Infomax strategies for an optimal balance between exploration and exploitation

Abstract

Proper balance between exploitation and exploration is what makes good decisions, which achieve high rewards like payoff or evolutionary fitness. The Infomax principle postulates that maximization of information directs the function of diverse systems, from living systems to artificial neural networks. While specific applications are successful, the validity of information as a proxy for reward remains unclear. Here, we consider the multi-armed bandit decision problem, which features arms (slot-machines) of unknown probabilities of success and a player trying to maximize cumulative payoff by choosing the sequence of arms to play. We show that an Infomax strategy (Info-p) which optimally gathers information on the highest mean reward among the arms, saturates known optimal bounds and compares favorably to existing policies. The highest mean reward considered by Info-p is not the quantity actually needed for the choice of the arm to play, yet it allows for optimal tradeoffs between exploration and exploitation.

pacs:

I Introduction

Shannon’s theory of information deliberately leaves aside the meaning of messages and focuses on their statistical properties [1]. This standpoint is crucial for the universality of the theory, as witnessed by its wide range of applications in communication, computation and learning [2, 3, 4].

Biological and economic sciences feature natural measures of “meaning”, i.e. evolutionary fitness and payoffs. The relation between payoffs and information was first addressed by Kelly for his model of horse race gambling [5], where information on the outcome of the race provides a bound on the increment in the doubling rate of returns. The question was further developed and applied to portfolio management in Refs. [6, 7, 8]. Kelly’s horse race appears in some aspects of evolutionary biology as well. There, the reward function is the population growth rate and information refers to the state of the environment [9, 11, 12, 13, 10].

Neurobiology is the field where information theory is arguably the most popular in biological sciences. Barlow’s efficient coding [14] postulated that early neural sensory layers efficiently represent environmental information, i.e. their evolutionary fitness is proportional to their efficiency in the transmission of information from the environment to higher parts of the brain. The hypothesis was spectacularly confirmed in the visual system [15, 16, 17], see also [10, 18]. Similar ideas were recently introduced in cellular biology, namely to transduction pathways [19], their computational inference [20] and evolution [21], adaptation [22, 23] and transcription regulation [24, 25].

The catchy name Infomax for the maximization of information was introduced in [26], where it was applied to the training of perceptual networks. Infomax was also later applied for blind separation and deconvolution [27]. Infotaxis [28] used information as an orientation cue for searches aimed at locating sources of chemicals transported in a turbulent environment. For a recent review of information theory for decisions and actions, see [29].

It is usually the case that the more information is available, the better decisions or performances are, e.g. for the evolutionary model discussed in [10] the fitness increases with available information on the state of the environment. However, acquiring information has costs so that maximizing information does not generally lead to the best decisions. A first reason is the direct cost of acquiring and processing information, e.g. energy consumption costs : random strategies can obviously be the most effective if those costs are too high. The second, more subtle cost is that the choice of an action entails the exclusion of other possibilities. That calls for a balance between exploration and exploitation [30], which is what we shall discuss in the sequel.

Decisions in fluctuating and unknown environments require a balance between two extremes : exhaustive exploration of all available options vs greedy exploitation of available information to maximize short-term return. While the first option seems wiser, it can still performs poorly as harvesting information does not coincide with maximizing reward. For instance, for the search problem of a source of chemicals discussed in [28], the actual quantity to be minimized is the time of completion of the search. The information on the location of the source was found to be an efficient proxy, which replaces the daunting estimation of completion times by a much simpler statistic. When is such a replacement possible? More generally, when is the Infomax principle applicable and what are the situations, if any, where it is optimal?

Here, we address the previous questions by considering a classical problem in statistical decision theory: the multi-armed bandits. The model is the prototype of a broad class of sequential allocation problems that aim at optimally dividing resources to projects which yield benefits at a rate that depends on their degree of development. Among its many applications, we mention clinical trials, adaptive routing, job-scheduling, portfolio design and military logistics (see [31, 32] and references therein). Beside practical applications, the multi-armed bandit problem embodies the dilemma between exploitation and exploration mentioned above [33]. The additional appeal of the model is that optimal strategies of decision are known, the so-called Gittins index [34], as well as asymptotic bounds on maximal gains [35]. That allows to gauge the performance of the Infomax strategies developed below, Info-p and Info-id, and to provide a systematic assessment of cost and value of information. Finally, optimal bounds for the multi-armed bandit can be generalized to the broader class of problems encompassing Markov Decision Processes [36], suggesting that methods developed for the multi-armed bandit problem can have general relevance. To facilitate reading, we shall first briefly review known relevant results and then present our own.

