Exact and Approximate Hidden Markov Chain Filters Based on Discrete Observations

Abstract

We consider a Hidden Markov Model (HMM) where the integrated continuous-time Markov chain can be observed at discrete time points perturbed by a Brownian motion. The aim is to derive a filter for the underlying continuous-time Markov chain. The recursion formula for the discrete-time filter is easy to derive, however involves densities which are very hard to obtain. In this paper we derive exact formulas for the necessary densities in the case the state space of the HMM consists of two elements only. This is done by relating the underlying integrated continuous-time Markov chain to the so-called asymmetric telegraph process and by using recent results on this process. In case the state space consists of more than two elements we present three different ways to approximate the densities for the filter. The first approach is based on the continuous filter problem. The second approach is to derive a PDE for the densities and solve it numerically and the third approach is a crude discrete time approximation of the Markov chain. All three approaches are compared in a numerical study.

keywords:

Hidden Markov Model, Discrete Bayesian Filter, Wonham Filter, Asymmetric Telegraph process1 Introduction

We consider a Hidden Markov Model (HMM) where the integrated continuous-time Markov chain can be observed at discrete time points perturbed by a Brownian motion. The aim is to derive a filter for the underlying continuous-time Markov chain. Thus, we have a continuous-time Hidden Markov Model with discrete observations. Models of this type are widely used in finance, in telecommunication or in biology. For references, we refer to the examples in Section 2. The knowledge of the filter is for example necessary in case one has to control the system in a dynamic way. Usually the principle of estimation and control is valid and implies that the filter has to be computed first and then the control is applied, see e.g. Bayraktar & Ludkovski (2009); Rieder & Bäuerle (2005); Sass & Haussmann (2004) for different kinds of applications. We assume that all parameters of the model are known or have been estimated before. In particular we assume that the number and values of the states of the hidden Markov chain are known. As far as model selection is concerned we refer e.g. to Frühwirth-Schnatter (2001); Otranto & Gallo (2002); Dannemann & Holzmann (2008). Papers dealing with the estimation of state values and transition intensities are e.g. Rydén (1996); Elliott et al. (2008); Hahn & Sass (2009); Hahn et al. (2010). Since we assume a finite number of states for the Markov chain, the filter has a finite dimension and it is in principal clear form the existing theory how to construct it. However, the filter recursion involves densities which are difficult to compute explicitly.

We rely on results from López & Ratanov (2014) and Di Masi et al. (1994) on the asymmetric telegraph process to obtain the exact filter in closed form in case the hidden Markov chain has only two states. We distinguish between the symmetric case, where the switching intensities are the same for both states and the asymmetric case where intensities are different. The first case is easier and related to the well-known telegraph process. The second problem is related to the asymmetric telegraph process. Estimates for the switching intensity of a symmetric telegraph process have e.g. been derived in Yao (1985), Iacus & Yoshida (2008) and for an inhomogeneous telegraph process in Iacus (2001).

In the general situation with more than two states, the required densities become rather complicated. So a procedure to compute these densities approximately is called for. We present three different ways to derive approximations. All three approaches are general and need no information about the size of the intensities, i.e. how fast the hidden Markov chain switches. Of course the faster the switching of the Markov chain, the harder it is to obtain a reasonable filter, given a fixed time lag between observations. If the switching intensity is too large compared to the observation time lag, the stationary distribution is a reasonable approximation. The first approach relies on results in Platen & Rendek (2010); Kloeden et al. (1993) where the authors derive an approximate continuous-time filter. When this continuous-time filter is discretized, it can also be used by someone who is only able to observe the data in discrete time. However, this approach is based on an assumption which is not true in general. The second approach is to derive a PDE for the densities which are involved in the filter process and to solve this PDE numerically. This approach is exact up to the error of the numerical PDE solution. The third attempt relies on a naive approximation of the continuous-time Markov chain by a discrete-time Markov chain. The finer the approximation, i.e. the smaller the time step of the discrete-time Markov chain, the better the approximate filter but the higher the computational effort.

Our paper is organized as follows: The next section contains a precise mathematical formulation of the problem and derives the basic filter recursion. Section 3 is then devoted to the problem with two states. Results about the telegraph process are used to derive the filter explicitly in both the symmetric and the asymmetric case. The following section considers the general problem and three approximate filters are derived. The last section is devoted to numerical results. In particular we compare our approximate filters in a setting with five states in situations with frequent or rare observations and with small or large variability of the error terms.

2 Hidden Markov Chain Filters

Suppose we have a filtered probability space with and a hidden stationary continuous-time Markov chain on it with finite state space and . The intensity matrix of this process is given by and the initial distribution by . Let us denote by the distribution of for , then satisfies the ODE

| (2.1) |

with . The formal solution of (2.1) is given by

where

is the matrix exponential. Moreover, the -step transition probabilities are given by

| (2.2) |

Now assume further that is a Brownian motion on our filtered probability space which is independent of the hidden continuous-time Markov chain and plays the role of a noise. Moreover, are different real numbers and . We assume that we can observe the process

| (2.3) |

at discrete time points for , and , i.e. the observation -algebra at time is given by

as opposed to the filtration which contains both the information about and . A simple interpretation of this model is as follows: Suppose a particle is moving on the real line, starting in zero. The velocity of the particle at time is determined by . Thus, gives the exact position of the particle at time . However, we are only able to observe the position at discrete time points together with a noise . The aim is now to filter from this observation the current velocity of the particle, i.e. to determine

where is given. It is well-known that we can derive a recursive filter formula with the help of Bayesian analysis which is given by

| (2.4) |

where is the density of the conditional distribution of given and is the density of the conditional distribution of given and , see e.g. Elliott et al. (1995), chapter 2, Fristedt et al. (2007) chapter 3 and Bäuerle & Rieder (2011) chapter 5, i.e.

Obviously by conditioning we have the relation

| (2.5) |

Thus, it is in principle enough to derive the densities from which we obtain .

In case consists of two elements only, we will derive explicit expressions for and in the next section. For general we derive approximate expressions in section 4.

Let us also shortly mention the situation when we have continuous observations. In this case the observation filtration is given by

and we have to determine

This is the well-known Wonham filter problem. From the Kallianpur-Striebel formula we have the following representation

| (2.6) |

where satisfies the Zakai equations

| (2.7) |

for where is a diagonal matrix with elements on the diagonal (see e.g. Platen & Rendek (2010)). Obviously, this filter makes use of a continuous observation of . However, we will later see that approximations of this filter at time t may only depend on which allows us to use this filter in case of discrete observations, too.

Applications of this model are given next.

