18mm18mm15mm10mm

This version:

, ,

Managing Systematic Mortality Risk in

Life Annuities: An Application of Longevity Derivatives

Abstract

This paper assesses the hedge effectiveness of an index-based longevity swap and a longevity cap. Although swaps are a natural instrument for hedging longevity risk, derivatives with non-linear pay-offs, such as longevity caps, also provide downside protection. A tractable stochastic mortality model with age dependent drift and volatility is developed and analytical formulae for prices of these longevity derivatives are derived. Hedge effectiveness is considered for a hypothetical life annuity portfolio. The hedging of the life annuity portfolio is comprehensively assessed for a range of assumptions for the market price of longevity risk, the term to maturity of the hedging instruments, as well as the size of the underlying annuity portfolio. The model is calibrated using Australian mortality data. The results provide a comprehensive analysis of longevity hedging, highlighting the risk management benefits and costs of linear and nonlinear payoff structures.

keywords:

longevity risk management; longevity swaps; longevity options; hedge effectivenessJEL Classification: G22, G23, G13

1 Introduction

Securing a comfortable living after retirement is fundamental to the majority of the working population around the world. A major risk in retirement, however, is the possibility that retirement savings will be outlived. Products that provide guaranteed lifetime income, such as life annuities, need to be offered in a cost effective way while maintaining the long run solvency of the provider. Annuity providers and pension funds need to manage the systematic mortality risk111From an annuity provider’s perspective, longevity risk modelling can lead to a (stochastically) over- or underestimation of survival probabilities for all annuitants. For this reason longevity risk is also referred to as the systematic mortality risk., associated with random changes in the underlying mortality intensity, in a life annuity or pension portfolio. Systematic mortality risk cannot be diversified away with increasing portfolio size, while idiosyncratic mortality risk, representing the randomness of deaths in a portfolio with fixed mortality intensity, is diversifiable.

Reinsurance has been important in managing longevity risk for annuity and pension providers. However, there are concerns that reinsurers have a limited risk appetite and are reluctant to take this “toxic” risk (Blake et al. (2006b)). In fact, even if they were willing to accept the risk, the reinsurance sector is not deep enough to absorb the vast scale of longevity risk currently undertaken by annuity providers and pension funds.222It is estimated that pension assets for the 13 largest major pension markets have reached nearly 30 trillions in 2012 (Global Pension Assets Study 2013, Towers Watson). The sheer size of capital markets and an almost zero correlation between financial and demographic risks, suggests that they will increasingly take a role in the risk management of longevity risk.

The first generation of capital market solutions for longevity risk, in the form of mortality and longevity bonds ( Blake and Burrows (2001), Blake et al. (2006a) and Bauer et al. (2010))333Of particular interest is an attempt to issue the EIB longevity bond by the European Investment Bank (EIB) in 2004, which was underwritten by BNP Paribas. This bond was not well received by investors and could not generate enough demand to be launched due to its deficiencies, as outlined in Blake et al. (2006a)., gained limited success.

The second generation involving forwards and swaps have attracted increasing interest (Blake et al. (2013)). Index-based instruments aim to mitigate systematic mortality risk, and have the potential to be less costly and are designed to allow trading as standardised contracts (Blake et al. (2013)). Unlike the bespoke or customized hedging instruments such as reinsurance, they do not cover idiosyncratic mortality risk and give rise to basis risk (Li and Hardy (2011)). Since idiosyncratic mortality risk is reduced for larger portfolios, portfolio size is an important factor that determines the hedge effectiveness of index-based instruments.

Longevity derivatives with a linear payoff, including q-forwards and S-forwards, have as an underlying the mortality and the survival rate, respectively (LLMA (2010a)). Their hedge effectiveness has been considered in Ngai and Sherris (2011) who study the effectiveness of static hedging of longevity risk in different annuity portfolios. They consider a range of longevity-linked instruments including q-forwards, longevity bonds and longevity swaps as hedging instruments to mitigate longevity risk and demonstrate their benefits in reducing longevity risk. Li and Hardy (2011) also consider hedging longevity risk with a portfolio of q-forwards. They highlight basis risk as one of the obstacles in the development of an index-based longevity market.

Longevity derivatives with a nonlinear payoff structure have not received a great deal of attention to date. Boyer and Stentoft (2013) evaluate European and American type survivor options using simulations and Wang and Yang (2013) propose and price survivor floors under an extension of the Lee-Carter model. These authors do not consider the hedge effectiveness of longevity options and longevity swaps as hedging instruments.

Although dynamic hedging has been considered, because of the lack of liquid markets in longevity risk, static hedging remains the only realistic option for annuity providers. Cairns (2011) considers q-forwards and a discrete-time delta hedging strategy, and compares it with static hedging. The lack of analytical formulas for pricing q-forwards and its derivatives, known as “Greeks”, can be a significant problem in assessing hedge effectiveness since simulations within simulations are required for dynamic hedging strategies. The importance of tractable models has also been emphasised in Luciano et al. (2012) who also consider dynamic hedging for longevity and interest rate risk. Hari et al. (2008) apply a generalised two-factor Lee-Carter model to investigate the impact of longevity risk on the solvency of pension annuities.

This paper provides pricing analysis of longevity derivatives, as well as their hedge effectiveness. We consider static hedging. A longevity swap and a cap are chosen as linear and nonlinear products to compare and assess index-based capital market products management of longevity risk management. The model used for this analysis is a continuous time model for mortality with age based drift and volatility, allowing tractable analytical formulae for pricing and hedging. The analysis is based on a hypothetical life annuity portfolio subject to longevity risk. The paper considers the hedging of longevity risk using a longevity swap and a longevity cap, a portfolio of S-forwards and longevity caplets respectively, based on a range of different underlying assumptions for the market price of longevity risk, the term to maturity of hedging instruments, as well as the size of the underlying annuity portfolio.

The paper is organised as follows. Section 2 specifies the two-factor Gaussian mortality model, and its parameters are estimated using Australian males mortality data. Section 3 analyses longevity derivatives, in particular, a longevity swap and a cap, from a pricing perspective. Explicit pricing formulas are derived under the proposed two-factor Gaussian mortality model. Section 4 examines various hedging features and hedge effectiveness of a longevity swap and a cap on a hypothetical life annuity portfolio exposed to longevity risk. Section 5 summarises the results and provides concluding remarks.

2 Mortality Model

Let be a filtered probability space where is the real world probability measure. The subfiltration contains information about the dynamics of the mortality intensity while death times of individuals are captured by . It is assumed that the interest rate is constant where denotes the price of a -year zero coupon bond, and our focus is on the modelling of stochastic mortality.

2.1 Model Specification

For the purpose of financial risk management applications one requires stochastic mortality model that is tractable, and is able to capture well the mortality dynamics for different ages. We work under the affine mortality intensity framework and assume the mortality intensity to be Gaussian such that analytical prices can be derived for longevity options, as described in Section 3. Gaussian mortality models have been considered in Bauer et al. (2010) and Blackburn and Sherris (2013) within the forward mortality framework. Luciano and Vigna (2008) suggest Gaussian mortality where the intensity follows the Ornstein-Uhlenbeck process. In addition, Jevtic et al. (2013) consider a continuous time cohort model where the underlying mortality dynamics is Gaussian.

