Matching distributions:

Derivatives pricing with physical density

shape correction

Abstract.

In this paper a clean, simple and economically cogent computational method is introduced for correcting for excess kurtosis and skew in the pricing of European-style options. In fact, virtually any deviation in the physical distribution (e.g. from the Black-Scholes-Merton model) can be accommodated in a flexible, non-structural and semi-parametric fashion. The method does not involve expansions. It is based on a kind of statistical-static hedging technique related to Dybvig’s (1988) distribution pricing. This gives rise to a state price density estimate with some tangible benefits. Its principle is transparent, and it is easy to implement numerically, while avoiding some typical issues involved in such an estimation. We will analyze the properties of this estimator and provide some justification for it. At the end we illustrate numerically how the Black-Scholes-Merton model can be flexibly accommodated with non-Gaussian physical distributions.

Key words and phrases:

state price density, static hedging, derivative, pricing kernel, non-Gaussian, fat tails, skew, non-structural, implied distribution, distribution matching, payoff distribution pricing modelJEL classification: G10, G12, G13, C02

1. Introduction

In incomplete markets the prices of a new asset and derivatives on it may not be attainable by using proper hedging strategies. Even then statistical hedging may be applicable in reducing the asset’s risk component with unknown risk premium. This may readily provide a reasonable model for the price of the asset by applying a simple correction, for instance Ross’s APT pricing on the residual unhedgeable risk component.

The pricing of equities, on one hand, and derivatives, on the other hand, are usually treated as separate problems with rather different techniques. However, the estimation or calibration of the state price density (SPD) of a new asset, studied here, incorporates the price information of both the asset and the European style derivatives on it.

The function formed by taking state-by-state the ratio of the SPD and the physical density is known as the pricing kernel or stochastic discount factor (SDF). The pricing kernel is a central frequently applied tool in finance, and its unexpected empirical shape is studied by Bakshi et al. (1997), (2010) and Song and Xiu (2016). The estimated pricing kernel may be U-shaped, which is not in line with its interpretation as the marginal utility at equilibrium. This connection is discussed by Beiglböck et al. (2012) and Reichlin (2013). The physical and risk-neutral characteristics of the observed densities have been connected by Chernov and Ghysels (2000), Bakshi et al. (2003), Chalamandaris and Rompolis (2012) and Engle and Figlewski (2015). The dependence between these densities remains interesting both from the theoretical and practical point of view. It is also the focus of this paper.

Several authors have considered the problem of correcting for skewness and leptokurtic effects of the equity returns in the Black-Scholes-Merton (BSM) and other pricing models. Gram-Charlier expansions are studied by Corrado and Su (1997), (2007), Knight and Satchel (2000), Longstaff (1995), Madan and Milne (1994), and discussed in the monograph by Jondeau et al. (2007) dedicated to the topic. The technique introduced here addresses the same issue, and some further possible uses are discussed at the end of the paper. The rough idea of the constructions is the same: one builds a new asset on the old benchmark model in such a way that some specifications, e.g. the physical moments, are satisfied by the newly modeled asset, which in turn has its new ‘internal’ SPD.

Here static hedging techniques and statistical hedging philosophy are combined to construct a hedgeable proxy derivative for the non-hedgeable new asset. The economic rationale in using such proxies is that if two assets appear superficially sufficiently similar, then the investors may not differentiate between them in pricing, even though their returns do not strictly coincide as cash flows, which is the case in hedging based on a proper arbitrage. For instance, statistical arbitrage activity in a market conceivably leads to a situtation described in the APT. Dybvig (1988) considers a payoff distribution pricing model (PDPM) where the price of an asset depends on its single-step payoff distribution. This work was recently extended by Rieger (2011) and Beare (2011) where there is further discussion on the devolepments around the PDPM. Dybvig is mainly interested in finding an extreme price range for a given payoff distribution. Although the starting point is somewhat similar in this paper, the approach is eventually quite the opposite, since here we investigate rather conservative monotone rearrangements of the state space which seem reasonable in ’correcting’ a benchmark model.

In this paper a SPD estimation technique is introduced for an asset highly correlated with a liquid proxy security, which in turn has a rich class of underlying European style options on it. A distribution matching pricing principle is introduced here. It is easily described; one simply constructs by static hedging a European derivative on the proxy security such that the payoff distribution matches the price distribution of the asset being priced. Thus, the asset is valued based on its price distribution at a given strike time of the derivatives. The constructed derivative and the security become comonotone. Ideally, the asset price becomes almost perfectly correlated with the proxy derivative payoff . Here is the proxy security price at the given strike .

This problem is mathematically ill-posed since for a given price distribution there exist several matching derivatives, martingales and prices. This serious issue is in part alleviated if the proxy derivative can be constructed in such a way that it is indeed highly correlated with the asset. Thus there are fewer hypothetical martingales on the proxy security to consider. The new pricing model is not merely an arbitrary one satisfying the given physical density specifications, it is also in some sense statistically close to the benchmark model. Despite the theoretical obstructions, the correction for distributions in analytical European style option pricing models remains of practical importance.

The treatment here is continuous-state, rather than being discrete, such as in implied trees studied by Rubinstein (1994) and Monte Carlo methods reviewed in Glasserman (2003) and Jaeckel (2002). Instead, the approach taken here follows to some extent the general philosophy of Bakshi et al. (2003) and Jarrow and Rudd (1982). The former raises the problem of differential pricing of individual equity options versus the market index. This can be addressed by using our main formula (1.1) for comparisons of SPDs. These matters are also closely related to the works of Buchen and Kelly (1996), Halperin and Itkin (2014), Hocquard et al. (2015) and Madan (2006).

The main benefits of the distribution matching are the following. It is essentially model-free, semi-analytic form and does not require any ad hoc discretizations or families of density functions. In particular, it does not require assumptions on the dynamics of the asset, which often play a major role in econometrics, see e.g. Andersen et al. (2015). This approach is stable even under infinite variance, a case which occurs typically in connection with fat-tailed distributions. The technique here can be seen as a non-structural, semi-parametric (cf. Stutzer 1996) version of moment matching techniques investigated by Airoldi (2005) and Brigo et al. (2004). Instead of matching some first moments of the physical distributions, the distributions are completely matched. In particular, the technique accommodates all skewness-kurtosis pairs, unlike Rubinstein’s (1998) Edgeworth trees and Johnson binomial trees investigated by Simonato (2011). It admits even multi-modal risk-neutral and physical distributions. Also, the issue of negative probabilities does not arise here.

The formula obtained for the new asset’s SPD is simple:

| (1.1) |

where and are the benchmark model physical density and SPD, respectively, and is the new model’s physical density. Model may be considered as the ’corrected’ version of pricing model . The state space transform is increasing, it preserves physical probabilities between the models and can be easily computed numerically.

The above SPD appears as a useful by-product from a proxy derivative construction. As an intermediate step, this proxy derivative is first approximately assembled using only finite portfolios of digital options on the proxy security. This shows how statistical-static hedging of a given asset could be accomplished in practice.The resulting asset pricing rule by such proxy derivatives is not linear in general, cf. Chateauneuf et al. (1996), but it is homogenous (respects the scaling of cash flows), respects a Modigliani-Miller type separation and satisfies some other natural properties, like continuity and monotonicity with respect to stochastic dominance of assets.

