Generalized Perron–Frobenius Theorem for Nonsquare Matrices

Abstract

The celebrated Perron–Frobenius (PF) theorem is stated for irreducible nonnegative square matrices, and provides a simple characterization of their eigenvectors and eigenvalues. The importance of this theorem stems from the fact that eigenvalue problems on such matrices arise in many fields of science and engineering, including dynamical systems theory, economics, statistics and optimization. However, many real-life scenarios give rise to nonsquare matrices. Despite the extensive development of spectral theories for nonnegative matrices, the applicability of such theories to non-convex optimization problems is not clear. In particular, a natural question is whether the PF Theorem (along with its applications) can be generalized to a nonsquare setting. Our paper provides a generalization of the PF Theorem to nonsquare matrices. The extension can be interpreted as representing client-server systems with additional degrees of freedom, where each client may choose between multiple servers that can cooperate in serving it (while potentially interfering with other clients). This formulation is motivated by applications to power control in wireless networks, economics and others, all of which extend known examples for the use of the original PF Theorem.

We show that the option of cooperation between servers does not improve the situation, in the sense that in the optimal solution no cooperation is needed, and only one server needs to serve each client. Hence, the additional power of having several potential servers per client translates into choosing the best single server and not into sharing the load between the servers in some way, as one might have expected.

The two main contributions of the paper are (i) a generalized PF Theorem that characterizes the optimal solution for a non-convex nonsquare problem, and (ii) an algorithm for finding the optimal solution in polynomial time. Towards achieving those goals, we extend the definitions of irreducibility and largest eigenvalue of square matrices to nonsquare ones in a novel and non-trivial way, which turns out to be necessary and sufficient for our generalized theorem to hold. The analysis performed to characterize the optimal solution uses techniques from a wide range of areas and exploits combinatorial properties of polytopes, graph-theoretic techniques and analytic tools such as spectral properties of nonnegative matrices and root characterization of integer polynomials.

1 Introduction

Motivation and main results.

This paper presents a generalization of the well known Perron–Frobenius (PF) Theorem [15, 27]. As a motivating example, let us consider the Power control problem, one of the most fundamental problems in wireless networks. The input to this problem consists of receiver-transmitter pairs and their physical locations. All transmitters are set to transmit at the same time with the same frequency, thus causing interference to the other receivers. Therefore, receiving and decoding a message at each receiver depends on the transmitting power of its paired transmitter as well as the power of the rest of the transmitters. If the signal to interference ratio at a receiver, namely, the signal strength received by a receiver divided by the interfering strength of other simultaneous transmissions, is above some reception threshold , then the receiver successfully receives the message, otherwise it does not [30]. The power control problem is then to find an optimal power assignment for the transmitters, so as to make the reception threshold as high as possible and ease the decoding process.

As it turns out, this power control problem can be solved elegantly by casting it as an optimization program and using the Perron–Frobenius (PF) Theorem [40]. The theorem can be formulated as dealing with the following optimization problem (where ):

| maximize subject to: | (1) | ||

Let denote the optimal solution for Program (1). The Perron–Frobenius (PF) Theorem characterizes the solution to this optimization problem and shows the following:

Theorem 1.1

(PF Theorem, short version, [15, 27]) Let be an irreducible nonnegative matrix. Then , where is the largest eigenvalue of , called the Perron–Frobenius (PF) root of . There exists a unique (eigen-)vector , , such that , called the Perron vector of . (The pair is hereafter referred to as an eigenpair of .)

Returning to our motivating example, let us consider a more complicated variant of the power control problem, where each receiver has several transmitters that can transmit to it (and only to it) synchronously. Since these transmitters are located at different places, it may conceivably be better to divide the power (or work) among them, to increase the reception threshold at their common receiver. Again, the question concerns finding the best power assignment among all transmitters.

In this paper we extend Program (1) to nonsquare matrices and consider the following extended optimization problem, which in particular captures the multiple transmitters scenario. (Here , .)

| maximize subject to: | (2) | ||

We interpret the nonsquare matrices as representing some additional freedom given to the system designer. In this setting, each entity (receiver, in the power control example) has several affectors (transmitters, in the example), referred to as its supporters, which can cooperate in serving it and share the workload. In such a general setting, we would like to find the best way to organize the cooperation between the supporters of each entity.

The original problem was defined for a square matrix, so the appearance of eigenvalues in the characterization of its solution seems natural. In contrast, in the generalized setting the situation seems more complex. Our main result is an extension of the PF Theorem to nonsquare matrices and systems that give rise to an optimization problem in the form of (2), with optimal solution .

Theorem 1.2

(Nonsquare PF Theorem, short version) Let be an irreducible nonnegative system (to be made formal later). Then , where is the smallest Perron–Frobenius (PF) root of all square sub-systems (defined formally later). There exists a vector such that and has entries greater than 0 and zero entries (referred to as a solution).

In other words, the theorem implies that the option of cooperation does not improve the situation, in the sense that in the optimum solution, no cooperation is needed and only one supporter per entity needs to work. Hence, the additional power of having several potential supporters per entity translates into choosing the best single supporter and not into sharing the load between the supporters in some way, as one might have expected.

As it turns out, the lion’s share of our analysis involves such a characterization of the optimal solution for (the non-convex) problem of Program (2). The main challenge is to show that at the optimum, there exists a solution in which only one supporter per entity is required to work; we call such a solution a solution. Namely, the structure that we establish is that the optimal solution for our nonsquare system is in fact the optimal solution of an embedded square PF system. Indeed, to enjoy the benefits of an equivalent square system, one should show that there exists a solution in which only one supporter per entity is required to work. Interestingly, it turned out to be relatively easy to show that there exists an optimal “almost ” solution, in which each entity except at most one has a single active supporter and the remaining entity has at most two active supporters. Despite the presumably large “improvement” of decreasing the number of servers from to , this still leaves us in the frustrating situation of a nonsquare system, where no spectral characterization for optimal solutions exists. In order to allow us to characterize the optimal solution using the eigenpair of the best square matrix embedded within the nonsquare system, one must overcome this last hurdle, and reach the “phase transition” point of servers, in which the system is square. Our main efforts went into showing that the remaining entity, too, can select just one supporter while maintaining optimality, ending with a square irreducible system where the traditional PF Theorem can be applied. Proving the existence of an optimal solution requires techniques from a wide range of areas to come into play and provide a rich understanding of the system on various levels. In particular, the analysis exploits combinatorial properties of polytopes, graph-theoretic techniques and analytic tools such as spectral properties of nonnegative matrices and root characterization of integer polynomials.

In the context of the above example of power control in wireless network with multiple transmitters per receiver, a solution means that the best reception threshold is achieved when only a single transmitter transmits to each receiver. Other known applications of the PF Theorem can also be extended in a similar manner. An Example for such applications is the input-output economic model [28]. In this economic model, each industry produces a commodity and buys commodities (raw materials) from other industries. The percentage profit margin of an industry is the ratio of its total income and total expenses (for buying its raw materials). It is required to find a pricing maximizing the ratio of the total income and total expenses of all industries. The extended PF variant of the problem concerns the case where an industry can produce multiple commodities instead of just one. In this example, the same general phenomenon holds: each industry should charge money only for one of the commodities it produces. That is, in the optimal pricing, one commodity per industry has nonzero price, therefore the optimum is a solution. For a more detailed discussion of applications, see Sec. 7. In addition, in Sec. 6, we provide a characterization of systems in which a solution does not exist.