We consider a two-factor Gaussian mortality model for the mortality intensity process of a cohort aged at time 444For simplicity of notation we replace by .:

| (2.1) |

where

| (2.2) | ||||

| (2.3) |

and . The first factor is a general trend for the intensity process that is common to all ages. The second factor depends on the initial age through the drift and the volatility terms.555We can in fact replace by in Eq. (2.3). Using will take into account the empirical observation that the volatility of mortality tends to increase along with age (Figures 1 and 2). However, for a Gaussian process the intensity will have a non-negligible probability of reaching negative value when the volatility from the second factor () becomes very high, which occurs for example when (given ). Using instead of will also make the result in Section 3 easy to interpret. For these reasons we assume that the second factor depends on the initial age only. The initial values and of the factors are denoted by and , respectively. The model is tractable and for a specific choice of the parameters (when ) has been applied to short rate modelling in Brigo and Mercurio (2007).

Proposition 2.1

Under the two-factor Gaussian mortality model (Eq. (2.1) - (2.3)), the - year expected survival probability of a person aged at time , conditional on filtration , is given by

| (2.4) |

where, using and ,

| (2.5) | ||||

| (2.6) |

are the mean and the variance of the integral , which is Gaussian distributed, respectively.

We will use the fact that the integral is Gaussian with known mean and variance to derive analytical pricing formulas for longevity options in Section 3.

-

Proof.

Solving Eq. (2.2) to obtain an integral form of , we have

(2.7) The first term in Eq. (2.7) can be simplified to

For the second term, we have

where stochastic integration by parts is applied in the second equality.

To obtain an integral representation for , we follow the same steps as above, replacing by in Eq. (2.7). It is then straightforward to notice that

(2.8) is a Gaussian random variable with mean (Eq. (2.5)) and variance (Eq. (2.6)). Equation (2.4) is obtained by applying the moment generating function of a Gaussian random variable.

2.2 Parameter Estimation

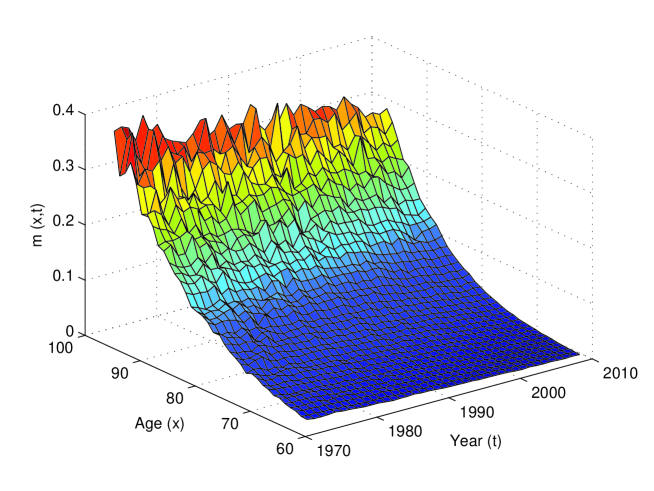

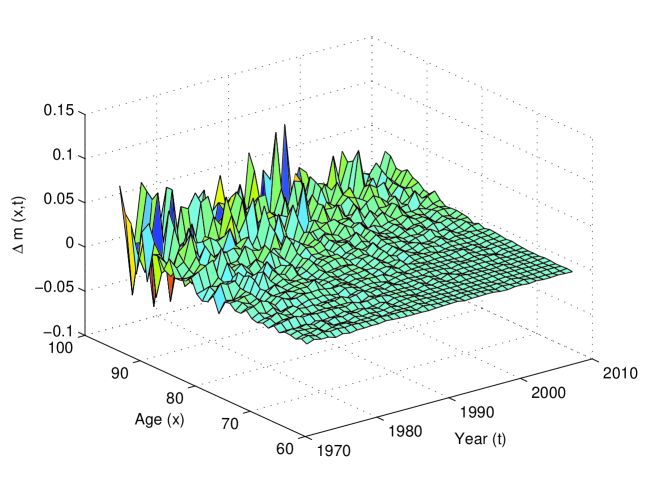

The discretised process, where the intensity is assumed to be constant over each integer age and calendar year, is approximated by the central death rates (Wills and Sherris (2011)). Figure 1 displays Australian male central death rates for years and ages . Figure 2 shows the difference of the central death rates . The variability of is evidently increasing with increasing age , which leads to the anticipation that . Furthermore, for a fixed age , there is a slight improvement in central death rates for more recent years, compared to the past.

The parameters , which determine the volatility of the intensity process, are estimated as described below. As in Jevtic et al. (2013), we aim to estimate parameters using the method of least squares, thus, calibrating the model to the mortality surface. However, we take advantage of the fact that a Gaussian model is employed where the variance of the model can be calculated explicitly and thus, we capture the diffusion part of the process by matching the variance of the model to mortality data. Specifically, the implemented procedure is as specified below:

-

1.

Using empirical data for ages we evaluate the sample variance of across time, denoted by .

-

2.

The model variance for age is given by

(2.9) Since the difference between the death rates is computed in yearly terms, we set .

-

3.

The parameters are then estimated by fitting the model variance to the sample variance for ages using least squares estimation, that is, by minimising

(2.10) with respect to the parameters .

The remaining parameters are then estimated as described below666We calibrate the model for ages 65 and 75 simultaneously to obtain reasonable values for and since the drift of the second factor is age-dependent.:

-

1.

From the central death rates, we obtain empirical survival curves for cohorts aged 65 and 75 in 2008. The survival curve is obtained by setting

(2.11) where is the central death rate of an years old at time .777Here represents calendar year 2008 and we approximate the 1-year survival probability by .

-

2.

The parameters are then estimated by fitting the survival curves () of the model to the empirical survival curves using least squares estimation, that is, by minimising

(2.12) where and , with respect to the parameters .

The estimated parameters are reported in Table 1. Since we observe that the volatility of the process is higher for older (initial) age .