The inter-model formula (1.1), which connects physical densities with state prices in a simple way, is the crux of this investigation. It may be interesting in connection with the volatility smile, pricing kernel shapes, non-parametric calibration of SPDs and related matters. Although (1.1) should be considered an estimate in general, it performs correctly for risk-neutral densities if the pricing models are sufficiently isomorphic. For instance, this is the case if we compare BSM models having the same market price of risk. See Section 7 where we provide some facts which support (1.1).

Interestingly, it turns out that the state space transform , arising purely from the proxy derivative construction, in fact induces an optimal transport plan for the given physical measures. This is a central notion in the theory of optimal transport, which in turn has been applied recently in various economic problems. These include martingale optimal transport, economic equilibration, matching problems and hedonic models, see e.g. Henry-Labordere (2017), Ghoussoub and Moameni (2014) for discussion. Hence the name of this paper.

As an application, the inter-model formula is applied in correcting for kurtosis and skew deviations in the BSM model. The numerical algorithm is easy to implement and is illustrated at the end. The considerations also appear to lead to some further interesting econometric analysis, which could be termed as ’Implied Physical Distributions’, generalizing implied volatility.

2. Preparations

The references Bakshi et al. (2003) and Jarrow and Rudd (1982) provide the context for this paper. For a suitable background information, see Aït-Sahalia and Lo (1998), Breeden and Litzenberger (1978), Carr and Chou (1997), Cochrane (2005), Derman et al. (1995), Fengler (2005), Föllmer and Schied (2005), Jondeau et al. (2007) and Shreve (2004).

2.1. Preliminaries on the formalism

First a word of warning: we often discuss matching a cash flow. Here we seldom hedge cash flows by proper arbitrage. Instead, we typically build a matching cash flow in distribution, which is a considerably weaker hedging notion, cf. Dybvig (1988). The terminology ’estimate’ and the corresponding notation are used rather liberally for the sake of convenience. In particular, the errors are not specified statistically and no unbiasedness etc. are claimed.

We will consider mostly a single-step model with the present time and the future maturity of options . As usual, the physical measure involving asset prices is denoted by . We will denote by the state price measure and by the risk-neutral measure, both assumed absolutely continuous with respect to the Lebesgue measure on the state space. For instance, the price of an asset and bond are

Recall that if the densities of measures and on the real line are continuous functions and , respectively, then the Radon-Nikodym derivative is

For convenience we assume throughout all densities to be continuous and their supports to be (possibly unbounded) intervals. In case of standard Lebesgue measure we surpress . The SPD and the risk-neutral density (RND) on an asset are denoted respectively by

As usual, the time- value of a ’plain vanilla’ European call option on security is denoted by . Similarly, we denote the price of a ’digital call’ having payoff . Here is time of valuation, is the expiration and is the strike price. More generally, stands for the value of portfolios and assets at a given time. Let us recall the market price of risk, , where , and are the usual parameters of the BSM model.

2.2. The valuation method explained

We will first price an asset , considered as a single-step stochastic cash flow, by constructing a derivative security with a matching payoff distribution. Thus the valuation involves statistical hedging in comparing the distributions and static hedging in constructing a suitable derivative in the single-step framework. However, by no means is such a derivative unique, nor is the price unique. Therefore, we are required to make some further specifications.

Pricing by distribution matching involves an asset being valued, , and a benchmark security, which is traded and has abundantly sorts of European style options written on it. The technique is focused on a given time interval and in particular the distributions of and which involve separate models, , . More precisely, these single-step models are

where the state space of and is considered here and and are the physical and state price densities on . The time is also the expiry of the options on .

Ideally, the asset being valued, i.e. , and the benchmark security are very highly correlated and with approximately same return distributions, that is, the asset is a ’quasi twin security’ of . In a less ideal situation we have non-perfectly, but still highly correlated liquid proxy security and European style call options on the proxy security. We will use the option price information here to patch some of the information lost due to imperfect correlation.

This is performed as follows. The SPD of the proxy security can be estimated from option prices. This density can be interpreted as a system of ’infinitesimal’ Arrow-Debreu securities, or degenerate double digital options. Intuitively, we will reweigh the A-D securities and reassemble them to obtain a portfolio with the same distribution as the asset being priced. The portfolio of A-D securites, which will be highly correlated with the asset, can be viewed as the derivative sought after.

To outline the distribution matching pricing method, we consider , an asset to be valued, and a proxy security . We take as given time- estimates of the following:

-

(1)

The continuous physical distributions and on and ,

-

(2)

The SPD on .

The distribution matching technique then yields , an estimate for the SPD on .

This technique boils down to SPD transformations. The particular transforming, or the A-D securities reassembly procedure, is performed in such a way that the resulting prices meet some natural ’rationality’ conditions.

The SPD may or may not follow some standard option pricing formula, and it may be estimated by a specialist from the market data. See e.g. the works Ait-Sahalia and Lo (1998) and Ait-Sahalia and Duarte (2003).

In fact, this approach can be viewed as an asset pricing counterpart of real options valuation, where cash flows are modeled by trees which can be solved. However, the analysis here is continuous-state and there is active calibration according to market information.

Next we will explin the assumptions, or rather the thought experiment behind distribution matching. This is also related to implied trees and Marketed Asset Disclaimer in real options analysis.

In distribution matching one first considers portolios of digital options on with expiry in such a way that the value of the portolio , considered at time , is highly correlated with and the distribution of the portfolio value at time is close to that of , in symbols

These portfolios are finite and as such the distributions are rough approximations of that of , and at this stage the portfolios are by no means unique.

As a response to the above issues one passes to the limit in the process of refining these portfolios in such a way that the payoff distribution of the portfolio matches exactly the distribution of . This leads to an analysis of physical and state price distributions with a particular state space transformation. The resulting idealized portfolio of infinitesimal Arrow-Debreu securities is not ad hoc anymore at this stage; instead it is a unique arrangement of options such that some natural properties of the pricing functional are satisfied.

Namely, the portfolio can be seen as a European style derivative on such the payoffs and are comonotone.

In an ideal case where the benchmark security and the asset are very highly correlated, the ideal portfolio then satisfies

| (2.1) |

Note that then statistically hedges but we argue the hedging notion is actually much stronger due to high correlation. If the correlation was in fact perfect, then the portfolio would be a complete hedge for in the single-step model.

The thought experiment is reasonable if we consider the known ill-posed problem of correcting the BSM model for deviations from lognormality. In such an analysis it appears a natural starting point to consider markets which accommodate two highly correlated and approximately similarly distributed assets: One which exactly follows the BSM model and another one with only approximately normal return rates.

The technical details are discussed next. It would be conventional to consider mainly risk-neutral measures in the analysis, but we adopt a different, albeit completely equivalent, approach, considering mainly ideal portfolios of Arrow-Debreu securities. We choose to do so, since the latter approach seems more transparent in this setting.