[0.2cm]

Example 1: Financial data suggest that parameter of asset prices depend on external macroeconomic factors which may be described by a continuous-time Markov chain (cp. Rydén et al. (1998)). A popular model for example is to take the classical Black Scholes model with parameters driven by a factor processes which is represented by a continuous-time Markov chain. Thus, the log-return of an asset price at time would be

where is a Brownian motion independent of , is the drift or appreciation rate and is a fixed volatility. The parameter may also depend on . Models where the factor process is assumed to be known are among others treated in Di Masi et al. (1994); Bäuerle & Rieder (2004); Yin & Zhou (2004); Costa & Araujo (2008); Zhang et al. (2010). If is not observable and constant we have exactly the generic situation which we consider in this paper. The model is then reasonably described by an HMM or Markov switching models for price parameters. The aim is to filter the underlying economic factor. For applications of this model see Sass & Haussmann (2004); Rieder & Bäuerle (2005); Hahn & Sass (2009); Sass & Wunderlich (2010); Bäuerle et al. (2012); Frey et al. (2012). In this case it is often only possible to observe the log-return, i.e. the integrated HMM at discrete time points. For example some asset prices are only quoted on a daily basis.

[0.4cm]

Example 2: In communication networks, information arrives to a multiplexer, switch or information processor at a rate which changes randomly and often shows a high degree of correlation in time. For example Heffes & Lucantoni (1986) modeled the input stream of a statistical multiplexer consisting of a mix of data and packetized voice sources as a Markov-modulated Poisson process. In Stern & Elwalid (1991) the authors used a Markov-modulated continuous flow model for the information stream at a multiplexer and analyzed the system performance. These and other findings fostered the investigation of so-called fluid queues, see e.g. Kulkarni (1997). A more recent reference is Rabehasaina & Sericola (2004) where the authors are interested in the stationary queueing level of a fluid queue whose buffer content evolution process is given by the SDE

Here again, if one is able to observe, perturbed by an error, the amount of fluid which came in, then the filter computes the distribution of the current inflow rate. Such fluid queues can also be used to model production processes.

3 HMM problem with two states

3.1 Symmetric -matrix

In case the state space consists of two elements only, i.e. and the intensities are symmetric, i.e.

| (3.1) |

with , the model can be reduced to the so-called telegraph process. The telegraph process is given by

| (3.2) |

where is a Poisson process with intensity . The telegraph process has been introduced by Kac in lecture notes from 1956, see also Kac (1974). It has been generalized in different ways and studied in various applications. For a recent paper with many references see López & Ratanov (2014). One usually distinguishes the symmetric case where the particle moves with symmetric velocities and and switches the direction with same intensity and the asymmetric case where we have different arbitrary velocities and different switching intensities.

Now let us denote

| (3.3) |

and define and . Then, given for we have

| (3.4) |

i.e. is linear transformation of . The transition probabilities in (2.2) in this case simplify to

| (3.5) |

It is now possible to derive explicit formulas for the densities . which appear in the filter formula (2.4). The density for the telegraph process at time , given the initial state can already be found in the appendix of Di Masi et al. (1994). In order to derive the densities for our application, let us introduce the following notations. The modified Bessel functions are given by

| (3.6) |

and we denote the density of the normal distribution with zero expectation and standard deviation by

Then we obtain:

Theorem 3.1.

The density of given for is

with

The density of given is

with

The density of given with and is

with

A proof of this statement can be found in the appendix.

3.2 Non-symmetric matrix

In this section we again assume that the state space consists of two elements only, i.e. but the transition intensities are arbitrary, i.e. . The transition probabilities in (2.2) are now given by

| (3.7) | |||||

| (3.8) |

In this case we interpret in (3.2) as the asymmetric telegraph process. This means that

where now

is the number of state transitions in of the Markov chain . Again explicit formulas for the densities , can be derived. The density of given has been obtained in Di Masi et al. (1994) by using the Girsanov theorem for point processes. In López & Ratanov (2014) the authors use a differential equations approach. For our situation we get (w.l.o.g. we assume in the next theorem that the initial state is ):

Theorem 3.2.

The density of given is

with

The density of given is for

with

The density of given is

with

The proof can again be found in the appendix.

4 Approximate filter for more states

Using the methods of the preceding section it is in principle possible to derive filters if consists of more than two states. However, formulas get quite complicated, in particular when the state space is large. Instead we try to derive approximate filters in this case. The first approach is based on the continuous filter obtained by (2.6) and (2.7).

4.1 Approach via continuous filter

In Platen & Rendek (2010); Kloeden et al. (1993) the solution of the Zakai equation (2.7) which is a homogeneous linear Itô SDE, is discussed. If the matrices and (recall that is the diagonal matrix with elements on the diagonal) commute, i.e. if then an explicit solution of (2.7) would be

| (4.1) |

However this is not true if the matrices do not commute, but still the expression can serve as an approximate filter, see Platen & Rendek (2010); Kloeden et al. (1993). Note that this solution only involves and not the path of the process and is thus also feasible for a filter with discrete observations. We will use (2.6) and (4.1) as one approximation for our discrete filter in Section 5. Since this approach relies on an assumption which is not valid in general it is not possible to show any kind of convergence of this approximation scheme. Alternatively, can be approximated by a discrete process using the Milstein scheme in order to solve the SDE in (2.7) numerically:

| (4.2) |

Here where as before. Again we see that this approximation only involves which can be observed in our situation, too and thus the approximate filter can also be used in the discrete setting. For (4.2) it is known that the continuous approximation which is obtained from converges with strong order to the true solution of (2.7) if the time step size of the discretization tends to zero. Moreover, this convergence is also true for the corresponding filter (see Platen & Rendek (2010) Theorem 4.1). Hence for frequent observations the approximation in (4.2) is supposed to work well in our setting. Note however, that a practical implementation of (4.2) requires some smoothing in order to avoid affects like getting negative.

4.2 Approach via PDEs

Here we derive a system of PDEs for the densities which appear in the filter (2.4). From we obtain the densities by (2.5). As soon as continuous-time Markov chains are involved it is a common tool to work with differential equations, see e.g. the system of ODEs for the probability distribution of a Markov chain (2.1) or the partial differential equation for the position of a particle given by the telegraph process, see Kac (1974). This equation is a hyperbolic second order differential equation and is known as the telegraph (or damped wave) equation. Partial differential equations for the densities of the telegraph process in the asymmetric case have been derived in López & Ratanov (2014).

In what follows define for , and the distribution

| (4.3) |

and the corresponding density by . By we denote the density of . Thus, we obviously have the following relation:

| (4.4) |

From we can compute immediately by convolution the required density for our filter using (2.3). Note that the density has an atom at of size where , since with probability no switch occurs in the time interval in which case .

We will now derive a PDE for by conditioning on what happens in the first time interval . We obtain

where is the transition probability of the embedded Markov chain given by

Rearranging terms and dividing by yields:

Now letting we obtain (note that the limit on the right hand side exists, hence also on the left hand side):

Applying the operator on both sides, we derive the following equation for the densities:

In matrix form this equations can be written as

| (4.5) |

where and is a diagonal matrix with on the diagonal. Moreover, we have the boundary conditions . This system of PDEs can then be solved numerically. The domain of is given by and . Outside the densities vanish. This approach is exact, however involves a numerical computation. One difficulty is the point mass which appears. However, the point mass is known and can be separated. More precisely, we know that where is smooth.