| 0.0022465 | 0.0000002 | 0.129832 | -0.795875 | 0.0017508 |

| 0.0000615 | 0.120931 | 0.0021277 | 0.0084923 | 0.0294695 |

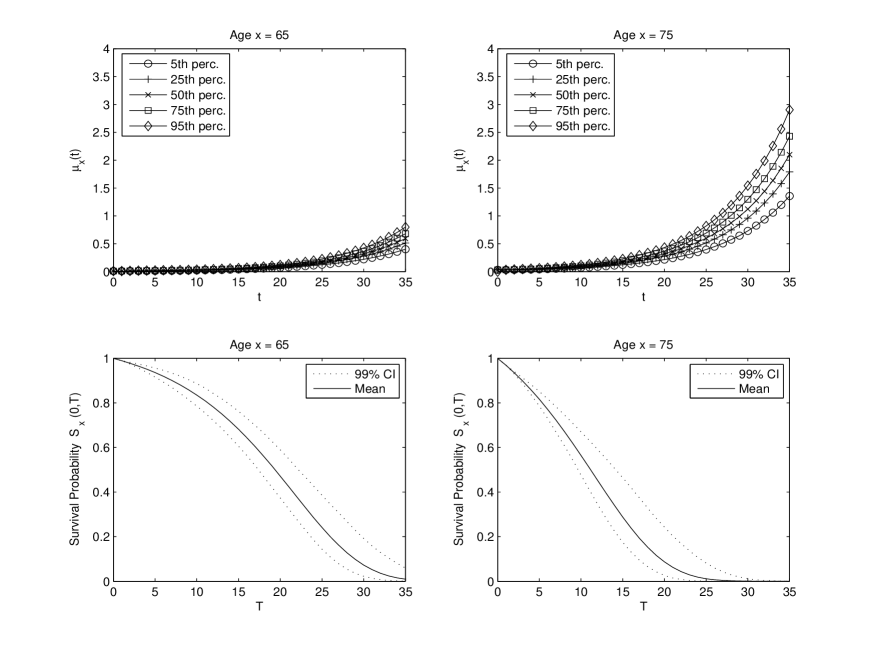

The upper panel of Figure 3 shows the percentiles of the simulated mortality intensity for ages 65 and 75 in the left and the right panel, respectively. One observes that the volatility of the mortality intensity is higher for a 75 year old compared to a 65 year old. Corresponding survival probabilities are displayed in the lower panel of Figure 3, together with the confidence bands computed pointwise. As it is pronounced from the figures, the two-factor Gaussian model specified above, despite its simplicity, produces reasonable mortality dynamics for ages 65 and 75.

3 Analytical Pricing of Longevity Derivatives

We consider longevity derivatives with different payoff structures including longevity swaps, longevity caps and longevity floors. Closed form expressions for prices of these longevity derivatives are derived under the assumption of the two-factor Gaussian mortality model introduced in Section 2. These instruments are written on survival probabilities and their properties are analysed from a pricing perspective.

3.1 Risk-Adjusted Measure

For the purpose of no-arbitrage valuation, we require the dynamics of the factors and to be written under a risk-adjusted measure.888Since the longevity market is still in its development stage and hence, incomplete, we assume a risk-adjusted measure exists but is not unique. To preserve the tractability of the model, we assume that the processes and with dynamics

| (3.1) | ||||

| (3.2) |

are standard Brownian motions under a risk-adjusted measure . In Eq. (3.2) represents the market price of longevity risk.999For simplicity, we assume that there is no risk adjustment for the first factor and is age-independent. Under we can write the factor dynamics as follows:

| (3.3) | ||||

| (3.4) |

The corresponding risk-adjusted survival probability is given by

| (3.5) |

where is replaced by in the expressions for and , see Eq. (2.5) and Eq. (2.6), respectively.

Since a liquid longevity market is yet to be developed, we aim to determine a reasonable value for based on the longevity bond announced by BNP Paribas and European Investment Bank (EIB) in 2004 as proposed in Cairns et al. (2006) and applied in Meyricke and Sherris (2014), see also Wills and Sherris (2011). The BNP/EIB longevity bond is a 25-year bond with coupon payments linked to a survivor index based on the realised mortality rates.101010The issue price was determined by BNP Paribas using anticipated cash flows based on the 2002-based mortality projections provided by the UK Government Actuary’s Department. The price of the longevity bond is given by

| (3.6) |

where is a spread, or an average risk premium per annum111111The spread depends on the term of the bond and the initial age of the cohort being tracked (Cairns et al. (2006)), and is related to but distinct from , the market price of longevity risk., and the T-year projected survival rate is assumed to be the T-year survival probability for the Australian males cohort aged 65 as modelled in Section 2, see Eq. (2.4). Since the BNP/EIB bond is priced based on a yield of 20 basis points below standard EIB rates (Cairns et al. (2006)), we have the spread of .121212The reference cohort for the BNP/EIB longevity bond is the England and Wales males aged 65 in 2003. Since the longevity derivatives market is under-developed in Australia, we assume that the same spread of (as in the UK) is applicable to the Australian males cohort aged 65 in 2008. Note however that sensitivity analyses will be performed in Section 4.

Under a risk-adjusted measure , the price of the longevity bond corresponds to

| (3.7) |

Fixing the interest rate to , we find a model-dependent , such that the risk-adjusted bond price matches the market bond price as close as possible. For example, for we have and . For more details on the above procedure refer to Meyricke and Sherris (2014). In the following we assume that the risk-adjusted measure is determined by a unique value of .

Figure 4 shows the risk-adjusted survival probabilities for Australian males aged 65 with respect to different values of the market price of longevity risk . As one observes from the figure, a larger (positive) value of leads to an improvement in survival probability, while a smaller values of indicate a decline in survival probability under the risk-adjusted measure .

3.2 Longevity Swaps

A longevity swap involves counterparties swapping fixed payments for payments linked to the number of survivors in a reference population in a given time period, and can be thought of as a portfolio of S-forwards, see Dowd (2003). An S-forward, or ‘survivor’ forward has been developed by LLMA (2010b). Longevity swaps can be regarded as a stream of S-forwards with different maturity dates. One of the advantages of using S-forwards is that there is no initial capital requirement at the inception of the contract and cash flows occur only at maturity.

Consider an annuity provider who has an obligation to pay an amount dependent on the number of survivors, and hence, survival probability of a cohort at time . If longevity risk is present, the survival probability is stochastic. In order to protect himself from a larger-than-expected survival probability, the provider can enter into an S-forward contract paying a fixed amount and receiving an amount equal to the realised survival probability at time . In doing so, the survival probability that the provider is exposed to is certain, and corresponds to some fixed value . If the contract is priced in such a way that there is no upfront cost at the inception, it must hold that

| (3.8) |

under the risk-adjusted measure . Thus, the fixed amount can be identified to be the risk-adjusted survival probability, that is,

| (3.9) |

Assuming that there is a positive market price of longevity risk, the longevity risk hedger who pays the fixed leg and receives the floating leg bears the cost for entering an S-forward.131313The risk-adjusted survival probability will be larger than the “best estimate” -survival probability if a positive market price of longevity risk is demanded, see Figure 4. Following terminology in Biffis et al. (2014), the amount can be referred to as the swap rate of an S-forward with maturity . In general, the mark-to-market price process of an S-forward with fixed leg (not necessarily as in Eq. (3.9)) is given by

| (3.10) |

for . The quantity

| (3.11) |

is the realised survival probability, or the survivor index for the cohort, which is observable given .

The term that appears in Eq. (3.10) has a natural interpretation. Given information at time , this term becomes , which is the risk-adjusted survival probability. As time moves on and more information , with , is revealed, the term is a product of the realised survival probability of the first years, and the risk-adjusted survival probability in the next years. At maturity , this product becomes the realised survival probability up to time . In order words, one can think of as the -year risk-adjusted survival probability with information known up to time .

The price process in Eq. (3.10) depends on the swap rate of an S-forward written on the same cohort that is now aged at time , with time to maturity . If a liquid longevity market was developed, the swap rate could be obtained from market data. As is observable at time , the mark-to-market price process of an S-forward could be considered model-independent. However, since a longevity market is still in its development stage, market swap rates are not available and a model-based risk-adjusted survival probability has to be used instead. An analytical formula for the mark-to-market price of an S-forward can be obtained if the risk-adjusted survival probability is expressed in a closed-form, which can be performed, for example, under the two-factor Gaussian mortality model.

Since a longevity swap is constructed as a portfolio of S-forwards, the price of a longevity swap is simply the sum of the individual S-forward prices.

