Quantile Versions of the Lorenz Curve

Abstract

The classical Lorenz curve is often used to depict inequality in a population of incomes, and the associated Gini coefficient is relied upon to make comparisons between different countries and other groups. The sample estimates of these moment-based concepts are sensitive to outliers and so we investigate the extent to which quantile-based definitions can capture income inequality and lead to more robust procedures. Distribution-free estimates of the corresponding coefficients of inequality are obtained, as well as sample sizes required to estimate them to a given accuracy. Convexity, transference and robustness of the measures are examined and illustrated.

Keywords: confidence interval, Gini index, inequality measures, influence function, quantile density

1 Introduction

The Lorenz curve and the associated Gini coefficient are routinely employed for comparisons of income inequality in various countries. There are also numerous applications of them in the biological, computing, health and social sciences. These concepts have nice mathematical properties, and thus are the subject of numerous theoretical studies; for a recent review see Kleiber, (2005). However, when it comes to statistical inference for the Lorenz curve and the Gini coefficient, thorny issues arise. An excellent review of existing methods and new proposals for estimating the standard error of the Gini coefficient are investigated by Davidson, (2008). However, as this author notes, such methods will not work when the variance of the income distribution is large or fails to exist, and of course this means that they are undermined when there are outliers in the data. Cowell & Victoria-Feser, (1996) show that most of the inequality measures in the econometrics literature are very sensitive to outliers and have unbounded influence functions.

There are methods available for resolving these inferential obstacles. One is to choose a parametric income model and then to find optimal bounded influence estimators for the parameters; for example, Victoria-Feser & Ronchetti, (1994) do this for the gamma and Pareto models. And, Victoria-Feser, (2000) shows how to robustly choose between parametric models and then find robust estimates of inequality indices based on a single data sample, even if it has been grouped or truncated. In a series of papers Cowell & Victoria-Feser, (2002, 2003, 2007) investigate damaging effects of data contamination on transfer properties of various inequality indices, as well as dealing with the effects of truncation of non-positive and/or large data values. They propose semi-parametric models for overcoming these issues.

We go one step further here, redefining the basic concept of the Lorenz curve in terms of quantiles instead of moments, and then determining what has been gained and lost in terms of conceptual clarity, inference and resistance to contamination. Examples of this approach are the standardized median in lieu of the standardized mean, and quantile measures of skewness and kurtosis, rather than the classical moment-based measures, Staudte, (2013b, 2014, 2015). Ratios of quantiles based on one sample are often presented as measures of inequality, and inferential procedures for them are in Prendergast & Staudte, (2015a, b).

The role of quantiles in inequality measures is long-standing. Gastwirth, (1971) observed that the definition of the Lorenz curve could be extended to all distributions having a finite mean by expressing the cumulative income as an integral of the quantile function. More recently Gastwirth, (2012) showed that the inequality coefficient of Gini, (1914) could be made much more sensitive to shifts in income inequality if the mean in its denominator were replaced by the median; this also has the advantage of protecting the coefficient from large outliers. Kampke, (2010) compares the effects of means versus medians on poverty indices. It is in this spirit that we begin in Section 2 by introducing three simple quantile versions of the Lorenz curve for distributions on the positive axis, and their associated coefficients of inequality. Numerous examples demonstrate how these curves and coefficients agree or disagree with the moment-based classical version. In particular, the effects of an income transfer function on the inequality coefficients are illustrated for the Type II Pareto model.

In Section 3 we study empirical versions of these inequality curves and their associated estimated coefficients. The latter estimates are found to have predictable distribution-free standard errors, unlike the sensitive Gini coefficient. For an assumed scale model, confidence intervals for the inequality coefficients are given. It is not surprising that these quantile measures of inequality are resistant to outliers, and in Section 4 we show that they have bounded influence functions.

2 Quantile analogues of the Lorenz curve

2.1 Definitions and basic properties

Let be the class of all cumulative distribution functions with Such will be interpreted as ‘income’ distributions and as the proportion of incomes less than or equal to Define the quantile function associated with at each by . If the support of is infinite; that is for all , this infimum does not exist for , and then we define . When the meaning of is clear, we will sometimes write or for .

The mean income of those with proportion of smallest incomes is , and the mean income of the entire population is defined by Let be the set of for which exists as a finite number. For each the Lorenz curve of is defined by for The lowest proportion of incomes have proportion of the total wealth.

What we are proposing here is to replace , the mean of the proportion of those with wealth less than by its median . In addition, we replace the mean of the entire population by one of three quantile measures of its size: , , or The robustness merits of this last divisor, a symmetric quantile average, are investigated by Brown, (1981).

Definition 1

For and let The three quantile-based functions whose graphs reveal income inequality are defined for each by:

| (1) | |||||

As with we sometimes abbreviate to .