While in the original setting the PF root and PF vector can be computed in polynomial time, this is not clear in the extended case, since the problem is not convex [6] (and not even log-convex) and there are exponentially many choices in the system even if we know that the optimal solution is and each entity has only two supporters to choose from. Our second main contribution is providing a polynomial time algorithm to find and . The algorithm uses the fact that fixing yields a relaxed problem which is convex (actually it becomes a linear program). This allows us to employ the well known interior point method [6], for testing a specific for feasibility. Hence, the problem reduces to finding the maximum feasible , and the algorithm does so by applying binary search on . Clearly, the search results in an approximate solution, in fact yielding a fully polynomial time approximation scheme (FPTAS) for program (2). This, however, leaves open the intriguing question of whether program (2) is polynomial. Obtaining an exact optimal , along with an appropriate vector , is thus another challenging aspect of the problem.

A central notion in the generalized PF theorem is the irreducibility of the system. While irreducibility is a well-established concept for square systems, it is less obvious how to define irreducibility for a nonsquare matrix or system as in Program (2). We provide a suitable definition based on the property that every maximal square (legal) subsystem is irreducible, and show that our definition is necessary and sufficient for the theorem to hold. A key tool in our analysis is what we call the constraint graph of the system, whose vertex set is the set on constraints (one per entity) and whose edges represent direct influence between the constraints. For a square system, irreducibility is equivalent to the constraint graph being strongly connected, but for nonsquare systems the situation is more delicate. Essentially, although the matrices are not square, the notion of constraint graph is well defined and provides a valuable square representation of the nonsquare system (i.e., the adjacency matrix of the graph). In [34, PF_Archive], we also present a polynomial-time algorithm for testing the irreducibility of a given system, which exploits the properties of the constraint graph.

Related work. The PF Theorem establishes the following two important “PF properties” for a nonnegative square matrix : (1) the Perron–Frobenius property: has a maximal nonnegative eigenpair. If in addition the matrix is irreducible then its maximal eigenvalue is strictly positive, dominant and with a strictly positive eigenvector. Thus nonnegative irreducible matrix is said to enjoy the strong Perron–Frobenius property [15, 27]. (2) the Collatz–Wielandt property (a.k.a. min-max characterization): the maximal eigenpair is the optimal solution of Program (1) [12, 38].

Matrices with these properties have played an important role in a wide variety of applications. The wide applicability of the PF Theorem, as well as the fact that the necessary and sufficient properties required of a matrix for the PF properties to hold are still not fully understood, have led to the emergence of many generalizations. We note that whereas all generalizations concern the Perron–Frobenius property, the Collatz–Wielandt property is not always established. The long series of existing PF extensions includes [23, 14, 31, 19, 33, 20, 29, 22]. We next discuss these extensions in comparison to the current work.

Existing PF extensions can be broadly classified into four classes. The first concerns matrices that do not satisfy the irreducibility and nonnegativity requirements. For example, [23, 14] establish the Perron-Frobenius property for almost nonnegative matrices or eventually nonnegative matrices. A second class of generalizations concerns square matrices over different domains. For example, in [31], the PF Theorem was established for complex matrices . In the third type of generalization, the linear transformation obtained by applying the nonnegative irreducible matrix is generalized to a nonlinear mapping [19, 33], a concave mapping [20] or a matrix polynomial mapping [29].

Last, a much less well studied generalization deals with nonsquare matrices, i.e., matrices in for . Note that when considering a nonsquare system, the notion of eigenvalues requires definition. There are several possible definitions for eigenvalues in nonsquare matrices. One possible setting for this type of generalizations considers a pair of nonsquare “pencil” matrices , where the term “pencil” refers to the expression , for . Of special interest here are the values that reduce the pencil rank, namely, the values satisfying for some nonzero . This problem is known as the generalized eigenvalue problem [22, 11, 5, 21], which can be stated as follows: Given matrices , find a vector , , so that . The complex number is said to be an eigenvalue of relative to iff for some nonzero and is called the eigenvector of relative to . The set of all eigenvalues of relative to is called the spectrum of relative to , denoted by .

Using the above definition, [22] considered pairs of nonsquare matrices and was the first to characterize the relation between and required to establish their PF property, i.e., guarantee that the generalized eigenpair is nonnegative. Essentially, this is done by generalizing the notions of positivity and nonnegativity in the following manner. A matrix is said to be positive (respectively,nonnegative) with respect to , if implies that (resp., ). Note that for , these definitions coincide with the classical definitions of a positive (resp., nonnegative) matrix. Let , for , be such that the rank of or the rank of is . It is shown in [22] that if is positive (resp., nonnegative) with respect to , then the generalized eigenvalue problem has a discrete and finite spectrum, the eigenvalue with the largest absolute value is real and positive (resp., nonnegative), and the corresponding eigenvector is positive (resp., nonnegative). Observe that under the definition used therein, the cases where (which is the setting studied here) is uninteresting, as the columns of are linearly dependent for any real , and hence the spectrum is unbounded.

Despite the significance of [22] and its pioneering generalization of the PF Theorem to nonsquare systems, it is not clear what are the applications of such a generalization, and no specific implications are known for the traditional applications of the PF theorem. Moreover, although [22] established the PF property for a class of pairs of nonsquare matrices, the Collatz–Wielandt property, which provides the algorithmic power for the PF Theorem, does not necessarily hold with the spectral definition of [22]. In addition, since no notion of irreducibility was defined in [22], the spectral radius of a nonnegative system (in the sense of the definition of [22]) might be zero, and the corresponding eigenvector might be nonnegative in the strong sense (with some zero coordinates). These degenerations can be handled only by considering irreducible nonnegative matrices, as was done by Frobenius in [15].

In contrast, the goal of the current work is to develop the spectral theory for a pair of nonnegative matrices in a way that is both necessary and sufficient for both the PF property and the Collatz–Wielandt property to hold (allowing the nonsquare system to be of the “same power” as the square systems considered by Perron and Frobenius). Towards this we define the eigenvalues and eigenvectors of pairs of matrices and in a novel manner. Such eigenpair satisfies . In [22], alternative spectral definitions for pairs of nonsquare matrices and are provided. We note that whereas in [22] formulation, the maximum eigenvalue is not bounded if , with our definition it is bounded.

Let us note that although the generalized eigenvalue problem has been studied for many years, and multiple approaches for nonsquare spectral theory in general have been developed, the algorithmic aspects of such theories with respect to the the Collatz–Wielandt property have been neglected when concerning nonsquare matrices (and also in other extensions). This paper is the first, to the best of our knowledge, to provide spectral definitions for nonsquare systems that have the same algorithmic power as those made for square systems (in the context of the PF Theorem). The extended optimization problem that corresponds to this nonsquare setting is a nonconvex problem (which is also not log-convex), therefore its polynomial solution and characterization are of interest.

Another way to extend the notion of eigenvalues and eigenvectors of a square matrix to a nonsquare matrix is via singular value decompositions (SVD) [25]. Formally, the singular value decomposition of an real matrix is a factorization of the form , where is an real or complex unitary matrix, is an diagonal matrix with nonnegative reals on the diagonal, and (the conjugate transpose of ) is an real or complex unitary matrix. The diagonal entries of are known as the singular values of . After performing the product , it is clear that the dependence of the singular values of is linear. In case all the inputs of are positive, we can add the absolute value, and thus the SVD has a flavor of dependence. In contrast to the SVD definition, here we are interested in finding the maximum, so our interpretation has the flavor of .

In a recent paper [37], Vazirani defined the notion of rational convex programs as problems that have a rational number as a solution. Our paper can be considered as an example for algebraic programming, since we show that a solution to our problem is an algebraic number.

2 Preliminaries

2.1 Definitions and terminology

Consider a directed graph . A subset of the vertices is called a strongly connected component if contains a directed path from to for every . is said to be strongly connected if is a strongly connected component.

