Negative Dependence Concept in Copulas and the Marginal Free Herd Behavior Index

Abstract

We provide a set of copulas that can be interpreted as having the negative extreme dependence. This set of copulas is interesting because it coincides with countermonotonic copula for a bivariate case, and more importantly, is shown to be minimal in concordance ordering in the sense that no copula exists which is strictly smaller than the given copula outside the proposed copula set. Admitting the absence of the minimum copula in multivariate dimensions greater than 2, the study of the set of minimal copulas can be important in the investigation of various optimization problems. To demonstrate the importance of the proposed copula set, we provide the variance minimization problem of the aggregated sum with arbitrarily given uniform marginals. As a financial/actuarial application of these copulas, we define a new herd behavior index using weighted Spearman’s rho, and determine the sharp lower bound of the index using the proposed set of copulas.

1 Introduction

The study of the dependence structure between random variables via copula is a classical problem in statistics and other applications. The ease of application of copulas has led to their popularity in various areas such as finance, insurance, hydrology and medical studies; see for example, Frees and Valdez, (1998), Genest et al., (2007) and Cui and Sun, (2004). This paper examines the mathematical property of copulas by focusing on their lower bound.

Every copula is bounded by Fréchet-Hoeffding lower and upper bounds. While Fréchet-Hoeffding upper bound corresponds to the maximum copula, Fréchet-Hoeffding lower bound is generally not a copula. Further, the minimum copula does not exist in general in high dimensions greater than ; see, for example, Kotz and Seeger, (1992) and Joe, (1997).

In the insurance and finance field, the maximum copula corresponds to the concept called comonotonicity (Dhaene et al., 2002b, ). In the respect of risk management, comonotonicity is an important concept, because it can be used to describe the perfect positive dependence between competing risks. Importantly it provides the solution to various optimization (maximization) problems. However, unlike the perfect positive dependence, mainly due to the absence of the minimum copula, controversy has remained even in the definition of negative extreme dependence In spite of these difficulties, the need for the concept of negative extreme dependence has remained in insurance and other applications because it may lead to solutions for related optimization problems. Many studies have investigated the negative extreme dependence in various contexts. Dhaene and Denuit, (1999), Cheung and Lo, (2014) and Cheung et al., (2015) defined the concept of mutual exclusivity which can be regarded as pairwise countermonotonic movements. On the other hand, (Wang and Wang,, 2011) proposed the concept of complete mixability, which can be used to minimize the variance of the sum of random variables with given marginal distributions. Many papers have recently been published in this field (Puccetti et al.,, 2012; Puccetti and Wang,, 2014; Wang and Wang,, 2014; Bernard et al.,, 2014). While the concepts of mutual exclusivity and complete mixability are both useful in various fields of optimization problems, since their concepts both depend on the marginal distributions and are problem specific, they may not provide the general concept of negative dependence.

Lee and Ahn, 2014b proposed a set of negative dependence joint distributions, which is named as -countermonotonic copulas (-CM). The definition of -CM is known to be the definition of copula only. Furthermore, the set of -CM copulas is minimal in terms of concordance ordering: there is no copula which is strictly smaller in concordance ordering than the given -CM copula except -CM copulas. Admitting the absence of the minimum element in multivariate dimensions , the set of minimal copulas can be important in optimization problems. However, without understanding the further properties of -CM copulas, choosing the proper -CM copulas for the given optimization problem can be difficult. Furthermore, as specified in Puccetti and Wang, (2014), -CM can be too general to be used for the negative extreme dependence For example, any vector with being a uniform[0,1] random variable is -CM, while it is close to a comonotonic random vector except the last element. Hence in this paper, to remove such an almost comonotonic case and emphasize the negative extreme dependence concept, we consider only a special subset of -CM copulas, which will be parameterized by the vector , where is a -dimensional positive Euclidean space. Such set of copulas will be named as -countermonotonic copulas (-CM). Due to the minimality property of the set of -CM copulas, which is inherited from -CM, we expect that the set of -CM copulas might be also useful in various optimization problems.

However, before we discuss the usefulness of -CM copulas in optimization problems, the existence of -CM copulas should be first investigated. While the existence of -CM copulas with

is well known in the literature, see, for example, Lee and Ahn, 2014b , existence of -CM copulas is not guaranteed for general . This paper provides the equivalence condition for the existence of -CM copulas. For the proof and construction of the copula, we use a simple geometrical method to construct the copula. A similar result obtained by using an algebraic method can be found in a recent working paper by Wang and Wang, (2014).

Since -CM is the property of the copula only, the usefulness of -CM may be limited to some optimization problems which do not depend on marginal distributions. Puccetti and Wang, (2014) also note the possible limitedness of -CM (hence -CM) in solving optimization problems by commenting that any dependence concept which does not take into account marginal distributions may fail to solve optimization problems which depend on marginal distributions. Variance minimization of the aggregated sum with given marginal distributions, which is formally stated in (19) below, is one such example; detailed literature can be found in Gaffke and Rüschendorf, (1981); Rüschendorf and Uckelmann, (2002); Wang and Wang, (2011); Puccetti and Wang, (2014). As can be intuitively expected, and as will be shown in Section 5 below, it can be shown that no single copula universally minimizes the variance of the aggregated sum with arbitrarily given marginals. However, we will show that using a set of -CM copulas rather than a single copula can minimize the variance of the aggregated sum for varying marginal distributions when restricted to the uniform distribution family. While our result provides a general solution with no restriction on , a partial solution can be observed in Wang and Wang, (2014) for some special cases of where they are mainly interested in so called joint mixability which aims for the constant aggregated sum. More detailed results will be provided in Section 5.

