The Gaussian Radon Transform and Machine Learning

Abstract.

There has been growing recent interest in probabilistic interpretations of kernel-based methods as well as learning in Banach spaces. The absence of a useful Lebesgue measure on an infinite-dimensional reproducing kernel Hilbert space is a serious obstacle for such stochastic models. We propose an estimation model for the ridge regression problem within the framework of abstract Wiener spaces and show how the support vector machine solution to such problems can be interpreted in terms of the Gaussian Radon transform.

Key words and phrases:

Gaussian Radon Transform, Ridge Regression, Kernel Methods, Abstract Wiener Space, Gaussian Process2010 Mathematics Subject Classification:

Primary 44A12, Secondary 28C20, 62J071. Introduction

A central task in machine learning is the prediction of unknown values based on ‘learning’ from a given set of outcomes. More precisely, suppose is a non-empty set, the input space, and

| (1.1) |

is a finite collection of input values together with their corresponding real outputs . The goal is to predict the value corresponding to a yet unobserved input value . The fundamental assumption of kernel-based methods such as support vector machines (SVM) is that the predicted value is given by , where the decision or prediction function belongs to a reproducing kernel Hilbert space (RKHS) over , corresponding to a positive definite function (see Section 2.1.1). In particular, in ridge regression, the predictor function is the solution to the minimization problem:

| (1.2) |

where is a regularization parameter and denotes the norm of in . The regularization term penalizes functions that ‘overfit’ the training data.

The minimization problem (1.2) has a unique solution, given by a linear combination of the functions . Specifically:

| (1.3) |

where is given by:

| (1.4) |

where is the matrix with entries , is the identity matrix of size and is the vector of outputs. We present a geometrical proof of this classic result in Theorem A.1.

Recently there has been a surge in interest in probabilistic interpretations of kernel-based learning methods; see for instance [Sollich, Muk, Aravkin, Ozertem, Zhang, Huszar]. As we shall see below, there is a Bayesian interpretation and a stochastic process approach to the ridge regression problem when the RKHS is finite-dimensional, but many RKHSs used in practice are infinite-dimensional. The absence of Lebesgue measure on infinite-dimensional Hilbert spaces poses a roadblock to such interpretations in this case. In this paper:

-

•

We show that there is a valid stochastic interpretation to the ridge regression problem in the infinite-dimensional case, by working within the framework of abstract Wiener spaces and Gaussian measures instead of working with the Hilbert space alone. Specifically, we show that the ridge regression solution may be obtained in terms of a conditional expectation and the Gaussian Radon transform.

-

•

We show that, within the more traditional spline setting, the element of of minimal norm that satisfies for can also be expressed in terms of the Gaussian Radon transform.

-

•

We propose a way to use the Gaussian Radon transform for a broader class of prediction problems. Specifically, this method could potentially be used to not only predict a particular output of a future input , but to predict a function of future outputs; for instance, one could be interested in predicting the maximum or minimum value over an interval of future outputs.

-

•

In this work we start with a RKHS and complete it with respect to a measurable norm to obtain a Banach space . However, the space does not necessarily consist of functions. In light of recent interest in reproducing kernel Banach spaces, which do consist of functions, we propose a method to realize as a space of functions.

1.1. Probabilistic Interpretations to the Ridge Regression Problem in Finite Dimensions

Let us first consider a Bayesian perspective: suppose that our parameter space is an RKHS with reproducing kernel . If is finite-dimensional, we take standard Gaussian measure on as our prior distribution:

where is the dimension of . Let denote, for every , the continuous linear functional on . With respect to standard Gaussian measure, every is normally distributed with mean and variance , and Cov. Now recall that contains the functions on , and for all , . Then is a centered Gaussian process on with covariance function : for all . If we are given the training data and we assume the measurement contains some error we would like to model as Gaussian noise, we choose an orthonormal set such that for every . Then

are independent centered Gaussian processes on , and for every we model our data as arising from the event:

where is a fixed parameter. Then for every , are independent Gaussian random variables on with mean and variance for every , which gives rise to the statistical model of probability distributions on :

for every . Replacing with the vector of observed values, the posterior distribution resulting from this is proportional to:

Therefore finding the maximum a posteriori (MAP) estimator in this situation amounts exactly to finding the solution to the ridge regression problem in (1.2).