4.3 Approach via Discretization

Here we use a very simple approximation of the densities involved in the filter by discretizing the continuous-time Markov chain. More precisely, when we consider with , then we obtain a discrete-time Markov chain with transition matrix . Note that for either or for all . We assume that the latter case is valid for all . We can now approximate the random variable in (3.3) by

Since is finite, the random variable is obviously discrete and can only take a finite number of values. We denote by the finite set of all possible values. Furthermore, we denote a multi-index as a vector , where each , i.e. . For denote

Then we obtain

Thus, we can approximate the density of the distribution of given by

| (4.6) |

Analogously, for fixed and denote

Then we obtain

Thus, we can approximate the density of the distribution of given by

| (4.7) |

It is rather obvious that in this approach the approximate density converges against the exact one if .

5 Numerical Examples

This section illustrates the results presented in this work using some numerical examples. Basically, we consider two cases. First, we evaluate a scenario in which the underlying continuous time Markov chain has two states in order to provide an illustration comparing the exact filter to the approximations. Second, we consider a five state case. For application of the continuous filter (4.1), it is important to keep in mind, that the induced approximation error not only stems from the fact that the we have discrete measurements, but also from the fact that the considered matrices , and do not commute.

All examples were implemented using Matlab R2014a on a laptop with an Intel i7-2620M CPU and 8GB RAM. The system of PDEs (4.5) was solved using the algorithm proposed by Skeel & Berzins (1990), which is directly implemented in Matlab. From the solution , we derived using (4.4) Then, a numerical convolution procedure was performed for obtaining the values of the density on the grid points and was obtained using (2.5). Cubic interpolation was used for evaluating these densities at other points.