II The multi-armed bandit problem in a nutshell

At each discrete time, an agent chooses to pull one arm among available. The agent receives a reward for the chosen action, according either to some unknown distribution or to a known distribution with unknown parameters. We shall consider for concreteness the case of Bernoulli arms whose (unknown) probabilities of success are , which are ordered for future convenience as . After each play, a reward is paid, which is (rescaled to) unity upon winning and zero otherwise. The long-term goal is to find a strategy that maximizes the average cumulated reward or, equivalently, minimize the expected regret : , where is the expected number of plays of the th arm.

Gittins index policy [34] applies to discounted rewards, i.e. maximizes the expected value of the sum where is a discount factor between zero and one. Even though the total number of steps is infinite, the discount factor introduces an effective horizon . For this formulation, Gittins [34] showed that the optimal strategy is an index policy, i.e. for each arm , one computes an index independent of all other arms, and then plays the arm with the highest index. The expression of the Gittins index for the -th arm at time is

| (1) |

where are the future rewards that one would obtain by choosing to play uniquely the -th arm up to the stopping time . The brackets in (1) denote the expectations of future success based on the posterior distribution defined by the past outcomes and (see (3)). Finally, the sup in (1) is taken over future stopping times, i.e. decisions that interrupt the game based only on information obtained up to the stopping time. In other words, the Gittins index (1) yields the expected rate of future rewards for the -th arm, given its past number of plays and wins . While (1) is the only expression consistent with an index policy (see Chap. 2 in [32]), the existence of an index policy itself is remarkable, and it is specific to the discounted formulation. The calculation of the Gittins index is usually done via dynamic programming [32]. However, the exponentially growing number of possible paths makes the problem intractable as the discount factor approaches unity.

The Lai-Robbins [35] lower bound on the expected number of plays of suboptimal arms reads :

| (2) |

The bound is generally valid when the number of plays is large and it does not involve any discount. In (2), and is the Kullback-Leibler relative entropy, that is the standard measure of divergence between two probability distributions [8]. Specifically, for two Bernoulli distributions parameterized by and . The closer the two probabilities and are, the larger is the constant in (2) and as . Strategies that attain the bound (2) are called asymptotically optimal.

III Results

Hereafter, we introduce two Infomax strategies, Info-p and Info-id. Info-p greedily acquires information on the estimated highest success probability among the arms of the bandit. We show below that Info-p saturates the bound (2), i.e. it is asymptotically optimal. Conversely, Info-id gathers information about the identity of the best arm. While Info-p leads to optimal payoffs, Info-id is shown below to yield an optimal rate of acquisition of information on the identity of the best arm but suboptimal payoffs.

III.1 Info-p

Unless specified otherwise, we discuss for simplicity a two-armed bandit with success probabilities . Results are easily generalized to arms. The probability of success for the th arm, as estimated from a sample of plays, is denoted by . Its posterior distribution after plays and wins reads (see, e.g., [4]) :

| (3) |

where is the Euler -function. In (3) we assumed a uniform prior ; a different prior requires minor modifications and does not affect subsequent results. We are interested in the distribution of , i.e. the largest success probability among the arms of the bandit. The probability density is the sum of the contributions by each arm, weighted by the probability for that arm to be the best:

| (4) |

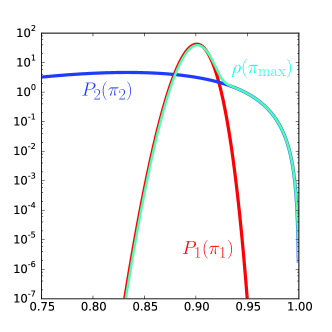

Fig. 1 shows the posterior distributions and when the number of plays is large and . By the law of large numbers, the sample means of the ’s converge to their respective values in the limit of large . It follows that typically , as in Fig. 1. The distribution matches to a large extent the first term in the right hand side of (4) except at the right tail, where the contribution by dominates as . The right tail corresponds to the unlikely event that the inferior sample mean is due to bad luck. Large deviations theory (see [8]) ensures that the probability for to be generated by a true probability of success , is exponentially small in , as we discuss below.

The differential entropy of the continuous distribution is – we shall be interested in the increments of the entropy so that normalization (see Chap. 8 in [8]) is not an issue here. The Info-p strategy chooses the arm which maximizes the expected reduction of entropy . Specifically, the expected reduction upon playing the th arm with the posterior given by (3) is :

| (5) |

where is the likelihood of , which denote win/loss, respectively. The increments are calculated by updating the posterior (3) appropriately, e.g. if then and . The corresponding distribution is then obtained using (4) and the increment of the entropy is finally calculated using the definition of above.