Let be a square matrix. Let , , be the set of real eigenvalues of . The characteristic polynomial of , denoted by , is a polynomial whose roots are precisely the eigenvalues of , , and it is given by

| (3) |

where is the identity matrix. Note that iff . The spectral radius of is defined as The element of a vector is given by , and the entry of a matrix is denoted . Let (respectively, ) denote the -th row (resp., column) of . Vector and matrix inequalities are interpreted in the component-wise sense. is positive (respectively, nonnegative) if all its entries are. is primitive if there exists a natural number such that . is irreducible if for every , there exists a natural such that An irreducible matrix is periodic with period if for .

2.2 Algebraic Preliminaries

Generalization of Cramer’s rule to homogeneous linear systems.

Let (respectively, ) denote the -th row (resp., column) of . Let denote the matrix that results from by removing the -th row and the -th column. Similarly, and denote the matrix after removing the -th row (respectively, -th column) from . Let , i.e., the -th column of without the last element . For , denote .

We make use of the following extension of Cramer’s rule to homogeneous square linear systems.

Claim 2.1

Let such that is invertible. Then,

-

(a)

-

(b)

Proof: Since , it follows that . As is invertible, we can apply Cramer’s rule to express . Let , for and . By Cramer’s rule, it then follows that . We next claim that . To see this, note that and are composed of the same set of columns up to order. In particular, can be transformed to by a sequence of swaps of consecutive columns starting from the -th column of . It therefore follows that establishing part (a) of the claim. We continue with part (b). Since , it follows that or that

We now turn to a nonsquare matrix . The matrix corresponds to the upper left square matrix of . Let i.e., and . Note that , i.e., both are square matrices.

Claim 2.2

Let and is invertible. Then,

-

(a)

-

(b)

Proof: Since , it follows that

.

As is invertible we can apply Cramer’s rule to express .

Let .

Let and

.

By the properties of the determinant function, it follows, that

We now turn to see the connection between and . Note that and correspond to the same columns up to order. Specifically, we can now employ the same argument of Claim 2.1 and show that (informally, the square matrix of Claim 2.1 is replaced by a “combination” of and ). In a similar way, one can show that . We now turn to prove part (b) of the claim. Since , by part (a), we get that

The claim follows.

Separation theorem for nonsymmetric matrices.

We make use of the following fact due to Hall and Porsching [16], which is an extension of the Cauchy Interlacing Theorem for symmetric matrices.

Lemma 2.3 ([16])

Let be a nonegative matrix with eigenvalues . Let be the principle minor of , with eigenvalues , . If is any real eigenvalue of different from , then

for every , with strict inequality on the left if is irreducible.

2.3 PF Theorem for square nonnegative irreducible matrices

The PF Theorem states the following.

Theorem 2.4 (PF Theorem, [15, 27])

Let be a nonnegative irreducible matrix with spectral ratio . Then . There exists an eigenvalue such that , called the Perron–Frobenius (PF) root of . The algebraic multiplicity of is one. There exists an eigenvector such that . The unique normalized vector defined by and is called the Perron–Frobenius (PF) vector. There are no nonnegative eigenvectors for with except for positive multiples of . If is a nonnegative irreducible periodic matrix with period , then has exactly eigenvalues, for and all other eigenvalues of are of strictly smaller magnitude than .

Collatz–Wielandt characterization (the min-max ratio).

Collatz and Wielandt [12, 38] established the following formula for the PF root, also known as the min-max ratio characterization.

Alternatively, this can be written as the following optimization problem.

| (4) |

Let be the optimal solution of Program (4) and let be the corresponding optimal vector. Using the representation of Program (4), Lemma 2.5 translates into the following.

Theorem 2.6

This can be interpreted as follows. Consider the ratio , viewed as the “repression factor” for entity . The task is to find the input vector that minimizes the maximum repression factor over all , thus achieving balanced growth. In the same manner, one can characterize the - ratio. Again, the optimal value (resp., point) corresponds to the PF eigenvalue (resp., eigenvector) of . In summary, when taking to be the PF eigenvector, , and , all repression factors are equal, and optimize the - and - ratios.

3 A generalized PF Theorem for nonsquare systems

3.1 The Problem

System definitions.

Our framework consists of a set of entities whose growth is regulated by a set of affectors , for some . As part of the solution, each affector is set to be either passive or active. If an affector is set to be active, then it affects each entity , by either increasing or decreasing it by a certain amount , which is specified as part of the input. If (resp., ), then is referred to as a supporter (resp., repressor) of . For clarity we may write for . The affector-entity relation is described by two matrices, the supporters gain matrix and the repressors gain matrix , given by

Again, for clarity we may write for , and similarly for .

We can now formally define a system as , where , and . We denote the supporter (resp., repressor) set of by

When is clear from the context, we may omit it and simply write and . Throughout, we restrict attention to systems in which for every . We classify the systems into three types:

-

(a) is the family of Square Systems.

-

(b) is the family of Weakly Square Systems, and

-

(c) is the family of Nonsquare Systems.

The generalized PF optimization problem.

Consider a set of entities and gain matrices , for . The main application of the generalized PF Theorem is the following optimization problem, which is an extension of Program (4).

| maximize | (5) | |||

| (6) | ||||

| (7) | ||||

We begin with a simple observation. An affector is redundant if for every .

Observation 3.1

If is redundant, then in any optimal solution .

In view of Obs. 3.1, we may hereafter restrict attention to the case where there are no redundant affectors in the system, as any redundant affector can be removed and simply assigned .

We now proceed with some definitions. Let denote the value of in , i.e., where the th entry in corresponds to . An affector is active in a solution if . Denote the set of affectors taken to be active in a solution by . Let denote the optimal value of Program (5), i.e., the maximal positive value for which there exists a nonnegative, nonzero vector satisfying the constraints of Program (5). When the system is clear from the context we may omit it and simply write . A vector is feasible for if it satisfies all the constraints of Program (5) with . A vector is optimal for if it is feasible for , i.e., . The system is feasible for if , i.e., there exists a feasible solution for Program (5).

For vector , the total repression on in for a given is . Analogously, the total support for is . We now have the following alternative formulation for the constraints of Eq. (6), stated individually for each entity .

| (8) |

We classify the linear inequality constraints of Program (5) into two types of constraints:

-

(2) Nonnegativity constraints: the constraints of Eq. (7).

When is clear from context, we may omit it and simply write and . As a direct application of the generalized PF Theorem, there is an exact polynomial time algorithm for solving Program (5) for irreducible systems, as defined next.

3.2 Irreducibility of PF systems

Irreducibility of square systems.

A square system is irreducible iff (a) is nonsingular and (b) is irreducible. Given an irreducible square , let

Note the following two observations.

Observation 3.3

(a) If is nonsingular, then

.

(b) If is an irreducible system,

then is an irreducible matrix as well.

Proof: Consider part (a). Since is square, for every . Combining with the fact that is nonsingular, it holds that is equivalent (up to column alternations) to a diagonal matrix with a fully positive diagonal, hence . Part (b) follows by definition.

Throughout, when considering square systems, it is convenient to assume that the entities and affectors are ordered in such a way that is a diagonal matrix, i.e., in (as well as in ) the column corresponds to , the unique supporter of .

Selection matrices.

To define a notion of irreducibility for a nonsquare system , we first present the notion of a selection matrix. A selection matrix is legal for iff for every entity there exists exactly one supporter such that . Such a matrix can be thought of as representing a selection performed on by each entity , picking exactly one of its supporters. Let be the square system corresponding to the legal selection matrix , namely, In the resulting system there are non-redundant affectors. Since redundant affectors can be discarded from the system (by Obs. 3.1), it follows that the number of active affectors becomes at most the number of entities, resulting in a square system. Denote the family of legal selection matrices, capturing the ensemble of all square systems hidden in , by

| (9) |

When is clear from the context, we simply write . Let be a solution for the square system for some . The natural extension of into a solution of the original system is defined by letting if and otherwise.