2.3. Continuous portfolios of infinitesimal Arrow-Debreu securities

Let us recall some well-known ideas of Breeden and Litzenberger (1978). See also the related works of Bick (1982), Brown and Ross (1991) and Jarrow (1986). Consider the price of digital call options with payoff . Suppose that exists and is continuous on (although the Breeden-Litzenberger representation generalizes to a more general setting). Then, regardless of the model, this represents the SPD:

Next we will consider a formal digital option on , which pays unit of numeraire if the underlying asset satisfies , and pays in the contrary case. We will apply a formal notation

| (2.2) |

which becomes sensible in the context of integration. The above corresponds intuitively to the degenerate case where the trigger is exactly or is negligible. Such an option is subsequently termed an infinitesimal Arrow-Debreu security. The chances of this option being triggered are negligible as well, so the value of it is ’infinitesimal’, hence the terminology and the right hand term .

We wish to form portfolios consisting of infinitesimal Arrow-Debreu securities with all possible strikes at the same time. Thus these portfolios are not only infinite, but they contain continuum many types of assets. The information on the distribution of different types of calls can be conveniently decoded as a Radon measure. We will formalize these portfolios as signed absolutely continuous measures, denoted by . Let us denote the value of the portfolio by .

If the Radon-Nikodym derivative is positive at a point this means that the portfolio has a long position on the Arrow-Debreu security corresponding to strike . Similarly, if is negative, then the portfolio has a short position on the A-D security corresponding to strike , and, moreover, the relative weight of the position is . It is instructive to think of relative weights as being analogous to probability densities, only the sign may vary according to the short/long position.

The payoff of such a portfolio at time in the case is

The financial interpretation here is that the portfolio is a bundle of A-D securities with different strikes, and all other securities, except the ones with strike , expire worthless. Thus the payoff of the portfolio is the amount of strike- A-D securities held.

The value of the portfolio at time is the aggregate value of all the A-D securities in it:

The financial interpretation is that is the price of strike- A-D security and is the amount of such securities in the portfolio.

Thus, if we wish to construct a European style derivative with payoff (which could also have negative values, e.g. in case of futures contracts), we assemble a portfolio with the weights for each strike . The value of the porfolio then assumes a familiar form:

For instance, a standard European call option with strike price is replicated by a portfolio as follows: For each there are included many strike- A-D securities, thus .

This idea discussed above is surely not new to specialists, but this tool will be useful in performing static replication transparently.

3. The pricing framework

Let us consider two assets, an asset that will be priced, , and a proxy asset . We will study different pricing models corresponding to these assets. When comparing the SPDs of the models we usually assume the short rates in the models coincide, , so that the SPDs and integrate to the same bond price.

Suppose that are continuous density distributions of and . We assume that the supports are intervals , . We denote by and the corresponding physical probability measures111It is debatable whether the assets, modeled as random variables, should coexist in a same probability space or not. If they do, then these measures can be seen as push-forward measures. This issue is analogous to the marketed asset disclaimer in real options analysis..

Thus there is an absolutely continuous increasing function such that (where is the image of ) for any interval 222Hence for any measurable subset by a Dynkin-type argument.. The above probability-preserving condition can be stated for an increasing and absolutely continuous map equivalently as

The purpose of is to pair up the distributions in a suitable way. This is certainly not the only possible --measure-preserving transformation (see Dybvig 1988), but it appears to be a natural one which leads to reasonable conclusions.

To replicate the value distribution of we will construct a suitably weighted portfolio of Arrow-Debreu securities of varying strikes on the state space of . Our aim is to build a portfolio whose time- value, given the event for any , satisfies

In other words, the portfolio ’contains many’ A-D securities corresponding to the event where the corresponding A-D securities are essentially degenerate double digital options on with payoff . Thus the portfolio of A-D securities pays exactly in the event . Since the transformation is order-preserving and --measure-preserving, it follows that for every we have

Thus the value distribution functions of and coincide.

3.1. Intermediate stage: Approximating the cash flow with finite portfolios of digital options

To make the analysis more tangible and cogent we begin the construction of with an intermediate step involving simple portfolios. This provides the means required to statistically hedge assets by static replication strategy containing long and short positions of (finitely many) potentially traded options on the proxy security. Eventually we will pass on to the limit, letting the number of steps used in discretization tend to infinity and thus asymptotically match the distribution of . Nachman (1988) studies the approximation of general European derivatives in a static model with portfolios of plain vanilla options.

For convenience, let us assume at this stage that the supports of are bounded intervals. Then we may approximate in distribution the value with a finite portfolio of digital calls. Let . Then there is an with the following partitions:

-

(1)

of the support of such that and for .

-

(2)

of the support of such that for .

Clearly

is bounded by , uniformly for all states . Motivated by this observation, we will build a portfolio on the security side to match the above linear combination of indicator functions. We form a portfolio of double digital calls by including in for each a position with payoff

| (3.1) |

which has the replication cost

| (3.2) |

The corresponding weights on the digital options are and for strikes and , respectively, and

| (3.3) |

for other strikes . Here we may define the corresponding portfolio of A-D securities by

Indeed, note that the arbitrage-free value of the instrument

is . The price of the described portfolio at time is

| (3.4) |

By cultivating the above portfolio construction with discretized version of (4.1) below, one may build an approximating portfolio with plain calls as well.

4. Constructing a cash-flow-distribution-equivalent portfolio

Recall that the density of the event is . The corresponding event on the proxy security side is , and its density is . In the case of such an event the corresponding A-D security returns unit of numeraire (and not units). Therefore we will compensate by using the weight on the A-D security corresponding to the event . Secondly,

since is measure-preserving. Here the fractions on the right hand side are the Radon-Nikodym derivatives of the measures. Thus, (see (2.2)) we will regard as a weak solution to the differential equation

| (4.1) |

In practice, the densities are continuous and the solution is in the usual sense. Note that can be computed easily by numerically solving the above separable ODE. If and are the corresponding cumulative distributions, then

| (4.2) |

There is an interesting digression independent of the subsequent financial motivations. Equation (4.2) defines a well-known solution333The above arrangement minimizes so-called Wasserstein’s distances on the real line, see e.g. Svetlozar and Ruschendorf (1998). to a problem in mathematical optimal transport theory, motivated by logistics and mathematical economics. Such problems were first considered rigorously by Kantorovich (1942).

For each the cash flow (considered a contingent claim on ) can be ’matched’ via transform , up to precision , by a portfolio (a contingent claim on ) with value

| (4.3) |

Thus, in both the cases the possible payoffs are the same ( and ), and the probabilities of the positive outcomes coincide.

In our portfolio we will buy at time the amount of (infinitesimal) A-D securities at each strike : Then can be characterized by

Recalling the chain rule of differentiation, (4.3) and the Breeden-Litzenberger representation considerations, we obtain the time- value of portfolio of A-D options.

Proposition 4.1.

In the above setup the arbitrage-free time- price of is

| (4.4) |

Here the portolio can be interpreted as a European style derivative on with the following properties:

-

(1)

At time the derivative at maturity and have the same value distribution.

