Spherical Cap Packing Asymptotics

and Rank-Extreme Detection

Abstract

We study the spherical cap packing problem with a probabilistic approach. Such probabilistic considerations result in an asymptotic sharp universal uniform bound on the maximal inner product between any set of unit vectors and a stochastically independent uniformly distributed unit vector. When the set of unit vectors are themselves independently uniformly distributed, we further develop the extreme value distribution limit of the maximal inner product, which characterizes its uncertainty around the bound.

As applications of the above asymptotic results, we derive (1) an asymptotic sharp universal uniform bound on the maximal spurious correlation, as well as its uniform convergence in distribution when the explanatory variables are independently Gaussian distributed; and (2) an asymptotic sharp universal bound on the maximum norm of a low-rank elliptically distributed vector, as well as related limiting distributions. With these results, we develop a fast detection method for a low-rank structure in high-dimensional Gaussian data without using the spectrum information.

Index Terms:

Spherical cap packing, extreme value distribution, spurious correlation, low-rank detection and estimation, high-dimensional inference.I Introduction

In modern data analysis, datasets often contain a large number of variables with complicated dependence structures. This situation is especially common in important problems such as the relationship between genetics and cancer, the association between brain connectivity and cognitive states, the effect of social media on consumers’ confidence, etc. Hundreds of research papers on analyzing such dependence have been published in top journals and conferences proceedings. For a comprehensive review of these challenges and past studies, see [1].

One of the most important measures on the dependence between variables is the correlation coefficient, which describes their linear dependence. In the new paradigm described above, understanding the correlation and the behavior of correlated variables is a crucial problem and prompts data scientists to develop new theories and methods. Among the important challenges of a large number of variables on the correlation, we focus particularly on the following two questions:

-

•

The maximal spurious sample correlation in high dimensions. The Pearson’s sample correlation coefficient between two random variables and based on observations can be written as

(I.1) where ’s and ’s are the independent and identically distributed (i.i.d.) observations of and respectively, and and are the sample means of and respectively. The sample correlation coefficient possesses important statistical properties and was carefully studied in the classical case when the number of variables is small compared to the number of observations. However, the situation has dramatically changed in the new high-dimensional paradigm [2, 1] as the large number of variables in the data leads to the failure of many conventional statistical methods. For sample correlations, one of the most important challenges is that when the number of explanatory variables, , in the data is high, simply by chance, some explanatory variable will appear to be highly correlated with the response variable even if they are all scientifically irrelevant [3, 4]. Failure to recognize such spurious correlations can lead to false scientific discoveries and serious consequences. Thus, it is important to understand the magnitude and distribution of the maximal spurious correlation to help distinguish signals from noise in a large- situation.

-

•

Detection of low-rank correlation structure. Detecting a low-rank structure in a high-dimensional dataset is of great interest in many scientific areas such as signal processing, chemometrics, and econometrics. Current rank estimation methods are mostly developed under the factor model and are based on the principal component analysis (PCA) [5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19, 20, 21], where we look for the “cut-off” among singular values of the covariance matrix when they drop to nearly 0. These methods also usually assume a large sample size. However, in practice often a large number of variables are observed while the sample size is limited. In particular, PCA based methods will fail when the number of observations is less than the rank. Moreover, although we may get low-rank solutions to many problems, more detailed inference on the rank as a parameter is not very clear. Probabilistic statements on the rank, such as confidence intervals and tests, would provide useful information about the accuracy of these solutions. The computation complexity of the matrix calculations can be an additional issue in practice. In summary, it is desirable to have a fast detection and inference method of a low-rank structure in high dimensions from a small sample.

Our study of the above two problems starts with the following question: Suppose points are placed on the unit sphere in If we now generate a new point on according to the uniform distribution over the sphere, how far will it be away from these existing points?

Intuitively, this minimal distance between the new point and the existing points should depend on and , in a manner that it is decreasing in and increasing in Yet, no matter how these existing points are located, this new point cannot get arbitrarily close to the existing points due to randomness. In other words, for any and there is an intrinsic lower bound on this distance that the new point can get closer to the existing points only with very small probability.

Studies of this intrinsic lower bound in the above question have a long history under the notion of spherical cap packing, and this question has been one of the most fundamental questions in mathematics [22, 23, 24]. In fact, this question is closely related to the 18th question on the famous list from David Hilbert [25]. This question is also a very important problem in information theory and has been studied in coding, beamforming, quantization, and many other areas [26, 27, 28, 29, 30, 31, 32, 33].

Besides the importance in mathematics and information theory, this question is closely connected to the two problems that we propose to investigate. For instance, the sample correlation between and can be written as the inner product

| (I.2) |

where and is the vector in with all ones. In general, if we observe i.i.d. samples from the joint distribution of , the sample correlations between ’s and can be regarded as inner products in between the unit vectors corresponding to ’s and another unit vector corresponding to Note that these unit vectors are all orthogonal to the vector due to the centering process. Thus, they lie on an “equator” of the unit sphere in which is in turn equivalent to Through this connection, the problem about the maximal spurious correlation is equivalent to the packing of the inner products, and existing methods and results from the packing literature can be borrowed to analyze this problem. In this paper, we particularly focus on probabilistic statements about such packing problems.

An important advantage of this packing perspective is a view of data that is free of an increasing . Suppose we view the data as points in a -dimensional space, then if exceeds all the points will lie on a low-dimensional hyperplane in This degeneracy forces us to change the methodology towards statistical problems, i.e., changing from the classical statistical methods to recent high-dimensional methods [34, 35]. However, if we view the data as vectors in , then we will never have such a degeneracy problem. No matter how large is, a packing problem is always a well-defined packing problem. Neither the theory nor the methodology needs to be changed due to an increase in . Thus, with the packing perspective, theory and methodology can be set free from the restriction of an increasing .

We summarize below our results on the asymptotic theories of the maximal inner products and spurious correlations. One major advantage of the packing approach is that instead of usual iterative asymptotic results which set and let our convergence results are uniform in , which leads to double limits in both and .