Observation 3.4

(a)

for every .

(b) For every solution for system , for some matrix ,

its natural extension is a feasible solution for the original .

(c) for every selection matrix .

Irreducibility of nonsquare systems.

We are now ready to define the notion of irreducibility for nonsquare systems, as follows. A nonsquare system is irreducible iff is irreducible for every selection matrix . Note that this condition is the “minimal” necessary condition for our theorem to hold, as explained next. Our theorem states that the optimum solution for the nonsquare system is the optimum solution for the best embedded square system. It is easy to see that for any nonsquare system , one can increase or decrease any entry in the matrices, while maintaining the sign of each entry in the matrices, such that a particular selection matrix would correspond to the optimal square system. With an optimal embedded square system at hand, which is also guaranteed to be irreducible (by the definition of irreducible nonsquare systems), our theorem can then apply the traditional PF Theorem, where a spectral characterization for the solution of Program (4) exists. Note that irreducibility is a structural property of the system, in the sense that it does not depend on the exact gain values, but rather on the sign of the gains, i.e., to determine irreducibility, it is sufficient to observe the binary matrices , treating as . On the other hand, deciding which of the embedded square systems has the maximal eigenvalue (and hence is optimal), depends on the precise values of the entries of these matrices. It is therefore necessary that the structural property of irreducibility would hold for any specification of gain values (while maintaining the binary representation of ). Indeed, consider a reducible nonsquare system, for which there exists an embedded square system that is reducible. It is not hard to see that there exists a specification of gain values that would render this square system optimal (i.e., with the maximal eigenvalue among all other embedded square systems). But since is reducible, the PF Theorem cannot be applied, and in particular, the corresponding eigenvector is no longer guaranteed to be positive.

Claim 3.5

In an irreducible system , for every .

Proof: Assume, toward contradiction, that there exists some affector , and consider a selection matrix for which and . It then follows by Obs. 3.3(a) that is singular. But the irreducibility of implies that is nonsingular for every ; contradiction.

Constraint graphs: a graph theoretic representation.

We now provide a graph theoretic characterization of irreducible systems . Let be the directed constraint graph for the system , defined as follows: , and the rule for a directed edge from to is

| (10) |

Note that it is possible that for some . A graph is robustly strongly connected if is strongly connected for every .

Observation 3.6

Let be an irreducible system.

-

(a) If is square, then is strongly connected.

-

(b) If is nonsquare, then is robustly strongly connected.

Proof: Starting with part (a), in a square system and therefore by definition, the two graphs coincide. Next note that for a diagonal (as can be achieved by column reordering), corresponds to (by treating positive entries as ). Since is irreducible (and hence corresponds to a strongly connected digraph), it follows that the matrix is irreducible, and hence is strongly connected. To prove part (b), consider an arbitrary . Since is irreducible, it follows that is irreducible, and by Obs. 3.6(a), is strongly connected. The claim follows.

Partial selection for irreducible systems.

Let be a subset of affectors in an irreducible system .

Then is a partial selection

if there exists a subset of entities such that (a) , and (b) for every , .

That is, every entity in has a single representative supporter

in . We refer to as the set of entities determined by .

In the system , the supporters

of any that were not selected by , i.e.,

, are discarded.

In other words, the system’s affectors set consists of the selected supporters

, and the supporters of entities that have not made up

their selection in .

We now turn to describe formally. The set of affectors in is given by

.

The number of affectors in is denoted by

.

Recall that the column of the

matrices corresponds to .

Let

be the index of the affector in the new system,

(i.e, the column in the contracted matrices corresponds to ).

Define the partial selection matrix

such that for every

, and

otherwise.

Finally, let

where .

Note that .

Observe that if the selection is a complete legal selection,

then and the system is a square

system. In summary, we have two equivalent representations for square systems

in the nonsquare system :

(a) by specifying a complete selection , ,

and

(b) by specifying the selection matrix,

.

Representations (a) and (b) are equivalent in the sense that the two square systems

and

are the same.

We now show that if the system is irreducible, then so must be

any , for any partial selection .

Observation 3.7

Let be an irreducible system. Then is also irreducible, for every partial selection .

Proof: Recall that a system is irreducible iff every hidden square system is irreducible. I.e., the square system is irreducible for every . We now show that if , then . This follows immediately by Eq. (9) and the fact that .

Agreement of partial selections. Let be partial selections for respectively. Then we denote by the property that the partial selections agree, namely, for every .

Observation 3.8

Consider determined by the partial selections respectively, such that , and . Then also .

Proof: is more restrictive than since it defines a selection for a strictly larger set of entities. Therefore every partial selection that agrees with agrees also with .

Generalized PF Theorem for nonnegative irreducible systems.

Recall that the root of a square system is is the eigenvector of corresponding to . We now turn to define the generalized Perron–Frobenius (PF) root of a nonsquare system , which is given by

| (11) |

Let be the selection matrix that achieves the minimum in Eq. (11). We now describe the corresponding eigenvector . Note that , whereas .

Consider and let , where

| (12) |

We next state our main result, which is a generalized variant of the PF Theorem for every nonnegative nonsquare irreducible system.

Theorem 3.9

Let be an irreducible and nonnegative nonsquare system. Then

-

(Q1) ,

-

(Q2) ,

-

(Q3) ,

-

(Q4) is not unique.

The difficulty: Lack of log-convexity.

Before plunging into a description of our proof, we first discuss a natural approach one may consider for proving Thm. 3.9 in general and solving Program (5) in particular, and explain why this approach fails in this case.

A non-convex program can often be turned into an equivalent convex one by performing a standard variable exchange. This allows the program to be solved by convex optimization techniques (see [35] for more information). An example for a program that’s amenable to this technique is Program (4), which is log-convex (see Claim 3.10(a)), namely, it becomes convex after certain term replacements. Unfortunately, in contrast with Program (4), the generalized Program (5) is not log-convex (see Claim 3.10(b)), and hence cannot be handled in this manner.

More formally, for vector and , denote the component-wise -power of by . An optimization program is log-convex if given two feasible solutions for , their log-convex combination (where “” represents component-wise multiplication) is also a solution for , for every . In the following we ignore the constraint , since we only validate the feasibility of nonzero nonnegative vectors; this constraint can be established afterwards by normalization.

Claim 3.10

Proof: We start with (a). In [24] it is shown that the power-control problem is log-convex. The log-convexity of Perron-Frobenius eigenvalue is also discussed in [6], for completeness we prove it here. We use the same technique of [24] and show it directly for Program (4). Let be a non-negative irreducible matrix and let be two feasible solutions for Program (4) with , resp. . We now show that (where “” represents entry-wise multiplication). is a feasible solution for , for any . I.e., we show that . Let , , . By the feasibility of (resp., ) it follows that (resp., ) for every . It then follows that

| (13) |

Let and . Then Eq. (13) becomes

where the last inequality follows by Holder Inequality which can be safely applied since for every . We therefore get that for every , , concluding that and as required. Part (a) is established. We now consider (b). For vector , , recall that , the first coordinates of . For given repressor and supporter matrices , define the following program. For :

| (14) | |||

This program is equivalent to Program (5). An optimal solution for Program (14) “includes” an optimal solution for Program (5), where and . We prove that Program (14) is not log-convex by showing the following example. Consider the repressor and supporters matrices

It can be verified that and are feasible. However, their log-convex combination is not a feasible solution for this system. Lemma follows.

3.2.1 Algorithm for testing irreducibility

In this subsection, we provide a polynomial-time algorithm for testing the irreducibility of a given nonnegative system . Note that if is a square system, then irreducibility can be tested in a straightforward manner by checking that is irreducible and that is nonsingular.