3.3 Longevity Caps

A longevity cap, which is a portfolio of longevity caplets, provides a similar hedge to a longevity swap but is an option-type instrument. Consider again a scenario described in Section 3.2 where an annuity provider aims to hedge against larger-than-expected -year survival probability of a particular cohort. Alternatively to hedging with an S-forward, the provider can enter into a long position of a longevity caplet with payoff at time corresponding to

| (3.12) |

where is the strike price.141414The payoff of a longevity caplet is similar to the payoff of the option embedded in the principal-at-risk bond described in Biffis and Blake (2014). If the realised survival probability is larger than , the hedger receives an amount from the longevity caplet. This payment can be regarded as a compensation for the increased payments that the provider has to make in the annuity portfolio, due to the larger-than-expected survival probability. There is no cash outflow if the realised survival probability is smaller than or equal to . In other words, the longevity caplet allows the provider to “cap” its longevity exposure at with no downside risk. Since a longevity caplet has a non-negative payoff, it comes at a cost. The price of a longevity caplet

| (3.13) |

under the two-factor Gaussian mortality model is obtained in the following Proposition.

Proposition 3.1

Under the two-factor Gaussian mortality model (Eq. (2.1)-Eq. (2.3)) the price at time of a longevity caplet , with maturity and strike , is given by

| (3.14) |

where is the realised survival probability observable at time , is the risk-adjusted survival probability in the next years, and denotes the cumulative distribution function of a standard Gaussian random variable.

- Proof.

Similar to an S-forward, the price of a longevity caplet depends on the product term . In particular, a longevity caplet is said to be out-of-the-money if ; at-the-money if ; and in-the-money if . Eq. (3.14), is verified using Monte Carlo simulation summarised in Table 2, where we set , and . Other parameters are as specified in Table 1.

| (T, K) | Exact | M.C. Simulation |

|---|---|---|

| (10, 0.6) | 0.15632 | 0.15644 [0.15631, 0.15656] |

| (10, 0.7) | 0.08929 | 0.08941 [0.08928, 0.08954] |

| (10, 0.8) | 0.02261 | 0.02262 [0.02250, 0.02275] |

| (20, 0.3) | 0.08373 | 0.08388 [0.08371, 0.08406] |

| (20, 0.4) | 0.03890 | 0.03897 [0.03879, 0.03914] |

| (20, 0.5) | 0.00525 | 0.00530 [0.00522, 0.00539] |

Following the result of Proposition 3.1, the two-factor Gaussian mortality model leads to the price of a longevity caplet that is a function of the following variables:

-

•

realised survival probability of the first years;

-

•

risk-adjusted survival probability in the next years;

-

•

interest rate ;

-

•

strike price ;

-

•

time to maturity ; and

-

•

standard deviation , which is a function of the time to maturity and the model parameters.

Since the quantity is log-normally distributed under the two-factor Gaussian mortality model, Eq. (3.14) resembles the Black-Scholes formula for option pricing where the underlying stock price follows a geometric Brownian motion. In our setup, the stock price at time is replaced by the -year risk-adjusted survival probability with information available up to time . While the stock is traded and can be modelled directly using market data, the underlying of a longevity caplet is the survival probability which is not tradable but can be determined as an output from the dynamics of mortality intensity. As a result, the role of the stock price volatility in the Black-Scholes formula is played by the standard deviation of the integral of the mortality intensity . Since the integral captures the whole history of the mortality intensity from to under , one can interpret the standard deviation as the volatility of the risk-adjusted aggregated longevity risk of a cohort aged at time , for the period from to .

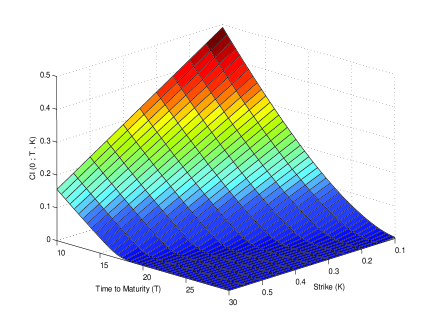

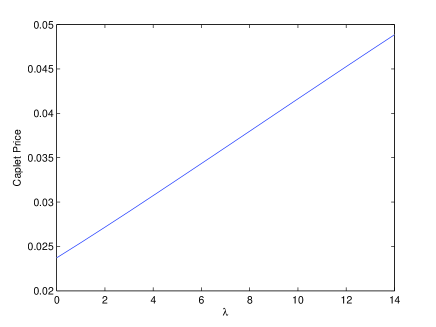

The left panel of Figure 5 shows caplet prices for a cohort aged , using parameters as specified in Table 1, as a function of time to maturity and strike . We set , and such that . A lower strike price indicates that the buyer of a caplet is willing to pay more to secure a better protection against a larger-than-expected survival probability. On the other hand, when the time to maturity is increasing, the underlying survival probability is likely to take smaller values, which leads to a higher probability for the caplet to become out-of-the-money at maturity for a fixed , see Eq. (3.12). Consequently, for a fixed the caplet price decreases with increasing .

The right panel of Figure 5 illustrates the effect of the market price of longevity risk on the caplet price. The price of a caplet increases with increasing . As shown in Figure 4, a larger value of will lead to an improvement in survival probability under . Thus, a higher caplet price is observed since the underlying survival probability is larger (on average) under when increases, see Eq. (3.13).

Since longevity cap is constructed as a portfolio of longevity caplets, it can be priced as a sum of individual caplet prices, see also Section 4.1.2.

4 Managing Longevity Risk in a Hypothetical Life Annuity Portfolio

Hedging features of a longevity swap and cap are examined for a hypothetical life annuity portfolio subject to longevity risk. Factors considered include the market price of longevity risk, the term to maturity of hedging instruments and the size of the underlying annuity portfolio.

4.1 Setup

We consider a hypothetical life annuity portfolio that consists of a cohort aged . The size of the portfolio that corresponds to the number of policyholders, is denoted by . The underlying mortality intensity for the cohort follows the two-factor Gaussian mortality model described in Section 2, and the model parameters are specified in Table 1. We assume that there is no loading for the annuity policy and expenses are not included.

Further, we assume a single premium, whole life annuity of per year payable in arrears conditional on the survival of the annuitant to the payment dates. The fair value, or the premium, of the annuity evaluated at is given by

| (4.1) |

where and is the maximum age allowed in the mortality model. The life annuity provider, thus, receives a total premium, denoted by , for the whole portfolio corresponding to the sum of individual premiums:

| (4.2) |

This is the present value of the asset held by the annuity provider at . Since the promised annuity cashflows depend on the death times of annuitants in the portfolio, the present value of the liability is subject to randomness caused by the stochastic dynamics of the mortality intensity. The present value of the liability for each policyholder, denoted by , is determined by the death time of the policyholder, and is given by

| (4.3) |

for a simulated , with denoting the next smaller integer of a real number . The present value of the liability for the whole portfolio is obtained as a sum of individual liabilities:

| (4.4) |

The algorithm for simulating death times of annuitants, which requires a single simulated path for the mortality intensity of the cohort, is summarised in Appendix A. The discounted surplus distribution () of an unhedged annuity portfolio is obtained by setting

| (4.5) |

The impact of longevity risk is captured by simulating the discounted surplus distribution where each sample is determined by the realised mortality intensity of a cohort. Since traditional pricing and risk management of life annuity relies on diversification effect, or the law of large numbers, we consider the discounted surplus distribution per policy