5.1 Two States Example

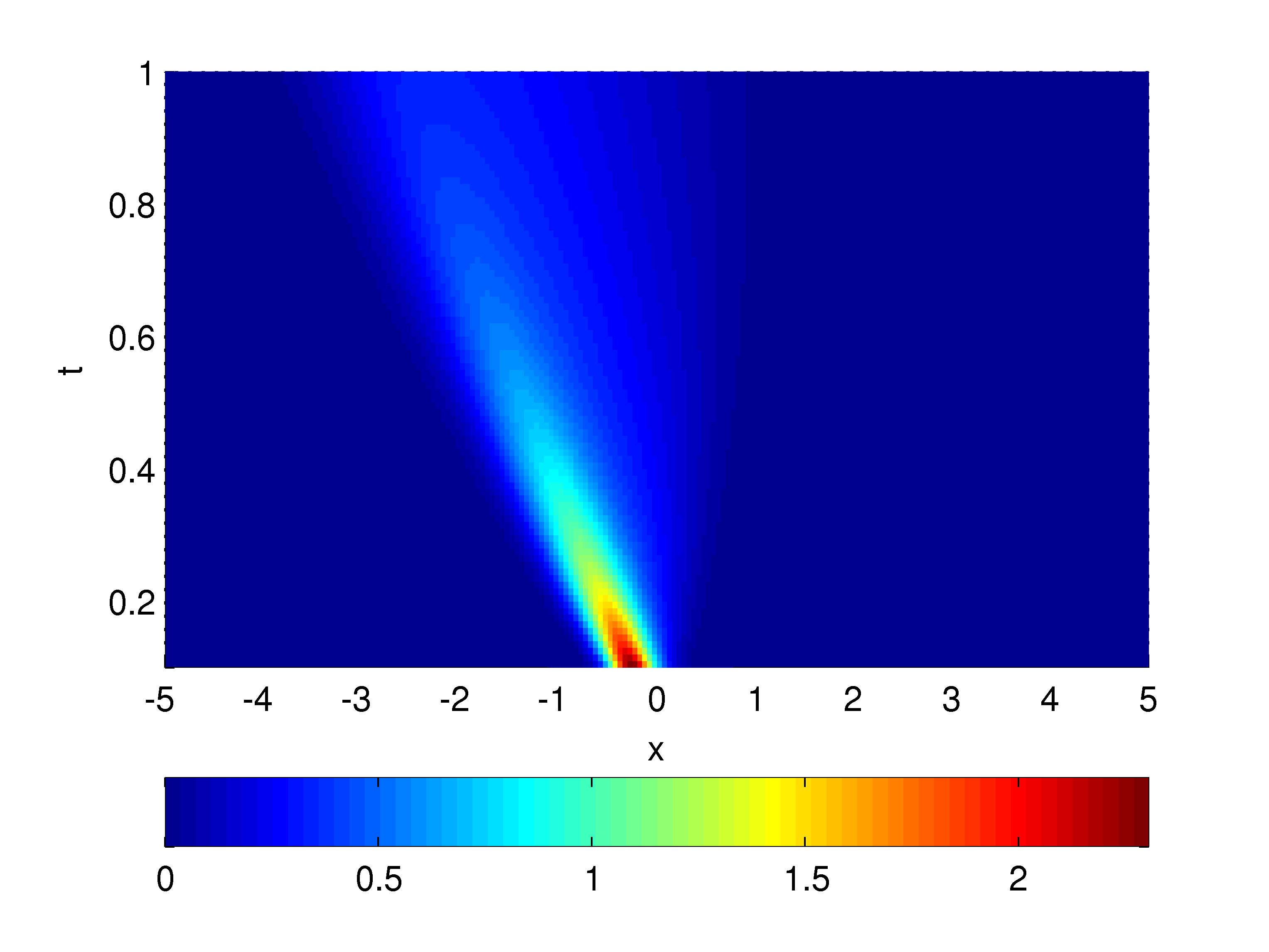

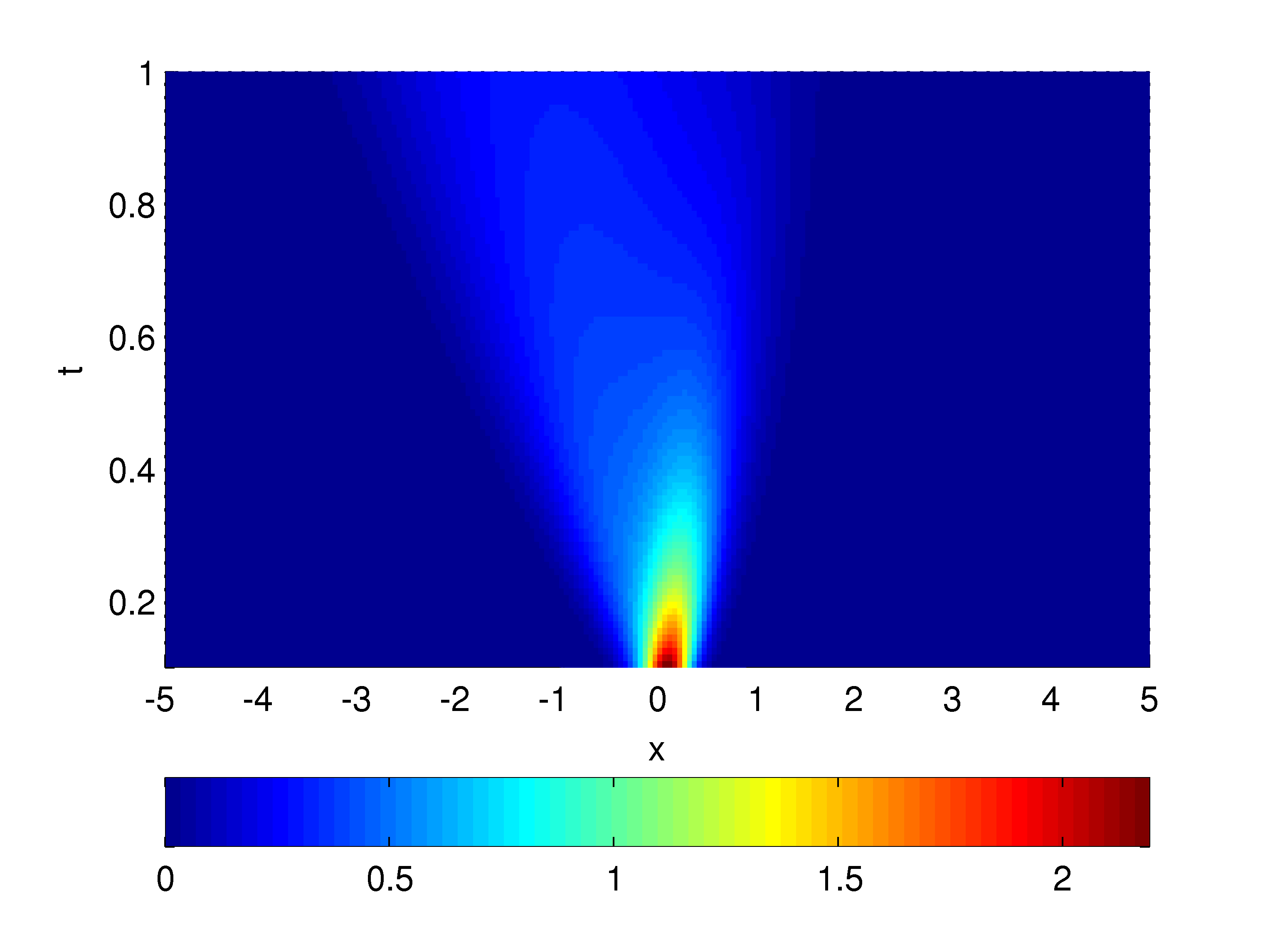

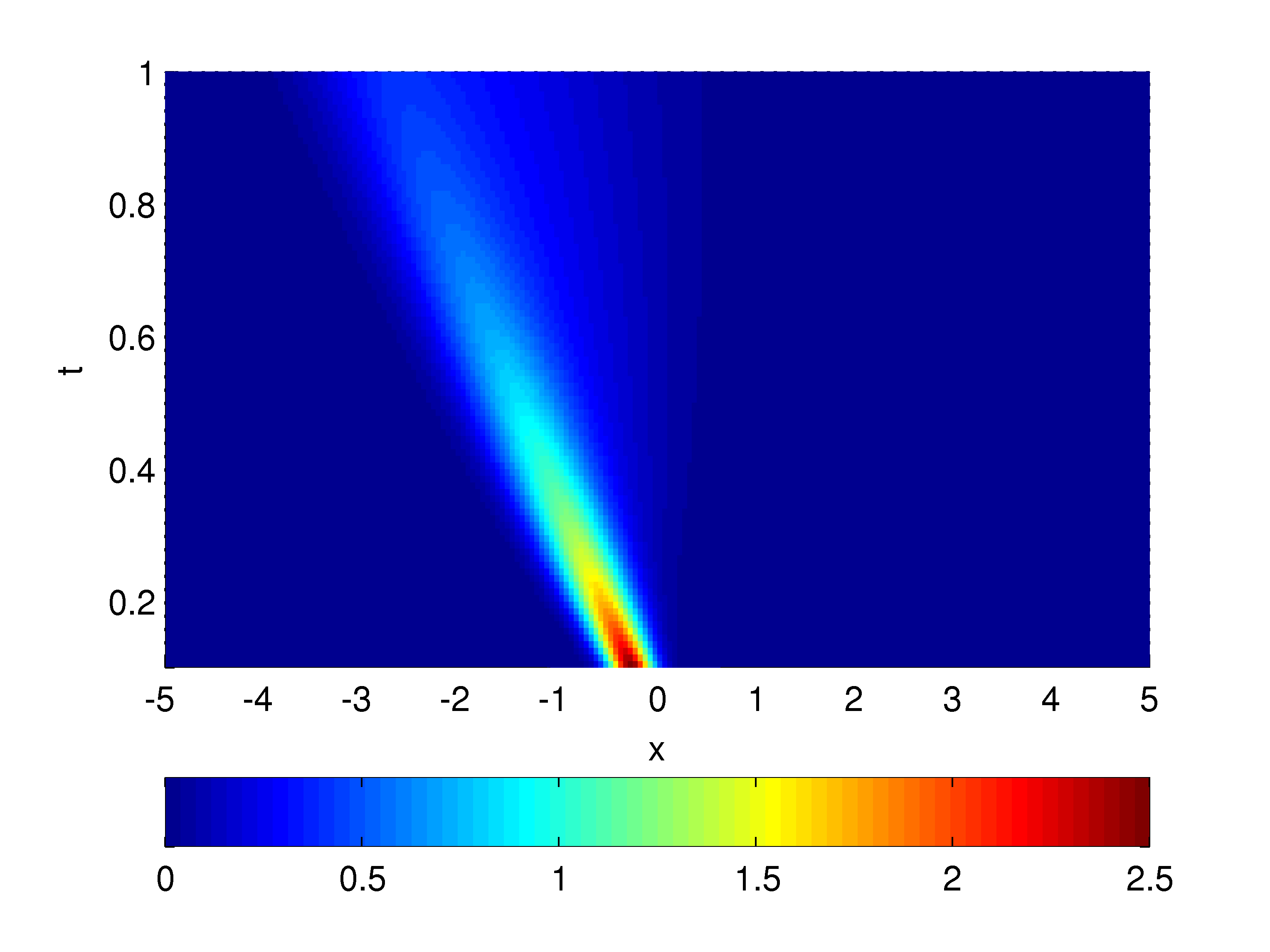

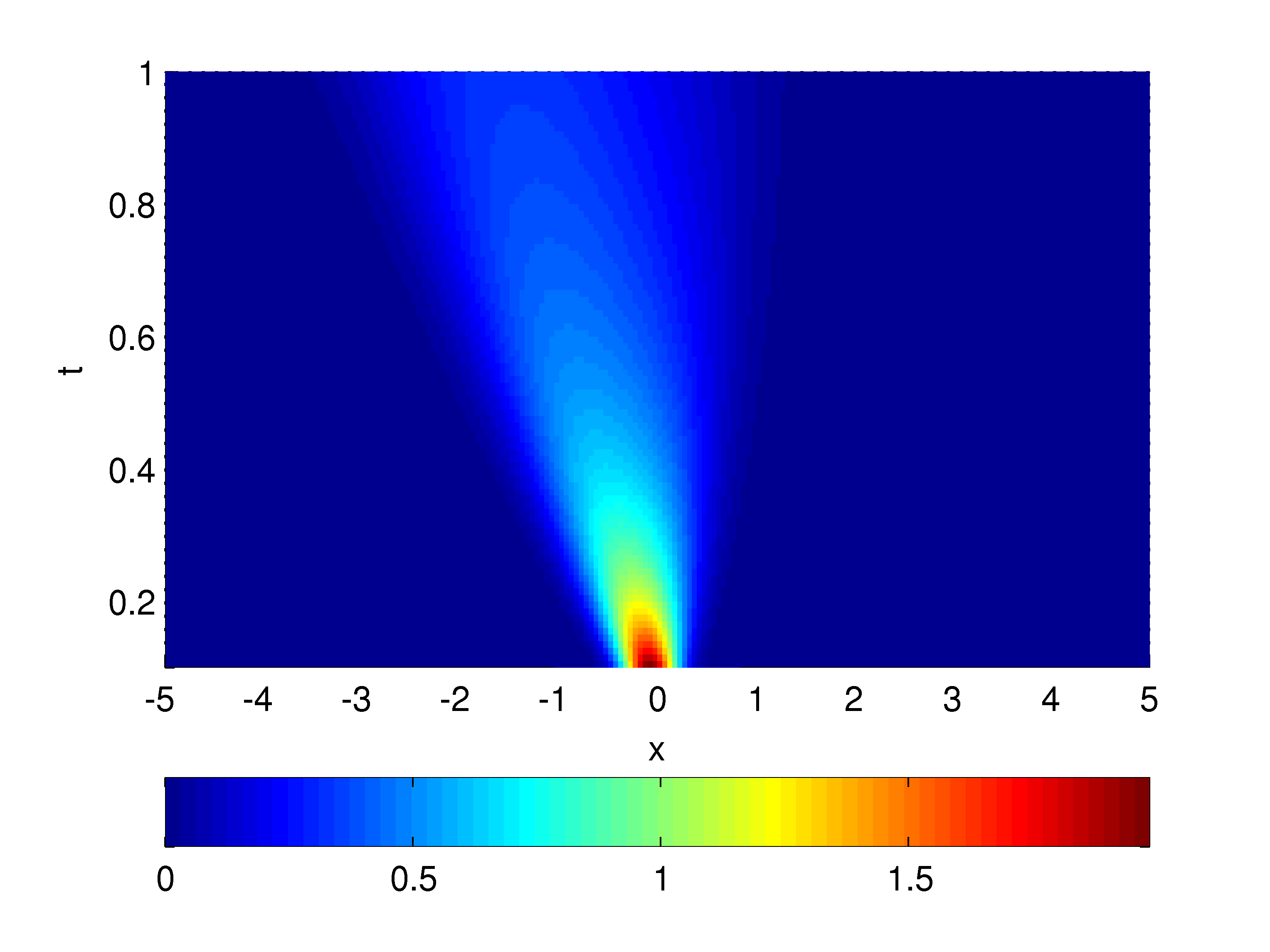

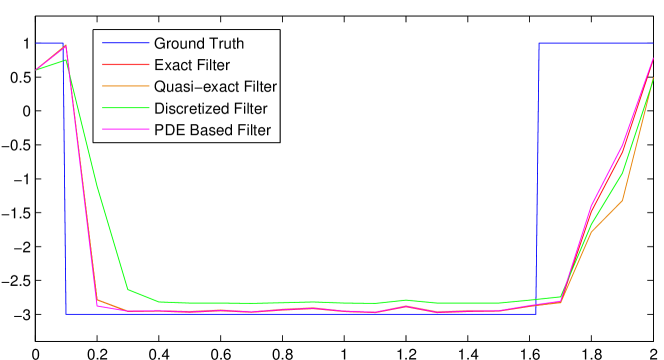

We consider the scenario , , , initial distribution of the continuous-time Markov chain , and intensity matrix