Clearly, this Bayesian approach depends on being finite-dimensional; however, reproducing kernel Hilbert spaces used in practice are often infinite-dimensional (such as those arising from Gaussian RBF kernels). The ridge regression SVM previously discussed goes through regardless of the dimensionality of the RKHS, and there is still a need for a valid stochastic interpretation of the infinite-dimensional case. We now explore another stochastic approach to ridge regression, which is equivalent to the Bayesian one, but which can be carried over in a sense to the infinite-dimensional case, as we shall see later. Suppose again that is a finite-dimensional RKHS over , with reproducing kernel , and equipped with standard Gaussian measure. Recall that is then a centered Gaussian process on with covariance function . If we assume that the data arises from some unknown function in , then the relationship suggests that the random variable is a good model for the outputs. Moreover, the training data provides some previous knowledge of the random variables , which we can use to refine our estimation of by taking conditional expectations. In other words, our first guess would be to estimate the output of a future input by:

| (1.5) |

But if we want to include some possible noise in the measurements, we would like to have a centered Gaussian process on , with covariance function Cov for some parameter , which is also independent of .

Let us fix , a ‘future’ input whose output we would like to predict. To take measurement error into account, we choose again an orthonormal set such that:

and , and set:

Then we estimate the output as the conditional expectation:

As shown in Lemma B.1 below:

where is:

with:

for all , with being the matrix with entries given by . Moreover:

Note that this last relationship is why we required that also be orthogonal to . This yields:

showing that the prediction is precisely the ridge regression solution in (1.3).

Our goal in this paper is to show that the Gaussian process approach does go through in infinite-dimensions and, moreover, that it remains equivalent to the SVM solution. Since the SVM solution in (1.3) is contained in a finite-dimensional subspace, the possibly infinite dimensionality of is less of a problem in this setting. However, if we want to predict based on a stochastic model for and is infinite-dimensional, the absence of Lebesgue measure becomes a significant problem. In particular, we cannot have the desired Gaussian process on itself. The approach we propose is to work within the framework of abstract Wiener spaces, introduced by L. Gross in the celebrated work [Gr]. The concept of abstract Wiener space was born exactly from this need for a “standard Gaussian measure” in infinite dimensions and has become a standard framework in infinite-dimensional analysis. We outline the basics of this theory in Section 2.1.2 and showcase the essentials of the classical Wiener space, as the “original” special case of an abstract Wiener space, in Section 2.1.4.

We construct a Gaussian measure with the desired properties on a larger Banach space that contains as a dense subspace; the geometry of this measure is dictated by the inner-product on . This construction is presented in Section 2.1.3. We then show in Section 3 how the ridge regression learning problem outlined above can be understood in terms of the Gaussian Radon transform. The Gaussian Radon transform associates to a function on the function , defined on the set of closed affine subspaces of , whose value on a closed affine subspace is the integral , where is a Gaussian measure on the closure of in obtained from the given Gaussian measure on . This is explained in more detail in Section 2.2. For more on the Gaussian Radon transform we refer to the works [BecGR2010, BecSen2012, Hol2013, HolSen2012, MS].

Another area that has recently seen strong activity is learning in Banach spaces; see for instance [Xu, learning, Der]. Of particular interest are reproducing kernel Banach spaces, introduced in [Xu], which are special Banach spaces whose elements are functions. The Banach space we use in Section 3 is a completion of a reproducing kernel Hilbert space, but does not directly consist of functions. A notable exception is the classical Wiener space, where the Banach space is . In Section 4 we address this issue and propose a realization of as a space of functions.

Finally, in Appendix A we present a geometric view. First we present a geometric proof of the representer theorem for the SVM minimization problem and then describe the relationship with the Gaussian Radon transform in geometric terms.

2. Background

2.1. Realizing covariance structures with Banach spaces

In this section we construct a Gaussian measure on a Banach space along with random variables defined on this space for which the covariance structure is specified in advance. In more detail, suppose is a non-empty set and

| (2.1) |

a function that is symmetric and positive definite (in the sense that the matrix is symmetric and positive definite); we will construct a measure on a certain Banach space along with a family of Gaussian random variables , with running over , such that

| (2.2) |

for all . A well-known choice for , for , is given by

where is a scale parameter.

The strategy is as follows: first we construct a Hilbert space along with elements , for each , for which for all . Next we describe how to obtain a Banach space , equipped with a Gaussian measure, along with random variables that have the required covariance structure (2.2). The first step is a standard result for reproducing kernel Hilbert spaces.

2.1.1. Constructing a Hilbert space from a covariance structure

For this we simply quote the well-known Moore-Aronszajn theorem (see, for example, Chapter 4 of Steinwart [Ingo]).

Theorem 2.1.

Let be a non-empty set and a function for which the matrix is symmetric and positive definite:

-

(i)

for all , and

-

(ii)

holds for all integers , all points , and all .

Then there is a unique Hilbert space consisting of real-valued functions defined on the set , containing the functions for all , with the inner product on being such that

| (2.3) |

Moreover, the linear span of is dense in .

The Hilbert space is called the reproducing kernel Hilbert space (RKHS) over with reproducing kernel .