However, recall that a nonsquare system is irreducible iff every hidden square system , , is irreducible. Since might be exponentially large, a brute-force testing of for every is too costly, hence another approach is needed. Before presenting the algorithm, we provide some notation.

Consider a directed graph . Denote the set of incoming neighbors of a node by . The incoming neighbors of a set of nodes is denoted .

Algorithm Description.

To test irreducibility, Algorithm Irr_Test (see Fig. 1) must verify that the constraint graph of every is strongly connected. The algorithm consists of at most rounds. In round , it is given as input a partition of into disjoint clusters such that . For round , the input is a partition of the entity set into singleton clusters . The output at round is a coarser partition , in which at least two clusters of were merged into a single cluster in . The partition is formed as follows. The algorithm first forms a graph on the clusters of the input partition , treating each cluster as a node, and including in a directed edge from to if and only if there exists an entity node such that each of its supporters is a repressor of some entity , i.e., .

The partition is now formed by merging clusters that belong to the same strongly connected component in into a single cluster in . Each cluster of corresponds to a unique strongly connected component in . If contains no strongly connected component except for singletons, which implies that no two cluster nodes of can be merged, then the algorithm declares the system as reducible and halts. Otherwise, it proceeds with the new partition . Importantly, in there are at least two entity subsets that belong to distinct clusters in but to the same cluster node in . If none of the rounds ends with the algorithm declaring the system reducible (due to clusters “merging” failure), then the procedure proceeds with the cluster merging until at some round the remaining partition consists of a single cluster node that encompasses the entire entity set.

Algorithm Irr_Test() 1. ; 2. ; 3. for every ; 4. ; 5. While do: (a) , for every ; (b) . (c) Let ; (d) number of strongly connected components in ; (e) If and , then return “no”. (f) Decompose into strongly connected components . (g) for every . (h) ; (i) ; 6. Return “yes”;

Analysis.

We first provide some high level intuition for the correctness of the algorithm. Recall, that the goal of the algorithm is to test whether the entire entity set resides in a single strongly connected component in the constraint graph for every selection matrix . This test is performed by the algorithm in a gradual manner by monotonically increasing the subsets of nodes that belong to the same strongly connected component in every . In the beginning of the execution, the most one can claim is that every entity is in its own strongly connected component. Over time, clusters are merged while maintaining the invariant that all entities of the same cluster belong to the same strongly connected component in every . More formally, the following invariant is maintained in every round : the entities of each cluster of the graph are guaranteed to be in the same strongly connected component in the constraint graph for every selection matrix . We later show that if the system is irreducible, then the merging process never fails and therefore the last partition consists of a single cluster node that contains all entities, and by the invariant, all entities are guaranteed to be in the same strongly connected component in the constraint graph of any hidden square subsystem.

We now provide some high level explanation for the validity of this invariant. Starting with round , each cluster node is a singleton and every singleton entity is trivially in its own strongly connected component in any constraint graph . Assume the invariant holds up to round , and consider round . The key observation in this context is that the new partition is defined based on the graph , whose edges are independent of the specific supporter selection that is made by the entities (and that determines the resulting hidden square subsystem). This holds due to the fact that a directed edge between the clusters exists if and only if there exists an entity node such that each of its supporter is a repressor of some entity . Therefore, if the edge exists in the , then it exists also in the cluster graph corresponding to the constraint graph (i.e., the graph formed by representing every strongly connected component of by a single node) for every hidden square subsystem , no matter which supporter was selected by for . Hence, under the assumption that the invariant holds for , the coarse-grained representation of the clusters of in is based on their membership in the same strongly connected component in the “selection invariant” graph , thus the invariant holds also for .

We next formalize this argumentation. We say that round is successful if contains a strongly connected component of size greater than 1. We begin by proving the following.

Claim 3.11

For every successful round , the partition satisfies the following properties.

-

(A1) is a partition of , i.e., , for every , and .

-

(A2) Every is a strongly connected component in the constraint graph for every selection matrix .

Proof: By induction on . Clearly, since for every , Properties (A1) and (A2) trivially hold for . We now show that if round is successful, then (A1) and (A2) hold for . Since the edges of exist also in the corresponding cluster graph of under any selection of the entities, the clusters of that are merged into a single strongly connected component in , belong also to the same strongly connected component in the constraint graph of every . Next, assume these properties to hold for every round up to and consider round . Since round is successful, any prior round was successful as well, and thus the induction assumption can be applied on round . In particular, since corresponds to strongly connected components of , it represents a partition of the clusters of . By the induction assumption for round , Property (A1) holds for and therefore is a partition of the entity set . Since corresponds to a partition of , it is a partition of as well so (A1) is established. Property (A2) holds for by the same argument provided for the induction base. The claim follows.

We next show that the algorithm return “yes” for every irreducible system. Specifically, we show that for an irreducible system, if then round is successful, i.e., the merging operation of the cluster graph succeeds. Once contains a single cluster (containing all entities), the algorithm terminates and returns “yes”. We first provide an auxiliary claim.

Claim 3.12

If is irreducible and , then for every .

Proof: First note that if is defined, then round was successful. Therefore, by Property (A1) of Cl. 3.11, is a partition of the entity set . Assume, towards contradiction that the claim does not hold, and let be such that . Denote the set of incoming neighbors of component in the constraint graph by . Since is irreducible, the vertices of are reachable from the outside, so . Let the repressors set of be . We now construct a square hidden system which is reducible, in contradiction to the irreducibility of . Specifically, we look for a selection matrix satisfying that for every entity , its selected supporter in (i.e., the one for which ) is not a repressor of any of the entities in , i.e., . Recall, that since is irreducible, the supporter sets are pairwise disjoint (see Claim 3.5). Note that since , such a selection matrix exists. To see this, assume, towards contradiction that does not exist. This implies that there exists an entity such that and therefore an affector in could not be selected for . Hence, . Let be the cluster such that . Since is a partition of the entity set , such exists. Since , it implies that the edge , in contradiction to the fact that has no incoming neighbors in . We therefore conclude that exists.

We now show that is reducible. In particular, we show that the incoming degree of the component (from entities in other components) in the constraint graph of the square system , is zero, i.e., . Assume, towards contradiction, that there exists a directed edge from entity to some in . This implies that exists in the constraint graph of the original (nonsquare) system and thus is in . Let be the selected supporter of in . By construction of , , in contradiction to the fact that the edge exists.

Since there exists a node in with no incoming neihbors, this graph is not strongly connected, implying that is reducible.

Finally, as is irreducible, it holds that every hidden square system is irreducible, in particular , hence, contradiction. The claim follows.

Lemma 3.13

If is irreducible then Algorithm Irr_Test() returns “yes”.

Proof: By Cl. 3.12, we have that if is irreducible and , then every node in has an incoming edge, which necessitates that there exists a (directed) cycle , for in . Since the nodes in such cycle are strongly connected, they can be merged in , and therefore round is successful. Moreover, since at least two clusters of are merged into a single cluster in , we have that . This means that the merging never fails as long as , so is monotonically decreasing. It follows that the algorithm terminates within at most rounds with a “yes”. The Lemma follows.

We now consider a reducible system and show that Irr_Test() returns “no”.

Lemma 3.14

If is reducible, then Algorithm Irr_Test() returns “no”.

Proof: Towards contradiction, assume otherwise, i.e., suppose that the algorithm accepts . This implies that every round in which is successful.

The reducibility of implies that there exists (at least one) hidden square system which is reducible, namely, its constraint graph is not strongly connected. Thus contains at least two nodes and that belong to distinct strongly connected components in . Note that and are in distinct clusters in , but belong to the same cluster in the partition of the final . Therefore, there must exists a round in which the cluster that contains and the cluster that contains appeared in the same strongly connected component in and were merged into a single strongly connected component in . (Note that since is a successful round, is a partition of the entity set (Prop. (A1) of Cl. 3.11) and therefore and exist.) Since round is successful (otherwise the algorithm would terminates with “no”), by to Property (A2) of Cl. 3.11, it follows that the entity subset of the unified cluster is in the same connected component in the constraint graph for every . Since as well it holds that and are in the same connected component in . Hence, contradiction. The lemma follows.