For a financial application of -CM, we provide a new definition of the herd behavior index. Herd behaviors describe the comovement of members in a group. Since herd behaviors in the stock markets are observed usually during financial crises (Dhaene et al.,, 2012; Choi et al.,, 2013), measuring the herd behavior can be important in managing financial risks. Focusing on the fact that the perfect herd behavior can be modeled with the comonotonicity, some herd behavior indices that measure the degree of comonotonicity via the concept of the (co)variance have been proposed (Dhaene et al.,, 2012; Dhaene et al., 2014a, ; Choi et al.,, 2013). Measuring the herd behavior using such herd behavior indices can be important as it has been shown to be an indicator of the market fear. However, while the concept of comonotonicity is free of marginal distribution (and hence so is the herd behavior), these herd behavior measures can depend on marginal distributions, as will be shown in Example 2 below. Alternatively, we define the new herd behavior index based on a weighted average of bivariate Spearman’s rho. This new herd behavior index is not affected by the marginal distributions by definition and will be shown to preserve the concordance ordering. We also show that the maximum and minimum of the new herd behavior are closely related with comonotonicity and -CM.

The rest of this paper is organized as follows. We first summarize the study notations, and briefly explain basic copula theory and countermonotonicity theory in Section 2. The concept of -CM is introduced in Section 3, and the existence of -CM copula is demonstrated in Section 4. Section 5 applies the concept of -CM to variance minimization problems. The definition and minimization of the new herd behavior index are discussed in in Section 6, which is followed by the conclusions.

2 Notations and Preliminary Results

2.1 Conventions

Let be integers and denotes dimensional Euclidean space. Especially, let be dimensional positive Euclidean space. Further is denoted by . We use to denote -variate vectors: especially, lower case

denotes constant vectors in and upper case

denotes -variate random vectors. More specifically

will be used to denote constant vectors in and , respectively. Finally, use to denote a uniform random variable.

Unless specified, we assume be a -dimensional random vector having as its cumulative distribution function defined by

and the marginal distribution of is for and . Define to be the Fréchet space of -variate random vectors with marginal distribution . Hence, . Equivalently, we also denote . We use to denote the special case of Fréchet space, where all marginal distributions are uniform.

This paper assumes that marginals distributions are continuous. According to Sklar (1959), given , there exists a unique function satisfying

The function is called a copula, which is also a distribution function on . Further information on copulas can be found, for example, Cherubini et al., (2004) and Nelsen, (2006).

Any satisfies

where

| (1) |

for . and in (1) are called the Fréchet-Hoeffding lower and Fréchet-Hoeffding upper bounds, respectively. Note that is a cumulative distribution of a -variate random vector while is not in general. Let be a survival distribution function defined as

For , the concordance ordering is defined by

Furthermore, define if

for any . Equivalently, denote if , where the cumulative distribution function of is . Unless specified,

are -variate random vectors in having copula , and as cumulative distributions functions, respectively. For example,

for .

It will be convenient to define the minimal and minimum copulas. For , we define -dimensional copula as a minimum(maximal) copula if the inequality

for any -dimensional copula . Similarly, for , define -dimensional copula as a minimal(maximal) copula if the inequality

for some -dimensional copula implies . Define the set of copulas to be minimal in set concordance ordering if any and with

implies

By definition, is minimal in set concordance ordering if is empty. Clearly, the definition of minimality in set concordance ordering is a weaker concept than the definition of minimal copula. In the minimality of set concordance ordering, the quality of the minimality depends on the size of the set. For example, Fréchet space is minimal in set concordance ordering. On the other hand, if has a single element, the definition of the minimality in set concordance ordering coincides with the definition of the minimal copula.

2.2 Review of -Countermonotonicity

Comonotonicity has gained popularity in actuarial science and finance. Conceptually, a random vector is comonotonic if all of its components move in the same direction. Comonotonicity is useful in several areas, such as the bound problems of an aggregate sum (Dhaene et al.,, 2006; Cheung and Vanduffel,, 2013) and hedging problems (Cheung et al.,, 2011). Recently, comonotonicity has been used in describing the economic crisis (Dhaene et al.,, 2012; Dhaene et al., 2014b, ; Choi et al.,, 2013).

Countermonotonicity is the opposite concept to comonotonicity. Conceptually, in the bivariate case, a random vector is countermonotonic if two components move in the opposite directions. The following classical results summarize the equivalent conditions of countermonotonicity in bivariate dimensions.

Definition 1.

A set is countermonotonic(comonotonic) if the following inequality holds

is called countermonotonic(comonotonic) if it has countermonotonic(comonotonic) support.

Theorem 1.

For a bivariate random vector , we have the following equivalent statements.

-

i.

is countermonotonic

-

ii.

For any

(2) -

iii.

For Uniform() random variable , we have

While the extension of comonotonicity into multivariate dimensions is straightforward, there is no obvious extension of countermonotonicity into multivariate dimensions . As discussed in Lee and Ahn, 2014b , the difficulty of the extension of countermonotonicity arises partially due to the lack of minimum copula. In this paper, we provide a set of minimal copulas, which can be viewed as a natural extension of countermonotonicity in two dimension into multivariate dimensions.

3 Weighted Countermonotonicity

As an extension of countermonotonicity or negative extreme dependence in multivariate dimensions, Lee and Ahn, 2014b introduced the concept of -CM. While -CM copulas are theoretically interesting, the existence and construction of -CM copulas with certain parametric functions remain unknown, and it may therefore be hard to apply -CM copulas to various optimization problems. Furthermore, the concept of -CM may be too general to describe the negative dependence concept as briefly specified in Puccetti and Wang, (2014), where the example of was given. Alternatively, Lee and Ahn, 2014b introduced the concept of strict -CM as a special case of -CM, which is useful in some minimization problems. However, because of the symmetricity of strict -CM, it cannot be used for non-symmetric optimization problems, as will be explained in Section 5. For completeness in the paper, we have summarized the definitions and properties of (strict) -CM in the Appendix.