-

(2)

The payoff of the derivative is an absolutely continuous strictly increasing function on the value .

The latter condition typically implies that the derivative payoff and are highly correlated.

Provided that all the relevant information is understood, we denote by the value (4.4). To summarize (see subsequent Proposition 5.5):

Proposition 4.2.

Assume the above setup. If is a European style derivative on with absolutely continuous strictly increasing payoff, , then the arbitrage-free price of is

Thus, if can be regarded as being approximately such a derivative, then pricing boils down to valuing the above derivative and an ’error term asset’, possibly by some other means, e.g. the APT.

Above we applied for simplicity the same discount factor in both pricing models. If we are comparing two models with a priori known or assumed discount factors, which are different, then the Arrow-Debreu assets must be additionally scaled, so that, for instance, the risk-free bond prices in asset- model become correctly priced. This leads to considering risk-neutral densities (RND) in place of SPDs .

5. Distribution matching asset valuation: Basic properties

There are potentially several possible measure-preserving transformations to choose from. However, the transformation , which continuously preserves the order of states, appears heuristically the most reasonable. The claim that this transform is ’natural’ is also corroborated by the following nice features which are specific to this particular type of transform.

Proposition 5.1 (Limit of approximate portfolios).

Assume that and are as above. Then the values of the approximating finite portfolios in (3.4) converge to the value (4.4). Moreover, a similar conclusion holds in case where the supports of are unbounded intervals if the averages (see (3.1)) are replaced by smaller absolute value terms of the respective subintervals.

The following fact is an immediate result of the construction of the portfolios in distribution matching.

Proposition 5.2 (Uniqueness up to distribution).

Assume that the distributions and coincide, , and the proxy security has a SPD in its model. As above, suppose that we are using the information of model with the distribution of to price by distribution matching. Then

Proposition 5.3 (Monotonicity w.r.t. stochastic dominance).

Suppose that and are securities such that and we are using the same proxy security model for both of them separately in distribution matching. Then

Along the same lines one can show that if , then . We note that the fact that the state space transformation is increasing is essential here. The pricing rule does not, however, preserve second order stochastic dominance without further assumptions.

Proposition 5.4 (Continuity).

Assume that the SPD corresponding to asset is bounded and as . Suppose that assets in -mean as . Suppose that we apply distribution matching technique with and , in forming the corresponding portfolios , , respectively where . Then

The pricing method is not linear, that is, if and are securities with respective A-D portfolios and , then the portfolio resulting from the combined cash flow typically satisfies and typically . This is due to the fact that the valuation machinery, on the asset (to be priced) side, depends only on the distribution of the cash flow and does not take into account correlations. Indeed, consider for instance equally distributed flows and such that has zero variance and has non-zero variance. However, a Modigliani-Miller type separation of value holds, see Proposition 5.7 below.

Proposition 5.5.

Suppose that asset is in fact a European style contingent claim on asset . We consider a model of with given and . Assume further that the payoff is absolutely continuous and strictly increasing on . Then the distribution matching method prices correctly; the arbitrage-free price coincides with the value .

This has the following rather immediate consequences. Pricing by distribution matching is in a sense consistent within the BSM framework.

Remark 5.6 (Consistency with the BSM model).

Consider a BSM model asset with a European option payoff and an asset . Assume that and are as in Proposition 5.5. Then coincides with the initial value of the BSM value process of the derivative replication

The suitable payoff function appears in the construction of the required portfolio above, namely, .

Proposition 5.7.

Suppose that at time the future prices and are perfectly correlated with the prices . This means that these are obtained from each other by affine transforms (i.e. shifted linear transforms) and and can be viewed as European style options with strictly increasing dependence on the underlying asset . Then distribution matching correctly prices and , considered derivatives on with strike time and the pricing is linear in this case:

The reason we require positive weights and and perfect correlation is that the distribution matching technique does not take into account the correlation structure of assets.

6. Applications: Performing a correction in the pricing of European calls under skew and fat tails

The above valuation technique suggests a method for correcting for any type of distribution deviation in a given analytic-form pricing model. The pricing of derivatives based on the price distribution of the underlying is plausible according to Proposition 4.2. However, without any information on the dynamics of the uderlying, the problem is ill-posed since there may be several martingale measures and corresponding arbitrage free prices. We assume that in addition to the analyzed underlying asset in the market there is a highly correlated ‘quasi-twin’ asset which accurately follows the dynamics of the analytic-form pricing model. Then the distribution matching technique produces a derivative with payoff which is equally distributed and highly correlated with . Here is statistically hedgeable but may not be properly hedgeable by using derivatives on . Thus there is a hypothetical ‘error term’ cash flow such that

| (6.1) |

where has mean and small variance. In modeling it seems reasonable to treat the value asymptotically as , e.g. by invoking the CAPM, APT or other factor models, possibly non-linear ones, see Atlan et al. (2007).

The benefit of this method, similarly as in non-structural techniques mentioned in the introduction, is that we may amalgamate the desirable properties of empirically realistic models of asset returns, and, on the other hand, those of analytically tractable models.

For example, we may attach skew and fat tail features in pricing European stock options, using the BSM model as the ’ground model’. To accomplish this we require all the data appearing in the BSM model at time , excluding and , and a modeled physical (non LogNormal) distribution of the stock price at . In the case of European type call we thus require the following data:

-

(1)

Asset price at time , . (Given empirically.)

-

(2)

Interest rate at time . (Empirically observed; we choose it similarly as if applying it in the BSM model.)

-

(3)

Maturity . (Given.)

-

(4)

Strike price . (Given.)

-

(5)

Modeled probability density function for the price of the stock at , . (Either analytical form fitted to data or directly from data by local regression.)

Setting the implied volatility and trend. The implied volatility and the implied trend are chosen in such a way that the median of the modeled physical distribution of coincides with the median of the log normal physical distribution of the BSM model with parameters , , and . Additionally, we require that the interquartile ranges (IQR) (i.e. the lengths of the intervals) coincide. The median and the IQR clearly determine and uniquely.

The motivation for doing this is twofold. Firstly, considering medians appears compatible with the way we constructed the derivative above. That is, by transforming distributions in states’ order-preserving and continuous fashion, so that there is one-to-one correspondence between the quantiles of the probability distribution and its transformed version. Secondly, suppose that we have a PDF of the form where , , is log normally distributed and is also a very skewed and fat tailed one. Thus is a kind of mildly modified version of with some added skew and fat tails. This case corresponds to a typical application here. Note that the median and IQR of are close to that of . Thus the internal calibration of and by equating the medians and IQRs. Also note that using the means or variances of the distributions would be out of the question, since the mean of the modeled physical distribution may fail to exist, due to fat tails, but, on the other hand, the quantiles of a distribution always exist.