By Lemmas 3.13 and 3.14 it follows that Algorithm Irr_Test() returns “yes” iff the system is irreducible, which establish the correctness of the algorithm.

Claim 3.15

Algorithm Irr_Test terminates in rounds.

Proof: The algorithm consists of at most rounds In each round , it constructs the cluster graph in time . The decomposition into strongly connected components can be done in . The claim follows.

Theorem 3.16

There exists a polynomial time algorithm for deciding irreducibility on nonnegative systems.

4 Proof of the generalized PF Theorem

4.1 Proof overview and roadmap

Our main challenge is to show that the optimal value of Program (5) is related to an eigenvalue of some hidden square system in (where “hidden” implies that there is a selection on that yields ). The flow of the analysis is as follows. In Subsec. 4.2, we consider a convex relaxation of Program (5) and show that the set of feasible solutions of Program (5), for every , corresponds to a bounded polytope. By dimension considerations, we then show that the vertices of such polytope correspond to feasible solutions with at most nonzero entries. In Subsec. 4.3, we show that for irreducible systems, each vertex of such a polytope corresponds to a hidden weakly square system . That is, there exists a hidden weakly square system in that achieves . Note that a solution for such a hidden system can be extended to a solution for the original (see Obs. 3.4).

Next, in Subsec. 4.4, we exploit the generalization of Cramer’s rule for homogeneous linear systems (Cl. 2.2) as well as a separation theorem for nonnegative matrices to show that there is a hidden optimal square system in that achieves , which establishes the lion’s share of the theorem.

Arguably, the most surprising conclusion of our generalized theorem is that although the given system of matrices is not square, and eigenvalues cannot be straightforwardly defined for it, the nonsquare system contains a hidden optimal square system, optimal in the sense that a solution for this system can be translated into a solution to the original system (see Obs. 3.4) that satisfies Program (5) with the optimal value . The power of a nonsquare system is thus not in the ability to create a solution better than any of its hidden square systems, but rather in the option to select the best hidden square system out of the possibly exponentially many ones.

4.2 Existence of a solution with affectors

We now turn to characterize the feasible solutions of Program (5). The following is a convex variant of Program (5).

| maximize | (15) | |||

| (16) | ||||

| (17) | ||||

| (18) |

Note that Program (15) has the same set of constraints as those of Program (5). However, due to the fact that is no longer a variable, we get the following.

Claim 4.1

Program (15) is convex.

To characterize the set of feasible solutions , of Program (5), we fix some , and characterize the solution set of Program (15) with this . It is worth noting at this point that using the above convex relaxation, one may apply a binary search for finding a near-optimal solution for Program (15), up to any predefined accuracy. In contrast, our approach, which is based on exploiting the special geometric characteristics of the optimal solution, enjoys the theoretically pleasing (and mathematically interesting) advantage of leading to an efficient algorithm for computing the optimal solution precisely, and thus establishing the polynomiality of the problem.

Throughout, we restrict attention to values of . Let be the polyhedron corresponding to Program (15) and denote by the set of vertices of .

Claim 4.2

(a) is bounded (or a polytope). (b) For every , . This holds even for reducible systems.

Proof: Part (a) holds by the Equality constraint (18) which enforces . We now prove Part (b). Every vertex is defined by a set of linearly independent equalities. Recall that one equality is imposed by the constraint (Eq. (18)). Therefore it remains to assign linearly independent equalities out of the (possibly dependent) inequalities of Program (15). Hence even if all the (at most ) linearly independent SR constraints (16) become equalities, we are still left with at least unassigned equalities, which must be taken from the remaining nonnegativity constraints (17). Hence, at most nonnegativity inequalities were not fixed to zero, which establishes the proof.

4.3 Existence of a weak -solution

We now consider the case where the system is irreducible and a more delicate characterization of can be deduced.

We begin with some definitions. A solution is called a solution (for Program (5)) if it is a feasible solution , , in which for each only one affector has a non-zero assignment, i.e., for every . A solution is called a solution, or a “weak” solution, if it is a feasible vector , , in which for each , except at most one, say , , and . A solution is called a solution if it is an optimal solution. Let be an optimal solution.

For a feasible vector , we say that is active in iff . A subgraph of a constraint graph is active in iff every edge in can be associated with (or “explained by”) an active affector, namely,

Towards the end of this section, we prove the following lemma which holds for every feasible solution of Program (15).

Lemma 4.3

Let be an irreducible system with a feasible solution of Program (5). For every entity there exists an active affector , such that , or in other words, .

Let be a partial selection determining . Define the collection of constraint graphs agreeing with as

| (19) |

Note that by Obs. 3.6(b), every constraint graph for every partial selection is strongly connected. I.e., contains the constraint graphs for all square systems restricted to the partial selection dictated by for . Note that when , is a complete selection, i.e., , and contains a single graph corresponding to the square system .

Given a feasible vector and an irreducible system , the main challenge is to find an active (in ) irreducible spanning subgraph of . Finding such a subgraph is crucial for both Lemma 4.3 and Lemma 4.12 later on.

We begin by showing that given just one active affector in , it is possible to “bootstrap” it and construct an active irreducible spanning subgraph of (in ).

Let be an entity satisfying that . (Such entity must exist, since there are no redundant affectors). In what follows, we build an “influence tree” starting at and spanning the entire set of entities .

For a directed graph and vertex let be the breadth-first search tree of rooted at , obtained by placing vertex at level of the tree if the shortest directed path from to is of length . Given a constraint graph , let be the level of .

We now describe an iterative process for constructing a complete selection of supporters with positive entries in , i.e., such that and for every . At step , we start from the partial selection constructed in the previous step, and extend it to . The partial selection should satisfy the following four properties.

-

(A1) (i.e., it consists of strictly positive supporters).

Consider the graph family defined in Eq. (19), consisting of all constraint graphs for square systems induced by a selection that agrees with .

-

(A2) For every it holds that , i.e., from step ahead, the ’th first levels coincide.

-

(A3) , (i.e., level coincides as well).

Denote , , for (by (A2) and (A3) this is well-defined). Let , and for , be set of entities in the first levels of graphs.

-

(A4) is a partial selection determining the entities in , (i.e., and for every ).

Let us now describe the construction process of in more detail. At step , let . Note that in this case

It is easy to see that Properties (A1)-(A4) are satisfied. For , let . As and for every , Properties (A2) and (A3) holds. Property (A4) holds as well since determines .

Now assume that Properties (A1)-(A4) hold after step (for ), and consider step . We show how to construct given , and then show that it satisfies Properties (A1)-(A4). Note that by definition . Our goal is to find a partial selection determining such that

Once finding such a set , the partial selection is taken to be , where is the partial selection determining nodes in by Property (A4) for step . Note that since , the corresponding selections and agree.

We now show that such exists. This follows by the next claim.

Claim 4.4

For every , every entity has an active repressor in , i.e., .

Proof: We prove the claim by showing a slightly stronger statement, namely, that for every there exists an affector .

For ease of analysis, let’s focus on one specific . Since , it follows that there exists some such that . Since determines and , there exists a unique affector . In addition, by Property (A1) for step , . Therefore, since is an immediate outgoing neighbor of , it holds by Eq. (10) that , which establishes the claim.

We now complete the proof for the existence of . By Claim 4.4, each entity has a strictly positive repression, or, . Since is feasible, it follows by Fact 3.2 that also . Therefore we get that for every , there exists an affector . Consequently, set and let .