-

•

We characterize the largest magnitude of independent inner products (or spurious correlations) through an asymptotic bound. This bound is universal in the sense that it holds for arbitrary distributions of ’s (or that of ’s). This bound is uniform in the sense that it holds asymptotically in but is uniform over This bound is sharp in the sense that it can be attained, especially when the unit vectors ’s are i.i.d. uniform (or when ’s are independently Gaussian). Thus, in an analogy, this bound is to the distribution of independent inner products (or to that of spurious correlations) as the fundamental bound is to the -dimensional Gaussian distribution [36]. We refer this bound as the Sharp Asymptotic Bound for indEpendent inner pRoducts (or spuRious corrElations), abbreviated as the SABER (or SABRE).

-

•

In the special important case when the set of unit vectors are i.i.d. uniformly distributed (or when ’s are independently Gaussian distributed), we show the sharpness of the SABER (or SABRE) and describe a smooth phase transition phenomenon of them according to the limit of . Furthermore, we develop the limiting distribution by combing the packing approach with extreme value theory in statistics [36, 37]. The extreme value theory results accurately characterize the deviation from the observed maximal magnitude of independent inner products (or that of spurious correlations) to the SABER (or SABRE). One important feature of these results is that they are not only finite sample results but also are uniform--large- asymptotics that are widely applicable in the high-dimensional paradigm.

The spherical cap packing asymptotics can be also applied to the problem of the detection of a low-rank linear dependency. For this problem, we observe that the largest magnitude among standard elliptical variables is closely related to the rank of their correlation matrix. This is seen by decomposing elliptically distributed random vectors into the products of common Euclidean norms and inner products of unit vectors in , thus reducing the problem to one of spherical cap packing. As a consequence, the previous asymptotics can be applied here. We thus obtained a universal sharp asymptotic bound for the maximal magnitude of a degenerate elliptical distribution, as well as its limiting distribution when the unit vectors in the decomposition are i.i.d. uniform. Although many asymptotic bounds and limiting distributions on full rank maxima are well developed under different situations (see [36, 38, 37] for reviews of the extensive existing literature), we are not able to find similar theory in literature on low-rank maxima from elliptical distributions, not even in the special case of Gaussian distribution. We refer the connection we found between the maximal magnitude and the rank as the rank-extreme (ReX) association.

Based on the asymptotic results on the degenerate elliptical distributions, we show that one can make statistical inference on a low-rank through the distributions of the extreme value as a statistic. One feature of this procedure is that it does not require the spectrum information from PCA. Thus, the new method works when , when PCA based methods fail to work. It is also computationally fast since no matrix multiplication is needed in the algorithm. These advantages allow a fast detection of a low-dimensional correlation structure in high-dimensional data.

I-A Related Work

We are not able to find similar probabilistic statements on uniform--large- asymptotics. The following statistical papers are related to the study on the maximal spurious correlation.

-

•

In [4], the authors obtain a result on the order of the maximal spurious correlations in the regime that Through the packing approach, we derive the explicit limiting distribution of the extreme spurious correlations for entire scope of and

-

•

In [39], the authors develop a threshold for marginal correlation screening with large and small The threshold appears in a similar form as the SABRE. We note two major differences between the results: (1) The results in [39] focus on the regime when (i.e., when the threshold converges to 1), while our asymptotic results cover the entire scope of and , and the SABRE is shown to be valid from 0 to 1; (2) we derive the explicit limiting distribution of the maximal spurious correlation in the most important case when the variables are i.i.d. Gaussian.

-

•

In [40, 41, 42], the minimal pairwise angles between i.i.d. uniformly random points on spheres are considered. A similar phase transition is described, and results on the limiting distribution are developed. We note two major differences between their results and ours: (1) Due to different motivations of the research, we focus on the marginal correlation between one response variable and explanatory variables. We also develop a universal uniform bound for marginal correlations. (2) The extreme limiting distributions in their papers are stated separately according to if the limit of is a proper constant, or From the packing perspective, we are able to state the convergence in a uniform manner with standardizing constants that are adaptive in and Since in real data, the limit of is usually not known, this uniform convergence with adaptive standardizing constants makes the result easy to apply in practice.

-

•

During the review process of this paper, we noticed the results in [43] which focus on the coupling and bootstrap approximations of the maximal spurious correlation when . Again our different focus is on explicit limiting distributions with adaptive standardizing constants from the packing perspective.

We are not able to find existing literature on the rank-extreme association. To evaluate the performance of our low-rank detection method, we compare our method with the algorithm in [14] which studies a similar problem. During the review process of the paper, we also noticed recent work by [21]. The most important difference from these papers is that they focus on the case when and are comparable and both large, while we consider the case when is small and is large.

I-B Outline of the Paper

In Section II, we derive the asymptotic bound on the spherical packing problem, as well as that of the maximal spurious correlation and the related extreme value distributions. In Section III, we describe the rank-extreme association of elliptically distributed vectors. In Section IV we develop a fast detection method of a low-rank by using the rank-extreme association reversely. In Section V, we study the performance of the detection method through simulations. We conclude and discuss future work in Section VI.

II Asymptotic Theory of the Spherical Cap Packing Problem

II-A The Sharp Asymptotic Bound for independent inner products (SABER) and Spurious Correlations (SABRE)

We first observe that as described in [44], when is uniformly distributed over . By borrowing strength from the packing literature [22, 26] on the total area of non-overlap spherical caps on , we develop the following theorem on a sharp asymptotic bound for independent inner products.

Theorem II.1.

Sharp Asymptotic Bound for Independent Inner Products (SABER).

For arbitrary deterministic unit vectors and a uniformly distributed unit vector over , the random variable satisfies that ,

| (II.1) |

Therefore, , as

| (II.2) |

In particular, if then we have the double limit

| (II.3) |

Theorem II.1 provides an explicit answer to the question at the beginning of Section I with a probabilistic statement: No matter how ’s are located on the unit sphere, the magnitude of the inner products (or cosines of the angle) between these points and a uniformly random point cannot exceed with high probability for large This upper bound on the inner products is equivalent to a lower bound on the minimal angle between the new random point to the existing points.

The SABER possesses the following important properties:

-

1.

This bound is universal in the sense that it holds for any configuration of ’s.

-

2.

This bound is uniform in the sense that it holds uniformity for .

-

3.

This bound is sharp in the sense that it can be attained for some configuration of ’s, especially when ’s are i.i.d. uniformly distributed, as will be discussed in Section II-B.

Thus, in an analogy, the SABER is to the distributions of the independent inner products as the fundamental bound is to the -dimensional Gaussian distribution.

