all probability measures such that the discounted price process in the subuniverse is a (uniformly integrable) -martingale with respect to F. The superscript “” shall indicate the chosen numéraire asset . Analogously, denotes the set of all probability measures that are equivalent to on such that is a local -martingale with respect to F. Moreover, whenever I drop the subscript , I mean that the corresponding martingale property holds for all in the given asset universe.

A statement like “” does not imply that is equivalent to on the -algebra and even if , is not necessarily a -martingale with respect to F. Nevertheless, we always have that and

Every probability measure is associated with a unique Radon-Nikodym (derivative or density) process (RNP) , i.e., a positive uniformly integrable -martingale with respect to F with . Although need not be trivial, we can assume without loss of generality that (see Section A.2.2). Each stochastic process that satisfies the aforementioned properties is said to be a (local) discount-factor process (DFP) if and only if is a (local) -martingale with respect to F for every discounted price process . Whenever the lifetime of the financial market is finite, the uniform-integrability assumption about can be dropped and it is clear that every DFP is a local DFP but not vice versa.151515Each local DFP is a so-called local martingale deflator (see Proposition 4). Every (local) DFP has an associated probability measure which is defined by

I say that is an F-RNP or a (local) F-DFP, respectively, to emphasize the underlying filtration F. Finally, each ratio () is said to be a discount factor and I write for all .

In the following, I refer to several no-arbitrage conditions. Most of them are frequently applied in financial mathematics. Only the ND condition is not widespread in the literature. This no-arbitrage condition has been introduced by Merton (1973) and can be found, e.g., in Jarrow (2012) as well as Jarrow and Larsson (2012). All other no-arbitrage conditions are well-established. See for example Karatzas and Kardaras (2007) for a nice overview or consult Section A.2.1.

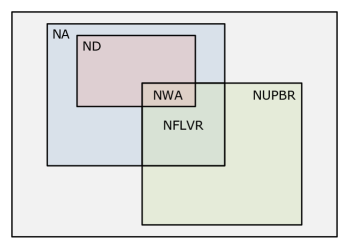

A dominant strategy, a free lunch with vanishing risk, and an unbounded profit with bounded risk can be seen as weak arbitrage opportunities. I say that there is no weak arbitrage (NWA) if and only if there is ND and NFLVR or, equivalently, ND and NUPBR, i.e.,

The relationship between the several no-arbitrage conditions is illustrated in Figure 1.

If the information flow F does not allow for a weak arbitrage in the given subuniverse , I say that is arbitrage free and write . The statements and shall be understood in the same sense. Moreover, the entire market or, equivalently, the asset universe , is said to be arbitrage free if and only if for all . The distinction between and is crucial if the market is complex.

3 The Third Fundamental Theorem of Asset Pricing

The 1st FTAP for unbounded price processes (Delbaen and Schachermayer, 1998) states that if and only if is a --martingale with respect to F, where is equivalent to .161616The stochastic process is said to be a --martingale with respect to F if and only if for all . Here is an -integrable F-predictable stochastic process and is a local -martingale with respect to F (see Proposition 2 (i) in Émery (1980) and Theorem III.6.41 in Jacod and Shiryaev (2003, p. 217)). Every local martingale is a -martingale and every -martingale that is bounded from below is a local martingale (Jacod and Shiryaev, 2003, p. 214, 216). Since the discounted asset prices are positive, is a local martingale if and only if it is a -martingale. For this reason, it is not necessary to distinguish between the terms “local martingale” and “-martingale” in the present context. This means if and only if is a local -martingale with . Every positive local martingale is a supermartingale. Hence, for all and so the 1st FTAP provides only a lower bound for the discounted price process.

Now, suppose that the financial market has a fixed finite lifetime . In this situation, the 3rd FTAP (Jarrow, 2012) strengthens the 1st FTAP. It states that there is NWA with respect to if and only if is a -martingale with respect to for any . Moreover, Jarrow and Larsson (2012, Theorem 3.2) show that the existence of an EMM with respect to is equivalent to the existence of a pure exchange economy, with finite lifetime , where all subjects use the same information flow and is a discounted Arrow-Radner equilibrium-price process with respect to .171717This means (i) the investment-consumption plans of all subjects are optimal with respect to and (ii) all (i.e., the security and the commodity) markets clear with . Hence, the absence of weak arbitrage opportunities seems to be an essential requirement—not only for risk-neutral valuation but also for the existence of any market equilibrium in a finite economy.181818Under short-selling constraints, a market equilibrium at least implies the existence of a local martingale deflator . This guarantees that is a local -martingale with respect to (Jarrow and Larsson, 2013, Theorem 3.1). This result marks a cornerstone in the development of the Efficient-Market Hypothesis.

The following theorem extends the 3rd FTAP to financial markets with infinite lifetime.

Theorem 1 (The 3rd FTAP).

Let be any subuniverse and some numéraire asset. Then if and only if .

Proof: If there cannot exist a free lunch with vanishing risk with respect to F in the subuniverse and thus we can apply Theorem 2.12 in Delbaen and Schachermayer (1997) as well as Theorem 5.7 in Delbaen and Schachermayer (1998).191919The admissibility condition given by Delbaen and Schachermayer (1998) is always satisfied in this context and recall that we do not have to distinguish between -martingales and local martingales. Since every asset in is F-maximal, it follows from Theorem 2.12 in Delbaen and Schachermayer (1997) that the sum of all assets in is F-maximal, too.202020Jarrow and Larsson (2012) remark that the requirement that is locally bounded, which is given by Delbaen and Schachermayer (1997), in fact is superfluous. Theorem 5.7 in Delbaen and Schachermayer (1998) implies that there exists an ELMM with respect to F such that the sum of all discounted asset prices in is a uniformly integrable -martingale with respect to F. Hence, the discounted price process in is a positive local -martingale bounded above by a uniformly integrable -martingale and so it is also a uniformly integrable -martingale with , i.e., . Conversely, if there exists a measure such that the discounted price process of is a uniformly integrable -martingale with respect to F, Theorem 5.7 in Delbaen and Schachermayer (1998) implies that each asset in is F-maximal, whereas the 1st FTAP guarantees that there is NFLVR with respect to F in . Hence, we have that . Q.E.D.