For each the first measure compares the typical (median) wealth of the poorest proportion of incomes with the typical (median) wealth of the entire population. The second measure compares the bottom typical wealth with the top typical wealth; for example corresponds to the popular ‘20-20 rule’, which compares the mean wealth of the lowest 20% of incomes with the largest 20%. For each the third gives the typical wealth of the poorest % incomes, relative to the mid-range wealth of the middle % of incomes. In all cases, extreme incomes are down-weighted because of multiplication by the factor , as it is for the Lorenz curve .

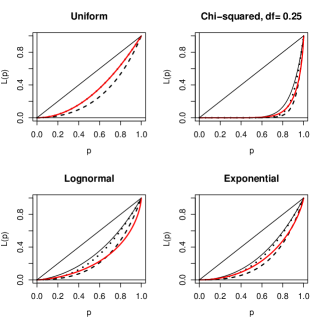

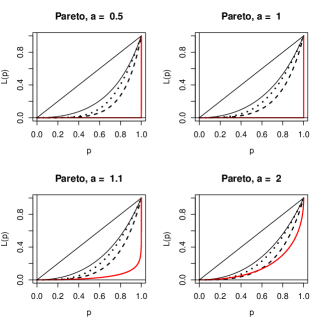

All of these quantile inequality curves are scale invariant and monotone increasing from to , and all satisfy for . Each when all incomes are equal. None are strictly speaking ‘Lorenz’ curves, because they are not convex for all , as examples will show. Nevertheless, for most commonly assumed income distributions , they are convex, see Section 5. Some examples of the quantile curves are depicted in Figures 2-2, which compares their graphs with the Lorenz curve. Note that for the uniform distribution. And, for the log-normal distribution.

2.2 Coefficients of inequality

The relative measure of dispersion, or concentration ratio due to Gini, (1914) is defined for by where are independent and each distributed as , and is the mean of . It is known, see Sen, (1986) for example, to equal twice the area between the Lorenz curve and the diagonal line; it is an indicator, on the scale of 0 to 1, of ‘how far’ the inequality graph is from the diagonal line representing equal incomes; the further it is, the larger the Gini coefficient.

Definition 2

For each of the given in (1) define the respective coefficients of inequality

| (2) |

Specific numerical comparisons of the s are given in Table 1. It lists a variety of ranging from uniform to very long-tailed distributions and the associated values of Gini’s index for the four s. The rankings of different s by these four measures of inequality are seen to be very similar and the Spearman rank correlation of with for and 3 are respectively 0.84, 0.88 and 0.88, for this list of s. For more background material on distributions, see Johnson et al., (1994, 1995).

Proposition 1

Given let denote its median. Choose two incomes independently and randomly from those incomes less than the median, and let It then follows that defined by (2) is given by the relative average distance of from the median. Next define so if is the th quantile of , It then follows that and

Proof: Let have the conditional distribution of given ; then its distribution function for and the distribution of is determined by , for For each of the three integrals in (2), make the change of variable The results are then immediate by observing that each integral with respect to the measure equals the corresponding claimed expected value.

Proposition 1 shows that and for all . It also allows for simple alternative interpretations of the three quantile inequality coefficients defined in (2) which can be compared with Gini’s original definition as a relative measure of concentration. Note that the Gini measure has been criticized for placing too much emphasis on the central part of the distribution. As Proposition 1 shows, the quantile versions can also be criticized for the same reason, because the main ingredient is the maximum of two randomly chosen incomes from the lower half of the population. This maximum arises because in the definition (1) all the ratios are multiplied by , which down-weights ratios involving relatively small and large incomes.

| 1. Uniform | 0.333 | 2 | 0.333 | 4.5 | 0.455 | 3 | 0.333 | 3 | ||||

| 2. | 0.762 | 11 | 0.671 | 13 | 0.792 | 13 | 0.720 | 13 | ||||

| 3. | 0.636 | 7 | 0.525 | 11 | 0.673 | 10 | 0.572 | 10 | ||||

| 4. | 0.423 | 4 | 0.329 | 3 | 0.483 | 4 | 0.361 | 4 | ||||

| 5. | 0.339 | 3 | 0.261 | 2 | 0.406 | 2 | 0.285 | 2 | ||||

| 6. Lognormal | 0.520 | 6 | 0.333 | 4.5 | 0.510 | 5 | 0.388 | 5 | ||||

| 7. Pareto(0.5)11footnotemark: 1 | 1.000 | 13.5 | 0.515 | 10 | 0.704 | 11 | 0.610 | 11 | ||||

| 8. Pareto(1) | 1.000 | 13.5 | 0.455 | 9 | 0.636 | 9 | 0.528 | 9 | ||||

| 9. Pareto(1.5) | 0.741 | 9 | 0.434 | 8 | 0.609 | 8 | 0.497 | 8 | ||||

| 10. Pareto(2) | 0.667 | 8 | 0.424 | 7 | 0.595 | 7 | 0.481 | 7 | ||||

| 11. Weibull(0.25) | 0.937 | 10 | 0.731 | 14 | 0.843 | 14 | 0.787 | 14 | ||||

| 12. Weibull(0.5) | 0.750 | 12 | 0.570 | 12 | 0.720 | 12 | 0.629 | 12 | ||||

| 13. Weibull(1) | 0.500 | 5 | 0.393 | 6 | 0.550 | 6 | 0.432 | 6 | ||||

| 14. Weibull(4) | 0.159 | 1 | 0.136 | 1 | 0.222 | 1 | 0.134 | 1 |

1. The Lorenz curve and Gini coefficient are not defined for distributions with , but if the definition were so extended, would be 0 for and the associated coefficient would be 1.