A technical note here is that when is finite, the fraction in the exponent of can be replaced by with any fixed integer This change would not alter the asymptotic result in due to a uniform convergence in the proof. The number only has an effect when the dimension is finite. For example, see [39] for a similar but different bound when is fixed. We focus on the bound due to its connection to the distribution. When all these bounds are equivalent.

Another technical note is that although Theorem II.1 is for a deterministic set of ’s, we note here that this set of unit vectors can be random as well. As long as ’s are stochastically independent of Theorem II.1 can be applied to random ’s by a conditioning argument on any realization of ’s.

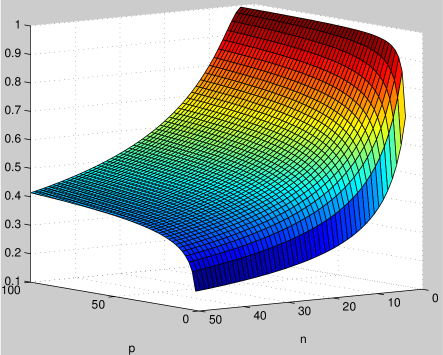

Figure 1 illustrates the SABER in Theorem II.1 as a function of and . It can be seen that the SABER has a range of as an increasing function in and a decreasing function in

Due to the connection between sample correlations and the inner products (I.2), this bound is immediately applicable to spurious correlations. Suppose records i.i.d. samples of a Gaussian variable then it is well-known (see [44]) that is a uniformly distributed unit vector over . Thus, we have the following bound on the maximal spurious correlation.

Corollary II.2.

Sharp Asymptotic Bound for Spurious Correlations (SABRE).

Suppose we observe i.i.d. samples of arbitrary random variables and a Gaussian variable that is independent of ’s. The maximal absolute sample correlation

satisfies that , as

| (II.4) |

In particular, if then we have the double limit

| (II.5) |

Similarly as the interpretation for the SABER, the implication of the SABRE is as follows: Uniformly for no matter how the variables are distributed, the magnitude of the sample correlations between ’s and a Gaussian cannot exceed the SABRE with high probability for large Note here that in practice, the requirement of Gaussianity of can be easily relaxed through a transformation of distributions. Since the SABRE is universal, uniform, and sharp as the SABER, this bound provides a way to distinguish true signals from spurious correlations. We shall investigate this application in future work.

II-B Limiting Distributions in the i.i.d. Case

In this section, we describe the asymptotics of the maximal inner product when ’s are i.i.d. uniformly distributed and the asymptotics of spurious correlations when ’s are independently Gaussian distributed. We first observe that when ’s are i.i.d. uniformly unit vectors over then for any random unit vector that is independent of ’s, we have the following two properties about the inner products :

-

1.

Conditioning on the variables ’s are independent since ’s are independent;

-

2.

For each the variable is distributed as . Since this conditional distribution does not depend on , it implies that unconditionally is stochastically independent of

From these two properties, we conclude that unconditionally, ’s are i.i.d. distributed. We thus show the sharpness of the SABER and SABRE by studying the maximum of i.i.d. variables.

Theorem II.3.

-

1.

(Sharpness of SABER)

Suppose ’s are i.i.d. uniformly distributed over the -sphere then for arbitrary random unit vector that is independent of ’s, uniformly for all , as the random variable has the following convergence:(II.6) i.e., as

(II.7) -

2.

(Sharpness of SABRE)

Similarly, suppose we observe i.i.d. samples of independent Gaussian variables and an arbitrarily distributed random variable that is independent of ’s. Consider the maximal absolute sample correlation Uniformly for all , as we have(II.8)

Theorem II.3 shows the sharpness of the SABER and the SABRE. It further describes a smooth phase transition of (also ) depending on the limit of

-

(i)

If , then and

-

(ii)

If for fixed , then

-

(iii)

If , then and

Note in particular that when , the SABRE satisfies

| (II.9) |

The rate has appeared in hundreds of books and papers and is very-well known in high-dimensional statistics literature [35]. However, it is just a special case of the general rate , which is obtained through the packing perspective. This fact demonstrates the power of this packing approach. In Figure 1, the smooth phase transition curves are represented as regions of the same color.

Below are some geometric intuitions on why the phase transition depends on the limit of : Note that the number of orthants in is and is growing exponentially in Therefore, if the growth of is faster than the exponential rate in then the unit vectors on would be so “dense” that they would cover the sphere, making the magnitude of the maximal inner product converging to 1; if the growth of is exponential in then there would be a constant number (depending on the limit of ) of points in each orthant, so that the new random point would stay around some proper angle to the existing points; if the growth of is slower than the exponential rate, then many orthants would be empty of points asymptotically, thus the new random point can be almost orthogonal to the existing points.

When ’s are i.i.d. uniformly distributed or when ’s are independently Gaussian, by combining the results in packing literature [22, 26] and classical extreme value theory [36, 37], we further develop the following uniform convergence in distribution of the corresponding maxima.

Theorem II.4.

-

1.

(Limiting Distribution of the Maximal Independent Inner Product)

Suppose ’s are i.i.d. uniformly unit vectors over For arbitrary random unit vector that is independent of ’s, consider . Letwhere is a correction factor with being the Beta function. Then for any fixed , as

(II.10) In particular, if and then for any fixed , we have the double limit

(II.11) -

2.

(Limiting Distribution of the Maximal Spurious Correlation)

Similarly, suppose we observe i.i.d. samples of independent Gaussian variables and an arbitrarily distributed random variable that is independent of ’s. Consider the maximal absolute sample correlation Then for any fixed , as(II.12) In particular, if and then for any fixed , we have the double limit

(II.13)

Theorem II.4 characterizes the uncertainty of the maximal independent inner product and the maximal spurious correlation from the SABER and SABRE respectively. This result possesses the following desirable properties for practice: (1) The convergence of () is uniform for () and is applicable provided the dataset contains two (three) observations. This uniformity over is due to the packing perspective. (2) The convergence is arbitrary for any distribution of . This arbitrariness results from the invariance property of the uniform distribution over the sphere. (3) The convergence is adaptive to the number of variables : Despite the phase transition phenomenon, the normalizing constants and adaptively adjust themselves for different and to guarantee a good approximation to a proper limiting distribution. (4) Instead of the “curse of dimensionality,” the convergence is a “blessing of dimensionality”: The larger is, the better the approximation is. These properties make the result widely applicable in the high-dimension-and-low-sample size situations.