The uniform integrability of is an essential requirement. It leads to a financial market that is consistent in the following sense.

Theorem 2 (Change of numéraire).

Let be some numéraire asset. If then for every other numéraire asset .

Proof: Let be the price process of the numéraire asset and the price process of any numéraire asset . Further, consider an EUIMM . Then is a positive uniformly integrable -martingale with respect to F with and . Hence, we obtain the EMM with for all . Since

for all and , each -martingale is closed by . This means , i.e., . Q.E.D.

The previous theorems justify the following definition.

Definition 1 (Risk-neutral measure).

Let be some numéraire asset. A probability measure is said to be a risk-neutral measure if and only if .

The existence of a risk-neutral measure implies that the market is arbitrage free in the sense of Theorem 1, i.e., that there is NWA with respect to F. Nonetheless, Herdegen (2014) points out that most no-arbitrage conditions essentially depend on the choice of the numéraire asset. For this reason, he refrains from using a numéraire asset and suggests a numéraire-independent modeling framework for financial markets. Theorem 2 at least guarantees that the existence of a risk-neutral measure is invariant under a change of numéraire. By contrast, only guarantees that there is NFLVR with respect to F, but a change of numéraire can destroy the local martingale property (Delbaen and Schachermayer, 1995).

The following theorem provides an equivalent representation of the discounted price process in terms of the real-world measure instead of the risk-neutral measure .

Theorem 3 (Representation Theorem).

Let be any subuniverse and some numéraire asset. Then if and only if there exists an F-DFP such that is a uniformly integrable -martingale with respect to F.

Proof: I start with the “only if” part. According to Theorem 1, implies that . Consider some risk-neutral measure and let be the associated F-RNP. From Lemma 2 we know that is a -martingale with respect to F. Moreover, from Lemma 1 we conclude that

and thus for all . Hence, the -martingale is closed by and thus uniformly integrable. Lemma 3 guarantees that is an F-DFP. For the “if” part consider the F-DFP and let be the associated EMM. Since is uniformly integrable, we have that and with Lemma 1 we obtain

for all . This means the -martingale is closed by and thus it is uniformly integrable. We conclude that and from Theorem 1 it follows that . Q.E.D.

So far, we have established the basic conditions for risk-neutral valuation, but some important issues are still missing on the agenda (see also p. 1):

-

(i)

In real life, we do not know the set of risk-neutral measures, i.e., . In fact, this set might be considerably smaller than .

-

(ii)

In general, contains a multitude of risk-neutral measures and so the fair value of a contingent claim might not be unique, even if was known.

-

(iii)

Moreover, even if is a singleton, it is practically impossible to derive the risk-neutral measure without making additional assumptions on the (discounted) price processes.

Theorem 3 is merely a re-formulation of Theorem 1. For this reason, the aforementioned obstacles cannot be cleared by the Representation Theorem: In general, (i) the DFP is not E-adapted, (ii) is not unique, and (iii) it is not a priori clear how to calculate . In the following, I present the economic conditions under which turns out to be a unique and well-defined E-adapted stochastic process so that the aforementioned problems evaporate.

4 Market Completeness and Sensitivity

4.1 Completeness

Consider a simple financial market with finite lifetime and choose any asset as a numéraire. Harrison and Pliska (1981) call every positive random variable a contingent claim. They suppose that and fix any . Now, according to Harrison and Pliska (1981), the financial market is complete if and only if for every contingent claim with , there exists an E-predictable strategy whose discounted value process is a -martingale with respect to E such that . This implies that is positive. Moreover, by the Predictable Stopping Theorem (Jacod and Shiryaev, 2003, Lemma I.2.27), also the left-continuous version of is positive. Since the -algebra is assumed to be trivial, is constant and so the chosen strategy is admissible.

The economic idea behind the definition of market completeness can be explained like this: The goal is to replicate a contingent claim by an admissible E-predictable strategy as favorable as possible. Theorem 2.9 in Delbaen and Schachermayer (1994) implies that must be a -supermartingale with respect to E. This means we have that for all . Hence, in a complete financial market, we achieve the best possible replicating strategy if and only if the resulting discounted value process is a -martingale with respect to E. We conclude that the fair value of (expressed in units of the basic currency) amounts to at every time . It is worth emphasizing that calculating the fair value of a contingent claim makes no sense if the market already contains an asset with discounted price process such that . In this case, we can already observe the (nominal) price of the contingent claim at every time and, since we have that , this can be considered a fair value of .

The 2nd FTAP (Harrison and Pliska, 1983) states that a market is complete if and only if is the unique EMM with respect to E. Moreover, it is complete if and only if satisfies the predictable-representation property. This means every -martingale with respect to E can be represented by for all , where is an E-predictable (not necessarily admissible) trading strategy. Unfortunately, in the continuous-time framework, only a small number of market models satisfy the desired predictable-representation property.

It is not meaningful to expand the concept of market completeness from E to F simply by substituting E with F. In this case, we could only guarantee that every contingent claim is replicable by an F-predictable trading strategy, but this is not necessarily E-predictable. This means a market that is complete with respect to F might be incomplete with respect to E. Put another way, if we substitute E with F, market completeness would lack the so-called subset property (Latham, 1986).212121Here, I use the term “subset property” in a broad sense, albeit Latham (1986) focuses on market efficiency. The subset property is a natural requirement and turns out to be crucial when switching between the filtrations E and F, which is frequently done in this work. Moreover, by substituting E with F we would allow to be an -measurable payoff, but in most practical situations it is sufficient and, for technical reasons, even necessary to assume that is determined only by the price history at time , i.e., .222222For example, the Black-Scholes model requires that F coincides with the natural filtration E (Harrison and Pliska, 1981, Jarrow and Madan, 1991). Interestingly, Harrison and Pliska (1981, p. 220) mention that they consider only the natural filtration E, whereas in Harrison and Pliska (1983) this essential point has been dropped.