The first arm of the bandit typically gives the dominant contribution to the entropy and Info-p plays it most frequently. However, as increases, the expected variation (5) of the first arm diminishes and the second arm is eventually played, as we proceed to discuss analytically and numerically.

III.2 Optimality of Info-p

In the region around the sample mean , the distribution in (4) can be written as where is approximately normal due to the central limit theorem, and its variance .

The right tail of away from is controlled by the theory of large deviations [8]. Specifically, the probability that a sequence of outcomes with sample mean is generated by a distribution with parameter is , where the Kullback-Leibler divergence was defined above, see (2). It follows from (4) that the right tail of where the second approximation holds for as the distribution of is strongly localized around its sample mean . Ignoring subdominant terms, the contribution to the entropy is . For moderately large , the integral is dominated by the maximum of the exponential term and Laplace method gives .

Adding up the two previous contributions, we conclude that

| (6) |

where is a subdominant prefactor. The first term on the right-hand side of (6) becomes smaller as the first arm is played due to , i.e. it is the exploitative term that selects the arm with the highest sample mean. The second, exploratory term in the right-hand side of (6) accounts for the probability of misclassification, and it reduces as increases.

The neutral decision boundary, i.e. the boundary where the expected reduction of entropy on playing either arm is equal, is calculated for large by equating the variation of the two contributions in (6). By using and neglecting subdominant prefactors, we find

| (7) |

In the limit of large , the sample means tend to their respective values ’s and (7) coincides with the Lai-Robbins bound (2). This establishes the optimality of Info-p, which we shall also verify numerically in the next Section.

Asymptotic optimality is intuited as follows. The order between sample means, say , might be due to fluctuations and we ought to make sure that the true probabilities of success are not inverted, i.e. that . The probability of inversion is by large-deviations theory [8]. The exponential dependence on pushes toward whilst short-term reward pushes to play greedily the arm with the highest sample mean. The optimal trade-off is dictated by marginality of sampling : the number of possible stretches of size times the probability of inversion should satisfy . The dominant order of this expression yields the Lai-Robbins inequality (2) and the marginal case defines the Info-p decision boundary (7).

III.3 Numerical simulations of Info-p

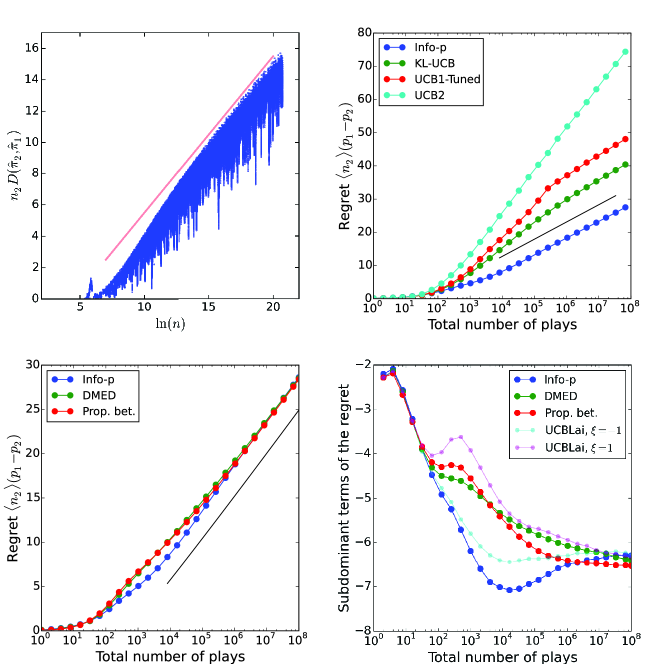

For our simulations, we chose a two-armed bandit with , . At every decision event, we compute the expected variation in entropy and choose the arm to play as described in (5). Subdominant corrections to the regret are [35]. Consequently, clean data for the asymptotic regime require , which is computationally demanding due to the updates of the posteriors at every step.

To simulate the asymptotic regime, we developed an exact numerical technique (see Appendix A) that dramatically speeds up simulations. The logarithmic dependence in (2) implies that asymptotically optimal strategies play long stretches of the estimated best arm, punctuated by short stretches of suboptimal arms. We derive then a rigorous lower bound for the duration of the long stretches and generate a single random variable for the cumulated reward over the entire stretch.