We also remark here that for statistical applications, although in principle the empirical distribution of can be simulated based on the Gaussian assumptions, in a large- situation, for example , such simulation can incur extremely high time and computation cost. On the other hand, these quantiles can be easily obtained through the formulas of and for an arbitrary large . Indeed, in modern data analysis, it is more and more often to encounter datasets with a number of variables in millions, billions, or even larger scales [45]. The uniform--large- type asymptotics presented in this paper can be especially useful in these situations.

III Rank-Extreme Association of Degenerate Elliptical Vectors

III-A Rank-Extreme Bound of Degenerate Elliptical Vectors

In this section we consider the maximal magnitude of an elliptically distributed vector. A -dimensional random vector is said to be elliptically distributed and is denoted as if its density satisfies that

| (III.1) |

for some continuous integrable function so that its isodensity contours are ellipses. The family of elliptical distributions is a generalization of multivariate Gaussian distributions and is an important and general class of distributions in practice [46].

In this paper, we focus on an elliptical distributed vector with a covariance matrix that has unit diagonals. Through a packing argument, we find a functional link between the distribution of and the rank of we thus refer this link as the rank-extreme (ReX) association.

Below are the observations that connect these results to the packing problem: Consider any covariance matrix that is positive semi-definite, has ones on the diagonal, and has rank . Through its eigen-decomposition, we can write , where is a matrix with columns ’s such that . Thus, we can write where Moreover, for any , if we consider the spherical coordinates, then we have where . Note that is a random variable which depends only on We thus assume is a random variable such that and where and are sequences of constants that depends only on and is a proper random variable. Note also that and are independent. Based on the above consideration, we obtain the following decomposition

| (III.2) |

Since the distribution of the maximal absolute inner products is studied in Section II, we can apply these asymptotic results to study the distribution of In particular, we develop the following universal bound on a degenerate elliptically distributed vector with a particular case of a degenerate Gaussian vector, where with .

Theorem III.1.

-

1.

(ReX Bound for Degenerate Elliptical Vectors)

For any vector of standard elliptical variables with , the random variable satisfies that for any fixed(III.3) -

2.

(ReX Bound for Degenerate Gaussian Vectors)

In particular, for any vector of standard Gaussian variables with , the random variable satisfies that for any fixed(III.4) If further with then

(III.5)

Similar to the SABER , this bound is universal over any correlation structures of rank We also show that this bound is sharp, as described in Section III-B.

III-B Attainment of the ReX Bound and Related Limiting Distributions

The sharpness of the bound in Theorem III.1 was shown by considering the case when ’s in the decomposition (III.2) are i.i.d. uniformly distributed over .

Theorem III.2.

(Sharpness of ReX Bounds) If ’s are i.i.d. uniformly distributed over the -sphere and are independent of then as and ,

| (III.6) |

i.e.,

| (III.7) |

In particular, if then as and ,

| (III.8) |

One remark here is that though each realization of ’s results in a degenerate elliptically distributed , unconditionally the joint distribution of is not elliptically distributed. Nevertheless, Theorem III.2 shows the existence of configurations of that attains the bound in Theorem III.1.

The limit in Theorem III.2 indicates the following phase transition for the extreme value in degenerate Gaussian vectors, again depending on the limit of :

-

(i)

If and , then

-

(ii)

If for fixed , then

-

(iii)

If , then

Note that the function is a smooth function for and its range is Thus, as the phase transition in Section II-B, the above phase transition is smooth. Moreover, the regime (iii) in the phase transition implies that when the rank is high compared to , the maximum magnitude of a degenerate Gaussian vector can behave as that of i.i.d. Gaussian vectors.

Note that by (III.2), we have the decomposition of the squared maximum norm

| (III.9) |

Thus, by the results in Section II-B, we also develop the following result on the limiting distribution of a degenerate elliptical vector when ’s are i.i.d. uniform.

Theorem III.3.

-

1.

(Limiting Distribution of the Maximum of Degenerate Elliptical Vectors)

Suppose and with for some sequences , and a proper random variable . Then with the constants and as in Theorem II.4, the random variable has the following limiting distribution:-

(a)

If is fixed and then

-

(b)

Suppose and

-

i.

If and then

-

ii.

If and with then where and and are independent.

-

iii.

If and then where .

-

i.

-

(a)

-

2.

(Limiting Distribution of the Maximum of Degenerate Gaussian Vectors)

In particular, if then the random variable has the following limiting distribution:-

(a)

If is fixed and then

-

(b)

Suppose and

-

i.

If and then where

-

ii.

If and with then where and and are independent.

-

iii.

If and then where .

-

i.

-

(a)

Theorem III.3 characterizes the limiting distribution of the squared maximum norm of degenerate elliptical vectors for the entire scope of the rank. The limiting distribution takes on a phase transition phenomenon according to the cross ratio between standardizing constants in the convergence of the norm and the convergence of the maximal squared inner product. This phenomenon is similar as the phase transitions in the classical extreme value theory for correlated random variables [36, 38, 37]. When is standard Gaussian distributed, the limiting distribution can be either , standard Gaussian, a mixture of the standard Gaussian and Gumbel, or Gumbel depending on the relationship between and .

IV ReX Detection of Low-Dimensional Linear Dependency

In this section we consider the problem of detection of low-rank dependency in high-dimensional Gaussian data. Suppose we have observations of a Gaussian vector whose covariance matrix has rank is One common technique in estimating is eigenvalue thresholding based on the principal component analysis (PCA). However, such methods become inaccurate when is small. Moreover, statistical inference, such as tests and confidence intervals, about as a parameter is not completely clear.

We propose to apply the rank-extreme association to obtain the information about . We consider the following generating process of the data matrix from a factor model:

| (IV.1) |

where is a fixed -dimensional vector, has i.i.d. entries, has columns of unit vectors, is a diagonal matrix with positive diagonal elements has i.i.d. entries as the observation noises, and is the standard deviation of the noise. and are mutually independent so that each entry is marginally distributed as All of the above variables are not observed except for the data matrix and our goal is to estimate the rank with these observations.

Conventional estimate of is through a proper threshold over the eigenvalues of the sample covariance matrix of . Such an approach requires the eigenvalues to be at least for possible detection, as shown in equation (7) and Theorem 1 in [14]. In [14], the authors consider the case when so that this required magnitude is In general, to set this required magnitude to be is equivalent to set

In what follows, we introduce our ReX method for the inference of based on the observed extreme values. We consider both the case when the columns are i.i.d. uniform unit vectors and the general case.