If there exists a risk-neutral measure with respect to F it is not sufficient to require that the discounted value process of the E-predictable strategy is a -martingale with respect to E. More precisely, when replicating it should be possible to produce a -martingale with respect to F. In this case, the replicating strategy is also fair with respect to F although it is only E-predictable. This can be seen as follows: Suppose that we would allow to be an admissible F-predictable and not only E-predictable strategy. From Theorem 2.9 in Delbaen and Schachermayer (1994) we conclude that the discounted value process of is a -supermartingale with respect to F, i.e., for all , where is the discounted value of the most favorable E-predictable replicating strategy at time . This means we cannot find a better result by allowing the replicating strategy to be F-predictable.

The following definition of market completeness is based on the aforementioned arguments and is less restrictive than the original one. It allows for complex financial markets with infinite lifetime and an arbitrary filtration . In particular, it satisfies the desired subset property. Thus it can be considered a natural generalization of the definition of market completeness given by Harrison and Pliska (1981, 1983).

Definition 2 (Complete market).

Let be some numéraire asset and suppose that . Fix any risk-neutral measure . The financial market is said to be complete if and only if for every contingent claim with , there exists an E-predictable strategy such that for all , where is the discounted value process of .

The requirement of a risk-neutral measure is motivated by Theorem 1. Definition 2 allows to be based on any subuniverse of the financial market and it is assumed that the contingent claim is -measurable. Moreover, the strategy must be E-predictable and thus its discounted initial value is constant. The discounted value process is a uniformly integrable -martingale with respect to F (and not only with respect to E). This implies that and , i.e., is admissible. Moreover, it follows that and so the given strategy indeed replicates the contingent claim .

The chosen definition of market completeness is relatively weak. Since it is only required that the contingent claim is -measurable, we need not assume that it is possible to assess the fair value of any exotic derivative based on events that go beyond the history of asset prices. Typical examples are weather derivatives or non-financial bets. Nonetheless, market completeness does not exclude the possibility to replicate (some) exotic instruments. Moreover, for a complex and complete market it is neither necessary nor sufficient that any finite subset of the asset universe forms a complete market. This means in a complete financial market, with an infinite number of assets, the predictable-representation property need not be satisfied in any subuniverse . In particular, every subuniverse might contain a multitude of equivalent martingale measures. The most striking example of a complex market, which is complete but model independent, is a “dense” market, i.e., a financial market where each contingent claim can be attained by a single asset. Note that the properties required by Definition 2 are implicitly satisfied for every E-predictable buy-and-hold single-asset strategy.

An important consequence of Definition 2 is that, for calculating the fair value of a contingent claim , we need only the information flow E but not the broader information flow F. On the one hand, the replicating strategy is only E-predictable and, on the other hand, it holds that for all . Hence, if the market is complete with respect to F, each information that goes beyond the evolution of asset prices, E, but does not exceed the general information flow F can be neglected. This solves the first part of the fundamental problem mentioned at the beginning of the introduction. The second part of the problem is solved by the following theorem.

Theorem 4 (Uniqueness).

Let be some numéraire asset. If the financial market is complete, is a singleton.

Proof: Since and , it follows that . Let be the E-RNP associated with any . The market is complete and so the contingent claim can be attained by an E-predictable trading strategy with discounted value process . We have that and thus

for all . Now, suppose that there exist two probability measures and let and be the associated E-RNPs. Then and are the discounted value processes for the contingent claims and . Define for all . We see that both and are -martingales with and thus for all . This means we have that

Since the function for all is strictly convex, Jensen’s inequality implies that and thus for all . This means must be a singleton and so is a singleton, too. Q.E.D.

Theorem 4 states that each complete financial market cannot have more than one risk-neutral measure. This result holds irrespective of whether the market contains a finite or infinite number of assets. Similar statements can be found, e.g., in Jarrow and Madan (1999), Jarrow et al. (1999) as well as Biagini (2010). Hence, in every complete financial market we are always able to find a unique representation of asset prices and fair values.

The following theorem guarantees that market completeness does not depend on the chosen numéraire asset.

Theorem 5 (Change of numéraire).

Let be some numéraire asset. If the market is complete with respect to it is also complete with respect to every other numéraire asset .

Proof: Let be the risk-neutral measure and choose any other numéraire asset . According to the proof of Theorem 2, we have that with for all . Consider any contingent claim with . It holds that

This means the contingent claim can be attained by an E-predicable strategy with value process —discounted by —such that for all . Now, given the numéraire asset , the same strategy leads to the discounted value process with

for all . We conclude that the market is complete with respect to . Q.E.D.

The third part of the fundamental problem discussed on p. 1 and p. 3 is still unsolved. This means I need to clarify the circumstances under which it is possible to represent asset prices and fair values in terms of . Put another way, we are waiting to see the (additional) condition that enables us to use the real-world measure as a risk-neutral measure.

4.2 Sensitivity

In the following, the time shall be understood as the “present,” every before is the “past,” whereas symbolizes the “future,” i.e., we have that unless otherwise stated. Let be some -measurable random vector. For example, could be a vector of asset prices, or any other function of asset prices, that will be manifested in the future. The complement of relative to , i.e., , represents the information in that goes beyond the price history . For example, if is the set of public information then denotes the subset of public information that does not belong to the price history at time .

A natural requirement arising in financial econometrics is

| (1) |

for all , , , and -measurable -dimensional random vectors . Eq. 1 implies that the random vector is -independent of conditional on the price history . This means the conditional distribution of future asset prices might depend on the current history of asset prices but not on any additional information contained in . Under these circumstances, it is impossible to produce a better prediction of future asset prices (or functions thereof) by using some information in , provided the price history has already been taken into account. More precisely, we have that

for all and with . Nevertheless, although it is superfluous to use any kind of information that exceeds but is contained in , there might exist some information beyond that could be useful.