6.1. Illustration: Parametric case. Modeling the risk-neutral distribution from a given mixed LogNormal-LogCauchy-LogStudent-Lévy type physical distributions superposed on the BSM model

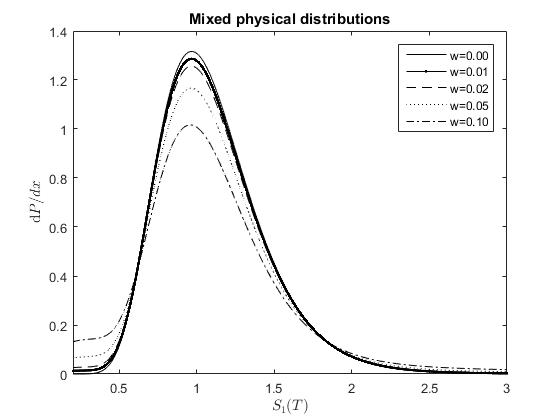

To illustrate the application of the pricing scheme under investigation we computed the prices of calls under varying underlying physical distributions with negative skew and excess kurtosis.

We approximate numerically the SPDs in a relatively dense grid. We denote by the mixed

PDF and by (resp. ) the log normal physical PDF (SPDs) of the BSM model. We compute the corresponding SPDs by the following loop in pseudo code:

Let and fix such that ;

For i=1 to N;

Let ;

Let and ;

Next;

To torture our model with super-heavy tails, we consider physical distributions which are mixtures of the following distributions: LogNormal, LogCauchy, LogStudent (), Lévy. The main component is the lognormal distribution with BSM model parameters , , , , , and the parameters of the rest of the distributions are in the program documentation. We formed the mixed distribution by taking a weighted average of the distributions, putting the same weight on all the non-LogNormal distributions and the rest of the weight on the LogNormal distribution. We performed the calculations under different weights involving the fat-tailed distributions. Thus the respective LogNormal weights were . Note that the LogCauchy density is unbounded which affects the mixed distributions as well. This puts some burden on the numerical implementation.

We identified the median and the quartile interrange (QIR) of each of the mixed distributions corresponding to different weights. We then searched for LogNormal distribution parameters, and , such that the median and the QIR coincide for the mixed distribution and the LogNormal one. We use the same values for and fixed previously. We are not assuming here that is the correct price of the underlying in question, it is merely the price of a ’nearby’ proxy security, possibly a hypothetical one. The BSM model fixed above is then used as a ground model which provides the required densities and .

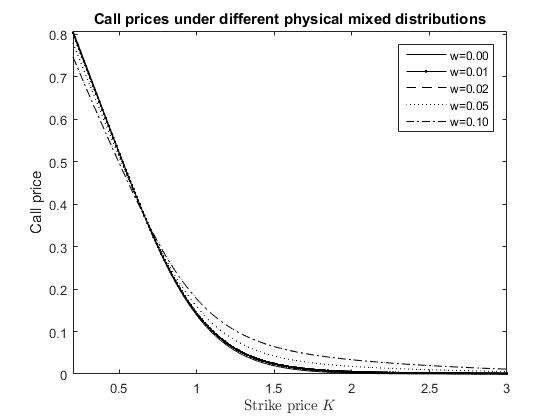

For the weight and strike price we get the value for the call option, as one expects. Changing the assumptions regarding the physical distribution, which in this framework is reflected by the risk neutral distributions, affects the modeled prices of the underlying asset (according to (4.5)) against the proxy security.

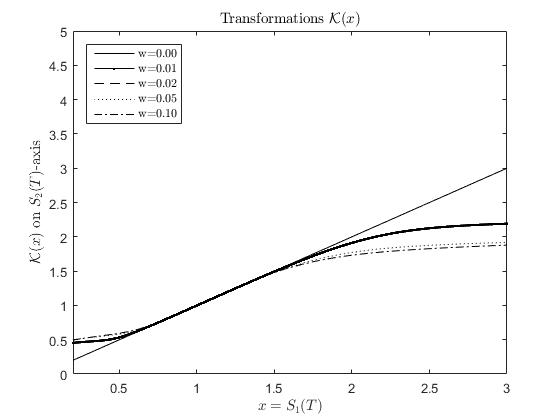

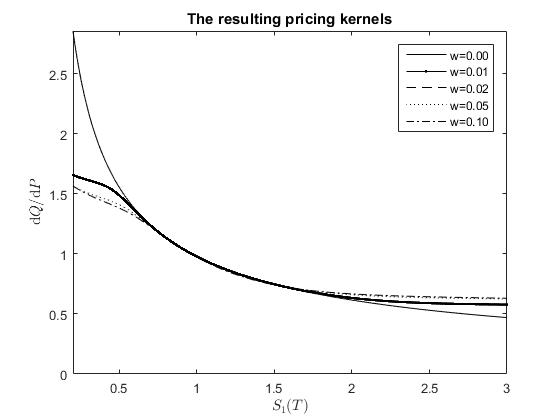

The formation of the modeled state-price density is illustrated below. On the -axis we have the states of the underlying asset where the benchmark security (corresponding to the case ) is at-the-money at . For numerical reasons we report states since has a singularity at .

The differential has a singularity at . For the sake of numerical stability of the algorithm, the interval had to be treated separately and the plot does not include this interval. This does not cause an economically significant error, since the probabilities and the prices of the stock are small on this interval anyway.

The computations were performed on Matlab 2015b (8.6.0.267246 win64). The accuracy of numerical integration and Euler’s method for solving ordinary differential equation performed was heuristically controlled by varying the step size . The computations required about minute on a laptop computer.

In the above illustration we took the initial benchmark security price as given, . Then we priced all European style options on , including the trivial case with the asset itself, . However, if the price of the asset is observed, then we may ’calibrate’ so that the method produces the right observed price . Indeed, recall that in the construction of the pricing measure the asset is modeled as a European derivative on security with increasing payoff function. Thus for instance in the BSM model the price is a strictly increasing continuous function of the initial price .

7. The soundness of the inter-model formula

Eventually we will apply our technique in correcting for the skew and kurtosis in BSM pricing model. This problem is in fact ill-posed, the way it is considered here, since we are not making any assumptions on the dynamics of the asset prices. Admittedly, this fact may bring into question the soundness of the valuation technique.

We argue that formula (1.1) provides a reasonable estimate for model SPD. To justify this we will sketch some situations where it performs accurately.

The assumptions made below are eventually rather restrictive. However, this does not mean that the pricing technique, understood as a reasonable estimate, should be equally restricted in its applicability.

Distribution matching also resembles some valuation methods in capital budgeting. Namely, the marketed asset disclaimer of real options analysis (see Trigeorgis 1999) is analogous to the proxying principle applied here.

7.1. Comparison to risk-neutral pricing

Let us assume that we have an asset modeled as a single-step cash flow

as in (6.1). If then we may use almost surely and then

becomes uncorrelated with , and . Then, in the setting of Proposition 5.5, we may price up to the error term,

if is a European-style derivative on in model . The first risk-neutral expectation on the right-hand side can be correctly priced by Distribution Matching if the above payoff is assumed to be absolutely continuous and increasing. The second expectation, or the pricing error, can be controlled if model is specified, so that can be calculated,

Here we applied the Cauchy-Schwarz inequality and is the standard deviation of .