| (4.6) |

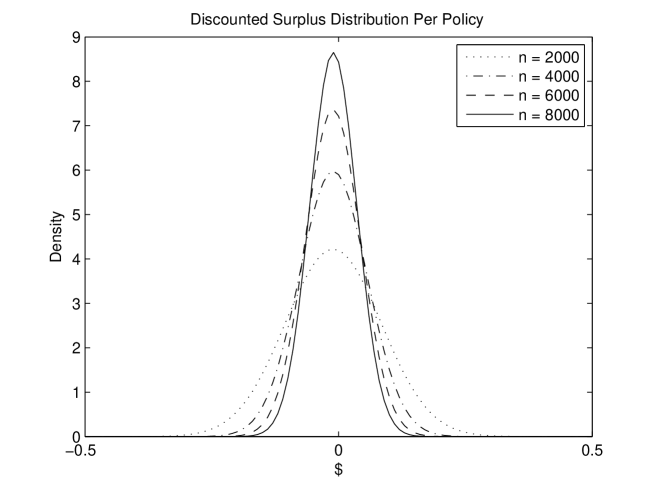

Figure 6 shows the discounted surplus distribution per policy without longevity risk (i.e. when setting ) with different portfolio sizes, varying from to . As expected, the mean of the distribution is centred around zero as there is no loading assumed in the pricing algorithm, while the standard deviation diminishes as the number of policies increases.

In the following we consider a longevity swap and a cap as hedging instruments. These are index-based instruments where the payoffs depend on the survivor index, or the realised survival probability (Eq. (3.11)), which is in turn determined by the realised mortality intensity. We do not consider basis risk151515If basis risk is present, we need to distinguish between the mortality intensity for the population () and mortality intensity for the cohort () underlying the annuity portfolio, see Biffis et al. (2014). but due to a finite portfolio size, the actual proportion of survivors, , where denotes the number of deaths experienced by a cohort during the period , will be in general similar, but not identical, to the survivor index (Appendix A). As a result, the static hedge will be able to reduce systematic mortality risk, whereas the idiosyncratic mortality risk component will be retained by the annuity provider.

4.1.1 A Swap-Hedged Annuity Portfolio

For an annuity portfolio hedged by an index-based longevity swap, payments from the swap

| (4.7) |

at time depend on the realised mortality intensity, where denotes the term to maturity of the longevity swap. The number of policyholders acts as the notional amount of the swap contract so that the quantity represents the number of survivors implied by the realised mortality intensity at time . We fix the strike of a swap to the risk-adjusted survival probability, that is,

| (4.8) |

such that the price of a swap is zero at , see Section 3.2. The discounted surplus distribution of a swap-hedged annuity portfolio can be expressed as

| (4.9) |

where

| (4.10) |

is the (random) discounted cashflow coming from a long position in the longevity swap. The discounted surplus distribution per policy of a swap-hedged annuity portfolio is determined by .

4.1.2 A Cap-Hedged Annuity Portfolio

For an annuity portfolio hedged by an index-based longevity cap, the cashflows

| (4.11) |

at are payments from a long position in the longevity cap. We set

| (4.12) |

such that the strike for a longevity caplet is the “best estimated” survival probability given .161616For a longevity swap, the risk-adjusted survival probability is used as a strike price so that the price of a longevity swap is zero at inception. In contrast, a longevity cap has non-zero price and is the most natural choice for a strike. The discounted surplus distribution of a cap-hedged annuity portfolio is given by

| (4.13) |

where

| (4.14) |

is the (random) discounted cashflow from holding the longevity cap and

| (4.15) |

is the price of the longevity cap. The discounted surplus distribution per policy of a cap-hedged annuity portfolio is given by .

4.2 Results

Hedging results are summarised by means of summary statistics that include mean, standard deviation (std. dev.), skewness, as well as Value-at-Risk (VaR) and Expected Shortfall (ES) of the discounted surplus distribution per policy of an unhedged, a swap-hedged and a cap-hedged annuity portfolio. Skewness is included since the payoff of a longevity cap is nonlinear and the resulting distribution of a cap-hedged annuity portfolio is not symmetric. VaR is defined as the -quantile of the discounted surplus distribution per policy. ES is defined as the expected loss of the discounted surplus distribution per policy given the loss is at or below the -quantile. We fix so that the confidence interval for VaR and ES corresponds to . We use 5,000 simulations to obtain the distribution for the discounted surplus. Hedge effectiveness is examined with respect to (w.r.t.) different assumptions underlying the market price of longevity risk (), the term to maturity of hedging instruments () and the portfolio size (). Parameters for the base case are as specified in Table 3.