Another desirable property is

| (2) |

for all , , , and -measurable -dimensional random vectors . For example, let be a variable that indicates whether a stock company has committed a balance-sheet fraud up to time () or not (). Since the choice of is arbitrary, we can suppose without loss of generality that for all . Consider an investor who takes only the current price history into account and is not aware of the fraud. It is assumed that the fraud will eventually have an impact on the stock price. Hence, it would be ideal for the investor to know the future price evolution today, since on the basis of the future price movements, he or she would get a better assessment of the fraud probability. Unfortunately, in real life, is unknown at time . Nonetheless, Eq. 2 states that the investor can readily substitute by . This means all information that would be useful for calculating the fraud probability, conditional on past and forthcoming price data, is already incorporated in the asset prices that can be observed now. This paraphrases the widely accepted idea that asset prices “rapidly adjust to” new information (Fama et al., 1969).

The following definition (Jeanblanc, 2010, p. 16) is crucial for the subsequent analysis.

Definition 3 (Immersion).

Let be any probability measure. The filtration E is said to be -immersed in F if and only if every square-integrable -martingale with respect to E is a square-integrable -martingale with respect to F.

The statement that “E is immersed in F” (with respect to a probability measure ) is often referred to as the H-Hypothesis (Brémaud and Yor, 1978).

The following theorem provides different characterizations of the H-Hypothesis under the physical measure .

Theorem 6 (H-Hypothesis).

The following assertions are equivalent:

-

(i)

E is -immersed in F.

-

(ii)

It holds that for all , , , and -dimensional random vectors .

-

(iii)

It holds that for all , , , and -dimensional random vectors .

-

(iv)

Every local -martingale with respect to E is a local -martingale with respect to F.

Moreover, if any one of the previous assertions is true it follows that

Proof: Statements (i) to (iv) follow from Proposition 2.1.1 in Jeanblanc (2010). The last implication is part of Theorem 3 in Brémaud and Yor (1978). Q.E.D.

Theorem 6 shows that the fundamental properties expressed by Eq. 1 and Eq. 2 are equivalent. This leads to the following definition.

Definition 4 (Sensitive market).

A financial market is said to be sensitive if and only if any one of the equivalent assertions expressed by Theorem 6 is true. This is denoted by .

A financial market that is sensitive to F is also sensitive to every subfiltration I . This means market sensitivity satisfies the subset property and does not exclude for any other filtration . Moreover, it is trivial that .

The following proposition provides a sufficient condition for market sensitivity.

Proposition 1.

Consider any probability measure and let be the F-RNP associated with . If E is -immersed in F and is E-adapted we have that .

Proof: This is a direct consequence of Proposition 2.1.4 in Jeanblanc (2010). Q.E.D.

There are many possibilities to define the meaning of informational efficiency in the sense that asset prices “fully reflect” some information flow F. For example, Dothan (2008) states that,

“The intuitive notion that prices fully reflect the information structure is then the requirement that the discounted price process be Markov.”

Unfortunately, the Markov assumption, i.e.,

essentially restricts the number of possible market models and it is well-known that this property is not satisfied in reality.232323It is often supposed that (), which implies both market sensitivity and the Markov property.

The concept of market sensitivity is less restrictive, but it is still intimately connected to different notions of the Efficient-Market Hypothesis:

-

•

The relationship expressed by (1) can be interpreted as a probabilistic definition of Fama’s (1970) famous hypothesis that asset prices “fully reflect” at every time . For example, let be the set of all private information at time . If the market is strong-form efficient (Fama, 1970) all private information, except for the price history , can be ignored because it is already “incorporated” in . Hence, if somebody aims at quantifying the conditional distribution of , the weaker condition is as good as the stronger condition , i.e., each private information beyond the price history is simply useless.

-

•

The probability distribution of future asset prices generally depends on the underlying information. In a risky situation (Knight, 1921), the quality of each decision cannot become worse the more information is used.242424This statement is no longer true under uncertainty (Frahm, 2015). This means every market participant should gather as much information as possible.252525This is true if the information costs are negligible (Grossman and Stiglitz, 1980). Otherwise, each rational subject stops searching for information when the marginal cost approaches the marginal revenue (Jensen, 1978). Consequently, the chosen market model must specify which kind of information is accessible by the economic subjects and used for their investment decisions. Suppose that their decisions are based only on the conditional distribution of future asset prices, i.e., other variables that will be manifested in the future do not matter. Eq. 1 says that any information contained in , but being complementary to , would not alter the conditional price distribution and so this information can be simply ignored. More precisely, the economic subjects cannot improve their asset allocations by using some information in provided they have already taken the current price history into account. Hence, in a pure investment economy where Eq. 1 is satisfied, the current asset prices would be unaffected by revealing to all market participants. For example, if is the set of private information, revealing some private information to the investors would not change their investment decisions and so the financial market is strong-form efficient in the sense of Latham (1986) and Malkiel (1992).262626Here, it is implicitly assumed that the subjects have already taken the current price history into account.

-

•

As already mentioned above, according to Fama et al. (1969), a financial market is considered efficient if it “rapidly adjusts to” new information. Eq. 2 is the probabilistic counterpart of this statement and implies that every “new information” is instantaneously incorporated in the asset prices that can be observed at time , i.e., now, and not only at a later time .

-

•

Samuelson (1965) conjectures that the market participants “properly anticipate” the future price evolution. He writes, “If one could be sure that a price will rise, it would have already risen.” Suppose that for some . Due to the last part of Theorem 6 it follows that the market is not sensitive. Hence, we have that and so there exists an event such that . Since the event is also contained in but exceeds , it leads to a situation where one can “foresee” to some degree the price evolution after time . More precisely, the information reveals which sample paths are going to follow and which are not. This can be seen as a contradiction to Samuelson’s doctrine. In the opposite case, i.e., if and thus for all , clairvoyance is impossible unless one has access to some information flow and the market is not sensitive to G.