IV-A The Case When the Columns of are i.i.d. Uniform Unit Vectors

We first consider the case when the columns of are realizations of i.i.d. uniform unit vectors over . To explain our ReX method, we start with the elementary noiseless case when it is known that , , and . In this case, we propose to approximate the asymptotic distribution of the maximal squared entry in each row of by that of . This approximation is particularly useful when where obtaining the spectrum information is difficult from PCA based methods. The accuracy of the approximation is due to the following two reasons: (1) the theorems in Section III are for each row of and have no requirement on ; (2) for each row, the condition in turn shows that the largest magnitude of noise in each row of is in the order of Thus, when , this magnitude is and will not affect the limiting distributions.

Note that for a large Theorem II.4, the distribution, and the generalized extreme value distribution [37] imply that

| (IV.2) |

where and are as in Theorem II.4. Thus, through (III.9) and Theorem III.2:

| (IV.3) |

Suppose we observe i.i.d. samples of which are denoted as By the central limit theorem we have

| (IV.4) |

where and An easy estimate of is thus the solution of the equation

| (IV.5) |

The estimators from this approach usually have a right-skewed distribution, as the distribution of and are both right-skewed. To reduce the right-skewness in the distribution of we take the square-root transformation and use the delta method as in [47] to obtain the following approximate probabilistic statement

| (IV.6) |

where and is the -quantile of the standard Gaussian distribution. One then solves the inequality

| (IV.7) |

in to obtain the -left-sided confidence interval from to this solution. Thus, probability statements about an unknown can be made. Note that needs not to be larger than throughout this approach.

Another advantage of the proposed inference method is the speed. Note that through the rank-extreme approach, there is no need of matrix multiplications. By quickly checking the maximal entry in each row, we may get a good sense of the rank as a parameter. Thus, much computation cost can be saved from the rank-extreme approach, and the proposed inference method for can be used for a fast detection of a low-rank.

When the parameters , , and ’s are unknown, we would need to estimate them. Since we are considering the case when is small while is large, the estimation of each component variance is difficult. However, when it is known that ’s are equal to some unknown we can estimate the variance by borrowing strength from all variables. Specifically, we propose the following procedure for the inference of :

-

1.

Center each column of by subtracting the column averages. Denote the resulting data matrix by

-

2.

Stack the columns of into an vector and estimate the component standard deviation with this the sample standard deviation of this vector. Denote the estimate by

-

3.

Standardize by dividing Denote the resulting data matrix by

-

4.

Apply the approach in the noiseless case above to for inference about

The above consideration is also applicable to the situation when the variables can be grouped into several blocks and the component variances within each block are close. Tests of equality variances such as [48] are widely available. We will study the case with unequal variances in future work.

IV-B General Case

In this section we discuss the much more challenging situation when the columns of are general unit vectors. For simplicity we restrict ourselves in the case when it is known that , , and . We observe that by the decomposition (III.2), we have the following proposition:

Proposition IV.1.

Suppose where has unit diagonals and If there exists a collection of deterministic unit vectors ’s in such that where and that for an independent uniformly distributed unit vector , as , then as

| (IV.8) |

With this proposition, we convert the inference about as a parameter to a simple inference problem on the degrees of freedom of a distribution. The condition is a condition on as It requires that the vectors ’s be “densely” distributed over the unit sphere in as increases, so that the minimal angle between the collection of ’s and the vector converges to 0 as the number of points on the unit sphere increases. The existence of such a is shown by the sharpness of the SABER. We aren’t able to find a more precise condition on to guarantee the convergence as it relates to the challenging question of the optimal configuration of spherical cap packing and spherical code, on which some recent development includes [49]. However, as long as for some and , by conditioning on this event, inference such as confidence intervals can be made about as a parameter. Unfortunately, as many conditions in statistical literature, neither of these above conditions can be checked in practice. We will consider further analysis on this approach in future work.

V Simulation Studies

In this section we study the performance of the ReX detection of a low-rank from the model in Section IV-A. We consider two cases: (1) the case when it is known that , , and and (2) the case when the unknown component variances for some unknown .

V-A Noiseless Case

In this subsection, we study the performance of the ReX detection when it is known that , , and . We set , to be from {10,20,30}, and to be from . In this case, the estimation of can be obtained by solving (IV.5), and the confidence interval can be obtained by solving (IV.7). We evaluate the performance of the ReX inference for with two criteria: (1) the sample mean squared error (MSE) of the point estimate of which is defined by

| (V.1) |

where is the number of simulations, and is the estimate of from the -th simulated data, ; and (2) the coverage and upper bounds for . As a comparison, we also study the MSE of an important PCA-based method, the KN method, proposed in [14] by applying to the algorithm posted on the authors’ website.

Table I represents simulation results on the performance of the ReX inference for different ’s and ’s. The results are based on 1000 simulated datasets. The first block in the table summarizes the MSE of the ReX estimation and the KN estimation. The second block shows the average coverage probability and the mean and median length of 95% left-sided confidence intervals for . When (IV.7) does not have a solution, we record the confidence interval as not covering .

In terms of estimation, although the MSE of the ReX estimation seems larger than that of the KN method in some cases, we noticed that in seven out of nine scenarios the KN method actually returns as an estimate of . Indeed, the consistency of the KN method is shown when and are large and comparable, whereas its consistency is not guaranteed in these difficult situations when is much larger than . In the scenarios in our simulations, the estimations of the KN method are not consistent and can lead to serious problems in practice, particularly when . On the other hand, we see from Table I that the MSE of the ReX estimation of gets better as grows. When the KN method returns better estimates, such as the cases when and or , the ReX method has a much smaller MSE.