For the mapping

| (2.4) |

known as the canonical feature map, we have

| (2.5) |

for all . Hence if is a topological space and is continuous then so is the function given in (2.5), and the value of this being when , it follows that is continuous. In particular, if has a countable dense subset then so does the image , and since this spans a dense subspace of it follows that is separable.

2.1.2. Gaussian measures on Banach spaces

The theory of abstract Wiener spaces developed by Gross [Gr] provides the machinery for constructing a Gaussian measure on a Banach space obtained by completing a given Hilbert space using a special type of norm called a measurable norm. Conversely, according to a fundamental result of Gross, every centered non-degenerate Gaussian measure on a real separable Banach space arises in this way from completing an underlying Hilbert space called the Cameron-Martin space. We work here with real Hilbert spaces as a complex structure plays no role in the Gaussian measure in this context.

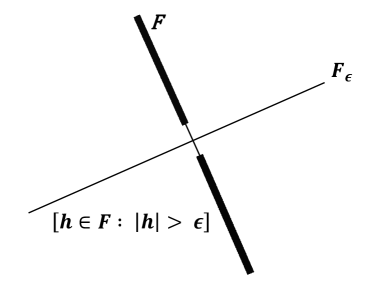

Definition 2.1.

A norm on a real separable Hilbert space is said to be a measurable norm provided that for any , there is a finite-dimensional subspace of such that:

| (2.6) |

for every finite-dimensional subspace of with , where denotes standard Gaussian measure on . Figure 1(a) illustrates this notion.

We denote the norm on arising from the inner-product by , which is not to be confused with a measurable norm . Here are three facts about measurable norms (for proofs see Gross [Gr], Kuo [Ku1] or Eldredge [Nate]):

-

(1)

A measurable norm is always weaker than the original norm: there is such that:

(2.7) for all .

-

(2)

If is infinite-dimensional, the original Hilbert norm is not a measurable norm.

-

(3)

If is an injective Hilbert-Schmidt operator on then

(2.8) specifies a measurable norm on .

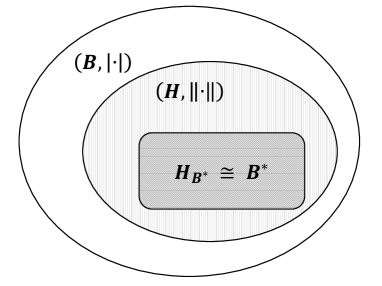

Henceforth we denote by the Banach space obtained by completion of with respect to .

Any element gives a linear functional

that is continuous with respect to the norm . Let

be the subspace of consisting of all for which is continuous with respect to the norm . Figure 1(b) illustrates the relationships between , , and .

By fact (1) above, any linear functional on that is continuous with respect to is also continuous with respect to and hence is of the form for a unique by the traditional Riesz theorem. Thus consists precisely of those for which the linear functional is the restriction to of a (unique) continuous linear functional on the Banach space . We denote this extension of to an element of by :

| the continuous linear functional on | (2.9) | ||||

for all . Moreover, consists exactly of the elements with : for any the restriction is in (because of the relation (2.7)) and hence for a unique .

The fundamental result of Gross [Gr] is that there is a unique Borel measure on such that for every the linear functional , viewed as a random variable on , is Gaussian with mean and variance ; thus:

| (2.10) |

for all . The mapping

is a linear isometry.

A triple where is a real separable Hilbert space, is the Banach space obtained by completing with respect to a measurable norm, and is the Gaussian measure in (2.10), is called an abstract Wiener space. The measure is known as Wiener measure on .

Suppose is orthogonal to ; then for any we have

where is the element of for which . Since for all it follows that . Thus,

| is dense in . | (2.11) |

Consequently extends uniquely to a linear isometry of into . We denote this extension again by :

| (2.12) |

It follows by taking -limits that the random variable is again Gaussian, satisfying (2.10), for every .

It will be important for our purposes to emphasize again that if is such that the linear functional on is continuous with respect to the norm then the random variable is the unique continuous linear functional on that agrees with on . If is not continuous on with respect to the norm then is obtained by -approximating with elements of .

Conversely, one can show that any real separable Banach space equipped with a centered, non-degenerate Gaussian measure , can be placed in the context of an abstract Wiener space. The corresponding Hilbert space is the Cameron-Martin space of , the subspace given by:

where for every :

The norm defined above is a complete inner-product norm on , it is stronger than the Banach norm on , and is dense in . Moreover, the norm , restricted to , is a measurable norm - for an interesting proof of this fact, due to Stroock, see section VIII of Driver’s notes [DriverNotes]. So is an abstract Wiener space and is uniquely determined by and .