The reason why the properties described by Theorem 6 characterize a “sensitive” market is best understood by examining a market that is not sensitive. For this purpose, we have to take a closer look into the measure-theoretic framework. Let be the current history of asset prices and with the price history at some future point in time . Suppose for the sake of simplicity that . Consider a trader who operates on the basis of the information flow F and let his or her investment decision at time be determined by the distribution of future asset prices conditional on . Since the market is not sensitive, we can assume that there exists some information with and such that . In this case, the investment decision made by the trader, given the current history of asset prices, could depend on the realization of .272727Here, if and else (). For example, the trader might want to buy some asset in case but decides to sell the same asset if . By definition, the price history at time is -measurable, i.e., the past and current asset prices are constant over the set . Hence, the current asset prices are not sensitive to , i.e., the trader is a price taker—conditional on the current price history . From an economic point of view, this is not desirable and characterizes a market where the asset prices do not “fully reflect” or “rapidly adjust to” the information flow F, although this flow of information could be useful also for other traders. Hence, perfect competition might enable a small investor to realize “abnormal profits” if he or she has access to information that is not already known to other investors. For example, this could be insider information.

We see that sensitivity is a highly desirable economic property. A market that is sensitive can immediately react to the news evolving with F, irrespective of whether those news are considered “good” or “bad.” This means in a sensitive market, the asset prices instantly adapt to the investment decisions that are based on the future price expectations of the market participants with respect to F. More precisely, each information that is considered useful for assessing the physical distribution of future asset prices has an immediate impact on the supply and demand curves, which instantaneously affects the market quotes at time . This does not mean that every subject who operates on the basis of F makes the same investment decision. Market sensitivity does not even imply that the investment decisions are rational in any sense and pricing in a sensitive market need not be fair. For this reason, market sensitivity must not be confused with Fama’s fair-game model (Fama, 1970) or any other approach to market efficiency that requires the absence of “economic profits” (Jensen, 1978). Hence, the concept of market sensitivity does not suffer from the joint-hypothesis problem (see Section A.1).

Let be the number of market participants and suppose that each investor operates on the basis of some information flow (). An ideal market is sensitive to the flow of private information, i.e., with for all . If insider trading is prohibited and all insiders follow this rule, even an ideal market is not sensitive to the flow of insider information. Even if there exist a few insider traders, but the market is competitive, each insider is a price taker and so the market is still not sensitive to the flow of insider information. The bigger a group of investors acting on the same information flow, the greater its potential impact on the market prices. Hence, it can be assumed that financial markets are at least sensitive to the flow of public information, i.e., with for all .

Market sensitivity per se does not guarantee that the market is arbitrage free and in this specific sense “efficient:” If the market is sensitive but not arbitrage free, it is evident that all market participants will search in F for arbitrage opportunities. No-arbitrage conditions only guarantee that the market is free of profits that would be realized by everyone, irrespective of his or her own expectation, interest, and risk attitude. Nonetheless, if the market is arbitrage free but not sensitive, some market participants might still improve their positions by collecting data in addition to the current history of asset prices and re-allocating their capital. In either case, the market participants have an incentive to search for information that cannot be found just by investigating the history of asset prices. Only if the market is arbitrage free and sensitive, it is impossible to “make money out of nothing” on the basis of F and the price evolution “fully reflects” or “rapidly adjusts to” the broader information flow F. The former is a fundamental assumption in financial mathematics, whereas the latter is a basic paradigm in finance theory. This justifies the following definition of market efficiency.

Definition 5 (Efficient market).

Let be some numéraire asset. The financial market is said to be efficient if and only if and .

Theorem 2 guarantees that market efficiency does not depend on the chosen numéraire asset. Moreover, every complete and sensitive market is also efficient.

5 The Growth-Optimal Portfolio

Fix a subuniverse and choose any asset as a numéraire. Further, let and be two normalized F-predictable strategies whose discounted value processes are denoted by and , respectively. Let be the value of benchmarked by at each time . Since for all , it does not matter whether we express the values in units of the chosen numéraire asset or in units of the basic currency. This implies that the benchmarked value process does not depend on the chosen numéraire asset at all.

The normalized strategy is said to be a numéraire portfolio with respect to F if and only if for every normalized F-predictable strategy , the benchmarked value process is a -supermartingale with respect to F, i.e., for all . In particular, the stochastic process is a positive -supermartingale. Doob’s Martingale Convergence Theorem guarantees that exists and is finite, i.e., . Hence, the terminal value is well-defined, but we could have that .282828Since is a nonnegative -supermartingale, it converges almost surely to some nonnegative random variable . This means also the discounted value process has a terminal value, i.e., . In the unfavorable case , the investor applies a so-called “suicide strategy” (Harrison and Pliska, 1981).

The strategy is said to be a growth-optimal portfolio with respect to F if and only if it maximizes the drift rate of with respect to F, i.e., the so-called growth rate of , for all . Since for all , every strategy is growth optimal with regard to the discounted price process if and only if it is growth optimal with regard to the nominal price process . Thus growth optimality cannot be destroyed by moving from discounted to nominal asset prices and vice versa. Put another way, the choice of the numéraire does not matter for a GOP and the same holds for every NP.

A historical summary of the GOP is given by Christensen (2005) and a rich collection of contributions related to the GOP can be found in MacLean et al. (2011). Karatzas and Kardaras (2007) provide deep insights into the mathematical properties of the GOP and vividly explain its connection to the several no-arbitrage conditions discussed in this work.292929See also Hulley and Schweizer (2010) as well as Imkeller and Petrou (2010) for similar results. Theorem 3.15 in Karatzas and Kardaras (2007) describes a set of regularity conditions which guarantee that there exists one and only one GOP with respect to F. In this case, this is also an NP with respect to F. Conversely, if an NP with respect to F exists, the regularity conditions are satisfied and the NP corresponds to the unique GOP with respect to F. Moreover, there exists an NP with finite terminal value if and only if there is NUPBR (Karatzas and Kardaras, 2007, Theorem 4.12). Throughout this section it is assumed that .