On the performance of ReX confidence intervals, note that the standard deviation of sample proportion of 1000 Bernoulli trials with success probability is about Thus, a scenario with an average coverage between and shows a satisfactory confidence interval without being too liberal or too conservative. With this criterion, all ReX confidence intervals are satisfactory except when and . In this case, not being able to solve (IV.7) is the main reason of not covering in this difficult situation, see discussions at the end of this section. The length of the ReX confidence intervals is decreasing as increases. The median lengths are less than the mean lengths, showing the distribution of the upper bound of confidence intervals is indeed right-skewed, as expected in Section IV-A.

| MSE of Estimation | |||||||||||

| ReX | 12.40 | 3.97 | 2.91 | 38.07 | 12.69 | 8.73 | 73.52 | 47.21 | 22.03 | ||

| KN | 9.00 | 49.00 | 148.16 | 64.00 | 4.00 | 143.98 | 169.00 | 9.00 | 49.00 | ||

| 95% left-sided ReX Confidence Interval | |||||||||||

| Coverage | 0.958 | 0.946 | 0.944 | 0.951 | 0.949 | 0.950 | 0.926 | 0.937 | 0.952 | ||

| Mean Upper Bound | 18.21 | 15.15 | 14.20 | 31.41 | 23.66 | 22.13 | 49.32 | 35.74 | 31.01 | ||

| Median Upper Bound | 16.55 | 14.65 | 13.87 | 26.27 | 22.34 | 21.48 | 38.11 | 31.38 | 29.30 | ||

V-B Equal Variance Case

In this case, we set , to be from {10,20,30}, and to be from as in Section V-A. We set to be as discussed in Section IV, set to be a regular sequence of length from to , and set to be Table II shows the results based on 1000 simulated datasets.

| MSE of Estimation | |||||||||||

| ReX | 0.49 | 0.65 | 0.82 | 1.93 | 1.52 | 1.51 | 6.89 | 4.24 | 3.42 | ||

| KN | 9 | 49 | 3.66 | 64 | 4 | 124.02 | 169 | 9 | 49.00 | ||

| 95% left-sided ReX Confidence Interval | |||||||||||

| Coverage | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | ||

| Mean Upper Bound | 17.74 | 15.87 | 15.18 | 28.10 | 24.27 | 22.84 | 41.43 | 34.03 | 31.44 | ||

| Median Upper Bound | 17.70 | 15.83 | 15.18 | 27.77 | 24.21 | 22.76 | 40.35 | 33.56 | 31.32 | ||

On the estimation, Table II shows again the problem of PCA based methods when is much larger than : the KN method returns for seven out of nine scenarios. When and or , the KN method returns better estimates, but its MSE is larger than that of the ReX estimation. Note that in these two scenarios for the KN method as well as in all nine scenarios for the ReX method, the MSEs are much smaller than those in Table I. One possible reason here is the standardization process. For the ReX method, recall from Section IV-A that the distribution of the estimators can be right-skewed. Since the variance estimation from the sample usually underestimates , the row maximum from standardized data can often be larger than that in the noiseless case, leading to a larger estimate of which offsets the right-skewness in the distribution.

On the ReX confidence intervals, Table II shows that the coverage probability of them is 1 for all nine scenarios. Although the coverage probability is conservative, the lengths of intervals are reasonably tight. Also, the median upper bounds are usually less than the mean ones, showing again the right-skewness. The problem of right-skewness is much more benign though. In summary, in our simulation studies when is much larger than , the traditional PCA based methods such as the KN method (1) may have a large MSE in estimating , (2) may not be able to provide confidence intervals for , and (3) requires matrix-wise calculation. On the other hand, the ReX inference (1) has a small MSE in estimation, (2) provides confidence interval statements for , and (3) only needs to scan through the row maxima in the matrix and is thus fast. These results demonstrate the advantages of using the ReX method for the detection of a low-rank structure in high dimensions with a small sample size.

The simulation results also reflect some issues of the ReX method that need further improvements. For example, for some cases in Table II, the MSE of the ReX method increases as increases. This problem could be related to the approximation error in (IV.3). Also, the ReX inference are based on solutions of (IV.5) and (IV.7). Such equations may not have a solution in difficult practical situations (This happens about 1% of the time when and ). Although this problem seems to disappear when is above 10, a more stable algorithm is needed. We shall improve our method in these directions in future work.

VI Discussions

We develop a probabilistic upper bound for the maximal inner product between any set of unit vectors and a stochastically independent uniformly distributed unit vector, as well as the limiting distributions of the maximal inner product when the set of unit vectors are i.i.d. uniformly distributed. We demonstrate the applications of these results the problems of spurious correlations and low-rank detections.

We emphasize that we focus our asymptotic theory in the uniform--large- paradigm. This type of asymptotics is motivated by the high-dimensional-low-sample-size framework [45] which is emerging in many areas of science. The proposed packing approach can be especially useful in this framework because (1) finite-sample properties can be studied, and (2) existing packing literature can be applied. In the future, we will continue to explore this type of asymptotics in more general situations. For the theory, we plan to investigate the distribution of the maximal inner products with more generally correlated ’s. One of the applications of the new theory could be a more accurate detection method of a low rank. We also plan to improve and generalize the ReX detection method in the case when ’s are different, as well as in the case when the data are not Gaussian distributed.

Appendix A Technical Lemmas

We provide some key proofs in the appendix. Proofs of other results are immediate corollaries of these results. We start with the key observation that the distribution of each is as discussed at the beginning in Section II-A and also in [44]. Based on this fact, we first derive a lemma on the tail bounds of the distribution. This lemma is proved by integration by parts, and the details are omitted.

Lemma A.1.

For we have the following bounds for an incomplete beta integral:

| (A.1) |

We also find a lemma on the uniform convergence of the function This lemma is important for the uniform convergence in the paper. The proof is easy and is omitted.

Lemma A.2.

Uniformly for any as

We derive below a lemma summarizing the uniform convergence of standardizing constants in the theorems. Their proofs are routine analysis and are omitted.

Lemma A.3.

Consider the sequences , in Theorem II.4 where is a correction factor. For any fixed let We have the following asymptotic results:

-

1.

Uniformly for any , as , and .

-

2.

Uniformly for any , as .

Appendix B Proofs in Section II

Proof of Theorem II.1.

Proof of Theorem II.3.

Since we already have the upper bound, it is enough to show that for any fixed such that ,

| (B.3) |

By the independence discussed at the beginning of Section II-B, we have that for

| (B.4) |

We will lower-bound the absolute value of the exponent in (B.4). By the lower bound in Lemma A.1 and the inequality that as in [51], we have

| (B.5) |

In the last step of (B.5), we use Lemma A.2 again. It is now easy to see that

| (B.6) |

as regardless of the rate of , which completes the proof of Theorem II.3. ∎

Appendix C Proofs in Section III

Proof of Theorem III.1.