2.1.3. Construction of the random variables

As before, we assume given a model covariance structure

We have seen how this gives rise to a Hilbert space , which is the closed linear span of the functions , with running over . Now let be any measurable norm on , and let be the Banach space obtained by completion of with respect to . Let be the centered Gaussian measure on as discussed above in the context of (2.10). We set

| (2.13) |

for all ; thus . As a random variable on the function is Gaussian, with mean and variance , and the covariance structure is given by:

| (2.14) |

Thus we have produced Gaussian random variables , for each , on a Banach space, with a given covariance structure.

2.1.4. Classical Wiener space

Let us look at the case of the classical Wiener space, as an example of the preceding structures. We take for some positive real , and

| (2.15) |

for all , where the superscript refers to Brownian motion. Then is for and is constant at when . It follows then that , the linear span of the functions for , is the set of all functions on with initial value and graph consisting of linear segments; in other words, consists of all functions on whose derivative exists and is locally constant outside a finite set of points. The inner product on is determined by observing that

| (2.16) |

we can verify that this coincides with

| (2.17) |

for all . Consequently, is the Hilbert space consisting of functions on that can be expressed as

| (2.18) |

for some ; equivalently, consists of all absolutely continuous functions on , with , for which the derivative exists almost everywhere and is in . The sup norm is a measurable norm on (see Gross [Gr, Example 2] or Kuo [Ku1]). The completion is then , the space of all continuous functions starting at . If then is Gaussian of mean and variance , relative to the Gaussian measure on . We can check readily that is Gaussian of mean and variance for all . The process yields standard Brownian motion, after a continuous version is chosen.

2.2. The Gaussian Radon Transform

The classical Radon transform of a function associates to each hyperplane the integral of over ; this is useful in scanning technologies and image reconstruction. The Gaussian Radon transform generalizes this to infinite dimensions and works with Gaussian measures (instead of Lebesgue measure, for which there is no useful infinite dimensional analog); the motivation for studying this transform comes from the task of reconstructing a random variable from its conditional expectations. We have developed this transform in the setting of abstract Wiener spaces in our work [HolSen2012] (earlier works, in other frameworks, include [MS, BecSen2012, BecGR2010]).

Let be a real separable Hilbert space, and the Banach space obtained by completing with respect to a measurable norm . Let be a closed subspace of . Then

| (2.19) |

is a closed affine subspace of , for any point . In [HolSen2012, Theorem 2.1] we have constructed a probability measure on uniquely specified by its Fourier transform

| (2.20) |

where denotes orthogonal projection on in . For our present purposes we formulate the description of the measure in slightly different terms. For every closed affine subspace there is a Borel probability measure on and there is a linear mapping

such that for every , the random variable satisfies

| (2.21) |

where is the point on closest to the origin in , and is the orthogonal projection operator onto the closed subspace . Moreover, is concentrated on the closure of in :

where denotes the closure in of the affine subspace . (Note that the mapping depends on the subspace . For more details about , see Corollary 3.1.1 and observation (v) following Theorem 2.1 in [Hol2013].)

From the condition (2.21), holding for all , we see that is Gaussian with mean and variance .

The Gaussian Radon transform for a Borel function on is a function defined on the set of all closed affine subspaces in by:

| (2.22) |

(Of course, is defined if the integral is finite for all such .)

The value corresponds to the conditional expectation of , the conditioning being given by the closed affine subspace . For a precise formulation of this and proof for being of finite codimension see the disintegration formula given in [Hol2013, Theorem 3.1]. The following is an immediate consequence of [Hol2013, Corollary 3.2] and will play a role in Section 3:

Proposition 2.1.

Let be an abstract Wiener space and linearly independent elements of . Let be a Borel function on , square-integrable with respect to , and let

Then is a version of the conditional expectation

3. Machine Learning using the Gaussian Radon Transform

Consider again the learning problem outlined in the introduction: suppose is a separable topological space and is the RKHS over with reproducing kernel . Let:

| (3.1) |

be our training data and suppose we want to predict the value at a future value . Note that is a real separable Hilbert space so, as outlined in Section 2.1.2, we may complete with respect to a measurable norm to obtain the Banach space and Gaussian measure . Moreover, recall from Section 2.1.3 that we constructed for every the random variable

| (3.2) |

where is the isometry in (2.12), and

| (3.3) |

for all . Therefore is a centered Gaussian process with covariance .

Since for every the value is given by , we work with as our desired random-variable prediction. The first guess would therefore be to use:

| (3.4) |

as our prediction of the output corresponding to the input .

Using Lemma B.1 the prediction in (3.4) becomes:

where and is, as in the introduction, the matrix with entries . As we shall see in Theorem A.2, the function is the element of minimal norm such that for all . Therefore (3.4) is the solution in the traditional spline setting, and does not take into account the regularization parameter . Combining this with Proposition 2.1, we have:

Theorem 3.1.