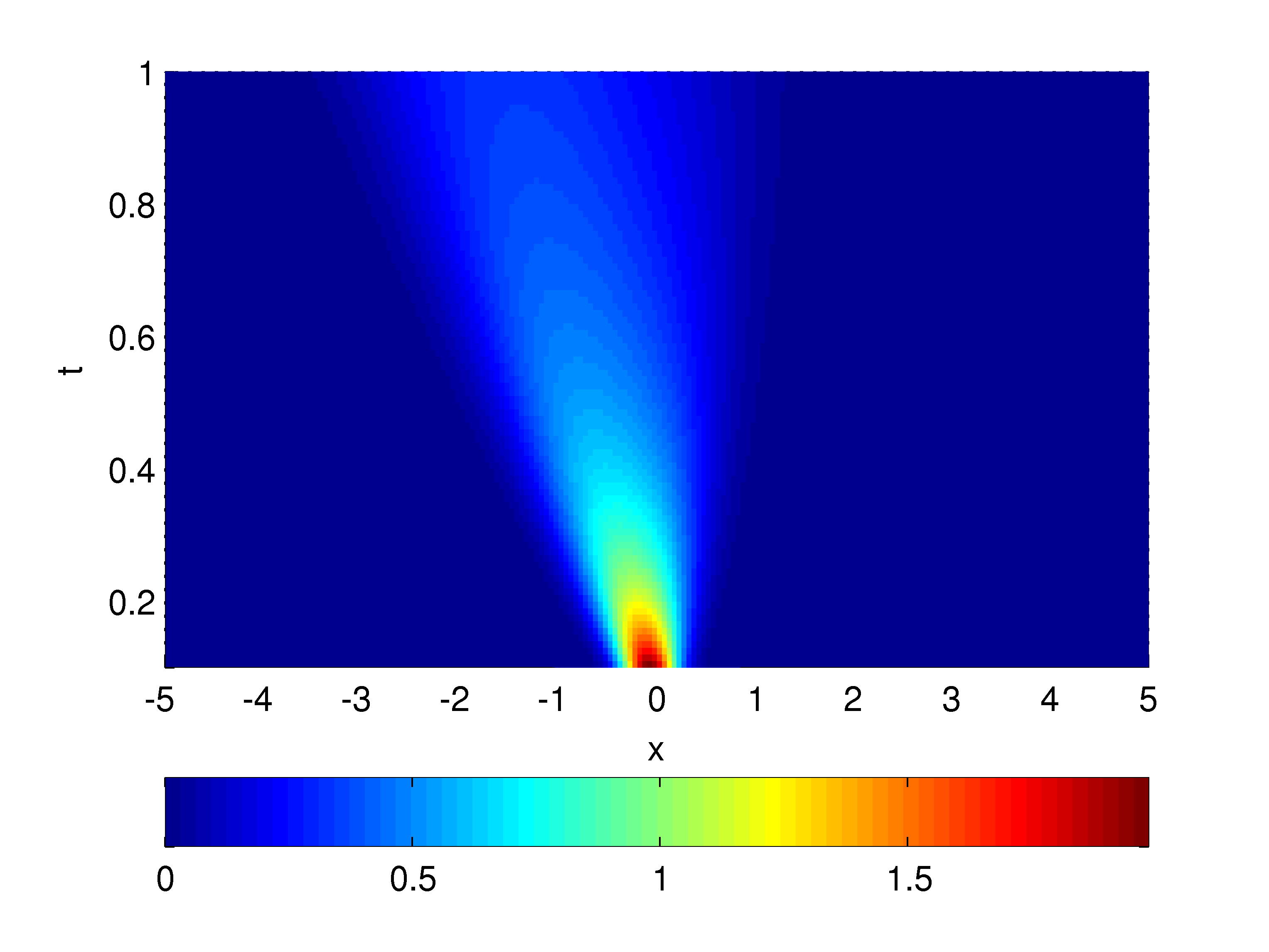

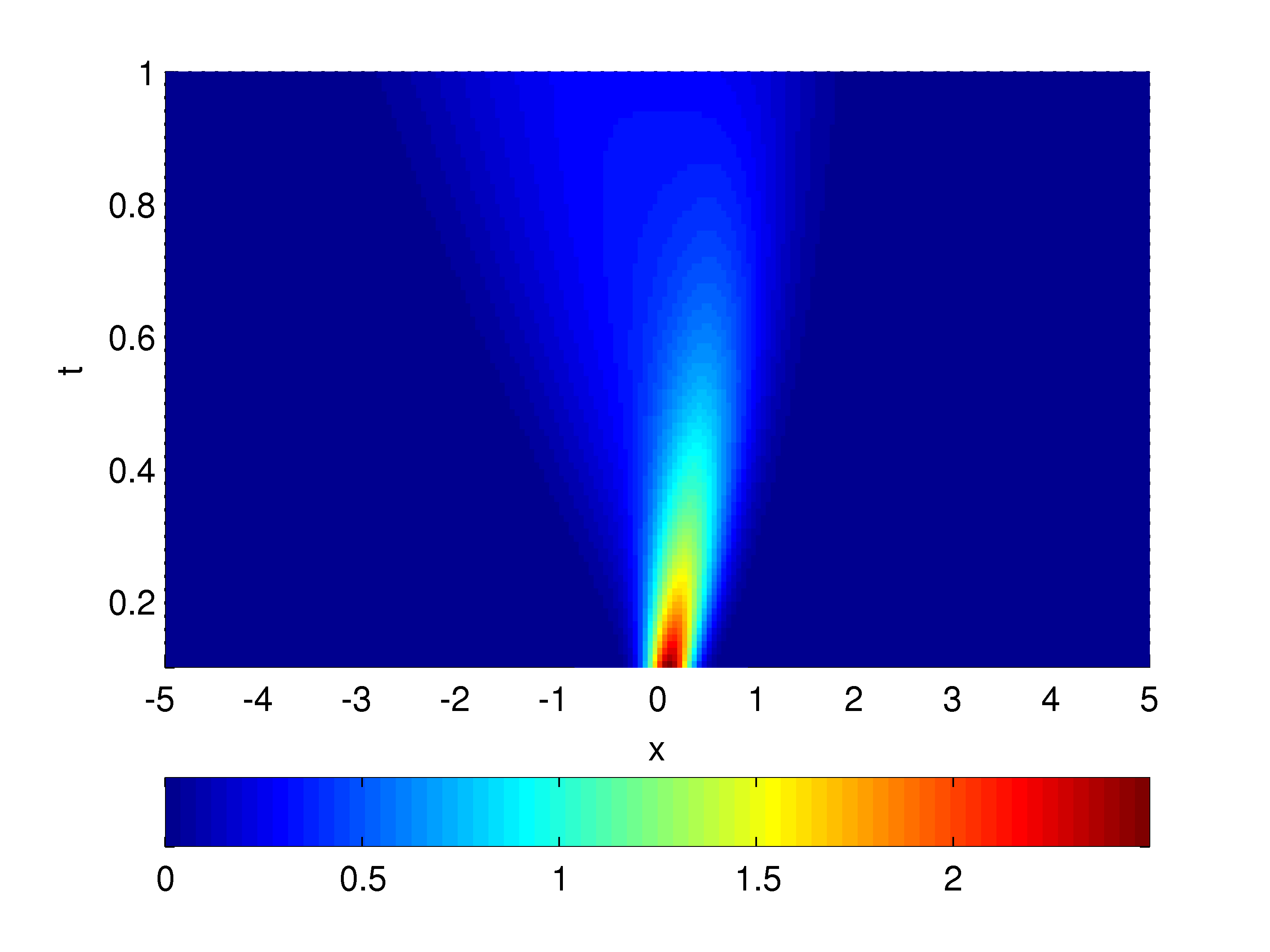

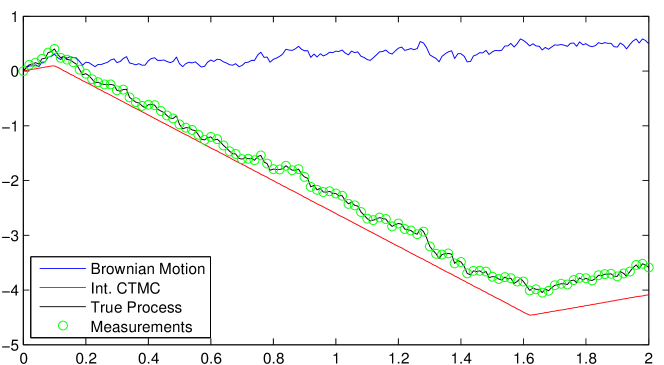

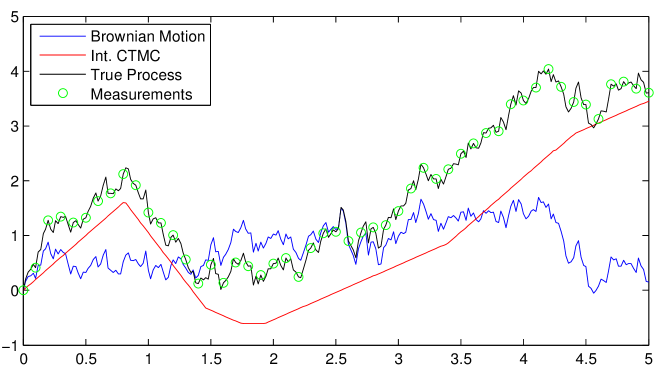

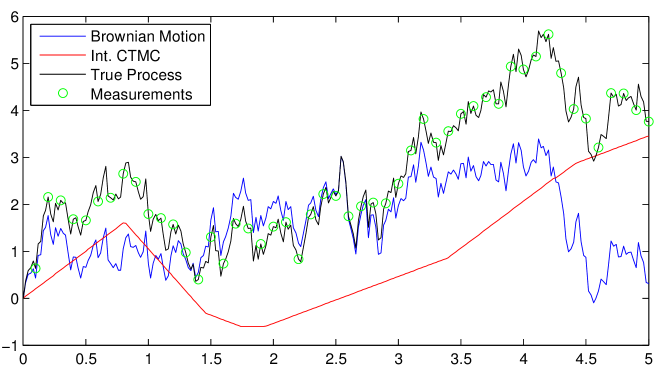

In fig. 1, we show the density of conditioned on the value of . In fig. 2, we show the density of conditioned on both, and . It can be seen that the additional restriction of has quite some impact on the shape of the density. For evaluation of the filters, the observed process was generated using 100 discretization points and 50 observations in each time step. Both, the process and its observations are shown in fig. 3