In this section, we introduce a new class of extremal negative dependent copulas, which will be called -Countermonotonic (-CM) copulas and can be interpreted as a set of minimal copulas as shown in Corollary 1 below. Remark 1 addresses that the set of -CM copulas can be interpreted as generalized strict -CM, and further shows that -CM copulas are the subset of -CM copulas.

Definition 2.

A -variate random vector is -CM if

Equivalently, we say that is -CM if is -CM. Furthermore, when is -CM, we define as a shape vector of .

-CM can be regarded as multivariate extension of countermonotonicity into multivariate dimensions. First, assume that is countermonotonic. Then, since is a continuous random vector, Theorem 1. iii concludes that

which in turn implies is -CM for any . On the other hand, assume that is -CM with . Then by Definition 2, we have

with probability , which in turn concludes that the support of is countermonotonic. So we can conclude that is countermonotonic if and only if is -CM with .

As can be expected from Definition 2, -CM is a property of copula only, and this is summarized in the following lemma. The proof is similar to that of Lemma 1 in Lee and Ahn, 2014b . However, the result in the following lemma is more useful as it shows that the shape vector is invariant to marginal distributions.

Lemma 1.

Let and be random vectors from the distribution functions

respectively, where marginal distribution functions, , are possibly different from marginal distribution functions, . Then is -CM if and only if is -CM.

Proof.

Since two random vectors and have copula as the same distribution functions, we have

| (3) |

if and only if

| (4) |

Hence we conclude that is -CM if and only if is -CM. ∎

In the following definition, we provide the copula version of -CM. Note that, for the property of -CM, it is enough to study the copula version of -CM, because -CM is a property of copula only. Hence, throughout this paper, we will use the following definition as the definition of -CM.

Definition 3.

A -variate random vector is -CM if

| (5) |

Equivalently, we say that is -CM if is -CM. Here, is called as a shape vector of .

Remark 1.

Note that -CM is -CM with parameter functions

for and , where

Furthermore, since -CM coincides with strict -CM when , the set of strict -CM copula is the subset of -CM copulas. in the Appendix. For convenience, we summarize the definitions of -CM and strict -CM in Definition 6 and Definition 7 in the Appendix.

The following corollary explains that the set of -CM copulas can be regarded to have minimality in concordance ordering as a set. Since -CM is a special case of -CM as shown in Remark 1, the proof of the following corollary is immediate from Lee and Ahn, 2014b . However, for completeness in the paper, we present the proof in the Appendix.

Corollary 1.

For given , let be the set of -CM: i.e. is defined as

Then is minimal in set concordance ordering.

As briefly mentioned in Section 1, since there is no minimum copula available for , it is clear that minimal copulas will play a key role in various minimization problems. In this sense, Corollary 1 addresses an important property of -CM copulas: the set of -CM copulas achieves minimality in the sense that there are no copulas strictly smaller than the -CM copula other than -CM copulas. Hence, the concept of -CM can be useful in various minimization/maximization problems as will be explained in Section 5 below. For a discussion of the usage of -CM copulas, it is essential to check the existence of -CM copulas as will be shown in the next section.

4 Condition to Achieve the Weighted Countermonotonicity

Depending on the given marginal distributions, (5) may not be always achieved. For example, for , none of can achieve the condition in (5). In this section, we provide the equivalence condition of the weight for the existence of -CM copula. Note that a similar result can be found in a recent working paper by Wang and Wang, (2014), which explains an algebraic way of constructing -CM copulas. We first define the set of weights where -CM copulas exists.

Notation 1.

Define the set of weights in -dimensions as follows

Note that the set is equivalent with the set of the line lengths in triangles (including degenerate triangles).

Lemma 2.

For any , there exists -CM copulas.

Proof.

For convenience, define

| (6) |

and denote if

Now, let us consider the following three points

and observe that the points satisfy for . Hence any point on the line that connects and is again in : i.e.

| (7) |

for any and . Further, by the assumption , the following inequalities can be derived

which in turn implies

| (8) |

for any and . Note that the trace of (8) is triangular in with vertices lying on , and .

Now for the given triangle with vertices , and , we give positive weights , , to each edge , and such that weights are uniformly distributed on each edge. Here we assume that that the sum of weights is given as , so that the weights on the edges of the triangle define a random vector . In defining as the cumulative distribution function of the random vector , our goal is to show that there exist the weights which make a copula.

To show that is a copula, it is enough to show that is -increasing and that the marginals of are a uniform distribution (Nelsen,, 2006). Since is defined by the nonnegative weights that are distributed on the edges of the triangular, it is obvious that is -increasing. Now, it remains to show that marginals of are a uniform distribution. Since weights are uniformly distributed on each edge, it is enough to check uniformity on each vertex of the triangle, which is equivalent to show

| (9) |

Each equation in (9) is equivalent with

| (10) | ||||

respectively. The solution of (10) is

| (11) | |||

While for general , a tedious but straightforward calculation shows that, with defined in (6), defined in (11) always satisfies

Finally, (7) derives that is -CM.

∎

While is some vector in , it is worth mentioning that the definition (6) is crucial to guarantee that the solution of (9) satisfies

In other words, , which satisfies (9) may not satisfy

for and arbitrarily given that does not satisfy the condition (6). For example, for the arbitrarily given , the solution of (9) defined in (11) has

The following lemma is an extension of Lemma 2 into multivariate dimensions .

Lemma 3.

For given , if there exist disjoint subsets , and of such that

| (12) |

then there exists a random vector whose marginals are uniform[] and it satisfies

| (13) |

Proof.