2.3 Tranference of income

The effect of income transfers on inequality measures is of great interest to economists, see Kleiber, (2005) and Fellman, (2012). The basic idea Dalton, (1920) is that if one transfers income from some members of the population having income above the mean to others having income below the mean, then the inequality measure should reflect this by decreasing. In keeping with our preference for quantiles over moments, we suggest replacing the mean by the median in defining the transference principle for inequality measures.

Definition 3

Given , and let be the median. We define a median preserving transfer (of income) function as one satisfying , for all , and for all .

In words, a median preserving transfer function can only increase income that is less than the median, and only decrease income if it exceeds the median. It follows that for all and for all

The effect on the quantile inequality curves is then easily seen: ; that is, the transfer function can only increase at each . This implies the associated coefficient of inequality (2) satisfies We say that preserves the ordering induced by the transfer function. The reader may readily verify that for the other quantile inequality curves satisfy and hence

For any non-trivial transfer function we will have a positive reduction in the coefficient of inequality. Can we quantify this amount for any specific transfer functions? An example is given in Section 2.4.

2.4 Example of transference

Suppose one wants to increase all incomes less than a specific threshold (say the poverty line) so that they equal . That is; for . This requires an amount per person of to be found, say, by transference from those with incomes above the median or some higher thresh-hold . One possibility is to charge a levy of amount on those with income exceeding , leading to the following transfer function :

| (3) |

In the interest of fairness one could also charge a proportional amount for those with income between and so that for , but this unnecessarily complicates our presentation.

Now jumps from 0 to at , equals for , jumps at from to and equals for . Therefore the quantile function for the transferred income is given by

| (4) |

At this point it is convenient to introduce the th cumulative income by where . As Cowell & Victoria-Feser, (2002) point out, this function is fundamental to analysis of Lorenz curves, and and We want to determine for the Type II Pareto distribution having shape parameter and scale parameter

Now , which has mean and th quantile . Integrating by parts we obtain

| (5) |

where The mean income of the poorest proportion is

For the transfer problem with , we have , so (5) implies

This amount can be obtained by a levy on each income greater than

For the Pareto distribution with parameters , , the median income is 41,421.36 and the mean income is . For , say, the quantities of interest are the poverty line , the mean cumulative income and All those having income greater than the 0.8 quantile would need to pay an impost of .

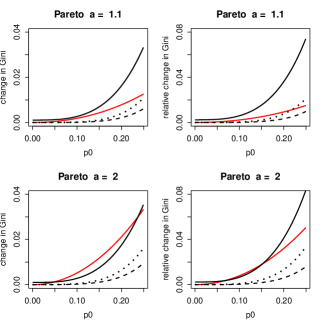

The absolute and relative effects of such a transfer function are depicted in Figure 3 for two income distributions, Pareto with and . For the first distribution, the change in the Gini coefficient is larger than for the and coefficients, but less than that for ; but the relative effect plot shows that the coefficient is most sensitive of the four, especially for near 0.25. For the second distribution both and are roughly the same in terms of sensitivity to changes by transference and again preferable to and

Many other transfer functions and income distributions could be considered, but those are applications beyond the scope of this work. It is important, of course, to identify real changes in coefficients of inequality after implementing a transfer of income. Estimation of is discussed in Section 3. Another factor that we have not included here are the costs of implementation of a transfer function.

3 Estimation of inequality measures

3.1 Empirical quantile inequality curves

Given data with ordered values let and for . The empirical Lorenz curve is then defined as the graph of the piecewise linear connection of the points , . The empirical distribution function defined for each by has inverse for , and so empirical versions of the quantile curves (1) can be expressed in terms of the order statistics. Such curves are discontinuous, but there are several continuous quantile estimators available, including kernel density estimators Sheather & Marron, (1990) and the linear combinations of two adjacent order statistics studied by Hyndman & Fan, (1996). Many of the latter are implemented on the software package Development Core Team, (2008), and here we use the Type 8 version of the quantile command recommended by Hyndman & Fan, (1996). It linearly interpolates between the points , where and is a continuous function of in We also denote this estimator .

Definition 4

All of the curves defined by (1) are functions of the quantile function , so given the estimator one can by substitution obtain estimators of each of the for any in we call these estimators for and 3.