If the market is sensitive, every decision at time that is based on the conditional probability for any can be done as well on the basis of . This can be seen as follows: Consider the two -martingales and with and for all . Obviously, these martingales are identical if . Now, the Predictable Stopping Theorem (Jacod and Shiryaev, 2003, Lemma I.2.27) implies that

Since for all (with for ), we have that

In particular, the drift rates conditional on and coincide at every time . Hence, if the GOP with respect to F equals the GOP with respect to E.

As already mentioned, the GOP plays a fundamental role in modern finance. It serves as a benchmark portfolio (Platen, 2006, 2009, Platen and Heath, 2006).303030Under some additional assumptions, the GOP is a linear combination of the market portfolio and the money-market account (Platen, 2006, Platen and Heath, 2006, Ch. 11). Typically, it is assumed that all market participants use the same information flow F or at least that their expectations are rational. There exists an important connection between the GOP and market sensitivity, which can be seen by the following theorem.

Theorem 7 (Benchmarked value process).

Suppose that and . Let be the discounted value process of a normalized F-predictable strategy and the discounted value process of the GOP with respect to E. Further, let with for all be the benchmarked value process of . Then

-

(i)

for all and

-

(ii)

for every -algebra and all we have that

Proof: (i) Since the market is sensitive, represents the discounted value process of the NP with respect to F, which leads to the supermartingale property of . (ii) If we substitute by , the first inequality is an immediate consequence of (i) and the second inequality follows from

The same inequalities with respect to rather than appear after applying the law of iterated expectations. Q.E.D.

Hence, if the market is sensitive, it is impossible to find a normalized F-predictable strategy whose benchmarked value process leads to a positive expected (log-)return, conditional on some information set at any time . The -algebra need not contain . This means it can be any sub--algebra of , e.g., the -algebra generated by a set of technical indicators or statistics based on the history of asset prices at time . This allows us to apply simple hypothesis tests for market sensitivity and/or growth optimality. Here, I ignore the econometric implications of Theorem 7 and concentrate on aspects of financial mathematics.

Let be the discounted value process of the GOP with respect to F and consider any contingent claim for a fixed time of maturity such that

Suppose that there is NFLVR with respect to F and consider an admissible F-predictable strategy that leads to , i.e., . Since is positive, the discounted value process and its left-continuous version must be positive, too. This means is a normalized F-predictable strategy with discounted value process . Hence, the benchmarked value process is a -supermartingale with respect to F and thus

for all . This means

forms a lower bound for the discounted value processes of all admissible F-predictable strategies that lead to . This means an investor who aims at replicating the payoff , but has no more information than F, should try to choose an F-predictable strategy whose discounted value process attains the lower bound with respect to F. By contrast, if the investor has access to some broader information flow , he or she might find a better strategy to obtain . These arguments lead to the following definition (Platen, 2009).313131Platen (2009) only requires , but he explicitly assumes that is positive.

Definition 6 (Fair strategy).

Suppose that and let be the discounted value process of the GOP with respect to F. An admissible F-predictable strategy that leads to the terminal value for any fixed such that

is said to be fair with respect to F if and only if

From the previous arguments, we conclude that the discounted value process of a fair strategy as well as its left-continuous version is always positive.

In general, if some information flow F is available to the investor, the GOP at time should be calculated by and not by , since otherwise he or she could overestimate the fair price of a contingent claim. By contrast, if the market is sensitive, using the information is sufficient. This is the quintessence of the following theorem.

Theorem 8 (Fair strategy).

Suppose that and . If a strategy is fair with respect to E it is fair with respect to F.

Proof: Let be the discounted value process of a fair strategy with respect to E that leads to and be the discounted value process of the GOP with respect to E, so that

for all . Since the market is sensitive, we have that

for all and the GOP with respect to E is also growth optimal with respect to F . Hence, is also fair with respect to F. Q.E.D.

This means an investor who aims at a positive payoff cannot gain anything by taking an information flow F into account if the market is sensitive to F, provided he has already found a fair strategy with respect to E.323232The proof of Theorem 8 reveals that the discounted value process of a fair strategy with respect to E coincides with the discounted value process of a fair strategy with respect to F. This means the strategies are identical.

6 The Martingale Hypothesis

The methodological framework that has been chosen in this work does not require a competitive market. In particular, it is not assumed that the market participants are price takers. This means any individual investment decision () can have an influence on and vice versa. Hence, the financial market can be highly illiquid. The price-taker assumption, i.e., the assumption that each order “gets lost in the masses,” does not adequately describe the pricing mechanism of financial markets. In fact, market sensitivity thrives on the fact that each investment decision has an impact on the asset prices, whereas completeness guarantees that the market participants are able to tailor each financial instrument to their needs. Therefore, completeness and sensitivity mutually support each other and enables us to derive a simple real-world valuation formula. This is done in the subsequent analysis.

A method which comes very close to the target is the benchmark approach discussed in Section 5. Fix any subuniverse with some numéraire asset . If there is , it must hold that

| (3) |

for all , where is the discounted value process of the GOP with respect to F. Unfortunately, the given result represents only a Law of Minimal Price (Platen, 2009) but not a Law of One Price. The reason is twofold: (i) It provides only a lower bound for the discounted price process and (ii) even if (3) was an equality, the conditional expectation in general is not stable under a change of filtration. Another drawback is that for calculating the GOP with respect to F it is not sufficient to take only asset prices into consideration. In general, it is necessary to search for data in F that go beyond E.

In the following, I derive a Law of One Price under the assumption that the market is complete and sensitive. The basic idea is simple: I fix the physical measure and search for a normalized E-predictable strategy such that . This means I treat the strategy like an asset,333333This is not to say that belongs to the asset universe, , which contains only the primary assets in the market. which is possible only because is determined by the evolution of asset prices. Hence, its value process is E-adapted, like every other price process. By contrast, risk-neutral valuation works the other way around: One fixes a numéraire asset and searches for some risk-neutral measure or at least for an EMM .