Let be random vectors with marginals being uniform[0,1]. Further, let

Now the proofs are trivial if we set ’s in the same subset as being comonotonic i.e. and are comonotonic if either , or . ∎

The following lemma provides the equivalence condition of (12), which is more intuitive and easy to verify.

Lemma 4.

For the given weight , we have the following inequality

| (14) |

if and only if there exist disjoint subsets , and of satisfying (12).

Proof.

First observe that (12) implies (14) is trivial. Hence it remains to show (14) implies (12). Without loss of generality, let . For any integer , define

where and . Then it is straightforward to show that

| (15) |

Hence, along with (15), if we assume that satisfies (14), we can conclude , which in turn implies (12) with , and . ∎

So far in Lemma 3 and Lemma 4, we have provided sufficient conditions for the existence -CM copula. Then the natural question is to check whether they are also necessary conditions or not. The following corollary shows that the condition in (14) is also a necessary condition for the existence of -CM copulas.

Corollary 2.

For the given weight , there exists random vector -CM random vector if and only if satisfies

| (16) |

Proof.

It is enough to show that -CM implies (16). First, consider a weight such that one weight, say , is greater than the sum of all other weights

| (17) |

Then, it is obvious that there does not exist any random vector whose marginals are uniform[] and satisfies (5): this can be easily verified using the following variance comparison;

Hence, we can conclude that there does not exist -CM copula under the condition (17), which concludes the claim.

∎

Remark 2.

For any satisfying (16), the choice of -CM copula is not unique. For example, in the proof of Lemma 2, we show how to construct -CM copula for . On the other hand, the construction method in the proof of Lemma 2 and the following choices of defined as

and three points defined as

will derive another choice of -CM copula with .

In the bivariate case, Corollary 2 concludes that being -CM implies that which coincides with the concept of countermonotonicity as we already mentioned in Section 3. The following example shows the numerical example of the construction of -CM copula using the logic in the proof of Lemma 2.

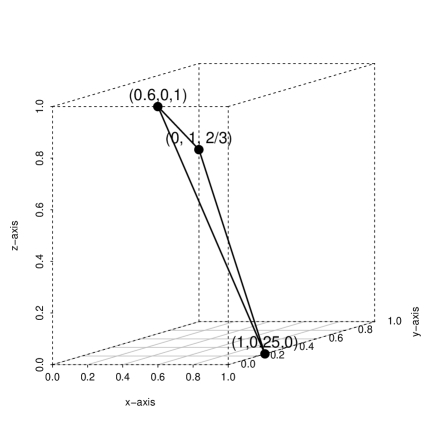

Example 1.

Let . Since

we know that and, by Corollary 2, there exists a -CM random vector . Using the techniques used in (2), we can construct -CM random vector having mass , and uniformly distributed on the each edge , and , respectively. Here

and

| (18) |

Hence, for example, we have

Finally, Figure 1 shows the support of random vector .

5 Application to the Variance Minimization Problem

Finding the maximum and the minimum of variance in the aggregated sum with given marginal distributions is the classical optimization problem

| (19) |

First of all, the maximization of (19) is straightforward using the comonotonic random vectors. For the minimization problem with , the answer is trivial with countermonotonic random variables. Regarding general dimensions , minimization of (19) was solved for some cases of marginal distributions (Gaffke and Rüschendorf,, 1981; Rüschendorf and Uckelmann,, 2002; Wang and Wang,, 2011; Puccetti and Wang,, 2014). However, minimization of (19) is not easy in general for . The following remark, which can be easily derived from Theorem 2.7 of Dhaene et al., 2014b , states that variance minimization problems are related with concordance ordering, which may offer some hints in the minimization of (19).

Remark 3.

Let be distribution functions having finite variances. If

with , then

From the remark, it is clear that the minimization and maximization of (19) is related with a minimum and maximum copula. While maximization of (19) is related with the comonotonic copula, due to the absence of the minimum copula for , the minimization of (19) is related with the set of the minimal copulas. Of course, the choice of the proper set of minimal copulas depends on the marginal distributions. Among many other choices of the marginal distributions in (19), this paper considers the uniform marginal distributions as shown in the following definition, which may be the simplest versions of (19). The following assumption is useful to simplify the notation in several theorems in this section.

Assumption 1.

Assume that .

Definition 4.

For given , define

| (20) |

and

where .

Equivalently, and can be written as

and

The upper bound

is achieved if and only if is comonotonic (Kaas et al.,, 2002; Dhaene et al., 2002a, ; Dhaene et al., 2002b, ). Regarding the lower bound, when

| (21) |

Corollary 2 concludes that

However for which does not satisfy (21), minimization is not straightforward.

For which does not satisfy (21), Theorem 2 below finds the explicit expression for . More importantly, we also show that the minimum is achieved with -CM copulas even though may not be the same as . Finally, Corollary 3 provides the complete solution for and for any given . Before we examine the main results, it is convenient to present the following lemma and notations.

Lemma 5.

Let satisfy Assumption 1 and

| (22) |

Then the following inequality holds

| (23) |

where the equality holds if and only if is -CM.

Proof.

We first prove the inequality (23) as

where the inequality arises from the fact that correlation of any two random variables is greater than , and the last equality is from the condition (22). Furthermore, since satisfies the condition (16), Corollary 2 concludes that the inequality in (23) becomes equality if and only if is -CM. ∎

Notation 2.

For given , define as

| (24) |

for . Then, one can easily confirm . Further, let

Since there always exists -CM random vector for , which satisfies the condition (16), we conclude in this case. The following proposition provides the tight bound of when does not satisfy the condition (16). The main idea of the proof is to shrink the largest weight so that the new weights satisfy the condition (16), which in turn results in constant summation or zero variance. Then Lemma 5 shows that only the remaining part of the largest weight contributes the lower bound of the variance specified in (20).