3.2 Empirical coefficients of inequality

With few exceptions, such as the uniform distribution, one cannot analytically compute the s, but using modern software packages such as R Development Core Team, (2008), it is easy to get very good approximations to them for many of interest as follows.

Definition 5

Given a large integer define a grid in (0,1) with increments of size by , for Then evaluate the quantile function for in the grid and find for each and 3.

Clearly one can make as close to as desired by choosing sufficiently large. We will estimate , and hence , as follows. Let be the estimated inequality curve value at , for each in the grid. Then is defined by

| (6) |

In our computations, we used . Hereafter we write for and for but it is understood that these are computed on a grid with increments

3.3 Simulation studies

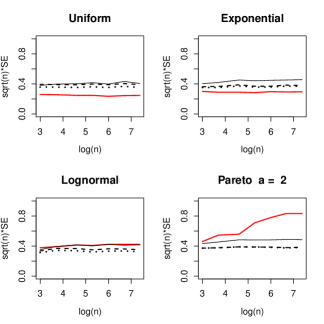

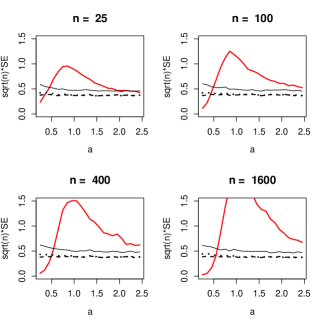

It will be seen that despite the fact that the values of the quantile coefficients of inequality vary greatly over the range of in Table 1, the standard errors of estimation are fairly predictable. By ‘standard error’ of , we mean the square root of the mean squared error. Initial simulations suggested that and so in Figure 5 we show some examples of , plotted as a function of for ranging from 20 to 1600. These plots are based on 1000 replications at each of the selected values of for various . In all four plots it is seen that the standard errors of while is a little larger. This enables one to choose a sample size which guarantees a desired standard error for each of the three estimators. Attempting to estimate Gini’s coefficient of inequality by means of the Lorenz curve areas has no such simple sample size solution.

It is also interesting to plot versus as in Figure 5, where denotes the Pareto distribution with shape parameter ranging from . Again all three standard errors of the estimated inequality coefficients derived from the -curves are well behaved, but those for the Lorenz curve are quite irregular. For the Lorenz curve is not defined because but if one defines the curve to be 0 in this case the corresponding measure of inequality is 1 and this can be estimated. Even if one restricts attention to , these plots show that for increasing the standard error is growing at a faster rate than the others, (because for the variance of is infinite).

The results in Table 2 suggest that one can choose the minimum sample size required to obtain ; it is . So for example, for standard error , one needs . Note that this accuracy is achieved for all in Table 2. Similarly for the required sample size is a little smaller

| 25 | 100 | 25 | 100 | 25 | 100 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Uniform | 0.40 | 0.40 | 0.421 | 0.38 | 0.39 | 0.399 | 0.35 | 0.35 | 0.361 | ||

| 2. | 0.55 | 0.55 | 0.550 | 0.39 | 0.38 | 0.359 | 0.43 | 0.43 | 0.405 | ||

| 3. | 0.50 | 0.53 | 0.521 | 0.40 | 0.41 | 0.402 | 0.42 | 0.44 | 0.427 | ||

| 4. | 0.39 | 0.40 | 0.408 | 0.34 | 0.36 | 0.351 | 0.31 | 0.33 | 0.316 | ||

| 5. | 0.32 | 0.33 | 0.337 | 0.30 | 0.32 | 0.305 | 0.26 | 0.27 | 0.253 | ||

| 6. Lognormal | 0.39 | 0.40 | 0.417 | 0.34 | 0.35 | 0.351 | 0.32 | 0.32 | 0.322 | ||

| 7. Pareto(0.5) | 0.53 | 0.54 | 0.540 | 0.38 | 0.39 | 0.351 | 0.41 | 0.42 | 0.370 | ||

| 8. Pareto(1) | 0.49 | 0.50 | 0.507 | 0.37 | 0.38 | 0.371 | 0.38 | 0.39 | 0.376 | ||

| 9. Pareto(1.5) | 0.46 | 0.47 | 0.492 | 0.36 | 0.38 | 0.379 | 0.36 | 0.38 | 0.380 | ||

| 10. Pareto(2) | 0.45 | 0.46 | 0.485 | 0.37 | 0.38 | 0.381 | 0.37 | 0.38 | 0.379 | ||

| 11. Weibull(0.25) | 0.55 | 0.53 | 0.540 | 0.35 | 0.34 | 0.330 | 0.40 | 0.39 | 0.384 | ||

| 12. Weibull(0.5) | 0.53 | 0.53 | 0.550 | 0.38 | 0.39 | 0.387 | 0.41 | 0.42 | 0.422 | ||

| 13. Weibull(1) | 0.44 | 0.45 | 0.461 | 0.37 | 0.38 | 0.382 | 0.36 | 0.37 | 0.370 | ||

| 14. Weibull(4) | 0.19 | 0.19 | 0.195 | 0.20 | 0.21 | 0.207 | 0.14 | 0.14 | 0.140 | ||