The idea of fixing the physical measure and searching for an appropriate numéraire such that or at least can be found in Becherer (2001) and Long (1990),343434According to Becherer (2001), this approach even goes back to Vasicek (1977, p. 184). but the results presented in this work differ in several aspects. The aforementioned authors (i) do not study conditions under which the discounted price processes turn out to be uniformly integrable -martingales with respect to F, (ii) do not distinguish between E and F, and (iii) assume a financial market with finite lifetime, so that the essential requirement of uniform integrability becomes superfluous.

Most of the following results require a complete financial market. They are applicable both to simple and complex markets but, due to the arguments given in Section 4.1, it is tempting to think about a market with an infinite number of assets. This leads to a model-independent framework, i.e., although the market is assumed to be complete, it is not necessary to make any specific assumption about the (discounted) price processes.

Proposition 2.

Let be some numéraire asset and suppose that the financial market is complete. If the F-RNP associated with any is E-adapted it follows that .

Proof: Consider any square-integrable -martingale with respect to E . Hence, is uniformly -integrable and converges to some limit . Choose any real number and define

so that . The market is complete and so the contingent claims and can be attained by two E-predictable trading strategies with discounted value processes and . It follows that

for all . Hence, we obtain

for all and so is a (square-integrable) -martingale with respect to F . This means E is -immersed in F. Now, Proposition 1 guarantees that . Q.E.D.

The usual definition of the GOP can be applied to complex financial markets by allowing the investors to operate in any subuniverse of . A GOP based on a subuniverse is simply said to be “the GOP” if and only if there is no GOP in any other subuniverse that leads to a higher growth rate. The GOP remains growth optimal if prices and values are denominated in the basic currency. Moreover, as is shown in Section 5, every GOP with respect to E is also growth optimal with respect to F if the market is sensitive.

Proposition 3.

Let be any normalized E-predictable strategy and suppose that . Then is the unique GOP with respect to F.

Proof: Fix any subuniverse containing the assets that are used by the strategy and take as a numéraire. Further, let be any normalized F-predictable strategy in . From Theorem 2.9 in Delbaen and Schachermayer (1994) it follows that the discounted value process of is a -supermartingale with respect to F. This means is an NP in with respect to F. Theorem 3.15 in Karatzas and Kardaras (2007) implies that is the unique GOP in with respect to F. The same holds for every other subuniverse that contains the assets of . Further, it is clear that any other subuniverse that does not contain all assets used by cannot lead to a higher growth rate. This means must be growth optimal with respect to F. By the same arguments, we may conclude that is unique. Q.E.D.

Theorem 9 (Growth-optimal portfolio).

Every complete and sensitive financial market contains a unique E-predictable GOP with respect to F.

Proof: Consider some numéraire asset . Let be the unique risk-neutral measure and the E-RNP associated with . From Lemma 3 we know that is an E-DFP, i.e., is a -martingale with respect to E for each discounted price process . Since the market is sensitive, Theorem 6 implies that is also a -martingale with respect to F for each discounted price process . Further, the market is complete and so there exists an E-predictable trading strategy with discounted value process such that and

for all . This means is a -martingale with respect to F for each discounted price process . Let with for all be the nominal value process of , so that each is a -martingale with respect to F, i.e., . Now, Proposition 3 implies that is the unique GOP with respect to F. Q.E.D.

The following theorem is the main result of this work. It provides a simple characterization of market completeness and sensitivity. Moreover, it clarifies that under these ideal circumstances, the GOP with respect to F is E-predictable and thus can be considered a “benchmark asset.”

Theorem 10 (Martingale Hypothesis).

A complete financial market is sensitive if and only if there exists a normalized E-predictable strategy such that . The strategy corresponds to the unique GOP with respect to F.

Proof: I start with the “only if” part. The proof of Theorem 9 reveals that there exists an E-predictable GOP with respect to F with nominal value process . Since the market is sensitive, we obtain

for all and , where represents the unique risk-neutral measure. This means each -martingale is closed by , i.e., . For the “if” part consider some numéraire asset and note that with for all is a positive uniformly integrable -martingale with respect to F such that and . This means is an F-DFP with associated probability measure and we have that

for all and . Thus each -martingale is closed by , i.e., . Since is a singleton, we conclude that . This means is the F-RNP associated with and, since is E-adapted, Proposition 2 implies that . Finally, from and Proposition 3, we conclude that is the unique GOP with respect to F. Q.E.D.

Hence, every complete financial market is sensitive to the information flow F if and only if the discounted price processes turn out to be uniformly integrable -martingales with respect to F after an appropriate choice of the numéraire. This leads to a Law of One Price. In fact, we have that with for all . Since the nominal value process is E-adapted, we can always substitute by . Theorem 10 also clarifies that the DFP given by Theorem 3 is directly related to the GOP. More precisely, represents a state-price density or pricing kernel, so that

Samuelson (1965) claims that the nominal price process is a -martingale with respect to the natural filtration if future prices are “properly anticipated.” In his proof he ignores interest and risk aversion. It is clear that this Martingale Hypothesis cannot be maintained if one takes interest and/or risk preferences into consideration. Theorem 10 provides a generalization of Samuelson’s Martingale Hypothesis. The trick is to apply the “correct” discount factor to asset prices, i.e., to choose the GOP as a numéraire, given that the market is complete and sensitive. In this case, we obtain the simple real-world valuation formula for all and each contingent claim . This solves the remaining part of the fundamental problem discussed at the beginning of the introduction and at the end of Section 3.

The actual challenge is to find the GOP. In practical situations, this can be done by applying econometric procedures. For this purpose, it is not necessary to propagate any specific market model. Another possibility is to approximate the GOP by a linear combination of the market portfolio and the money-market account (Platen, 2006, Platen and Heath, 2006, Ch. 11). In either case, since the market is sensitive, it is not necessary to investigate any information that goes beyond the evolution of asset prices and does not exceed the general information flow F.