| (years) | ||

|---|---|---|

| 8.5 | 30 | 4000 |

4.2.1 Hedging Features w.r.t. Market Price of Longevity Risk

| Mean | Std.dev. | Skewness | VaR0.99 | ES0.99 | |

| No hedge | -0.0076 | 0.3592 | -0.2804 | -0.9202 | -1.1027 |

| Swap-hedged | -0.0089 | 0.0718 | -0.1919 | -0.1840 | -0.2231 |

| Cap-hedged | -0.0086 | 0.2054 | 1.0855 | -0.3193 | -0.3515 |

| No hedge | 0.1520 | 0.3592 | -0.2804 | -0.7606 | -0.9431 |

| Swap-hedged | 0.0048 | 0.0718 | -0.1919 | -0.1703 | -0.2094 |

| Cap-hedged | 0.0682 | 0.2054 | 1.0855 | -0.2425 | -0.2746 |

| No hedge | 0.2978 | 0.3592 | -0.2804 | -0.6148 | -0.7973 |

| Swap-hedged | 0.0204 | 0.0718 | -0.1919 | -0.1547 | -0.1938 |

| Cap-hedged | 0.1205 | 0.2054 | 1.0855 | -0.1903 | -0.2224 |

| No hedge | 0.4475 | 0.3592 | -0.2804 | -0.4650 | -0.6476 |

| Swap-hedged | 0.0398 | 0.0718 | -0.1919 | -0.1354 | -0.1744 |

| Cap-hedged | 0.1619 | 0.2054 | 1.0855 | -0.1489 | -0.1810 |

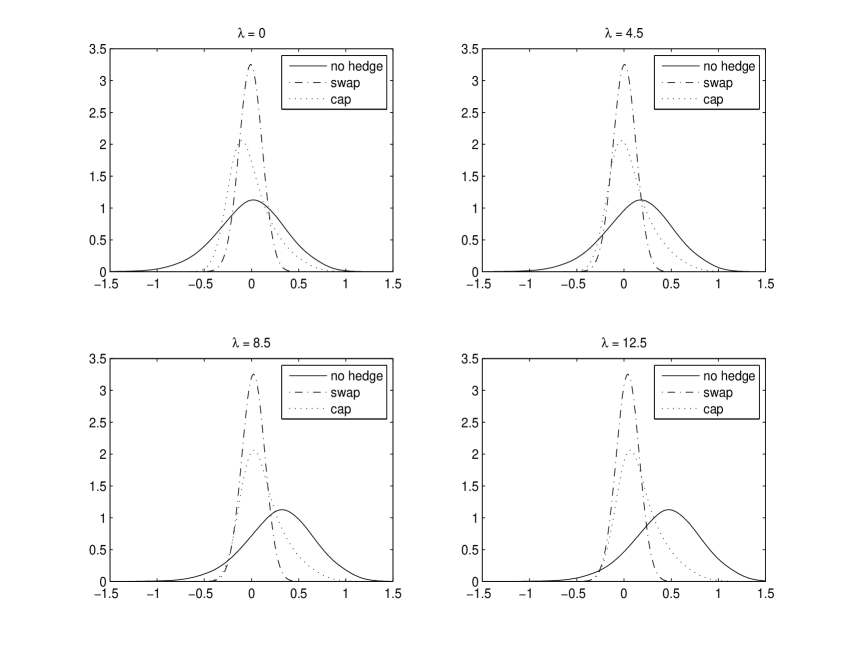

The market price of longevity risk is one of the factors that determines prices of longevity derivatives and life annuity policies. Since payoffs of a longevity swap, a cap and a life annuity are contingent on the same underlying mortality intensity of a cohort, all these products are priced using the same . Figure 7 and Table 4 illustrate the effect of changing on the distributions of an unhedged, a swap-hedged and a cap-hedged annuity portfolio. The degree of longevity risk can be quantified by the standard deviation, the VaR and the ES of the distributions. We observe that increasing leads to the shift of the distribution to the right, resulting in a higher average surplus. On the other hand, changing has no impact on the standard deviation and the skewness of the distribution.

For an unhedged annuity portfolio, a higher leads to higher premium for the life annuity policy since the annuity price is determined by the risk-adjusted survival probability , see Eq. (4.1). In other words, an increase in the annuity price compensates the provider for the longevity risk undertaken when selling life annuity policies. There is also a trade-off between risk premium and affordability. Setting a higher premium will clearly improve the risk and return of an annuity business, it might, however, reduce the interest of potential policyholders. An empirical relationship between implied longevity and annuity prices is studied in Chigodaev et al. (2014).

When life annuity portfolio is hedged using a longevity swap, the standard deviation and the absolute values of the VaR and the ES reduce substantially. The higher return obtained by charging a larger market price of longevity risk in life annuity policies is offset by an increased price paid implicitly in the swap contract (since in Eq. (4.10)). It turns out that as increases an extra return earned in the annuity portfolio and the higher implicit cost of the longevity swap nearly offset each other out on average. The net effect is that a swap-hedged annuity portfolio remains to a great extent unaffected by the assumption on , leading only to a very minor increase in the mean of the distribution.

For a cap-hedged annuity portfolio, the discounted surplus distribution is positively skewed since a longevity cap allows an annuity provider to get exposure to the upside potential when policyholders live shorter than expected. Compared to an unhedged portfolio, the standard deviation and the absolute values of the VaR and the ES are also reduced but the reduction is smaller compared to a swap-hedged portfolio. When increases, we observe that the mean of the distribution for a cap-hedged portfolio increases faster than for a swap-hedged portfolio but slower than for an unhedged portfolio. It can be explained by noticing that when the survival probability of a cohort is overestimated, that is, when annuitants turn out to live shorter than expected, holding a longevity cap has no effect (besides paying the price of a cap for longevity protection at the inception of the contract) while there is a cash outflow when holding a longevity swap, see Eq. (4.10) and Eq. (4.14).

In the longevity risk literature, the VaR and the ES are of a particular importance as they are the main factors determining the capital reserve when dealing with exposure to longevity risk (Meyricke and Sherris (2014)). As shown in Table 4, the difference between a swap-hedged and a cap-hedged portfolio in terms of the VaR and the ES becomes smaller when increases. In fact, for , a longevity cap becomes more effective in reducing the tail risk of an annuity portfolio compared to a longevity swap.171717Given , the VaR and the ES for a swap-hedged portfolio are and respectively. For a cap-hedged portfolio they become and , respectively. This result suggests that a longevity cap, besides being able to capture the upside potential, can be a more effective hedging instrument than a longevity swap in terms of reducing the VaR and the ES when the demanded market price of longevity risk is large.

4.2.2 Hedging Features w.r.t. Term to Maturity

| Mean | Std.dev. | Skewness | VaR0.99 | ES0.99 | |

| Years | |||||

| No hedge | 0.2978 | 0.3592 | -0.2804 | -0.6148 | -0.7973 |

| Swap-hedged | 0.2820 | 0.2911 | -0.3871 | -0.5707 | -0.7490 |

| Cap-hedged | 0.2893 | 0.2989 | -0.2661 | -0.5801 | -0.7592 |

| Years | |||||

| No hedge | 0.2978 | 0.3592 | -0.2804 | -0.6148 | -0.7973 |

| Swap-hedged | 0.1740 | 0.1794 | -0.7507 | -0.3656 | -0.5061 |

| Cap-hedged | 0.2234 | 0.2310 | 0.2006 | -0.3870 | -0.5259 |

| Years | |||||

| No hedge | 0.2978 | 0.3592 | -0.2804 | -0.6148 | -0.7973 |

| Swap-hedged | 0.0204 | 0.0718 | -0.1919 | -0.1547 | -0.1938 |

| Cap-hedged | 0.1205 | 0.2054 | 1.0855 | -0.1903 | -0.2224 |

| Years | |||||

| No hedge | 0.2978 | 0.3592 | -0.2804 | -0.6148 | -0.7973 |

| Swap-hedged | -0.0091 | 0.0668 | 0.0277 | -0.1616 | -0.1869 |

| Cap-hedged | 0.0984 | 0.1999 | 1.1527 | -0.1909 | -0.2131 |

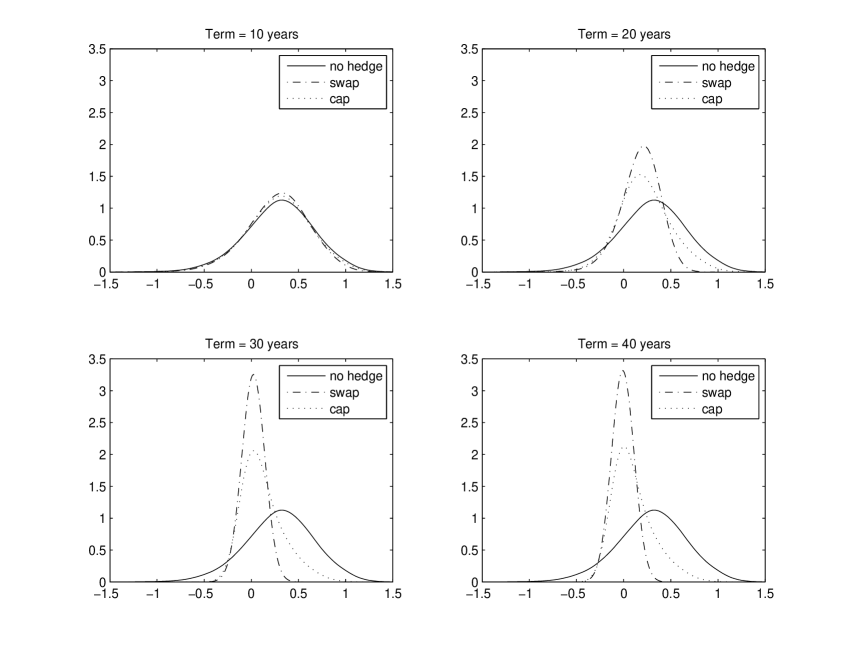

Table 5 and Figure 8 summarize hedging results with respect to the term to maturity of hedging instruments. Due to the long-term nature of the contracts, the hedges are ineffective for years and the standard deviations are reduced only by around for both instruments. The lower left panel of Figure 3 shows that there is little randomness around the realised survival probability for the first few years for a cohort aged 65, and consequently the hedges are insignificant when is short.