3.4 Confidence intervals for the coefficients of inequality

Recall from (6) that for each and large fixed the estimated coefficient of inequality is Now the estimate , as a ratio of finite linear combinations of quantile estimates, is consistent for , so is also consistent for . Further, Prendergast & Staudte, (2015b) show that is asymptotically normal with mean 0 and variance depending on certain quantiles and quantile densities of the underlying . Beach & Davidson, (1983) find the limiting joint normal distribution of estimates of a finite number of Lorenz curve ordinates, based on a finite number of sample quantiles, assuming that where is specified in Definition 6. In the same way, for , the limiting joint normal distribution of the estimated ordinates , can be established. We do not need an analytic expression for the covariance matrix, because we only require the asymptotic normality of the estimated , which being an average of the , is immediate. Its asymptotic variance is available from the expected value of the squared influence function see (9) and (4.3).

Here we present the results of a modest simulation study of confidence intervals for of the form , with nominal coefficient 95% , with results in Table 3. For the lognormal distribution, the respective found in Table 2 are respectively 0.417, 0.351 and 0.322. For the Pareto with distribution, these values are 0.485, 0.381 and 0.379.

To obtain distribution-free confidence intervals for , one needs consistent estimates for the asymptotic variance , a project beyond the scope of this work.

| 25 | 100 | 400 | 25 | 100 | 400 | 25 | 100 | 400 | |||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Lognormal | 0.967 | 0.956 | 0.951 | 0.954 | 0.947 | 0.947 | 0.954 | 0.946 | 0.948 | ||

| 0.327 | 0.164 | 0.082 | 0.275 | 0.138 | 0.069 | 0.252 | 0.126 | 0.063 | |||

| Pareto(2) | 0.966 | 0.960 | 0.956 | 0.955 | 0.952 | 0.951 | 0.954 | 0.951 | 0.950 | ||

| 0.380 | 0.190 | 0.095 | 0.299 | 0.149 | 0.075 | 0.297 | 0.149 | 0.074 | |||

4 Robustness properties

In this section we show that the quantile inequality curves and their associated coefficients of inequality have bounded influence functions, which guarantees that a small amount of contamination can only have a limited effect on the asymptotic bias of estimators of these quantities. For background material on robustness concepts for functionals, see Hampel et al., (1986), although we attempt to make the presentation self-contained. To this end, we must restrict to the following subclass of smooth distributions:

Definition 6

In order to find the influence function of the -curves at any specific in we also require the mixture distribution which places positive probability the point (the contamination point) and on the income distribution . Formally, it is defined for each by , where is the indicator function. The influence function for any functional is then defined for each as the . The influence function of the th quantile functional , where of Definition 6, is well-known to be (Staudte & Sheather,, 1990, p.59)

| (8) |

where and is given by (7).

One can show that and . One reason for calculating this variance is that it arises in the asymptotic variance of the functional applied to the empirical distribution , namely . That is, in distribution; and sometimes a simple expression for the asymptotic variance is not otherwise available.

4.1 Influence functions of quantile inequality curves

Cowell & Victoria-Feser, (2002) show that the influence function of the Lorenz curve at the point is unbounded, implying that a small amount of contamination can lead to a large bias in estimation of its value; on the other hand the quantile inequality curves proposed here all have bounded influence functions, provided only that To see this, note that each where , and are all quantile functionals or an average of them.

Proposition 2

The influence function of the functional defined by is a multiple of the derivative of the ratio of two functionals, so by elementary calculus we have for each

For each case and 3 one only requires substitution of the respective quantile influence functions for the s found in (8).

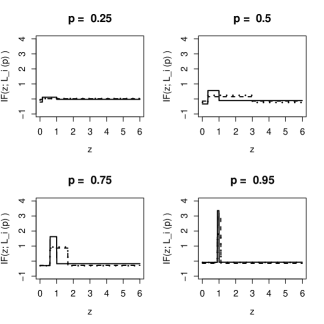

While these influence functions are complicated, the are easy to compute and plot using currently available software. Specific examples are shown Figure 7 when the underlying is the Pareto distribution with shape parameter and are plotted as functions of a possible contamination at

For small there is very little influence on of contamination at any point . However, as increases, there is a noticeable increase in influence on for near the median, which equals one in this case. Contamination at near zero is slightly negative, then rises to a positive relatively large positive peak as approaches the median, and then drops to a small negative and constant influence again as increases past the median. This is to be expected, because when the median is pulled to the left by contamination, then is increased, but when the median is pulled to the right, the values of are decreased.