7.2. Digression: Value-at-Risk threshold utility correspondence between market models with representative agents

In this section we study a special case where the SPDs of the market models are determined by utility functions of representative investors. The conditions for aggregating the markets by means of the notion of a representative investor have been studied e.g. by Ait-Sahalia and Lo (2000) and Rubinstein (1974). Recall that in pricing with market equilibrium and representative agent utility function a first order optimality condition involving the equilibrium can be expressed as follows:

where the left hand side denotes the SPD of the state , is the utility function of the representative agent and is a suitable constant depending on the time value of money and the marginal utility of the initial capital at time .

Suppose that and are differentiable representative agent utility functions of market models and , respectively. Usually the single-attribute utility functions are thought to depend on the absolute level of money (or numeraire, or consumption level), but alternatively they may be written in the form

where is a suitable differentiable strictly increasing auxiliary function and is the cumulative distribution of . This can be arranged as a convention, since there is typically a -to- correspondence between the states of and the cumulative probabilities. In terms of Value-at-Risk essentially the same can be expressed by stating that the map (confidence level to the respective quantile), together with the given utility function induce the auxiliary function . Writing the utility function in this form is merely a matter of convention.

Suppose that the representative agents partially agree on their utility in the sense that there is a universal way the utility functions are formed, only the market model specific physical distributions differ:

| (7.1) |

This means that both the utility functions are values of a common auxiliary value profile parametrized according to confidence levels and

This is one instance where the distribution matching, pairing the market models and , can be applied to correctly predict the prices in one of the models with respect to that of the other. This essentially follows from the chain rule:

Note that if the values of maturity face value risk-free zero-coupon bonds at time coincide in the market models and , then

so that . Even if this were not the case, we may consider risk-neutral probability measures and , in place of the pricing measures. Thus, we may essentially suppress the constants, .

Now, if is taken to be increasing, continuous and --measure-preserving on the positive real line, we have that . Thus

so that

This condition clearly states that (4.4) correctly prices the model asset in terms of the European call price system in model, up to discounting. More generally, in this case the price of any European style option written on the asset can be recovered from the market model together with the physical distribution of the asset.

Example 7.1.

Let us compare two separate BSM models with the same market price of risk:

| (7.2) |

The required transform is defined by

after surpressing some insignificant terms. Indeed, this is clearly increasing, continous and it is also measure preserving by the basic properties of the normal distribution.

Note that

for a suitable constant , since all the BSM model parameters and , are deterministic. This means that

| (7.3) |

Note that direct calculations involving the risk-neutral and physical BSM model densities yield

Next we will follow the approach where a utility function is implied by matching equilibrium first-order utility condition and the pricing kernel. Thus

where we have isoelastic utility functions

so

According to (7.2) and (7.3) we obtain

up to multiplicative constants which we will continue surpressing bluntly. Recall that we are working in risk-neutral price system which means that at the end the multiplicative factors are normalized suitably. Put

Then

and

Then we obtain, given a European derivative payoff profile , that

This means that in our setting with two separate BSM models with the same market price of risk the SPD estimation technique (see (4.5)) performs correctly between the models for risk-neutral prices. The short rates in the models and may of course differ and hence the discount terms must be reconciled.

Next we will extend these ideas to the dynamical setting.

7.3. Sufficiently isomorphic pricing models

Up to this point we have studied the behavior of assets essentially with a single time step and next will consider assets with continuous evolution of prices. We will study conditions relating the dynamics of the securities ( and above) together, which guarantee that our pricing method indeed connectes the models together properly, see (7.4).

The result in this section roughly states that if one has a misspecified model for a security, then, under suitable conditions, one can still recover the true value of the European style contingent claim on the security. To manage this we are clearly required to have some extra information and to assume some things on the model(s). Namely, assuming that the stochastic asset price models within the class are ’sufficiently isomorphic’ we proceed by using distribution matching, thus coupling the biased SPD and physical density together with the true physical density. Then we recover the true SPD.

We analyze a case where two assets dynamically depend on a common latent stochastic state variable. Suppose that and are driven by a common process with almost surely continuous realizations and

We denote by a filtration generated by the above stochastic processes and we assume it to be continuous. Here we assume that functions and are continuous.

Suppose that the price processes can be approximated by binomial models corresponding to even discrete increments in time where the above stochastic differential equations are replaced by discrete type difference equations described shortly. We consider -valued random variables (ups () and downs () in the binomial models) such that in probability as for every , where is defined by piecewise linear interpolation from the values

This means that , , are binomial processes. Intuitively speaking, are asymptotically adapted to . Define the corresponding assets

In the literature it is customary to use scaling in innovations in binomial models. However, we may resort to the above definition since the scale of the innovation terms is not fixed here a priori. This provides us with the states and the corresponding probabilites of the binomial models . Let us consider instantaneous short rates and in the binomial model let the short rate used in the step be .

The above seems to suggest approximating stock prices which are obtained by piecewise linear interpolation from the binomial processes:

, so that

where .

Instead, we define directly by

where the trajectories are absolutely continuous almost surely. The dynamics appear very close to that of (notice the superscript ) but here the definition actually runs by means of classical analysis since the realizations of are piecewise linear.

Theorem 7.2.

Let us consider the setting described above. We additionally assume the following stability conditions:

-

(1)

The physical and risk-neutral distributions of , and , are continuous functions on .

-

(2)

, in probability as for all .

-

(3)

The unique risk-neutral probabilities of the states in models converge in distribution to in the sense that

-

(4)

is an increasing function of for each .

We assume that the ‘local market prices of risk’ in the models almost surely coincide:

If the risk-neutral density on is applied together with the physical laws of in distribution matching method with the corresponding transform (see (4.4)), then the risk-neutral density of can be represented as follows:

| (7.4) |

and in particular the correct risk-neutral prices of derivatives are recovered:

Since the short rates may differ in the models, the AD securities may be differently scaled in these models and this is why we have a formula for risk-neutral prices, instead of state prices.

8. Discussion

We introduced a novel ’Distribution Matching’ asset pricing technique which provides a natural correction to derivatives prices with respect to a benchmark model. The corrected RND (estimate) can be neatly expressed:

This is operational in the sense that the densities can be estimated or assumed from a given model and can be easily solved numerically.

In distribution matching one constructs essentially a European style derivative on a liquid proxy security. According to the static hedging principles this derivative will be correctly priced, per se, in the given framework. Of course, the value of a derivative need not be close in general to the value of an asset with the same future price distribution. However, if the derivative payoff and the asset price are additionally highly correlated, then there are various avenues of financial arguments suggesting that the values should be close as well. In fact, this principle seems to have been applied in the finance literature abundantly in this connection, although, usually somewhat implicitly. For some related works, apart from the Grahm-Charlier approach and references above, see Jackwerth and Rubinstein (1996) and Madan, Carr and Chang (1998).

Athough intended primarily as an approximate estimate, some example frameworks were given where the technique performs exactly correctly. The technique induces a RND estimate which is interesting on its own right and serves as a basis for further analysis of derivatives prices. Namely, using the distribution matching technique in reverse with estimated state prices as an input one obtains ’Implied Physical Distributions’, generalizing implied volatility. Recall in this connection the well-known Recovery Theorem of Ross (2015).