Theorem 2.

Proof.

First, observe for the given satisfying the condition (25). Further we have

| (27) | ||||

Since , we have

| (28) | ||||

where the last inequality is from (27) and Lemma 5. Furthermore, since variance of the random variable is if and only if the random variable is constant with probability , Lemma 5 concludes that the inequality in (28) is equality if and only if is -CM.

Finally, since satisfies the condition (27) (hence the condition (16)), there always exists -CM random vector , which in turn implies that the equality in (26) can be always achieved.

∎

Based on Theorem 2, the following corollary provides the complete solution for the optimization problem in Definition 4.

Corollary 3.

Proof.

The upper bound in (29) is a classical result which can explained by comonotonic ; see Kaas et al., (2002); Dhaene et al., 2002a ; Dhaene et al., 2002b for details. Hence it is enough to show the lower bound

| (30) |

and the equality holds if and only if is -CM.

For the lower bound in (29), consider two cases depending on . First, consider the following condition on

Since in this case, nonnegativeness of the variance shows the left inequality of (29). Furthermore, Corollary 2 implies that the equality in (29) holds if and only if is -CM. Finally, for satisfying

the same result was summarized in Theorem 2. ∎

6 Marginal Free Herd Behavior Index

In this section, we define the marginal free measure of dependence which can be interpreted as the measure for the herd behavior. We first review various herd behavior indices, which measure the degree of comovement or comonotonicity (Dhaene et al.,, 2012; Dhaene et al., 2014a, ; Choi et al.,, 2013). While such indices need to be marginal free (because the concept of comovement or comonotonicity is a definition of copula only), in Subsection 6.2, we observe that such indices can be distorted by marginal distributions. Alternatively, Subsection 6.3 presents a definition of measures of dependence that is free of marginal distributions.

6.1 Review of the Measures of Dependence

Herd behavior is a general concept often used in various fields such as financial and psychology to describe the irrational comovement of members in a group. The recent financial crises have further highlighted the importance of understanding the herd behavior. There have been several attempts to measure the herd behaviors through herd behavior indices. In this subsection, we will briefly review some known herd behavior indices in the financial context.

Let be individual stock prices at a time assuming that the current time is fixed at . For the given , the market index is defined as the weighted sum of the individual stock prices:

where weights can be interpreted as the total number of each stock available in the market.

Since a comonotonic random vector can be represented as

the market index under the comonotonic stock prices assumption, assuming the marginal distributions of individual stock prices to be unchanged, can be defined as

Noting the fact that, as shown in Remark 3, the variance of the market index is maximized when the individual stock prices are comonotonic, the herd behavior index by Dhaene et al., (2012) is defined as the ratio of variance of the market index to that of the index under the comonotonic assumption. The following definition defines the simplified version of HIX. The original version of HIX defined using the option prices can be found in Dhaene et al., (2012).

While HIX is a convenient measure which can measure the herd behavior effectively, HIX may be sensitive to the marginal distributions (Choi et al.,, 2013). The revised version of HIX (RHIX) defined as

is known to reduce the marginal distribution effects (Choi et al.,, 2013; Lee and Ahn, 2014a, ). The same measure was proposed by Dhaene et al., 2014a from a slightly different perspective.

Importantly, original definition of HIX (hence RHIX) can be calculated using the individual option prices and option price of the market index (Dhaene et al.,, 2012; Linders and Schoutens,, 2014), and these measures can be used as predictors of the degree of herd behaviors in the future as implied by current option prices. These are the main reasons why HIX and RHIX are favorable herd behavior indices, although there may be some preference between HIX and RHIX. Of course, HIX and RHIX can also be estimated from the high frequency stock market data (Lee and Ahn, 2014a, ).

6.2 Marginal Dependency of RHIX

Despite some controversy, if the perfect herd behavior corresponds to comonotonic movement (Dhaene et al.,, 2012), the herd behavior should be a phenomenon that solely depends on the copula. In this sense, RHIX may be more favorable than HIX, because it is known to reduce the marginal distribution effects (Choi et al.,, 2013). However, as expected from the definition of RHIX (it is defined based on covariances), RHIX cannot thoroughly remove the marginal effects. Through a simple example, this section explains that such marginal effects in the calculation of RHIX can be arbitrarily large.

For expository purposes, we consider the following Toy Model using the bivariate lognormal distribution, which is frequently used to describe the stock prices.

Toy Model.

Consider only two assets that follow a bivariate lognormal distribution with drift vector and covolatility matrix which is defined as

Note that , and are parameters related with marginal distributions, and is the only parameter for the (Gaussian) copula; see, for example, Nelsen, (2006) and Cherubini et al., (2004) for more details.

Under the Toy Model, simple calculation shows that

| (31) |

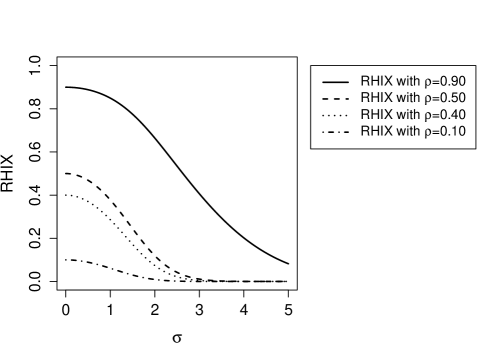

We refer to Choi et al., (2013) for more detailed calculation for HIX and RHIX under the lognormal model. Now from (31), the following equality shows that RHIX under the Toy Model converges to , when the common volatility coefficient increases, regardless of the copula coefficient .

| (32) |

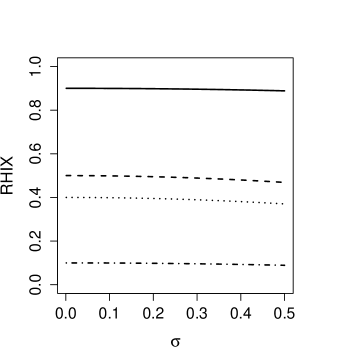

Knowing the degeneracy of RHIX as described in (32), the convergence rate can be important for the practical use of RHIX. The following example shows the convergence rate of RHIX in (32) under various circumstances.