| Filter | Time |

|---|---|

| Exact | 248.53 |

| PDE Based | 3.32 |

| Discretized | 4.73 |

| Quasi-Exact | 0.18 |

| Filter | Time |

|---|---|

| Exact | - |

| PDE Based | 4.99 |

| Discretized | 171.48 |

| Quasi-Exact | 0.23 |

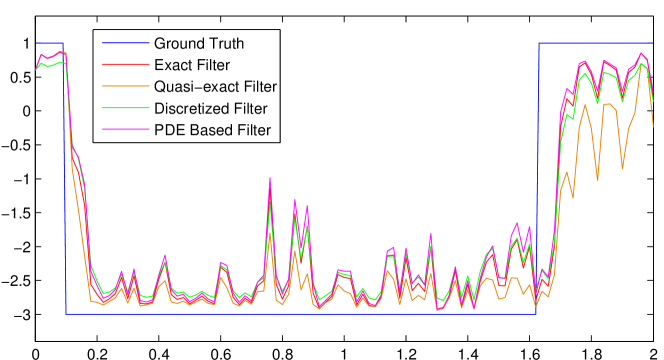

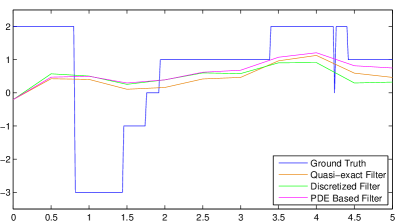

In fig. 4, we show filter results in terms of the expectation value of the true state. This is done for two scenarios. In the first case, every measurement is used. In the second case, only every fifth measurement is used. As expected, more frequent measurements result in a faster convergence of the estimate after a change of the underlying state. On the other hand, the filter with fewer observations is less sensitive to observed errors. The exact filter is almost indistinguishable from the PDE based approach. The time discretization based filter assumed the Markov process to perform at most one jump between each measurement, i.e., we used .

The computation time of the filters are given in table 1. The high computation time for the exact filter is due to the need for performing numerical integration in each filter step. The numbers of the PDE based filter do not include the time required for numerically solving the PDE, because the resulting solution is reused in every filter step, and thus, the impact on the average computation time depends on the number of performed filter steps. The PDE was solved on an equidistant grid on consisting of 3000 discretization points for 2000 equidistantly distributed time-points on .

5.2 Five States Example

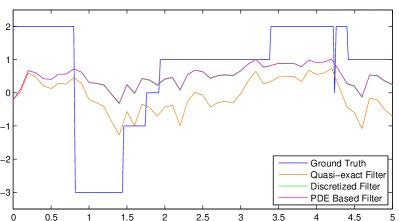

Now, we take a look at a more complex example where the (for ) are given by the values , , , , respectively. Furthermore, we used and

as initial distribution and intensity matrix. Two different diffusion parameters, and were considered in this example in order to observe the impact of on the quality of the filters. This time, we simulated 5 time steps with 50 discretization points and 10 observations per time step. The true process is shown in fig. 5.

The filter results are shown in fig. 6 (once again by showing the expectation value of the obtained distributions). For a high number of measurements, the PDE based filter is almost indistinguishable from the discretized filter (which uses 4 discretization cells here, i.e., ). This is due to the fact that the PDE based approach yields the exact density which is only corrupted by numerical errors induced from solving the PDE and by interpolation errors arising when evaluating the densities. Obviously, the expected number of jumps between two consecutive measurements decreases as the frequency of measurements goes up. Thus, in the considered scenario, the densities obtained from the discretization approach yield a good approximation of the exact density when every measurement is used. This approximation quality does not depend on the diffusion parameter . However, a larger results in less clear differences between all filtering approaches, because less information can be obtained about the underlying true state of the continuous time Markov chain.

Looking at the computation time in table 1 gives a somewhat different picture this time compared to the two states case. Once again, we only show the computation times of the run using every measurement and (it does not differ significantly for other runs). This time, the discretized filter requires a significantly higher amount of computation time. This is due to its recursive implementation and use of a higher number of discretization cells. However, this could also be optimized by obtaining the set and the densities and (according to (4.6) and (4.7) respectively) before the actual filter run. In that case, evaluation of these densities comes down to evaluating a precomputed Gaussian Mixture density.

6 Conclusion

In this paper we considered a Hidden Markov Model where the integrated continuous-time Markov chain can be observed at discrete time points perturbed by a Brownian motion. Using recent results on the asymmetric telegraph process, we derived exact formulas for a filter for the underlying continuous-time Markov chain, given this chain has only two different states. In case of more states we propose three approximate algorithms to compute the filter numerically. We investigated the performance of these filters with the help of two examples: one with two states and the other with five states. Problems like this arise for example when we have to filter the underlying economic state from observed asset prices.

Acknpwledgment

We would like to thank our student Fehmi Mabrouk for some initial work on this topic during his Diploma Thesis which encouraged us to further pursue this topic.

Appendix

Proof of Theorem 3.1: The density of the integrated telegraph process is given in Di Masi et al. (1994):

where is the Dirac-measure in point and

where the modified Bessel functions have been defined in (3.6). The density of given is then by the density transformation formula

Finally the density of given is obtained by the convolution formula

Thus, the first part of Theorem 3.1 is shown. Next we determine the density of given is even. From this we can compute as in the previous calculation. First note that

For the density of given is

see Lemma A.1 in Di Masi et al. (1994). Moreover we have

For the density of given has a point mass of one on , i.e. and . Altogether we obtain:

where

Next we determine the density of given is odd. For the density of given is

see Lemma A.1 in Di Masi et al. (1994). Moreover we have

Altogether we obtain:

Hence the density of given is again obtained by the density transformation formula

and finally the density of given is

Analogously we obtain the density of given with by

and the density of given is

Proof of Theorem 3.2: The density of the asymmetric telegraph process given is according to López & Ratanov (2014)

where is the Dirac-measure in point and

From this, the density of given follows as in the previous proof.

Next we have to determine the density of given . Note that we first have:

From (3.7) we obtain that

From the results in López & Ratanov (2014) we can derive . We have that

where

The density follows by joining the results.

We proceed similar for the density of given . Here we have

From (3.7) we obtain

and for the density of and given in the asymmetric case note that

Using the usual transformation yields the statement.