Let be an abstract Wiener space, where be the real RKHS over a separable topological space with reproducing kernel . Given:

such that are linearly independent, the element of minimal norm that satisfies for all is given by:

| (3.5) |

where is the Gaussian Radon transform of for every .

The next theorem shows that the ridge regression solution can also be obtained in terms of the Gaussian Radon transform, by taking the Gaussian process approach outlined in the introduction.

Theorem 3.2.

Let be the RKHS over a separable topological space with real-valued reproducing kernel and be the completion of with respect to a measurable norm with Wiener measure . Let

| (3.6) |

be fixed and . Let be an orthonormal set such that:

| (3.7) |

and for every let where is the isometry in (2.12). Then for any :

| (3.8) |

where is the solution to the ridge regression problem in (1.2) with regularization parameter . Consequently:

| (3.9) |

where is the Gaussian Radon transform of .

Note that a completely precise statement of the relation (3.8) is as follows. Let us for the moment write the quantity , involving the vector , as

Then

| (3.10) |

is a version of the conditional expectation

| (3.11) |

Proof.

The interpretation of the predicted value in terms of the Gaussian Radon transform allows for quite a broad class of functions that can be considered for prediction. As a simple example, consider the task of predicting the maximum value of an unknown function over a future period using knowledge from the training data. The predicted value would be

| (3.12) |

where is the closed affine subspace of the RKHS reflecting the training data, and is, for example, a function of the form

| (3.13) |

for some given set of ‘future dates’. We note that the prediction (3.12) is, in general, different from

where is the SVM prediction as in (3.9); in other words, the prediction (3.12) is not the same as simply taking the supremum over the predictions given by the SVM minimizer. We note also that in this type of problem the Hilbert space, being a function space, is necessarily infinite-dimensional.

3.1. An approach using direct sums of abstract Wiener spaces

One disadvantage of Theorem 3.2 is that the choice of could change with every training set and every future input - specifically, given the training data (3.6), one must choose an orthonormal set that is not only orthogonal to each , but also to , for every future input whose outcome we would like to predict. Clearly a set that would “universally” work cannot be found in , because span is dense in . We would therefore like to attach to another copy of which would function as a “repository” of errors - so the two spaces would need to be in a sense orthogonal to each other. This is precisely the idea behind direct sums of Hilbert spaces: if and are Hilbert spaces, their orthogonal direct sum:

is a Hilbert space with inner-product:

for all and .

Proposition 3.1.

Let and be abstract Wiener spaces, where and are real separable infinite-dimensional Hillbert spaces and , are the Banach spaces obtained by completing , with respect to measurable norms , , respectively. Then:

is an abstract Wiener space, where is a separable Banach space with the norm , for all , .

It then easily follows that if is the isometry described in (2.12), then:

where is the corresponding isometry for .

Going back to the ridge regression problem, let now be an abstract Wiener space, where is the RKHS over a separable topological space with reproducing kernel and be our training data. Recall that we would like an “orthogonal repository” for the errors - so let be an abstract Wiener space, where is a real separable infinite-dimensional Hilbert space. For every let and:

where is the isometry in (2.12). As previously noted:

where .

Let and be an orthonormal basis for and for every positive integer let:

where . Then:

for all and . Then by Lemma B.1 and Proposition 2.1, for any :

where is the ridge regression solution and both the conditional expectation and the Gaussian Radon transform above are with respect to . In this approach, for any number of training points and any future input we may simply work with , and we no longer have to choose this orthonormal set for every training set and every new input.

We return to the proof of Proposition 3.1.

Proof.

Every continuous linear functional on is of the form for some and , where:

Since and are weaker than and on and , respectively, there is such that for all and all . Then:

which shows that is a weaker norm than on . Consequently, to every we may associate a unique such that for all , . As can be easily seen, this element is exactly , where for .

The characteristic functional of the measure on is then:

for all . Therefore is a centered non-degenerate Gaussian measure with covariance operator:

for all , . Define for :

| (3.14) |

and the Cameron-Martin space of :

| (3.15) |

For every and ,

so:

which shows that .

Conversely, suppose . Then by letting :

so is in the Cameron-Martin space of - which is just . Similarly, , proving that as sets. To see that the norms also correspond, note that for any and , not both :

So:

| (3.16) |

Since is dense in both and , (3.16) proves that for all , so and are the same as Hilbert spaces. Thus is the Cameron-Martin space of , which concludes our proof. ∎

4. Realizing as a space of functions

In this section we present some results of a somewhat technical nature to address the question as to whether the elements of the Banach space can be viewed as functions.

4.1. Continuity of

A general measurable norm on does not ‘know’ about the kernel function and hence there seems to be no reason why the functionals on would be continuous with respect to the norm . To remedy this situation we prove that there exist measurable norms on relative to which the functionals are continuous for running along a dense sequence of points in :

Proposition 4.1.