Observation 4.5

.

Proof: By definition, determines , for every . The selection consists of and a new selection for the new layer such that and therefore and agree on their common part.

We now turn to prove Properties (A1)-(A4) for step . Property (A1) follows immediately by the construction of . We next consider (A2).

Claim 4.6

.

Proof: Consider some . By Eq. (19), there exists a complete selection , where , such that . Recall that for every and for every and that and where . Therefore . By the inductive assumption, determines and by construction determines . Combining all the above, Obs. 4.5, . Obs. 3.8 implies that . Therefore, by Eq. (19) again, .

Due to Claim 4.6, and Properties (A2) and (A3) for step , Property (A2) follows for step . It is therefore possible to fix some and define for every (by (A2) for this is well-defined)

We consider now Property (A3) and show that for every .

For every graph , define as the set of all immediate outgoing neighbors of in , .

Observation 4.7

for every .

Proof: Let and , where correspond to complete legal selections. Since , it follows that . Since determines , every entity has the same unique supporter in both . By the definition of the constraint graph in Eq. (10), it then follows that for graph , the immediate outgoing neighbors of , are fully determined by the partial selection . The observation follows.

Hereafter, let , , be the set of immediate neighbors of in (by Obs. 4.7, this is well-defined). Finally, note that , for every . By Property (A2), for every and . Hence, and by Obs. 4.7, Property (A3) is established.

Finally, it remains to consider Property (A4). First, note that by Property (A2) and (A3) for step , we get that for every . By Property (A4) for step and Properties (A2) and (A3) for step , it follows that the selection determines .

We now turn to discuss the stopping criterion. Let be the first time step where . (Since for every , such exists). We then have the following.

Lemma 4.8

hence is a square system, and ,

Proof: Recall that for every , by Eq. (19), represents a square system, and therefore by Obs. 3.6 it is strongly connected. Fix some arbitrary and let for every (By Property (A2) and (A3) this is well defined). By Property (A4) it holds that the partial selection (resp., ) determines (resp., ). As , we have that . Hence, . This implies that the BFS graph consists of levels . In addition, since is strongly connected it follows that . By Property (A4), determines , hence meaning that is a complete selection, so corresponds to a unique square system. Finally, since the layers of every are the same (Property (A2) and (A3)) and span all the entities it follows that consists of a single constraint graph, the lemma follows.

In summary, we end with a complete selection that spans the entities. Every affector is active and therefore the constraint graph is active in . This establishes the following lemma.

Lemma 4.9

For every feasible point for Program (15) and every active affector in , there exists a complete selection for such that , hence the corresponding constraint subgraph is active in .

The following is an interesting implication.

Corollary 4.10

For every feasible vector there exists an active spanning irreducible graph.

Proof: Since every feasible vector is non-negative, there exists at least one active affector in it, from which an active spanning irreducible graph can be constructed by Lemma 4.9.

Finally, we are ready to complete the proof of Lemma 4.3 for any irreducible system .

Proof: [Lemma 4.3] Since , it follows that there exists at least one affector such that . By Lemma 4.9, there is a complete selection vector . The lemma follows.

We end this subsection by showing that every vertex is a solution.

Lemma 4.11

If the system of Program (15) is irreducible, then every is a solution for it, and in particular every optimal solution is a solution.

4.4 Existence of a solution

In the previous section we established the fact that when is irreducible, every vertex corresponds to an solution for Program (15). In particular, this statement holds for , the optimal for . By the feasibility of the system for , the corresponding polytope is non-empty and bounded (and each of its vertices is a solution), hence there exist solutions for the problem. The goal of this subsection is to establish the existence of a solution for the problem and thus complete the proof of Thm. 3.9. In particular, we consider Program (15) for an irreducible system and , i.e., the optimal value of Program (5) for , and show that every optimal solution is in fact a solution.

We begin by showing that for , the set of SR Inequalities (Eq. (16)) hold with equality for every optimal solution , including one that is not a solution.

Lemma 4.12

If is irreducible, then for every optimal solution of Program (15).

Proof: Consider an irreducible system . By Lemma 4.3, every entity has at least one active supporter in . Select, for every , one such supporter . Let . By definition, . Also, by Claim 3.5 the sets are disjoint. Therefore is a complete selection (i.e, for every , ), and hence is a square irreducible system. Let be the constraint graph of . By Obs. 3.6(a), is strongly connected. In addition, since has exactly one affector for every , and this affector is active, it follows that every edge corresponds to an active affector in , i.e., , and hence is active.

Therefore, for an edge in , if we reduce the power of the active supporter of which, by the definition of (see Eq. (10)) is a repressor of , then inequality can be made strict. Such reduction makes sense only because we consider active affectors. This intuition is next used in order to prove the lemma. For a feasible solution of Program (15) and vaule , let us formulate the SR constraints in terms of total support and total repression as in (Eq. (8)) , and let

| (20) |

be the residual amount of the SR constraint of (8)(hence implies strict inequality on the th constraint with ). Then the lemma claims that for the optimal solution and , for every .

Assume, toward contradiction, that there exists at least one entity, w.l.o.g. , for which . In what follows, we gradually construct a new assignment that achieves a strictly positive residue , or, a strict inequality in the SR constraint of Eq. (8), for all . Clearly, if all SR constraints are satisfied with strict inequality, then there exists some larger that still satisfies all the constraints, in contradiction to the optimality of .

To construct , we trace paths of influence in the strongly connected (and active) constraint graph . Think of as the root, and let be the level of (with ). Let , and for . Let be the partial selection determining the entities in . I.e., and for every , .

The process of constructing consists of steps, where is the depth of . At step , we are given and use it to construct . Essentially, should satisfy the following properties.

-

(B1) The set of SR inequalities corresponding to entities hold with strict inequality with . That is, for every , , i.e.,

-

(B2) is an optimal solution, i.e., it satisfies Program (5) with .

-

(B3) for every and for every .

Let us now describe the construction process in more detail. Let . Consider step and recall that . Let be the active supporter of , i.e., . Then it is possible to slightly reduce the value of in while still maintaining feasibility, yielding . Formally, let and leave the rest of the entries unchanged, i.e., for every other . We now show that Properties (B1)-(B3) are satisfied for and then proceed to consider the construction of for . Since , and , also , so (B1) holds vacuously, and (B2) and (B3) follow by the fact that . Next, consider . By the irreducibility of the system (in particular, see Cl. 3.5), since only was reduced in (compared to ), only the constraint of could have been damaged (i.e., become unsatisfied). Yet, it is easy to verify that the constraint of still holds with strict inequality for , so Property (B2) holds. As , Property (B1) needs to be verified only for , and indeed the new value of ensures , so (B1) is satisfied. Finally, , and Property (B3) checks out as well.

Next, we describe the general construction step. Assume that we are given solution satisfying Properties (B1)-(B3) for each . We now describe the construction of and then show that it satisfies the desired properties. We begin by showing that the set of SR inequalities of Eq. (8) on the entities in hold with strict inequality with .

Claim 4.13

, or, , for every entity .

Proof: Consider some . By definition of , there exists an entity such that . Since and is a partial selection determining , a (unique) supporter is guaranteed to exist. By the definition of , implies that . Finally, note that by Property (B3), and for every (since ). I.e.,

| (21) |

which implies by Eq. (8) that

| (22) |

By the optimality of (Property (B2) for step ), we have that . Combining this with Eq. (22), , which establishes the claim for . The same argument can be applied for every , thus the claim is established.

Let be the partial selection that determines . In the solution , only the entries of have been reduced and the other entries remain as in . Recall that by construction, and therefore also . By Claim 4.13, the constraints of nodes hold with strict inequality, and therefore it is possible to slightly reduce the value of their positive supporters while still maintaining the strict inequality (although with a lower residue). Formally, for every , consider its unique supporter in , . By Claim 4.13, . Set . In addition, for every other supporter .