The difference in hedge effectiveness between and for both instruments is also insignificant. In fact, the longevity risk underlying the annuity portfolio becomes small after years since the majority of annuitants has already deceased before reaching the age of 95. In our model setup the chance for a 65 years old to live up to 95 is around (Figure 4 with ) and, hence, only around policies will still be in-force after 30 years. Much of the risk left is attributed to idiosyncratic mortality risk, and hedging longevity risk for a small portfolio using index-based instruments is of limited use.

For a swap-hedged portfolio, the standard deviation is reduced significantly when years. The mean surplus, on the other hand, drops to nearly zero since there is a higher cost implied for the hedge with increasing number of S-forwards involved to form the swap as increases.

Similar hedging features with respect to are observed for a longevity cap. However, the skewness of the distribution of a cap-hedged portfolio increases with increasing . It can be explained by noticing that while a longevity cap is able to capture the upside potential regardless of , it provides a better longevity risk protection when is larger. As a result, the distribution of a cap-hedged portfolio becomes more asymmetric when increases.

4.2.3 Hedging Features w.r.t. Portfolio Size

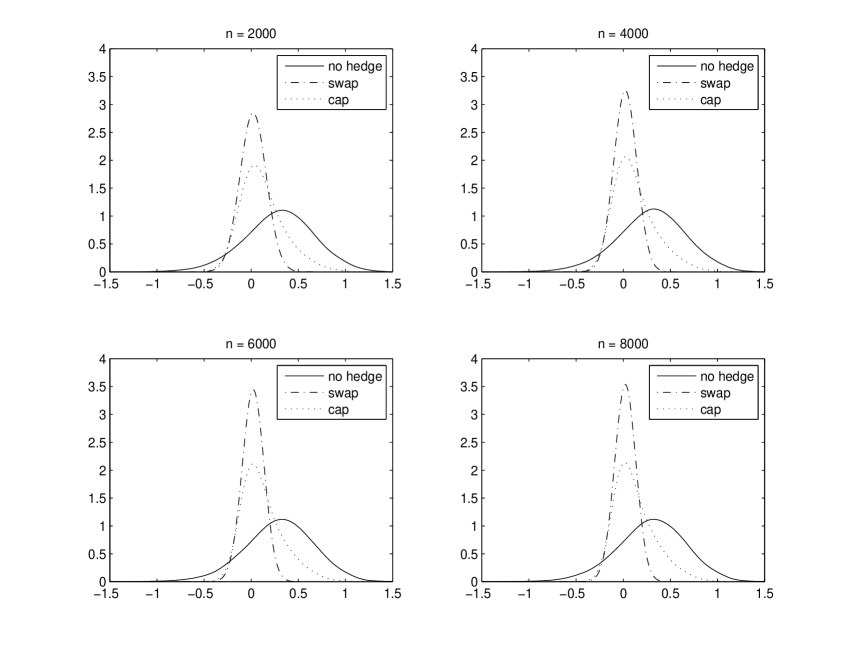

| Mean | Std.dev. | Skewness | VaR0.99 | ES0.99 | |

| No hedge | 0.2973 | 0.3646 | -0.2662 | -0.6360 | -0.8107 |

| Swap-hedged | 0.0200 | 0.0990 | -0.1615 | -0.2120 | -0.2653 |

| Cap-hedged | 0.1200 | 0.2160 | 0.9220 | -0.2432 | -0.2944 |

| No hedge | 0.2978 | 0.3592 | -0.2804 | -0.6148 | -0.7973 |

| Swap-hedged | 0.0204 | 0.0718 | -0.1919 | -0.1547 | -0.1938 |

| Cap-hedged | 0.1205 | 0.2054 | 1.0855 | -0.1903 | -0.2224 |

| No hedge | 0.2977 | 0.3566 | -0.2786 | -0.6363 | -0.8001 |

| Swap-hedged | 0.0204 | 0.0594 | -0.3346 | -0.1259 | -0.1660 |

| Cap-hedged | 0.1204 | 0.2016 | 1.1519 | -0.1639 | -0.2051 |

| No hedge | 0.2982 | 0.3554 | -0.2920 | -0.6060 | -0.7876 |

| Swap-hedged | 0.0209 | 0.0536 | -0.5056 | -0.1190 | -0.1595 |

| Cap-hedged | 0.1209 | 0.1992 | 1.1616 | -0.1598 | -0.1991 |

Table 6 and Figure 9 demonstrate hedging features of a longevity swap and a cap with changing portfolio size . We observe a decrease in standard deviation, as well as the VaR and the ES (in absolute terms) when portfolio size increases. Compared to an unhedged portfolio, the reduction in the standard deviation and the risk measures is larger for a swap-hedged portfolio, compared to a cap-hedged portfolio. Recall that idiosyncratic mortality risk becomes significant when is small. We quantify the effect of the portfolio size on hedge effectiveness by introducing the measure of longevity risk reduction , defined in terms of the variance of the discounted surplus per policy, that is,

| (4.16) |

where and represent the variances of the discounted surplus distribution per policy for a hedged and an unhedged annuity portfolio, respectively. The results are reported in Table 7.

| 2000 | 4000 | 6000 | 8000 | |

|---|---|---|---|---|

Li and Hardy (2011) consider hedging longevity risk using a portfolio of q-forwards and find the longevity risk reduction of and for portfolio size of 10,000 and 3,000, respectively. In contrast to Li and Hardy (2011), we do not consider basis risk and the result of using longevity swap as a hedging instrument leads to a greater risk reduction. Overall, our results indicate that hedge effectiveness for an index-based longevity swap and a cap diminishes with decreasing since idiosyncratic mortality risk cannot be effectively diversified away for a small portfolio size. Even though a longevity cap is less effective in reducing the variance, part of the dispersion is attributed to its ability of capturing the upside of the distribution when survival probability of a cohort is overestimated. From Table 6 we also observe that the distribution becomes more positively skewed for a cap-hedged portfolio when increases, which is a consequence of having a larger exposure to longevity risk with increasing number of policyholders in the portfolio.

5 Conclusion

Life and pension annuities are the most important types of post-retirement products offered by annuity providers to help securing lifelong incomes for the rising number of retirees. While interest rate risk can be managed effectively in the financial markets, longevity risk is a major concern for annuity providers as there are only limited choices available to mitigate the long-term risk. Development of effective financial instruments for longevity risk in capital markets is arguably the best solution available.

Two types of longevity derivatives, a longevity swap and a cap, are analysed in this paper from a pricing and hedging perspective. We apply a tractable Gaussian mortality model to capture the longevity risk, and derive explicit formulas for important quantities such as survival probabilities and prices of longevity derivatives. Hedge effectiveness and features of an index-based longevity swap and a cap used as hedging instruments are examined using a hypothetical life annuity portfolio exposed to longevity risk.