Let be the reproducing kernel Hilbert space associated to a continuous kernel function , where is a separable topological space. Let be a countable dense subset of . Then there is a measurable norm on with respect to which is a continuous linear functional for every .

Proof. As noted in the context of (2.5), the feature map is continuous. So if then the map is continuous and so if is a point for which then there is a neighborhood of such that for all . Since is dense in we conclude that there is a point for which . Turning this argument into its contrapositive, we see that a vector orthogonal to for every is orthogonal to for all and hence is because the span of is dense in . Thus spans a dense subspace of , where . By the Gram-Schmidt process we obtain an orthonormal basis of such that is contained in the span of , for every . Now consider the bounded linear operator specified by requiring that for all ; this is Hilbert-Schmidt because and is clearly injective. Hence, by Property (3) discussed in the context of (2.8),

| (4.1) |

specifies a measurable norm on . Then

from which we see that the linear functional on is continuous with respect to the norm . Hence, by definition of the linear isometry given in (2.9), is the element in that agrees with on . In particular each is continuous and hence is a continuous linear functional on for every . QED

The measurable norm we have constructed in the preceding proof arises from a (new) inner-product on . However, given any other measurable norm on the sum

is also a measurable norm (not necessarily arising from an inner-product) and the linear functional is continuous with respect to the norm for every .

4.2. Elements of as functions

If a Banach space is obtained by completing a Hilbert space of functions, the elements of need not consist of functions. However, when is a reproducing kernel Hilbert space as we have been discussing and under reasonable conditions on the reproducing kernel function it is true that elements of can ‘almost’ be thought of as functions on . For this we first develop a lemma:

Lemma 4.1.

Suppose is a separable real Hilbert space and the Banach space obtained by completing with respect to a measurable norm . Let be a closed subspace of that is transverse to in the sense that , and let

| (4.2) |

be the quotient Banach space, with the standard quotient norm, given by

| (4.3) |

Then the mapping

| (4.4) |

where is the inclusion, is a continuous linear injective map, and

| (4.5) |

specifies a measurable norm on . The image of under is a dense subspace of .

Proof. Let us first note that by definition of the quotient norm

Hence

Let . Then since is a measurable norm on there is a finite-dimensional subspace such that if is any finite-dimensional subspace of orthogonal to then, as noted back in (2.6),

where is standard Gaussian measure on . Then

| (4.6) |

where the first inequality holds because whenever we also have . Thus, is a measurable norm on . The image is the same as the projection of the dense subspace onto the quotient space and hence this image is dense in (an open set in the complement of would have inverse image in that is in the complement of , and would have to be empty because is dense in ). QED

We can now establish the identification of as a function space.

Proposition 4.2.

Let be a continuous function, symmetric and non-negative definite, where is a separable topological space, and a countable dense subset of . Let be the corresponding reproducing kernel Hilbert space. Then there is a measurable norm on such that the Banach space obtained by completing with respect to can be realized as a space of functions on the set .

Proof. Let be the completion of with respect to a measurable norm of the type given in Proposition 4.1. Thus is continuous with respect to when ; let

be the continuous linear extension of to the Banach space , for . Now let

| (4.7) |

a closed subspace of . We observe that is transverse to ; for if is in then for all and so since spans a dense subspace of as noted in Theorem 2.1 and the remark following it. Then by Lemma 4.1, is a Banach space that is a completion of in the sense that is continuous linear with dense image and , for , specifies a measurable norm on . Let be the linear functional on induced by :

| (4.8) |

which is well-defined because the linear functional is on . We note that

for all , and so is the continuous linear ‘extension’ of to through , viewed as an ‘inclusion’ map.

Now to each associate the function on given by:

We will shows that the mapping

is injective; thus it realizes as a set of functions on the set . To this end, suppose that

for some . This means

and so for all . Then

Thus and so . Thus we have shown that is injective. QED

We have defined the function on the set , with notation and hypotheses as above. Now taking a general point and a sequence of points converging to the function on is the -limit the sequences of functions . Thus we can define , with the understanding that for a given , the value is -almost-surely defined in terms of its dependence on . In the theory of Gaussian random fields one has conditions on the covariance function that ensure that is continuous in for -a.e. , and in this case the function extends uniquely to a continuous function on , for -almost-every .