References

- Bäuerle & Rieder (2004) Bäuerle, N. & Rieder, U. (2004). Portfolio optimization with Markov-modulated stock prices and interest rates. IEEE Trans. Automat. Control 49, 442–447.

- Bäuerle & Rieder (2011) Bäuerle, N. & Rieder, U. (2011). Markov Decision Processes with applications to finance. Universitext Springer, Heidelberg.

- Bäuerle et al. (2012) Bäuerle, N., Urban, S. P. & Veraart, L. A. M. (2012). The relaxed investor with partial information. SIAM J. Financial Math. 3, 304–327.

- Bayraktar & Ludkovski (2009) Bayraktar, E. & Ludkovski, M. (2009). Sequential tracking of a hidden Markov chain using point process observations. Stochastic Process. Appl. 119, 1792–1822.

- Costa & Araujo (2008) Costa, O. L. & Araujo, M. V. (2008). A generalized multi-period mean variance portfolio optimization with Markov switching parameters. Automatica 44, 2487 – 2497.

- Dannemann & Holzmann (2008) Dannemann, J. & Holzmann, H. (2008). Testing for two states in a hidden Markov model. Canad. J. Statist. 36, 505–520.

- Di Masi et al. (1994) Di Masi, G. B., Kabanov, Y. M. & Runggaldier, V. I. (1994). Mean-square hedging of options on a stock with Markov volatilities. Teor. Veroyatnost. i Primenen. 39, 211–222.

- Elliott et al. (2008) Elliott, R., Krishnamurthy, V. & Sass, J. (2008). Moment based regression algorithm for drift and volatility estimation in continuous time Markov switching models. Econometrics Journal 11, 244–270.

- Elliott et al. (1995) Elliott, R. J., Aggoun, L. & Moore, J. B. (1995). Hidden Markov models, vol. 29 of Applications of Mathematics (New York). Springer-Verlag, New York. Estimation and control.

- Frey et al. (2012) Frey, R., Gabih, A. & Wunderlich, R. (2012). Portfolio optimization under partial information with expert opinions. Int. J. Theor. Appl. Finance 15, 1250009, 18.

- Fristedt et al. (2007) Fristedt, B., Jain, N. & Krylov, N. (2007). Filtering and prediction: a primer. American Mathematical Society, Providence, RI.

- Frühwirth-Schnatter (2001) Frühwirth-Schnatter (2001). Fully Bayesian analysis of switching Gaussian state space models. Ann. Inst. Statist. Math. 53, 31–49.

- Hahn et al. (2010) Hahn, M., Frühwirth-Schnatter, S. & Sass, J. (2010). Markov chain Monte Carlo methods for parameter estimation in multidimensional continuous-time Markov switching models. J. of Financ. Econom. 8, 88–121.

- Hahn & Sass (2009) Hahn, M. & Sass, J. (2009). Parameter estimation in continuous time Markov switching models: a semi-continuous Markov chain Monte Carlo approach. Bayesian Anal. 4, 63–84.

- Heffes & Lucantoni (1986) Heffes, H. & Lucantoni, D. (1986). A Markov modulated characterization of packetized voice and data traffic and related statistical multiplexer performance. IEEE J. Select. Areas Commun. 4, 856–867.

- Iacus (2001) Iacus, S. M. (2001). Statistical analysis of the inhomogeneous telegrapher’s process. Statist. Probab. Lett. 55, 83–88.

- Iacus & Yoshida (2008) Iacus, S. M. & Yoshida, N. (2008). Estimation for the discretely observed telegraph process. Teor. Ĭmovīr. Mat. Stat. 32–42.

- Kac (1974) Kac, M. (1974). A stochastic model related to the telegrapher’s equation. Rocky Mountain J. Math. 4, 497–509.

- Kloeden et al. (1993) Kloeden, P. E., Platen, E. & Schurz, H. (1993). Higher order approximate Markov chain filters. In Stochastic processes, 181–190, Springer, New York.

- Kulkarni (1997) Kulkarni, V. G. (1997). Fluid models for single buffer systems. In Frontiers in queueing, 321–338, Probab. Stochastics Ser., CRC, Boca Raton, FL.

- López & Ratanov (2014) López, O. & Ratanov, N. (2014). On the asymmetric telegraph processes. J. Appl. Probab. 51, 569–589.

- Otranto & Gallo (2002) Otranto, E. & Gallo, G. M. (2002). A nonparametric Bayesian approach to detect the number of regimes in Markov switching models. Econometric Rev. 21, 477–496.

- Platen & Rendek (2010) Platen, E. & Rendek, R. (2010). Quasi-exact approximation of hidden Markov chain filters. Commun. Stoch. Anal. 4, 129–142.

- Rabehasaina & Sericola (2004) Rabehasaina, L. & Sericola, B. (2004). A second-order Markov-modulated fluid queue with linear service rate. J. Appl. Probab. 41, 758–777.

- Rieder & Bäuerle (2005) Rieder, U. & Bäuerle, N. (2005). Portfolio optimization with unobservable Markov-modulated drift process. J. Appl. Probab. 42, 362–378.

- Rydén (1996) Rydén, T. (1996). An EM algorithm for estimation in Markov-modulated Poisson processes. Comput. Statist. Data Anal. 21, 431–447.

- Rydén et al. (1998) Rydén, T., Teräsvirta, T. & Åsbrink, S. (1998). Stylized facts of daily return series and the hidden Markov models. Journal of Applied Econometrics 13, 217–244.

- Sass & Haussmann (2004) Sass, J. & Haussmann, U. G. (2004). Optimizing the terminal wealth under partial information: the drift process as a continuous time Markov chain. Finance Stoch. 8, 553–577.

- Sass & Wunderlich (2010) Sass, J. & Wunderlich, R. (2010). Optimal portfolio policies under bounded expected loss and partial information. Math. Methods Oper. Res. 72, 25–61.

- Skeel & Berzins (1990) Skeel, R. D. & Berzins, M. (1990). A Method for the Spatial Discretization of Parabolic Equations in One Space Variable. SIAM Journal on Scientific and Statistical Computing 11, 1–32.

- Stern & Elwalid (1991) Stern, T. E. & Elwalid, A. I. (1991). Analysis of separable Markov-modulated rate models for information-handling systems. Adv. in Appl. Probab. 23, 105–139.

- Yao (1985) Yao, Y.-C. (1985). Estimation of noisy telegraph processes: nonlinear filtering versus nonlinear smoothing. IEEE Trans. Inform. Theory 31, 444–446.

- Yin & Zhou (2004) Yin, G. & Zhou, X. Y. (2004). Markowitz’s mean-variance portfolio selection with regime switching: from discrete-time models to their continuous-time limits. IEEE Trans. Automat. Control 49, 349–360.

- Zhang et al. (2010) Zhang, X., Siu, T. & Meng, Q. (2010). Portfolio selection in the enlarged Markovian regime-switching market. SIAM Journal on Control and Optimization 48, 3368–3388.