It remains to show that satisfies the Properties (B1)-(B3). (B1) follows by construction. To see (B2), note that since for every , only the constraints of nodes might have been violated by the new solution . Formally, and for every . Although, for , we get that (yet ), this reduction in the total support of nodes was performed in a controlled manner, guaranteeing that the corresponding inequalities hold with strict inequality. Finally, (B3) follows immediately. After steps, by Property (B1) all inequalities hold with strict inequality (as ) with the solution . Thus, it is possible to find some that would contradict the optimally of . Formally, let . Since , we get that is feasible with , contradicting the optimally of . Lemma 4.12 follows.

We proceed by considering a vertex of . By Lemma 4.11, is a solution. To complete the proof of Thm. 3.9, we have to prove that it is a solution. To do that, we first transform into a weakly square system . First, if , then the system is already weak. Otherwise, without loss of generality, let the entry in correspond to where for and the and entries correspond to and respectively such that . It then follows that for every and for every . Let . Let where for every and every , and define analogously. From now on, we restrict attention to the weakly square system where . Note that this system results from by discarding the corresponding entries of . Therefore, . Let correspond to the upper left submatrix of . Let be obtained from by removing the column. Finally, is obtained from by removing the column. The matrices are defined analogously.

To study the weakly square system , we consider the following three square systems:

| (23) | |||||

Note that a feasible solution for the system , for , corresponds to a feasible solution for by setting for every and . For ease of notation, let , and , where is the characteristic polynomial defined in Eq. (3). Let be the optimal value of Program (5) for the system . Let and let

Claim 4.14

.

Proof: The left inequality follows as any optimal solution for (respectively, ) can be achieved in the weakly square system by setting (resp., ).

Assume towards contradiction that and let be the optimal solution for .

By Lemma 4.3, it holds that . Without loss of generality, assume that . By Obs. 3.6(a) and the irreducibility of , is strongly connected to the rest of the graph for every selection of one of its two supporters. Thus there exists at least one entity , such that .

Let be obtained by taking the values of the first affectors as in and discarding the values of and . We have the following.

| (24) |

where strict inequality follows by the assumption that and is a repressor of . Since is an optimal solution for the system , by Lemma 4.12, it holds that . Combining with Eq. (24), we get that . Since is an optimal solution for , we end with contradiction to Lemma 4.12, concluding that . The claim follows.

Our goal in this section is to show that the optimal value for can be achieved by setting either or , essentially showing that the optimal solution corresponds to a solution. This is formalized in the following lemma.

Lemma 4.15

.

The following observation holds for every and follows immediately by the definitions of feasibility and irreducibility and the PF Theorem 2.4.

Observation 4.16

-

(1) is the maximal eigenvalue of .

-

(2) For an irreducible system , .

-

(3) If the system is feasible then .

For a square system , let be a modified form of the matrix , defined as follows.

More explicitly,

Clearly, cannot be defined for a nonsquare system . Instead, a generalization of for any (nonsquare) system is given by

or explicitly,

Note that if is a feasible solution for , then . If , it also holds that .

For , where both and are well-defined, the following connection becomes useful in our later argument. Recall that is the characteristic polynomial of (see Eq. (3)).

Observation 4.17

For a square system ,

(a) and

(b) .

Proof: The observation follows immediately by noting that for every and , and by Eq. (3).

The next equality plays a key role in our analysis.

Lemma 4.18

Proof: By Lemma 4.12, it follows that , or

Next, we need to apply Claim 2.2(b). To do that, we first need to verify that , i.e., the upper left submatrix of , is nonsingular. This follows by noting that and by Claim 4.14, . Moreover, note that is the largest real root of , hence

| (25) |

Combining with Obs. 4.17(b), it follows that or that is nonsingular.

Now we can safely apply Claim 2.2(b), yielding

By plugging Obs. 4.17(b) and simplifying, the lemma follows.

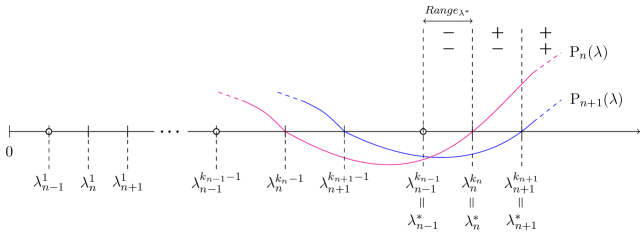

Our work plan from this point on is as follows. We first define a range of ‘candidate’ values for . Essentially, our interest is in real positive . Recall that and are nonnegative irreducible square matrices and therefore Theorem 2.4 can be applied throughout the analysis. Without loss of generality, assume that (and thus ) and let . Let the corresponding range of be

| (26) |

To complete the proof for Lemma 4.15 we assume, towards contradiction, that . According to Claim 4.14 and the fact that , it then follows that , and hence .

In addition, . Note that since , also , namely, the corresponding is real and positive as well. This is important mainly in the context of nonnegative irreducible matrices for . In contrast to nonnegative primitive matrices (where ) for irreducible matrices, such as , by Thm. 2.4 there are eigenvalues, , for which . However, note that only one of these, namely, , might belong to . (This follows as by Thm. 2.4, every other such is either real but negative or with a nonzero complex component).

Fix and let be the number of real and positive

eigenvalues of . Let

be the ordered set of real and positive eigenvalues for

, i.e., real positive roots of .

Note that .

By Theorem 2.4, we have that for every

(a) , and

(b) , .

We proceed by showing that the potential range for , namely, , can contain no root of and . Since is real and positive, it is sufficient to consider only real and positive roots of and (or real and positive eigenvalues of and ).

Claim 4.19

for every real , for .

Proof: Note that is the principal minor of both and . By the separation theorem of Hall and Porsching, see Lemma. 2.3, we get that for every and , concluding by Eq. (26) that .

We proceed by showing that and have the same sign in . See Fig. 2 for a schematic description of the system.

Claim 4.20

for every .

Proof: Fix . By Claim 4.19, has no roots in , so for every . Also note that by Thm. 2.4, , for every . We now make two crucial observations. First, as and correspond to a characteristic polynomial of an matrix, they have the same leading coefficient (any characteristic polynomial is monic, i.e., with leading coefficient 1 and degree ) and therefore for (recall that we assume that ). Second, due to the PF Theorem, the maximal roots of and are of multiplicity one and therefore the polynomial (resp., ) necessarily changes its sign when passes through its maximal real positive root (respectively, ). Using these two observations, we now prove the claim via contradiction. Assume, toward contradiction, that for some . Then for and also for and . (This holds since when encountering a root of multiplicity one, the sign necessarily flips). In particular, this implies that for every , in contradiction to the fact that for every . The claim follows.

We now complete the proof of Lemma 4.15.

Proof: By Eqs. (25) and (26), for every . We can safely apply Claim 4.20 to Lemma 4.18 and and get that . Since and are nonnegative, it follows that and . In contradiction to Lemma 4.3. We conclude that .

We complete the geometric characterization of the generalized PF Theorem by noting the following.

Lemma 4.21

Every vertex is a solution.

Proof: By Lemma 4.11, it is sufficient to show that there exists no that is weak, namely, which is a solution but not a solution. Assume, towards contradiction, that and that both and . From now on, we replace by its truncated sub-vector in , i.e., we discard the zero entries in .

Let and be defined as in Eq. (23). Recalling the notation of Sec. 2 where for matrix , we denote by the matrix that results from by removing the -th row and the -th column, define

and

for . By Eq. (3), Claim 2.2(a) and the proof of Lemma 4.18, every optimal solution, and in particular every , satisfies

| (27) |

for . This implies that our weak solution is given by

Let

and