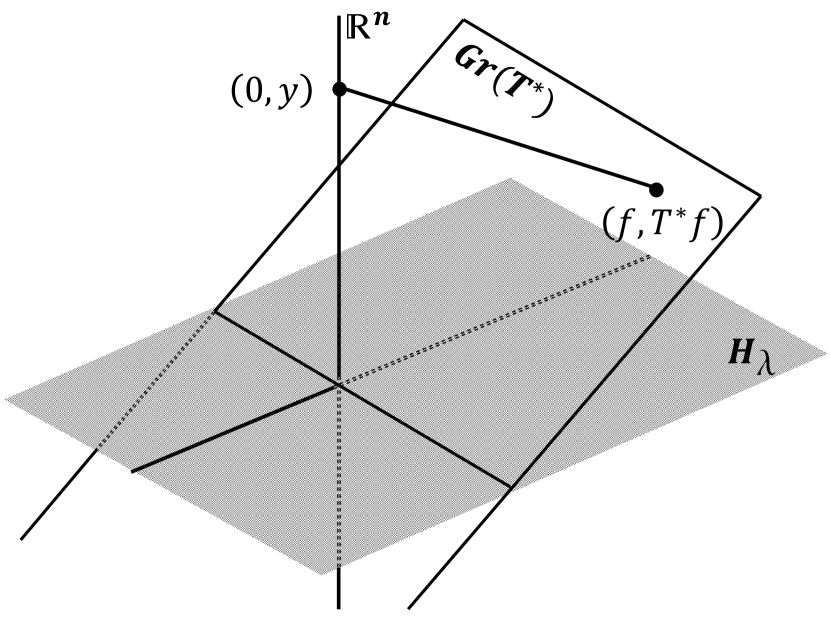

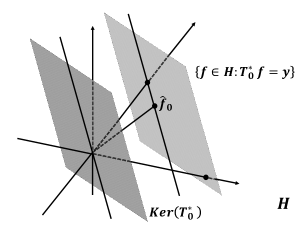

Appendix A A geometric formulation

In this section we present a geometric view of the relationship between the Gaussian Radon transform and the representer theorem used in support vector machine theory; thus, this will be a geometric interpretation of Theorem 3.2.

Given a reproducing kernel Hilbert space of functions defined on a set with reproducing kernel , we wish to find a function that minimizes the functional

| (A.1) |

where are given points in , are given values in , and is a parameter.

Our first goal in this section is to present a geometric proof of the following representer theorem widely used in support vector machine theory. The result has its roots in the work of Kimeldorf and Wahba [Wahba1, Wahba2] (for example, [Wahba1, Lemmas 2.1 and 2.2]) in the context of splines; in this context it is also worth noting the work of de Boor and Lynch [deBLyn] where Hilbert space methods were used to study splines.

Theorem A.1.

With notation and hypotheses as above, there is a unique such that is . Moreover, is given explicitly by

| (A.2) |

where the vector is , with being the matrix with entries and .

Proof.

It will be convenient to scale the inner-product of by . Consequently, we denote by the space with inner-product:

| (A.3) |

We shall use the linear mapping

| (A.4) |

that maps to for , where is the standard basis of :

We observe then that for any

| (A.5) |

for each , and so

| (A.6) |

Consequently, we can rewrite as

| (A.7) |

and from this we see that has a geometric meaning as the distance from the point to the point in :

| (A.8) |

Thus the minimization problem for is equivalent to finding the point on the subspace

| (A.9) |

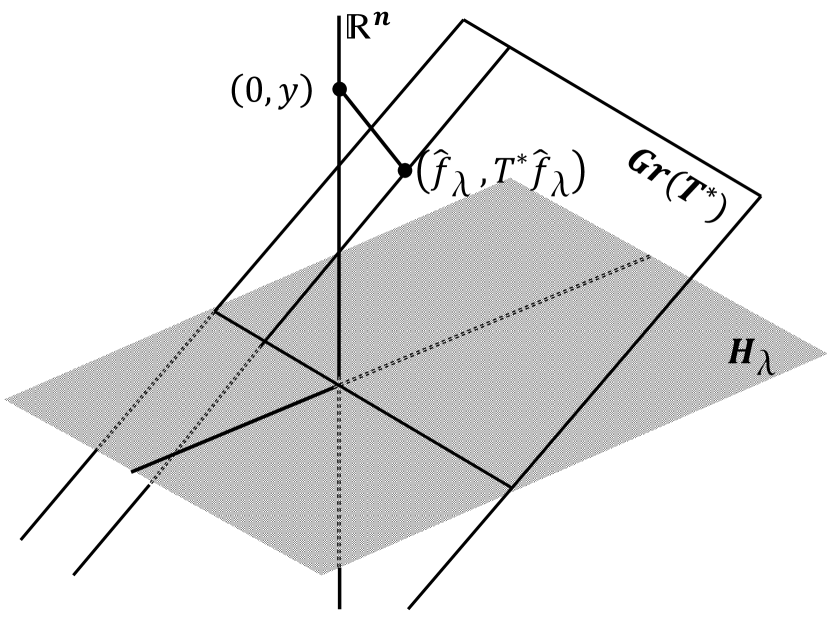

closest to . Now the subspace is just the graph and it is a closed subspace of because it is the orthogonal complement of a subspace (as we see below in (A.13)). Hence by standard Hilbert space theory there is indeed a unique point on that is closest to , and this point is in fact of the form