The other two are similarly affected by contamination at , but to a lesser extent. Plots of the influence functions of the quantile inequality curves for other Pareto() distributions (not shown) are similar to those in Figure 7, and again the peak is located at the median . Similar influence function plots are obtained for uniform, lognormal and Weibull distributions, again with peaks near their respective medians.

4.2 Influence of contamination at on the graph

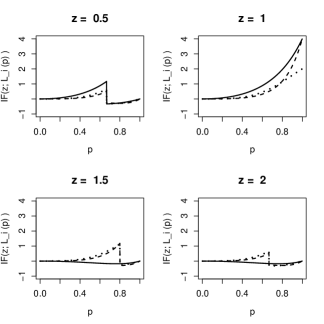

We have found, for each fixed , the influence functions . Now we consider, for fixed , the graph , which shows the influence of contamination at on the respective inequality curves Examples are shown in Figure 7, again for the Pareto () distribution, and selected values of .

First we concentrate on only the solid lines corresponding to . Inspection of (9) shows that the discontinuity points are and . Now if and only if . Thus in the upper left plot of Figure 7 where there are only two cases of interest: and ; in the first interval the influence of contamination at on the -curve is positive and increasing in , but its influence is negative for in For the top right plot so the influence of contamination at the median on the -curve is positive and increasing for all . For the other two plots exceeds the median and there is only a slight negative influence of on the -curve for all .

The influence of contamination at on the graphs of , is also shown in Figure 7 as dashed and dotted lines, respectively. Such influence is similar to that on in the top two plots where does not exceed the median. But in the lower plots where exceeds the median, the contamination is positive and increasing on and negative for larger . For the bottom left plot this interval is , and for the bottom right it is . Details are left as an exercise for the reader. Further increasing the values of only diminishes its effect on the graphs.

4.3 Influence functions of quantile coefficients of inequality

The influence functions of the inequality coefficients associated with the -curves are easily found, because the functional , which contains an average of values over .

Proposition 3

For each and 3 the influence function of the inequality coefficients are given respectively by

| (9) |

One only needs to justify taking the derivative with respect to at under the integral sign. An argument based on the Leibniz Integration Rule is given in the Appendix.

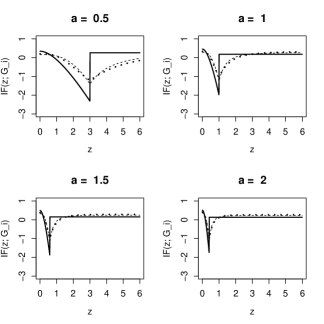

Figure 8 gives plots of the influence functions of the inequality coefficients when is the Pareto distribution for selected values of . The biggest influence of contamination occurs at

5 Convexity of the quantile inequality curves

One of the nice mathematical properties of the Lorenz curve is that it is convex for all distributions . The quantile-based versions (1) are defined for all in the larger class , but need not be convex. In particular, empirical versions are often not convex over . The following examples demonstrate that for the more commonly assumed income distributions, the quantile inequality curves are convex. See Johnson et al., (1994, 1995) for background material on these distributions.

5.1 Non-convex example

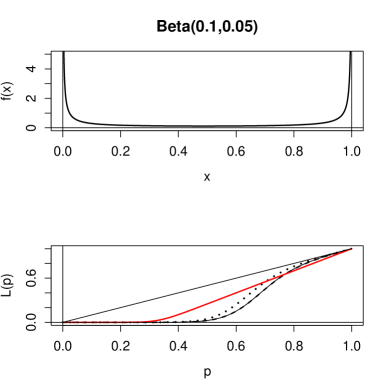

Figure 9 shows that for the very U-shaped Beta distribution with parameters only the Lorenz curve is convex. This distribution appears to have a symmetric density, but in fact is quite asymmetric, with mean 2/3, and the quartiles 0.050,0.997, and 1.000, to three decimal places. The inequality coefficients are , , and Note that the Gini coefficient , its value for the uniform distribution, a non-intuitive result to us.

Other plots, not shown, for parameters , and indicate that all four curves are convex.

| Exponential | |||||

|---|---|---|---|---|---|

| Normal | |||||

| Lognormal | |||||

| Type I Pareto | |||||

| Type II Pareto | |||||

| Weibull |

5.2 Convex examples

Example 1. Uniform.

Starting with , we find and , all clearly convex functions of in (0,1).

Example 2. Exponential.

Here , so where . Similarly, and and it is not difficult to show that both and so that , and are all convex.

Example 3. Lognormal.

It is ‘obvious’ from the lower left plot in Figure 2 that all three curves are convex on (0,1) for the lognormal distribution. Proving it using the calculus is not as straightforward as one might expect. Note that , Further, observe that and that is not convex, so one cannot use the fact that two monotone increasing convex functions is convex. Taking derivatives,

Thus if and only if and this again, while obvious from a plot, is not readily verified.