It is easy to show (III.3) and (III.4). To show (III.5), note that for any ,

| (C.1) |

We will show each of the two summands in the last line can be made small with a proper choice of

By the proof of Theorem II.1, we see that

| (C.2) |

Note also that . Thus by the Chernoff bound for distribution,

| (C.3) |

Due to (C.2) and (C.3), we let In the case when both (C.2) and (C.3) converge to .

∎

Proof of Theorem III.3.

Note that,

| (C.4) |

Now note also that is bounded and that Therefore, the theorem follows from Slutsky’s theorem by checking the limit of the ratio and and picking the one with a larger magnitude as the scaling factor. ∎

Acknowledgment

The author appreciates the insightful suggestions from L. D. Brown, A. Buja, T. Cai, J. Fan, J. S. Marron, and H. Shen. The author thanks R. Adler, J. Berger, R. Berk, A. Budhiraja, E. Candes, L. de Haan, J. Galambos, E. George, S. Gong, J. Hannig, T. Jiang, I. Johnstone, A. Krieger, R. Leadbetter, R. Li, D. Lin, H. Liu, J. Liu, W. Liu, Y. Liu, Z. Ma, X. Meng, A. Munk, A. Nobel, E. Pitkin, S. Provan, A. Rakhlin, D. Small, R. Song, J. Xie, M. Yuan, D. Zeng, C.-H. Zhang, N. Zhang, L. Zhao, Y. Zhao, and Z. Zhao for helpful discussions. The author also thanks the editors and reviewers for important comments that substantially improve the manuscript. The author is particularly grateful for L. A. Shepp for his inspiring introduction of the random packing literature.

This research is partially supported by NSF DMS-1309619, NSF DMS-1613112, NSF IIS-1633212, and the Junior Faculty Development Award at UNC Chapel Hill. This material was also partially based upon work supported by the NSF under Grant DMS-1127914 to the Statistical and Applied Mathematical Sciences Institute. Any opinions, findings, and conclusions or recommendations expressed in this material are those of the author(s) and do not necessarily reflect the views of the National Science Foundation.

References

- [1] J. Fan, F. Han, and H. Liu, “Challenges of big data analysis,” National Science Review, vol. 1, pp. 293–314, 2014.

- [2] I. M. Johnstone and D. M. Titterington, “Statistical challenges of high-dimensional data,” Philosophical Transactions of the Royal Society A: Mathematical, Physical and Engineering Sciences, vol. 367, no. 1906, pp. 4237–4253, 2009. [Online]. Available: http://rsta.royalsocietypublishing.org/content/367/1906/4237.abstract

- [3] J. Fan, J. Lv, and L. Qi, “Sparse high dimensional models in economics,” Annual review of economics, vol. 3, p. 291, 2011.

- [4] J. Fan, S. Guo, and N. Hao, “Variance estimation using refitted cross-validation in ultrahigh dimensional regression,” J. R. Statist. Soc. B, vol. 74, pp. 37–65, 2012.

- [5] I. Markovsky, Low-Rank Approximation: Algorithms, Implementation, Applications. New York: Springer, 2012.

- [6] B. Yang, “Projection approximation subspace tracking,” Signal Processing, IEEE Transactions on, vol. 43, no. 1, pp. 95–107, Jan 1995.

- [7] D. J. Rabideau, “Fast, rank adaptive subspace tracking and applications,” Signal Processing, IEEE Transactions on, vol. 44, no. 9, pp. 2229–2244, 1996.

- [8] A. Kavc̆ić and B. Yang, “Adaptive rank estimation for spherical subspace trackers,” Signal Processing, IEEE Transactions on, vol. 44, no. 6, pp. 1573–1579, Jun 1996.

- [9] E. C. Real, D. W. Tufts, and J. W. Cooley, “Two algorithms for fast approximate subspace tracking,” Signal Processing, IEEE Transactions on, vol. 47, no. 7, pp. 1936–1945, 1999.

- [10] M. Shi, Y. Bar-Ness, and W. Su, “Adaptive estimation of the number of transmit antennas,” in Military Communications Conference, 2007. MILCOM 2007. IEEE. IEEE, 2007, pp. 1–5.

- [11] R. Badeau, G. Richard, and B. David, “Fast and stable yast algorithm for principal and minor subspace tracking,” Signal Processing, IEEE Transactions on, vol. 56, no. 8, pp. 3437–3446, 2008.

- [12] S. Bartelmaos and K. Abed-Meraim, “Fast principal component extraction using givens rotations,” Signal Processing Letters, IEEE, vol. 15, pp. 369–372, 2008.

- [13] X. G. Doukopoulos and G. V. Moustakides, “Fast and stable subspace tracking,” Signal Processing, IEEE Transactions on, vol. 56, no. 4, pp. 1452–1465, 2008.

- [14] S. Kritchman and B. Nadler, “Determining the number of components in a factor model from limited noisy data,” Chemometrics and Intelligent Laboratory Systems, vol. 94, no. 1, pp. 19 – 32, 2008. [Online]. Available: http://www.sciencedirect.com/science/article/pii/S0169743908001111

- [15] ——, “Non-parametric detection of the number of signals: Hypothesis testing and random matrix theory,” Signal Processing, IEEE Transactions on, vol. 57, no. 10, pp. 3930–3941, Oct 2009.

- [16] I. M. Johnstone and A. Y. Lu, “On consistency and sparsity for principal components analysis in high dimensions,” Journal of the American Statistical Association, vol. 104, no. 486, 2009.

- [17] P. Perry and P. Wolfe, “Minimax rank estimation for subspace tracking,” Selected Topics in Signal Processing, IEEE Journal of, vol. 4, no. 3, pp. 504–513, June 2010.

- [18] Q. Berthet and P. Rigollet, “Optimal detection of sparse principal components in high dimension,” The Annals of Statistics, vol. 41, no. 4, pp. 1780–1815, 08 2013. [Online]. Available: http://dx.doi.org/10.1214/13-AOS1127

- [19] D. L. Donoho and M. Gavish, “The optimal hard threshold for singular values is 4/sqrt (3),” arXiv preprint arXiv:1305.5870, 2013.

- [20] T. Cai, Z. Ma, and Y. Wu, “Optimal estimation and rank detection for sparse spiked covariance matrices,” Probability Theory and Related Fields, pp. 1–35, 2014. [Online]. Available: http://dx.doi.org/10.1007/s00440-014-0562-z

- [21] Y. Choi, J. Taylor, and R. Tibshirani, “Selecting the number of principal components: estimation of the true rank of a noisy matrix,” arXiv preprint arXiv:1410.8260, 2014.