| (A.10) |

where the vector is orthogonal to . Now the condition for orthogonality to means that

and this is equivalent to

for all . Therefore

| (A.11) |

Thus,

| (A.12) |

Conversely, we can check directly that

| (A.13) |

Returning to (A.10) we see that the point on closest to is of the form

| (A.14) |

for some . Since the second component is applied to the first, we have

and solving for we obtain

| (A.15) |

Note that the operator on is invertible, since , so that if then . Then from (A.14) we have given by

| (A.16) |

Now we just need to write this in coordinates. The matrix for has entries

| (A.17) |

and so

Since , we can write this as

which simplifies readily to (A.2). ∎

The observations about the graph used in the preceding proof are in the spirit of the analysis of adjoints of operators carried out by von Neumann [JvN1932].

With being the minimizer as above, we can calculate the minimum value of :

| (A.18) |

It is useful to keep in mind that our definition of in (A.4), and hence of , depends on . We note that the norm squared of itself is

| (A.19) |

Let us now turn to the traditional spline setting. A function , whose graph passes through the training points , for , of minimum norm has to be found. We present here a geometrical description in the spirit of Theorem A.1. This is in fact the result one would obtain by formally taking in Theorem A.1.

Theorem A.2.

Let be a reproducing kernel Hilbert space of functions on a set , and let be points in . Let be the reproducing kernel for , and let , for every . Assume that the functions are linearly independent. Then, for any , the element in

of minimum norm is given by

| (A.20) |

where , with being the matrix whose -th entry is .

The assumption of linear independence of the is simply to ensure that there does exist a function with values at the points .

Proof.

Let be the linear mapping specified by , for . Then the adjoint is given explicitly by

and so

| (A.21) |

Since the linear functionals are linearly independent, no nontrivial linear combination of them is and so the only vector in orthogonal to the range of is ; thus

| (A.22) |

Let be the point on the closed affine subspace in (A.21) that is nearest the origin in . Then is the point on orthogonal to .

Now it is a standard observation that

(If then , so that ; conversely, if then for all and so .) Hence is the closure of . Now is a finite-dimensional subspace of and hence is closed; therefore

| (A.23) |

Returning to our point we conclude that . Thus, for some . The requirement that be equal to means that , and so

| (A.24) |

We observe here that is invertible because any satisfies , so that , and this is , again by the linear independence of the functions . The matrix for is just the matrix because its -th entry is

Thus, using (A.24), works out to . ∎

Working in the setting of Theorem A.2, and assuming that is separable, let be the Banach space obtained as completion of with respect to a measurable norm. Recall from (2.21) that the Gaussian Radon transform of a function on is the function on the set of closed affine subspaces of given by

| (A.25) |

where is any closed affine subspace of , and is the Borel measure on specified by the Fourier transform

| (A.26) |

wherein is the point on closest to the origin in and is the orthogonal projection onto the closed subspace . Let us apply this to the closed affine subspace

From equation (A.26) we see that is a Gaussian variable with mean and variance . Now let us take for the function , for any point ; then is Gaussian, with respect to the measure , with mean

| (A.27) |

where is the random variable defined on . The function is as given in (A.20). Now consider the special case where from the training data. Then

because belongs to , by definition. Moreover, the variance of is the norm-squared of the orthogonal projection of onto the closed subspace

However, for any we have

and so the variance of is . Thus, with respect to the measure , the functions take the constant values almost everywhere. This is analogous to our result Theorem 3.2; in the present context the conclusion is

| (A.28) |

Appendix B Proof of Lemma B.1

The following result is a standard one, but we include a proof here for completeness.

Lemma B.1.

Suppose that is a centered -valued Gaussian random variable on a probability space and let be the covariance matrix:

and suppose that is invertible. Then:

| (B.1) |

where is given by

| (B.2) |

where is given by for all .

Proof.

Let be the orthogonal projection of on the linear span of ; thus is orthogonal to and, of course, is Gaussian. Hence, being all jointly Gaussian, the random variable is independent of . Then for any we have

| (B.3) |

Since this holds for all , and since the random variable , being a linear combination of , is -measurable, we conclude that

| (B.4) |

Thus the conditional expectation of is the orthogonal projection onto the linear span of the variables .

Writing

we have

noting that since all these variables have mean by hypothesis. Hence we have . ∎

Acknowledgments. This work is part of a research project covered by NSA grant H98230-13-1-0210. I. Holmes would like to express her gratitude to the Louisiana State University Graduate School for awarding her the LSU Graduate School Dissertation Year Fellowship, which made most of her contribution to this work possible. We thank Kalyan B. Sinha for useful discussions.