Next consider . The argument is very similar to that for :

Thus if and only if , a weaker condition than required for convexity of .

Finally, consider . It suffices to show that is convex in and this is readily verified.

Example 4. Type I Pareto.

For the Type I Pareto distribution where , . Let which is positive. Then so that is convex. Similarly, so that is also convex. The expression for is much more complicated although plots and computational minimization reveal that convexity holds. For example, over all and , min (at and ).

Example 5. Type II Pareto.

For the Type II Pareto distribution where , . We then have that

so that is convex. Both and are complicated expressions although computational minimization reveals non-negative minimums over all and .

Example 6. Weibull.

For the Weibull distribution with shape parameter , we have

The term is a decreasing function in with limit equal to -2 as approaches 0. Consequently, so that is convex. For and , again we used computational minimization for all values up to 100. Neither had a negative minimum so both were found to be convex.

6 Summary and further research

We have shown that quantile versions of the Lorenz curve have most of the properties of the original definition, with two exceptions. The first exception is convexity, which is not satisfied for some very U-shaped distributions and many empirical ones. Nevertheless, for all continuous distributions commonly used to model population incomes, the quantile versions are convex.

The second exception is the first order transference principle, which is mean-centric. When replaced by a median-centric definition, this principle is satisfied for all three quantile versions of the Lorenz curve. We then studied a specific example of a transfer function and showed how it could be measured by the associated inequality coefficients, defined as twice the area between the quantile inequality curve and the equity diagonal. These inequality coefficients can also be interpreted as expected values of certain functions of independent randomly drawn incomes from the population.

These concepts have distinct advantages over the traditional Lorenz curve and Gini index. They are defined for all positive income distributions, and their influence functions are bounded. Distribution-free confidence intervals for the ordinates of inequality curves at fixed points are readily found, since they are just ratios of finite linear combinations of quantiles. In addition, we showed that the standard errors of estimates for the quantile analogues of the Gini coefficient do not appear to depend much on the underlying population model, so that sample sizes can be chosen in advance to obtain desired standard errors. Simulation studies suggest that these sample inequality coefficients approach normality very rapidly, and confidence intervals for them can be constructed when the underlying scale family is known. One way to obtain distribution-free confidence intervals for them would be to find distribution-free estimates of their standard errors, which involves quantile density estimation.

Many other challenges remain. It would be good to have simple necessary and sufficient conditions in terms of the underlying income distribution for convexity of each of the inequality curves. If one is interested in confidence bands for the quantile curves, one could utilize functionals of the quantile process to determine them, starting with the results in Doss & Gill, (1992). Finally, applications to other fields which use diversity indices Patil & Taillie, (1982) would be of interest, as well as connections to the ‘Lorenz dominance’ literature, see Aaberge & Mogstad, (2011) and references therein.

References

- Aaberge & Mogstad, (2011) Aaberge, M., & Mogstad, R. 2011. Robust inequality measures. Journal of Economic Inequality, 9(3), 353–371.

- Beach & Davidson, (1983) Beach, C.M., & Davidson, R. 1983. Distribution-free statistical inference with lorenz curves and income shares. Review of Economic Studies, L, 723–735.

- Brown, (1981) Brown, B.M. 1981. Symmetric quantile averages and related estimators. Biometrika, 68(1), 235–242.

- Cowell & Victoria-Feser, (1996) Cowell, F.A., & Victoria-Feser, M.P. 1996. Robustness properties of inequality measures. Econometrica, 64(1), 77–101.

- Cowell & Victoria-Feser, (2002) Cowell, F.A., & Victoria-Feser, M.P. 2002. Welfare rankings in the presence of contaminated data. Econometrica, 70(3), 1221–1233.

- Cowell & Victoria-Feser, (2003) Cowell, F.A., & Victoria-Feser, M.P. 2003. Distribution-free inference for welfare indices under complete and incomplete information. The Journal of Economic Inequality, 1(3), 191–219.

- Cowell & Victoria-Feser, (2007) Cowell, F.A., & Victoria-Feser, M.P. 2007. Robust stochastic dominance: A semi-parametric approach. The Journal of Economic Inequality, 5(1), 21–37.

- Dalton, (1920) Dalton, H. 1920. The measurement of the inequality of incomes. Economic Journal, 30, 348–361.

- Davidson, (2008) Davidson, R. 2008. Reliable inference for the Gini index. Journal of Econometrics, 150, 30–40.

- Development Core Team, (2008) Development Core Team, R. 2008. R: A language and environment for statistical computing. R Foundation for Statistical Computing, Vienna, Austria. ISBN 3-900051-07-0.

- Doss & Gill, (1992) Doss, H., & Gill, R.D. 1992. An elementary approach to weak convergence for quantile processes. Journal of the American Statistical Association, 87, 869–877.

- Fellman, (2012) Fellman, J. 2012. Properties of Lorenz curves for transformed income distributions. Theoretical Economics Letters, 2, 487–493.