Example 2.

Figure 2. (a) and (b) show the variation of RHIX in the Toy Model depending on the varying common volatility on the different scale time intervals of and respectively. As shown in Figure 2. (a), RHIX looks stable around reasonable weekly volatilities of the stock markets assuming the weekly volatility to be .111The weekly volatility for the S&P 500 index and IBM from March to May of 2003 were and respectively. RHIX around yearly volatility () even looks stable. However, Figure 2. (b) shows that RHIX slowly but surely decreases and converges to as increases.

6.3 New Herd Behavior Index: The Marginal Free Measure of Dependence

In the following definition, we propose a new herd behavior index that is free of marginal distribution and hence defined in terms of copula only.

Definition 5.

For a given random vector , Spearman’s rho type of the Herd Behavior Index (SIX) is defined as

where Spearman’s rho is defined as

with and are independent copies of . Sometimes we use to denote . Note that SIX coincides with pairwise Spearman’s rho defined in Schmid and Schmidt, (2007) with the equal weights .

Since bivariate Spearman’s rho does not depend on the marginal distribution, clearly SIX does not depend on the marginal distributions. Hence, for continuous marginals, we have

Since SIX can be obtained by replacing the covariance terms in RHIX with the Spearman’s rho terms, it can be interpreted as the ratio of the weighted pairwise Spearman’s rho of stock prices to the weighted average of Spearman’s rho of stock prices under the comonotonic assumption. Furthermore, similar to RHIX as in Lee and Ahn, 2014a , SIX can be expressed as the weighted average of the pairwise Spearman’s rhos as shown below

where

with

Unlike HIX or RHIX, the calculation of SIX using the vanilla option prices may be difficult in reality because, whereas the calculation of HIX and RHIX requires the option prices on the individual stocks and the market index, the calculation of SIX requires the option prices related to every pairs of the individual stock prices. As an alternative, high frequency stock price data can be used for the estimation of SIX: a detailed method for the estimation of HIX and RHIX using high frequency stock price data can be found in Lee and Ahn, 2014a and a similar method can be applied to the estimation of SIX. Empirical analysis of herd behaviors in the stock market using stock price data and SIX can be found in Lee and Ahn, 2014b .

Remark 4.

In the calculation of HIX and RHIX, we have to calculate the variance or covariance under the comonotonic assumptions. Hence, in the calculation of HIX and RHIX, an assumption on the marginal distributions is essential as shown in Lee and Ahn, 2014a , where lognormal distributions are assumed. However, for the calculation of SIX, since Spearman’s rho under comonotonic assumption is always regardless of the marginal distributions, marginal assumption is not necessary.

The following example present the representation of SIX in the multivariate log-normal distribution, and confirms that SIX is free of marginal distribution.

Example 3.

For and -variate log-normal random vector with drift vector and covolatility matrix , SIX can be represented as

| (33) | ||||

where , and the first inequality is from Kendall and Gibbons, (1990).

Spearman’s rho preserves the concordance ordering, and one can easily expect that SIX also preserves the concordance ordering. Hence it is possible to show that the maximum of SIX is achieved with the comonotonic copula. However, due to the absence of the minimum copula in the Fréchet Space, the minimum of SIX is not as clear. The following theorem provides some properties of SIX and determines the maximum and minimum of SIX.

Theorem 3.

For given , define and . Then, for the given distribution functions and , the following holds:

-

i.

If copulas satisfy , then .

- ii.

-

iii.

The upper bound of (34) is attained if and only if is comonotonic.

- iv.

Proof.

The proof of part i comes from the concordance property of Spearman’s rho and the fact that SIX is a linear combination of bivariate Spearman’s rho. For the proof of the remaining parts, note that

and

| (35) | ||||

where a constant is defined as

Now, Theorem 3 and (35) derive that

| (36) |

where the first equality in the first inequality is achieved if and only if is -CM, and the second inequality is achieved if and only if is comonotonic. Now (36) and the following observation

conclude the following inequalities

where the first equality holds if and only if is -CM and the second inequality holds if and only if is comonotonic.

∎

6.4 Data Analysis

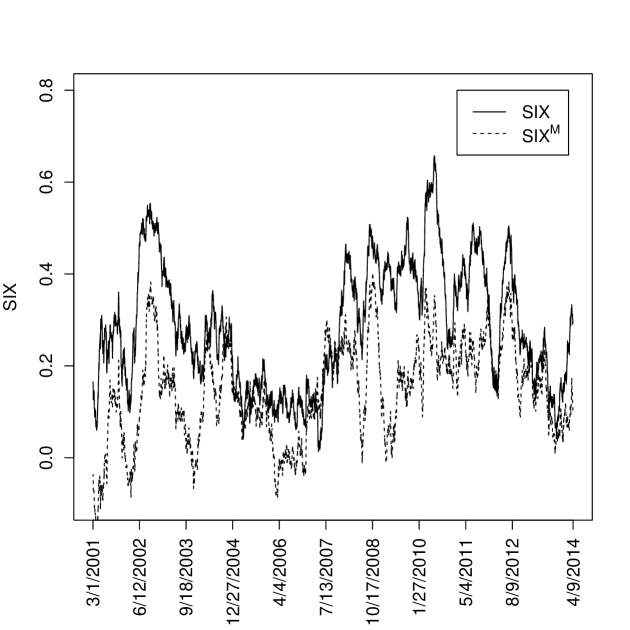

In this subsection, we analyze the herd behaviors in the US stock market using SIX. Daily stock prices of three stocks are collected from Apple, Hewlett-Packard Company and New York Times in the time interval between 2001/March/01 and 2014/April/09. Under the lognormal model, the line graph () in Figure 3 shows estimated SIX, where SIX at each point is estimated based on 4 month observations. Similar to Choi et al., (2013), three stock prices shows generally strong herd behavior during the global financial crisis starting from 2008.