In case the asset to be priced is essentially a derivative on the market index in a representative agent model, then the Lucas (1978) first order condition can in principle be applied in pricing the asset. However, this requires the knowledge of the exact form of the representative utility function. In practice there are some problematic issues with this approach. For instance, the Equity Premium Puzzle by Mehra and Prescott (1985) involves risk aversion constants in CRRA utility functions which are higher than anticipated by behavioral empirical studies. Even worse, Bakshi et al. (2010) observe that some empirically observed pricing kernels, which should coincide with marginal utility in respective states at the equilibrium, implies that the corresponding utility function should strongly fail to be concave. Therefore flexible calibration techniques are required instead.

One is tempted simply using the Lucas first order condition anyway, outside the equilibrium framework, with a model- pricing kernel , say of a BSM model. Namely, in some frameworks under equilibrium prices one may equate a marginal utility up to scaling, see Aït-Sahalia and Lo (2003), Breeden and Litzenberger (1978). Therefore it seems promising to analyze the expectation

However, this does not result in the correct BSM model- risk-neutral value of the option, , even if the states formally coincide, . See Example 7.1. The point is that and changing the market’s physical distribution affects the equilibrium as well, even if risk preferences remain the same. Instead, the risk-neutral measures must be reconciled more carefully. Theorem provides an interpretation for the state space transformation investigated here. The transform may reflect a Girsanov style change of dynamics between risk-neutral processes.

We discussed distribution matching both with SPDs and RNDs. The former is mildy simpler. The latter is more flexible in the sense that the compared pricing models may then have different short rates or discounting terms. This may be a useful feature if the short rates in the models must be adjusted such that the resulting market prices of risk coincide.

Here we were working essentially with one market index only. Relying on an analogy where the version of the technique investigated here corresponds to CAPM, one may ask about a multifactor case, in the spirit of the APT. Thus, future work may include extending the pricing technique to a multidimensional state price density, where the dimensions may correspond to macroeconomical indicators. Other future work may include more generally differential asset pricing, where there is a benchmark state price density available. These may include corporate bonds with respect to stocks and government bonds, index options with respect to other highly correlated index options (e.g. SP100 vs. SP500), and commodity derivatives with respect to related commodity derivatives.

References

- [1] Andersen, T. G., Fusari, N. Todorov, V. : Parametric inference and dynamic state recovery from option panels, Econometrica 83, 1081–1145 (2015)

- [2] Airoldi, M. : A moment expansion aprroach to option pricing, Quantitative Finance, 5, 89–104 (2005)

- [3] Aït-Sahalia, Y., Lo, A. : Nonparametric estimation of state-price densities implicit in financial asset prices, The Journal of Finance, 53, 499–547 (1998)

- [4] Aït-Sahalia, Y., Lo, A. , Nonparametric Risk Management and Implied Risk Aversion, Journal of Econometrics 94, pp. 9–51 (2000)

- [5] Aït-Sahalia, Y., Duarte, J. : Nonparametric option pricing under shape restrictions, Journal of Econometrics, 116, 9–47 (2003)

- [6] Arrow, K.J., Debreu, G. : Existence of an Equilibrium for a Competitive Economy, Econometrica, 22, 265–290 (1954)

- [7] Atlan M., Geman H., Madan D.B., Yor M. : Correlation and the pricing of risks, Annals of Finance, 3, 411–453 (2007)

- [8] Bakshi, G., Cao, C. and Chen, Z. : Empirical Performance of Alternative Option Pricing Models. The Journal of Finance, 52, 2003–2049 (1997)

- [9] Bakshi, G., Kapadia, N. , Madan, D.B. : Stock return characteristics, skew laws, and differential pricing of individual equity options, Review of Financial Studies, 16, 101–143 (2003)

- [10] Bakshi, G., Madan, D., Panayotov, G. : Returns of claims on the upside and the viability of U-shaped pricing kernels, Journal of Financial Economics, 97, 130–154 (2010)

- [11] Beiglböck, M., Muhle-Karbe, J., Temme, J. : Utility maximization, risk aversion, and stochastic dominance, Mathematics and Financial Economics 6, 1–13 (2012)

- [12] B.K. Beare : Measure preserving derivatives and the pricing kernel puzzle, Journal of Mathematical Economics, 47 (2011), 689–697.

- [13] Bick, A. : Comments on the valuation of derivative assets, Journal of Financial Economics, 10, 331–345 (1982)

- [14] Brigo, D., Mercurio, F., Rapisarda, F., Scotti, R. : Approximated moment-matching dynamics for basket-options pricing, Quantitative Finance, 4 , 1–16 (2004)

- [15] Breeden, D.T., Litzenberger, R. H. : Prices of State-Contingent Claims Implicit in Option Prices, The Journal of Business, 51, 621–651 (1978)

- [16] Brown, D.J., Ross, S.A. : Spanning, valuation and options, Economic theory, 1, 3–12 (1991)

- [17] Buchen, P.W., Kelly, M. : The maximum entropy distribution of an asset inferred from option prices, Journal of Financial and Quantitative Analysis, 31, 143–159 (1996)

- [18] Carr, P., Chou, A. : Breaking Barriers, Risk, 10, 139–145 (1997)

- [19] Chalamandris, G., Rompolis, L. : Exploring the role of the realized return distribution in the formation of the implied volatility smile, Journal of Banking and Finance, 36 , 1028–1044 (2012)

- [20] Chateauneuf, A., Kast, R., Lapied, A. : Choquet pricing for financial markets with frictions, Mathematical Finance, 6, 323–330 (1996)

- [21] Chernov, M., Ghysels, E. : A study towards a unified appraoch to the joint estimation of objective and risk neutral measures for the purpose of options valuation, Journal of Financial Economics, 56, 407–458 (2000)

- [22] Cochrane, J.H. : Asset Pricing, Princeton University Press (2005)

- [23] Corrado, C.J., Su, T. : Implied volatility skews and stock return skewness and kurtosis implied by stock option prices European, Journal of Finance, 3 , 73–85 (1997)

- [24] Corrado, C. : The hidden martingale restriction in Grahm-Charlier option prices, The Journal of Futures Markets, 27, 517–534 (2007)

- [25] Derman, E., Ergener, D., Kani, I. : Static Options Replication, Journal of Derivatives, 2, 78–95 (1995)

- [26] Dybvig, P.H. : Distributional Analysis of Portfolio Choice, Journal of Business, 61, 369–393 (1988).

- [27] Dybvig, P.H. : Inefficient dynamic portfolio strategies or how to throw away a milloin dollars in the stock markets. Review of Financial Studies, 1, 67–88 (1988).