- Gastwirth, (1971) Gastwirth, J.L. 1971. A general definition of the Lorenz curve. Econometrika, 39, 1037–1039.

- Gastwirth, (2012) Gastwirth, J.L. 2012. A robust Gini-type index better detects in the income distribution: a reanalysis of income distribution in the United States from 1967-2011. SSRN Electronic Journal. DOI: 10.2139/ssrn.2164745.

- Gini, (1914) Gini, C. 1914. Sulla misura della concentrazione e della variabilit‘a dei caratteri. Atti del Reale Istituto Veneto di Scienze, Lettere ed Arti, 73, 1203–1248. English translation (2005) in Metron Vol. 63, pp. 3–38.

- Hampel et al., (1986) Hampel, F.R., Ronchetti, E.M., Rousseeuw, P.J., & Stahel, W.A. 1986. Robust Statistics: The Approach Based on Influence Functions. New York: John Wiley and Sons.

- Hyndman & Fan, (1996) Hyndman, R.J., & Fan, Y. 1996. Sample quantiles in statistical packages. The American Statistician, 50, 361–365.

- Johnson et al., (1994) Johnson, N.L., Kotz, S., & Balakrishnan, N. 1994. Continuous Univariate Distributions. Vol. 1. New York: John Wiley & Sons.

- Johnson et al., (1995) Johnson, N.L., Kotz, S., & Balakrishnan, N. 1995. Continuous Univariate Distributions. Vol. 2. New York: John Wiley & Sons.

- Kampke, (2010) Kampke, T. 2010. The use of mean values vs. medians in inequality analysis. Journal of Economic and Social Measurement, 35, 43–62.

- Kleiber, (2005) Kleiber, C. 2005. The Lorenz curve in Economics and Econometrics. Technical Report 30. University of Dortmund, SFB 475.

- Parzen, (1979) Parzen, E. 1979. Nonparametric statistical data modeling. Journal of the American Statistical Association, 7, 105–131.

- Patil & Taillie, (1982) Patil, G.P., & Taillie, C. 1982. Diversity as a concept and its measurement. Journal of the American Statistical Association, 77, 548–561.

- Prendergast & Staudte, (2015a) Prendergast, L.A., & Staudte, R.G. 2015a. Exploiting the Quantile Optimality Ratio to Obtain Better Confidence Intervals of Quantiles. arXiv preprint arXiv:1505.04234.

- Prendergast & Staudte, (2015b) Prendergast, L.A., & Staudte, R.G. 2015b. When large n is not enough-Distribution-free Interval Estimators for Ratios of Quantiles. arXiv preprint arXiv:1508.06321v2.

- Sen, (1986) Sen, P.K. 1986. The Gini coefficient and poverty indexes: some reconciliations. Journal of the American Statistical Association, 81, 1050–1057.

- Sheather & Marron, (1990) Sheather, S.J., & Marron, J.S. 1990. Kernel quantile estimators. Journal of the American Statistical Association, 85, 410–416.

- Staudte, (2013b) Staudte, R.G. 2013b. Distribution-free confidence intervals for the standardized median. STAT, 2(1), 184–196.

- Staudte, (2014) Staudte, R.G. 2014. Inference for quantile measures of skewness. Test, 23(4), 751–768.

- Staudte, (2015) Staudte, R.G. 2015. Inference for quantile measures of kurtosis, peakedness and tail-weight. Communications in Statistics. In press.

- Staudte & Sheather, (1990) Staudte, R.G., & Sheather, Simon J. 1990. Robust Estimation and Testing. New York: Wiley.

- Tukey, (1965) Tukey, J.W. 1965. Which part of the sample contains the information? Proceedings of the Mathemetical Academy of Science USA, 53, 127–134.

- Victoria-Feser, (2000) Victoria-Feser, M.P. 2000. Robust methods for the analysis of income distribution, inequality and poverty. International Statistical Review, 68(3), 277–293.

- Victoria-Feser & Ronchetti, (1994) Victoria-Feser, M.P., & Ronchetti, E. 1994. Robust methods for personal-income distribution models. The Canadian Journal of Statistics, 22(2), 247–258.

7 Appendix: Proof of Proposition 3

The interchange of limit (as ) and integral is justified by the Leibniz Integral Rule. It requires that be continuous in , and bounded in absolute value for by an integrable function.

Proof for .

Proof for .

For we have

| (11) |

The first term in the last line of (7) is bounded above by and it has already been shown that was integrable on (0,1).

Next we show that the second term is bounded by an integrable function. Let and make the change of variable to obtain:

| (12) | |||||

This shows that is bounded on by an integrable function.

Proof for .

Let so is the median, and It is immediate that and that

Consider bounding by an integrable function.

| (13) |

The first term , which has already shown to be integrable. The third term shown to be integrable in (12). The second term using the fact that . Therefore is bounded by an integrable function.