Sometimes, we may be interested in the relationship between the the stock prices of three companies only. For example, we may assume that the stock prices of three companies reflect the preferences between the traditional media system (newspapers), the traditional internet based media system (computers), and the mobile internet based media system (smartphones or tablets). However, strong dependency of the three stock prices may not stand for the strong dependency between three companies in particular, because the strong comovement of the stock prices during the period may be the result of the illusion effect caused by devaluation of the whole stock market (the global economic crisis in 2008, for example). Hence, to understand the actual physical relation between three stock prices, it can be beneficial to consider the detranded stock price by the market index (S&P in this data analysis) defined as follows:

where is S&P index. The dashed line graph ()in Figure 3 shows estimated SIX using the adjusted stock price on the same time interval. Here, we have used the weight . Note that, under the lognormal model in (3), specific statistical estimation procedures can be found in Lee and Ahn, 2014a , for example.

From Figure 3, we can conclude that main source of the comovement during the global financial crisis is the devaluation of the whole stock market. After removing the comovement effect by the global financial crisis, comovement of adjusted stock prices is not as strong.

7 Conclusion

In this paper, we have provided the set of copulas called -CM copulas, and have shown these to be the minimal in set concordance ordering. Given the absence of the minimum copula, the minimality can be important in optimization problems. Especially, we show that the proposed set of copulas minimize the variance of the aggregated sum where the marginal distributions are given as various uniform distributions. As shown in Remark 3 in Section 5, the set of minimal copulas can be related with the variance of aggregated sum with given marginal distributions. In this respect, the approach using -CM copulas, which are the generalized version of -CM copulas, can be shown to be useful in minimizing the variance of the aggregated sum for some special marginal distributions. We leave this topic for future research.

Finally, although -CM copulas do not minimize the variance of the aggregated sum in general when the marginal distributions are not uniform distributions, many other interesting optimization problems have uniform marginals as their solutions. Optimization of the herd behavior index is one such example. In this paper, we have provided a herd behavior index that does not depend on the marginal distributions, and showed that the herd behavior index is minimized with -CM copulas.

Acknowledgements

For Jae Youn Ahn, this work was supported by the National Research Foundation of Korea(NRF) grant funded by the Korean Government (2013R1A1A1076062).

References

- Bernard et al., (2014) Bernard, C., Jiang, X., and Wang, R. (2014). Risk aggregation with dependence uncertainty. Insurance Math. Econom., 54:93–108.

- Cherubini et al., (2004) Cherubini, U., Luciano, E., and Vecchiato, W. (2004). Copula methods in finance. Wiley Finance Series. John Wiley & Sons Ltd., Chichester.

- Cheung et al., (2015) Cheung, K. C., Denuit, M., and Dhaene, J. (2015). Tail mutual exclusivity and tail-var lower bounds. FEB Research report AFI_15100.

- Cheung et al., (2011) Cheung, K. C., Dhaene, J., and Tang, Q. (2011). On partial hedging and counter-monotonic sums. Available at SSRN 1966995.

- Cheung and Lo, (2014) Cheung, K. C. and Lo, A. (2014). Characterizing mutual exclusivity as the strongest negative multivariate dependence structure. Insurance Math. Econom., 55:180–190.

- Cheung and Vanduffel, (2013) Cheung, K. C. and Vanduffel, S. (2013). Bounds for sums of random variables when the marginal distributions and the variance of the sum are given. Scandinavian Actuarial Journal, 2013(2):103–118.

- Choi et al., (2013) Choi, Y., Kim, C., Lee, W., and Ahn, J. Y. (2013). Analyzing herd behavior in global stock markets: An intercontinental comparison. arXiv preprint arXiv:1308.3966.

- Cui and Sun, (2004) Cui, S. and Sun, Y. (2004). Checking for the gamma frailty distribution under the marginal proportional hazards frailty model. Statistica Sinica, 14(1):249–267.

- Dhaene and Denuit, (1999) Dhaene, J. and Denuit, M. (1999). The safest dependence structure among risks. Insurance Math. Econom., 25(1):11–21.

- (10) Dhaene, J., Denuit, M., Goovaerts, M. J., Kaas, R., and Vyncke, D. (2002a). The concept of comonotonicity in actuarial science and finance: applications. Insurance: Mathematics & Economics, 31(2):133–161.

- (11) Dhaene, J., Denuit, M., Goovaerts, M. J., Kaas, R., and Vyncke, D. (2002b). The concept of comonotonicity in actuarial science and finance: Theory. Insurance: Mathematics and Economics, 31(1):3–33.

- Dhaene et al., (2012) Dhaene, J., Linders, D., Schoutens, W., and Vyncke, D. (2012). The Herd Behavior Index: a new measure for the implied degree of co-movement in stock markets. Insurance: Mathematics and Economics, 50(3):357–370.

- (13) Dhaene, J., Linders, D., Schoutens, W., and Vyncke, D. (2014a). A multivariate dependence measure for aggregating risks. J. Comput. Appl. Math., 263:78–87.