- [22] R. A. Rankin, “The closest packing of spherical caps in n dimensions,” Proceedings of the Glasgow Mathematical Association, vol. 2, pp. 139–144, 7 1955. [Online]. Available: http://journals.cambridge.org/article_S2040618500033219

- [23] T. M. Thompson, From Error-correcting Codes through Sphere Packings to Simple Groups. Mathematical Association of America, 1983.

- [24] J. H. Conway, N. J. A. Sloane, and E. Bannai, Sphere-packings, Lattices, and Groups. New York, NY, USA: Springer-Verlag New York, Inc., 1987.

- [25] D. Hilbert, “Mathematical problems,” Bulletin of the American Mathematical Society, vol. 8, no. 10, pp. 437–479, 1902.

- [26] A. D. Wyner, “Random packings and coverings of the unit -sphere,” Bell System Technical Journal, vol. 46, pp. 2111–2118, 1967.

- [27] A. Barg and D. Nogin, “Bounds on packings of spheres in the grassmann manifold,” Information Theory, IEEE Transactions on, vol. 48, no. 9, pp. 2450–2454, Sep 2002.

- [28] K. K. Mukkavilli, A. Sabharwal, E. Erkip, and B. Aazhang, “On beamforming with finite rate feedback in multiple-antenna systems,” Information Theory, IEEE Transactions on, vol. 49, no. 10, pp. 2562–2579, 2003.

- [29] O. Henkel, “Sphere-packing bounds in the grassmann and stiefel manifolds,” IEEE Transactions on Information Theory, vol. 51, no. 10, pp. 3445–3456, 2005.

- [30] R. Koetter and F. R. Kschischang, “Coding for errors and erasures in random network coding,” Information Theory, IEEE Transactions on, vol. 54, no. 8, pp. 3579–3591, 2008.

- [31] W. Dai, Y. Liu, and B. Rider, “Quantization bounds on grassmann manifolds and applications to mimo communications,” Information Theory, IEEE Transactions on, vol. 54, no. 3, pp. 1108–1123, 2008.

- [32] R.-A. Pitaval, H.-L. Maattanen, K. Schober, O. Tirkkonen, and R. Wichman, “Beamforming codebooks for two transmit antenna systems based on optimum grassmannian packings,” Information Theory, IEEE Transactions on, vol. 57, no. 10, pp. 6591–6602, 2011.

- [33] M. Dalai, “Lower bounds on the probability of error for classical and classical-quantum channels,” Information Theory, IEEE Transactions on, vol. 59, no. 12, pp. 8027–8056, Dec 2013.

- [34] T. Hastie, R. Tibshirani, and J. Friedman, The Elements of Statistical Learning: Prediction, Inference and Data Mining, 2nd ed. Springer Verlag., 2009.

- [35] P. Bühlmann and S. van de Geer, Statistics for High-Dimensional Data. Springer, 2011.

- [36] M. R. Leadbetter, Extremes and Related Properties of Random Sequences and Processes. Springer-Verlag, 1983.

- [37] L. de Haan and A. Ferreira, Extreme Value Theory: An Introduction. Springer, 2006.

- [38] R. J. Adler, “An introduction to continuity, extrema, and related topics for general gaussian processes,” Lecture Notes-Monograph Series, pp. i–155, 1990.

- [39] A. Hero and B. Rajaratnam, “Large-scale correlation screening,” Journal of the American Statistical Association, vol. 106, pp. 1540–1552, 2012.

- [40] T. T. Cai and T. Jiang, “Limiting laws of coherence of random matrices with applications to testing covariance structure and construction of compressed sensing matrices,” Ann. Statist, vol. 39, pp. 1496–1525, 2011.

- [41] ——, “Phase transition in limiting distributions of coherence of high-dimensional random matrices,” J. Multivariate Analysis, vol. 107, pp. 24–39, 2012.

- [42] T. T. Cai, J. Fan, and T. Jiang, “Distribution of angles in random packing on spheres,” J. Machine Learning Research, vol. 14, pp. 1801–1828, 2013.

- [43] J. Fan, Q.-M. Shao, and W.-X. Zhou, “Are discoveries spurious? distributions of maximum spurious correlations and their applications,” arXiv preprint arXiv:1502.04237, 2015.

- [44] R. J. Muirhead, Aspects of Multivariate Statistical Theory. Wiley, 1982.

- [45] P. Hall, J. S. Marron, and A. Neeman, “Geometric representation of high dimension, low sample size data,” Journal of the Royal Statistical Society: Series B (Statistical Methodology), vol. 67, no. 3, pp. 427–444, 2005. [Online]. Available: http://dx.doi.org/10.1111/j.1467-9868.2005.00510.x

- [46] K.-T. Fang, S. Kotz, and K. W. Ng, Symmetric multivariate and related distributions. Chapman and Hall, 1990.

- [47] A. W. van der Vaart, Asymptotic Statistics. Cambridge University Press, Cambridge, 1998.

- [48] M. S. Bartlett, “Properties of sufficiency and statistical tests,” Proceedings of the Royal Society of London. Series A, vol. 160, no. 901, pp. 268–282, 1937.

- [49] H. Cohn and Y. Zhao, “Sphere packing bounds via spherical codes,” Duke Mathematical Journal, vol. 163, no. 10, pp. 1965–2002, 07 2014. [Online]. Available: http://dx.doi.org/10.1215/00127094-2738857

- [50] R. Berk, L. Brown, A. Buja, K. Zhang, and L. Zhao, “Valid post-selection inference,” The Annals of Statistics, vol. 41, no. 2, pp. 802–837, 04 2013. [Online]. Available: http://dx.doi.org/10.1214/12-AOS1077

- [51] G. J. O. Jameson, “Inequalities for gamma function ratios,” The American Mathematical Monthly, vol. 120, pp. 936–940, 2013.

| Kai Zhang received the Ph.D. degree in Mathematics from Temple University in 2007 and the Ph.D. degree in Statistics from the Wharton School, University of Pennsylvania, in 2012. He is now with the Department of Statistics and Operations Research at the University of North Carolina, Chapel Hill. His research interests include high-dimensional regression and inference, causal inference and observational studies, and quantum computing. |