- [28] Engle, R., Figlewski, S. : Modeling the Dynamics of Correlations among Implied Volatilities, Review of Finance, 19, 991–1018 (2015)

- [29] Fengler, M. : Semiparametric modeling of Implied Volatility, Springer (2005)

- [30] Föllmer, H., Schied, A. : Stochastic finance : an introduction in discrete time, De Gruyter (2011)

- [31] Glasserman, P. : Monte Carlo methods in financial engineering. Springer-Verlag (2003)

- [32] Ghoussoub, N., Moameni, A.: Optimal mass transport and symmetric representations of their cost functions, Mathematics and Financial Economics 8, 435–451 (2014)

- [33] Halperin, I., Itkin, A. : Pricing options on illiquid assets with liquid proxies using utility indifference and dynamic-static hedging, Quantitative Finance, 14, 427–442 (2014)

- [34] Henry-Labordere, P.: Model-free Hedging: A Martingale Optimal Transport Viewpoint, Chapman and Hall/CRC Financial Mathematics Series (2017)

- [35] Hocquard, A., Papapgeorgiou, N., Remillard, B. : The payoff distribution model: an application to dynamic portfolio insurance, Quantitative Finance, 15, 299–312 (2015)

- [36] Jackwerth, J.C., Rubinstein, M. : Recovering probability distributions from option prices, The Journal of Finance, 51, 1611–1631 (1996)

- [37] Jaeckel, P. : Monte Carlo methods in finance. John Wiley and Sons (2002)

- [38] Jarrow, R. A. : A characterization theorem for unique risk neutral probability measures, Economics Letters, 22, 61–65 (1986)

- [39] Jarrow, R., Rudd, A.: Approximate option valuation for arbitrary stochastic processes, Journal of Financial Economics, 10, 347–369 (1982)

- [40] Jondeau, E., Poon, S.H., Rockinger, M. : Financial Modeling under Non-Gaussian Distributions, Springer (2007)

- [41] Kantorovich, L.: On the translocation of masses. C.R. (Doklady) Acad. Sci. URSS (N.S.), 37, 199–201 (1942)

- [42] Knight, J., Satchell, S. : Pricing derivatives written on assets with arbitrary skewness and kurtosis. In Return Distributions in Finance (2000)

- [43] Longstaff, F. : Option pricing and the martingale restriction, Review of Financial Studies, 8, 1091–1124 (1995)

- [44] Lucas, R.E.: Asset Prices in an Exchange Economy, Econometrica 46, 1429–1445 (1978)

- [45] Madan, D. : Equilibirium asset pricing: with non-Gaussian factors and exponential utilities, Quantitative Finance, 6, 455–463 (2006)

- [46] Madan, D., Carr, P. Chang, E. : The Variance Gamma Process and Option Pricing, European Finance Review, 2, 79–105 (1998)

- [47] Madan, D., Milne, F. : Contingent claims valued and hedged by pricing and investing in a basis, Mathematical Finance, 4, 223–245 (1994)

- [48] Mehra, R., Prescott E.C.: The Equity Premium: A Puzzle, Journal of Monetary Economics. 15 145–161 (1985)

- [49] D.C. Nachman, Spanning and completeness with options, Rev. Financ. Stud. 1 (1988), 311–328.

- [50] Reichlin, C.: Utility Maximization with a Given Pricing Measure When the Utility Is Not Necessarily Concave, Mathematics and Financial Economics, 7, 531–556 (2013)

- [51] Rieger, M. : Co-monotonicity of optimal investments and the design of structured financial products, Finance and Stochastics 15, 27–55, (2011)

- [52] Ross, S. : The Recovery Theorem, The Journal of Finance, LXX, 615–648 (2015)

- [53] Rubinstein, M. : An aggregation theorem for securities markets, Journal of Financial Economics, 1, 225–244 (1974)

- [54] Rubinstein, M. : Implied Binomial Trees, The Journal of Finance, 49, 771–818 (1994)

- [55] Rubinstein, M. : Edgeworth binomial trees, The Journal of Derivatives, 5, 20–27 (1998)

- [56] Shreve, S.E., Stochastic calculus for finance II, Springer (2004)

- [57] Simonato, J.-G. : Johnson binomial trees, Quantitative Finance, 11, 1165–1176 (2011)

- [58] Song, Z., Xiu, D. : A tale of two option markets: Pricing kernels and volatility risk, Journal of Econometrics, 190, 176–196 (2016)

- [59] Stutzer, M. : A simple nonparametric approach to derivative security valuation, The Journal of Finance, 51, 1633–1652 (1996)

- [60] Svetlozar, R., Ruschendorf, L. : Mass Transportation Problems: Volume I: Theory. Springer (1998)

- [61] Trigeorgis L.,: Real Options: A Primer, Kluwer Academic Publishers, Boston (1999)

Appendices

Appendix A Proofs

We will give sketches of proofs retaining the notations and assumptions appearing in the statements.

Proof of Proposition 5.1.

For each let and be increasing partitions of the supports of and (possibly with ) such that

for all .

It follows from the properties of that as . By compactness considerations we observe that

exists and is non-zero. Therefore the function

defined on is uniformly continuous. This means that

| (A.1) |

for .

Note that by the integrability of we have that

as for every (including cases ).

Since is integrable and bounded, we have by (A.1) that

and

from which the claim follows. ∎

Proof of Proposition 5.2.

Observe that is necessarily an identical mapping and for -a.e. . By using the definition of (the absence of) arbitrage we obtain that

∎

Proof of Proposition 5.3.

We will follow the finite approximation of the portfolios as follows. Let , and be increasing sequences of such that for each . Then by the assumption. Thus

| (A.2) |

∎

Proof of Proposition 5.4.

Indeed, let . We will apply (4.4). We will compare the values

Since we are dealing with pricing measures we may restrict to analysing intervals of the form where . Fix . By using the unimodality of and the selection it follows that there is an upper bound for on the interval such that

since in the -mean. The argument is finished by using the fact that as . ∎

Proof of Proposition 5.5.

It follows from the assumptions that we may consider . Then

This is the risk-neutral price of the contingent claim with payoff . ∎

Proof of Theorem 7.2.

According to the previous lemma we see that the states and , written in an increasing order and with , have equal probabilities:

Therefore the assumption regarding the convergence of the discretized versions of yield with an easy approximation argument that

for each where is the -state-to--state binding map appearing in the definition of .

What remains to be verified is that the following holds:

| (A.3) |

for all . Note that then

Recall the simple well-known equalities of discounted risk-neutral probabilities in a single-step model (see e.g. Föllmer and Schied (2011)):

Consider the discounted price processes of the securities

and their binomial counterparts. Denote . Then in the binomial discrete models for the single-step subtrees have the same risk-neutral probabilities. Indeed, in the discounted world the risk-neutral terms corresponding to , and become

and

respectively. We use arrows to indicate the change of a state. Thus

Consequently, under the assumption on coinciding local market prices of risk we obtain that

We conclude that the binomial trees corresponding to the assets are isomorphic to that of , since the orders are preserved, and, moreover, both the physical probabilities and state prices of the corresponding nodes coincide. This means that

for the mutually corresponding terminal node state values and (in the trees of the respective models) for each . A straight-forward approximation argument then yields the claim that (A.3) holds and this finishes the proof. ∎