Our results suggest that the market price of longevity risk is a small contributor to hedge effectiveness of a longevity swap since a higher annuity price is partially offset by an increased cost of hedging when is taken into account. It is shown that a longevity cap, while being able to capture the upside potential when survival probabilities are overestimated, can be more effective in reducing longevity tail risk compared to a longevity swap, provided that is large enough. The term to maturity is an important factor in determining hedge effectiveness. However, the difference in hedge effectiveness is only marginal when increases from to years for an annuity portfolio consisting of a single cohort aged 65 initially. This is due to the fact that only a small number of policies will still be in-force after a long period of time (30 to 40 years), and index-based instruments turn out to be ineffective when idiosyncratic mortality risk becomes a larger contributor to the overall risk, compared to systematic mortality risk. The effect of the portfolio size on hedge effectiveness is quantified and compared with the result obtained in Li and Hardy (2011) where population basis risk is taken into account. In addition, we find that the skewness of the surplus distribution of a cap-hedged portfolio is sensitive to the term to maturity and the portfolio size, and, as a result, the difference between a longevity swap and a cap when used as hedging instruments becomes more pronounced for larger and .

As discussed in Biffis and Blake (2014), developing a liquid longevity market requires reliable and well-designed financial instruments that can attract sufficient amount of interests from both buyers and sellers. Besides of a longevity swap, which is so far a common longevity hedging choice for annuity providers, option-type instruments such as longevity caps can provide hedging features that linear products cannot offer. A longevity cap is shown to have alternative hedging properties compared to a swap, and this option-type instrument would also appeal to certain classes of investors interested in receiving premiums by selling a longevity insurance. Further research on the design of longevity-linked instruments from the perspectives of buyers and sellers would provide a further step towards the development of an active longevity market.

Appendix A Appendix

To simulate death times of annuitants, we notice that once a sample of the mortality intensity is obtained, the Cox process becomes an inhomogeneous Poisson process and the first jump times, which are interpreted as death times, can be simulated as follows (see e.g. Brigo and Mercurio (2007)):

-

1.

Simulate the mortality intensity from to .

-

2.

Generate a standard exponential random variable . For example, using an inverse transform method, we have where .

-

3.

Set the death time to be the smallest such that . If then set .

-

4.

Repeat step (2) and (3) to obtain another death time.

The payoff of an index-based hedging instrument depends on the realised survival probability . The payoff of a customised instrument, on the other hand, depends on the proportion of survivors, , underlying an annuity portfolio where the number of deaths, , is obtained by counting the number of simulated death times that are smaller than . Note that

| (A.1) |

and the accuracy of the approximation improves when increases.

References

- Bauer et al. (2010) Bauer, D., Borger, M., Russ, J., 2010. On the pricing of longevity-linked securities. Insurance: Mathematics and Economics 46, 139–149.

- Biffis and Blake (2014) Biffis, E., Blake, D., 2014. Keeping some skin in the game: How to start a capital market in longevity risk transfers. North American Actuarial Journal 18 (1), 14–21.

- Biffis et al. (2014) Biffis, E., Blake, D., Pitotti, L., Sun, A., 2014. The cost of counterparty risk and collateralization in longevity swaps. To appear in: Journal of Risk and Insurance.

- Blackburn and Sherris (2013) Blackburn, C., Sherris, M., 2013. Consistent dynamic affine mortality models for longevity risk applications. Insurance: Mathematics and Economics 53, 64–73.

- Blake and Burrows (2001) Blake, D., Burrows, W., 2001. Survivor bonds: Helping to hedge mortality risk. Journal of Risk and Insurance 68, 339–348.

- Blake et al. (2013) Blake, D., Cairns, A., Coughlan, G., Dowd, K., MacMinn, R., 2013. The new life market. Journal of Risk and Insurance 80(3), 501–557.

- Blake et al. (2006a) Blake, D., Cairns, A., Dowd, K., 2006a. Living with mortality: longevity bonds and other mortality-linked securities. British Actuarial Journal 12 (1), 153–228.

- Blake et al. (2006b) Blake, D., Cairns, A., Dowd, K., MacMinn, R., 2006b. Longevity bonds: Financial engineering, valuation and hedging. Journal of Risk and Insurance 73, 647–672.

- Boyer and Stentoft (2013) Boyer, M. M., Stentoft, L., 2013. If we can simulate it, we can insure it: An application to longevity risk management. Insurance: Mathematics and Economics 52(1), 35–45.

- Brigo and Mercurio (2007) Brigo, D., Mercurio, F., 2007. Interest Rate Models, 2nd Edition. Springer.

- Cairns (2011) Cairns, A., 2011. Modelling and mangement of longevity risk: Approximations to survivor functions and dynamic hedging. Insurance: Mathematics and Economics 49, 438–453.

- Cairns et al. (2006) Cairns, A., Blake, D., Dowd, K., 2006. A two-factor model for stochastic mortality with parameter uncertainty: Theory and calibration. Journal of Risk and Insurance 73(4), 687–718.

- Chigodaev et al. (2014) Chigodaev, A., Milevsky, M. A., Salisbury, T. S., 2014. How long does the market think you will live? Implying longevity from annuity prices. Tech. rep., IFID Center, Canada.

- Dowd (2003) Dowd, K., 2003. Survivor bonds: A comment on blake and burrows. Journal of Risk and Insurance 70(2), 339–348.

- Hari et al. (2008) Hari, N., Waegenaere, A., Melenberg, B., Nijman, T., 2008. Longevity risk in portfolios of pension annuities. Insurance: Mathematics and Economics 42, 505–519.

- Jevtic et al. (2013) Jevtic, P., Luciano, E., Vigna, E., 2013. Mortality surface by means of continuous time cohort models. Insurance: Mathematics and Economics 53(1), 122–133.

- Li and Hardy (2011) Li, J., Hardy, M., 2011. Measuring basis risk in longevity hedges. North American Actuarial Journal 15(2), 177–200.

- LLMA (2010a) LLMA, 2010a. Longevity pricing framework.

- LLMA (2010b) LLMA, 2010b. Technical note: The S-forward.

- Luciano et al. (2012) Luciano, E., Regis, L., Vigna, E., 2012. Delta-Gamma hedging of mortality and interest rate risk. Insurance: Mathematics and Economics 50, 402–412.

- Luciano and Vigna (2008) Luciano, E., Vigna, E., 2008. Mortality risk via affine stochastic intensities: calibration and empirical relevance. Belgian Actuarial Bulletin 8(1), 5–16.

- Meyricke and Sherris (2014) Meyricke, R., Sherris, M., 2014. Longevity risk, cost of capital and hedging for life insurers under solvency II. Insurance: Mathematics and Economics 55, 147–155.

- Ngai and Sherris (2011) Ngai, A., Sherris, M., 2011. Longevity risk management for life and variable annuities: the effectiveness of static hedging using longevity bonds and derivatives. Insurance: Mathematics and Economics 49, 100–114.

- Wang and Yang (2013) Wang, C., Yang, S., 2013. Pricing survivor derivatives with cohort mortality dependence under the Lee-Carter framework. Journal of Risk and Insurance 80(4), 1027–1056.

- Wills and Sherris (2011) Wills, S., Sherris, M., 2011. Integrating financial and demographic longevity risk models: an Australian model for financial applications. UNSW Australian School of Business Research Paper No.2008ACTL05.