7 Conclusion

After an appropriate choice of the numéraire, the discounted price processes in a complete financial market are uniformly integrable martingales under the real-world measure if and only if the market is sensitive. The given result is model independent, i.e., the underlying probabilistic assumptions are minimal, and it highlights two fundamental axioms of neoclassical finance: (i) The absence of arbitrage opportunities and (ii) informational efficiency. An arbitrage opportunity can be either a free lunch with vanishing risk or a dominant strategy. This particular notion of arbitrage is motivated by the 3rd FTAP. Informational efficiency means that the evolution of asset prices is immersed in a general flow of information with respect to the physical measure. Roughly speaking, the market prices must “fully reflect” or “rapidly adjust to” all relevant information.

To the best of my knowledge this work presents novel results. For example, it extends the 3rd FTAP to markets with infinite lifetime. Further, it illustrates how no-arbitrage conditions, completeness, efficiency, and the growth-optimal portfolio are connected to each other. The presented theorems strengthen the general findings that have been thoroughly discussed in the literature under the label of “benchmark approach,” which leads to a Law of Minimal Price. A key observation of this work is that in a complete and sensitive market, the growth-optimal portfolio is determined by the evolution of asset prices and so we obtain a Law of One Price.

The given results could be used for constructing hypothesis tests for market efficiency. For example, one can test the null hypothesis that a market is efficient with respect to the flow of public or private information. Additionally, it is possible to test whether a trader makes use of information that is not “fully reflected” by the asset prices. The econometric implications of the presented results and their empirical implementation shall be addressed in the future.

Acknowledgments

I would like to thank very much Martin Larsson for his splendid answers to my questions related to martingale theory and his comments on the manuscript. Many thanks belong also to Dirk Becherer, Robert Jarrow, Christoph Memmel, Ilya Molchanov, and Alexander Szimayer.

Appendix A Appendix

A.1 The Classic Approach to Market Efficiency

The literature on the Efficient-Market Hypothesis is overwhelming and even the number of review papers is huge. Here, I give only a very brief overview of the classic approach to market efficiency.353535See Sewell (2011) for a comprehensive discussion on the history of the Efficient-Market Hypothesis. This suggests that the market is a fair game (Fama, 1970):

-

(i)

Each asset has a fair equilibrium expected return conditional on for all and

-

(ii)

the true expectations conditional on coincide with the fair equilibrium expected returns given by (i) at every time .363636The assumption that asset returns are serially independent or that they follow a random walk is neither necessary nor sufficient for a fair game (Campbell et al., 1997, LeRoy, 1973, Lucas, 1978).

Another, more general, interpretation of market efficiency is due to Jensen (1978):

“A market is efficient with respect to information set if it is impossible to make economic profits by trading on the basis of information set . By economic profits, we mean the risk adjusted returns net of all costs.”

Similarly, Timmermann and Granger (2004) conclude that,

“A market is efficient with respect to the information set, , search technologies, , and forecasting models, , if it is impossible to make economic profits by trading on the basis of signals produced from a forecasting model in defined over predictor variables in the information set and selected using a search technology in .”

For identifying “economic profits” we need to define “equilibrium expected” or “risk adjusted” asset returns. This leads to the following problem (Campbell et al., 1997):

“[…] any test of efficiency must assume an equilibrium model that defines normal security returns. If efficiency is rejected, this could be because the market is truly inefficient or because an incorrect equilibrium model has been assumed. This joint hypothesis problem means that market efficiency as such can never be rejected.”

The joint-hypothesis problem can be considered the Achilles heel of the classic approach to market efficiency (Fama, 1991). There exist many definitions or interpretations of the Efficient-Market Hypothesis. Some of them are discussed in Section 4.2. Definition 5 does not require any equilibrium model and thus it is not affected by the joint-hypothesis problem.

A.2 Arbitrage-Free Markets

A.2.1 No-Arbitrage Conditions

In the following, I use the shorthand notation for the final gain of the strategy .373737Here, it is implicitly assumed that the limit exists almost surely. An admissible F-predictable strategy that is such that

-

(i)

and

-

(ii)

is said to be an arbitrage. Now, consider two admissible F-predictable strategies and . The strategy is said to dominate if and only if

-

(i)

and

-

(ii)

.

By contrast, if there is no admissible F-predictable strategy that dominates , the latter is said to be F-maximal (Delbaen and Schachermayer, 1998).

Dominance can be interpreted as “relative arbitrage” (Merton, 1973).383838For a similar concept see, e.g., Karatzas and Fernholz (2005) as well as Platen (2004). A strategy that is dominated by another strategy can be considered Pareto inefficient. This is because the final gain of the dominating strategy can never be worse, but it is better in some possible states of the world. I say that there is no dominance if and only if each single asset in is F-maximal. ND implies no arbitrage (NA) but the converse is not true. Moreover, the ND condition implies that no asset can be dominated on any time interval with . Otherwise, one could hold the corresponding asset from time to time , switch to the dominant strategy at time , apply this strategy from time to time , switch back to the asset at time and maintain this position until the end of time. This would dominate the asset and so the ND condition would be violated.393939See Jarrow and Larsson (2012) for a similar argument.

Let be a sequence of admissible F-predictable strategies and the final gain of the -th strategy ().404040Each is bounded below by a common number . This is implicit in the definition of in Delbaen and Schachermayer (1994, p. 473). The sequence is said to be a free lunch with vanishing risk if and only if there exist some real numbers such that as and for each there exists a natural number such that

A free lunch with vanishing risk is essentially an arbitrage, since the maximum loss can be made arbitrarily small by choosing a sufficiently large .424242It is worth emphasizing that the loss vanishes uniformly (on the essential part of ) as and not only in probability (Delbaen and Schachermayer, 1994, p. 501). No free lunch with vanishing risk implies NA but the converse is not true. NFLVR also guarantees that the final gain of every admissible strategy exists and is finite (Delbaen and Schachermayer, 1994).