- (14) Dhaene, J., Linders, D., Schoutens, W., and Vyncke, D. (2014b). A multivariate dependence measure for aggregating risks. J. Comput. Appl. Math., 263:78–87.

- Dhaene et al., (2006) Dhaene, J., Vanduffel, S., Goovaerts, M. J., Kaas, R., Tang, Q., and Vyncke, D. (2006). Risk measures and comonotonicity: a review. Stochastic Models, 22(4):573–606.

- Frees and Valdez, (1998) Frees, E. W. and Valdez, E. A. (1998). Understanding relationships using copulas. North American Actuarial Journal, 2(1):1–25.

- Gaffke and Rüschendorf, (1981) Gaffke, N. and Rüschendorf, L. (1981). On a class of extremal problems in statistics. Mathematische Operationsforschung und Statistik Series Optimization, 12(1):123–135.

- Genest et al., (2007) Genest, C., Favre, A., Béliveau, J., and Jacques, C. (2007). Metaelliptical copulas and their use in frequency analysis of multivariate hydrological data. Water Resources Research, 43(9):W09401.

- Joe, (1997) Joe, H. (1997). Multivariate models and dependence concepts, volume 73 of Monographs on Statistics and Applied Probability. Chapman & Hall, London.

- Kaas et al., (2002) Kaas, R., Dhaene, J., Vyncke, D., Goovaerts, M. J., and Denuit, M. (2002). A simple geometric proof that comonotonic risks have the convex-largest sum. Astin Bull., 32(1):71–80.

- Kendall and Gibbons, (1990) Kendall, M. and Gibbons, J. D. (1990). Rank correlation methods. A Charles Griffin Title. Edward Arnold, London, fifth edition.

- Kotz and Seeger, (1992) Kotz, S. and Seeger, J. P. (1992). Lower bounds on multivariate distributions with preassigned marginals. In Stochastic inequalities (Seattle, WA, 1991), volume 22 of IMS Lecture Notes Monogr. Ser., pages 211–218. Inst. Math. Statist., Hayward, CA.

- (23) Lee, W. and Ahn, J. Y. (2014a). Financial interpretation of herd behavior index and its statistical estimation. Journal of the Korean Statistical Society, In Press.

- (24) Lee, W. and Ahn, J. Y. (2014b). On the multidimensional extension of countermonotonicity and its applications. Insurance: Mathematics and Economics, 56:68–79.

- Linders and Schoutens, (2014) Linders, D. and Schoutens, W. (2014). A framework for robust measurement of implied correlation. J. Comput. Appl. Math., 271:39–52.

- Nelsen, (2006) Nelsen, R. B. (2006). An introduction to copulas. Springer Series in Statistics. Springer, New York, second edition.

- Puccetti et al., (2012) Puccetti, G., Wang, B., and Wang, R. (2012). Advances in complete mixability. Journal of Applied Probability, 49(2):430–440.

- Puccetti and Wang, (2014) Puccetti, G. and Wang, R. (2014). General extremal dependence concepts. Available at SSRN 2436392.

- Rüschendorf and Uckelmann, (2002) Rüschendorf, L. and Uckelmann, L. (2002). Variance minimization and random variables with constant sum. In Distributions with given marginals and statistical modelling, pages 211–222. Kluwer Academic Publishers, Dordrecht.

- Schmid and Schmidt, (2007) Schmid, F. and Schmidt, R. (2007). Multivariate extensions of Spearman’s rho and related statistics. Statistics & Probability Letters, 77(4):407–416.

- Wang and Wang, (2011) Wang, B. and Wang, R. (2011). The complete mixability and convex minimization problems with monotone marginal densities. Journal of Multivariate Analysis, 102(10):1344–1360.

- Wang and Wang, (2014) Wang, B. and Wang, R. (2014). Joint mixability. Preprint, University of Waterloo.

Appendix A

Lee and Ahn, 2014b proposed the class of minimal copulas which can be viewed as alternatives to countermonotonicity in multivariate dimensions.

Definition 6 (Lee and Ahn, 2014b ).

A -variate random vector will be called -countermonotonic (-CM) or -CM if there exist function and

| (37) |

with probability for some constant . Equivalently, we say that the distribution function is -CM if is -CM. Especially, for the choice of functions with in (37), is called -CM with parameter functions .

Since Lee and Ahn, 2014b have shown that -CM does not depend on marginal distributions (see Lemma 1 in Lee and Ahn, 2014b ), we provide a version of -CM definition for a copula only in this appendix. As we have briefly mentioned in Section 3, -CM may be too general to be used for the extreme negative dependence as it includes almost countermonotonic movement. Alternatively, Lee and Ahn, 2014b provide a definition of strict -CM as a subset of -CM in the following sense.

Definition 7 (Lee and Ahn, 2014b ).

A -variate random vector is strict -CM if

Equivalently, we say that is strict -CM if is strict -CM.

It is obvious that strictly -CM is -CM having constant multiplication of identity functions as parameter functions: i.e.

for . The existence of a strict -CM copula is shown in Rüschendorf and Uckelmann, (2002); Lee and Ahn, 2014b . Strict -CM is useful in various minimization/maximization problems (Lee and Ahn, 2014b, ).

Proof of Corollary 1 .

Showing Corollary 1 is equivalent to show that for any given -CM copula and satisfying

implies that is also -CM.

First observe that if does not satisfy (16), then is empty and the proof is trivial. So we can assume that satisfies (16) and is not empty. Now, define two sets

and

Then, by the denseness of rational numbers in real line, we have

which in turn implies

| (38) | ||||

where the last inequality holds because is countable set. Similar logic derives

which in turn concludes the proof with (38). ∎