III.4 Comparison between Info-p and other strategies of decision

The goal of this Section is to first briefly introduce state-of-the-art decision strategies whose regret increases logarithmically with , and then compare them with Info-p.

Kelly’s proportional betting [5] (known as Thompson sampling [40] in the machine learning community) is a randomized Bayesian strategy that plays arms with a probability proportional to their respective probability to be the best. Its asymptotic optimality was recently proved in Ref. [40] (see also Appendix B).

Upper Confidence Bound (UCB) strategies are based on an index policy, like Gittins’ index (1), yet the calculation of the index is vastly simplified. Specifically, UCBs are formed by inflating the sample mean estimate of the probability of success of an arm with an additional positive term that accounts for the uncertainty in that estimate. A notable example is the UCB index introduced in Ref. [43] : if the th arm was played times and its sample mean is , the index is defined via : , with . The constant generalizes the value found by considering the Gittins’ index (1) for Gaussian rewards in the limit [44]. The class of models above is asymptotically optimal [44, 43]. The value of is chosen empirically and controls subdominant terms.

Figure 2B shows the comparison between Info-p and UCB-Tuned [37], UCB2 [37], KL-UCB [38], which all exhibit logarithmic regret. However, their prefactor does not saturate the Lai-Robbins bound (2) and UCB regrets are asymptotically bigger as compared to Info-p.

Figures 2C-D present a comparison of the regret vs for Info-p, Kelly’s proportional betting [5], the UCB strategy DMED [39] and the UCBLai index policy [43] for various values of its free parameter . All the algorithms are asymptotically optimal and Info-p compares quite favorably with the others, especially at early and intermediate times when its regret remains below other curves.

III.5 Information about the identity of the best arm

Infomax approaches can pursue information about diverse quantities. For multi-armed bandits, choosing which arm to play requires a priori only the identity of the best arm and not its probability of success. It is then natural to investigate the alternative Infomax approach that maximizes the information gain about the identity of the best arm. This possibility, which was previously mentioned in Ref. [41], is analyzed in detail in the next Section. Here, we determine the maximum possible rate of information gain on .

The estimated probability for the -arm to be the best is denoted . For two-armed bandits, and

| (8) |

The posterior distributions are given by (3).

The entropy of the unknown identity of the best arm is . We are interested in the asymptotic limit of and large. Sample means are then close to their true values and typically satisfy . It follows that is close to unity and

| (9) |

The integrals that define in (8) have three contributions :

(I) The region . There, we have and by large deviations theory [8]. Integrating over and using that the dominant contribution comes from , we obtain .

(II) The region of ’s between and . Its contribution is by large deviations theory. The integral can be calculated by Laplace method (see below) and we denote by the point where the maximum of the exponent is achieved.

(III) Finally, the contribution from the rightmost region of ’s is dominated by and reads .

To minimize – thereby achieving the maximum acquisition of information, see (9) – we must extremize with respect to and . We show in Appendix C that the dominant contribution comes from the second exponential term in (10). The resulting extremum (with ) gives . An important consequence of this equality is that is at a finite distance from and . It follows then from the expression (10) of that , which is also confirmed by explicit expressions derived in the Appendix. As for the fastest rate of decay of the average logarithm of the entropy, we obtain :

| (11) |

where is defined by the equality .

III.6 Info-id

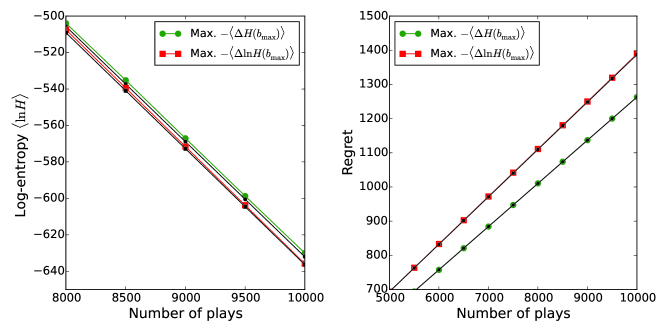

The Info-Id algorithm is defined as the decision strategy that chooses the arm which maximizes the expected reduction of . Specifically, the expected reduction upon playing the -th arm with posterior is analogous to (5) with replaced by . Increments are calculated by updating the posterior as for (5), by using (8) and finally obtaining the increment using the definition of above. This greedy, one-step-in-time procedure indeed achieves the fastest decrease (11) of (see Fig. 3). Note the logarithm in the definition of Info-id : maximizing the expected reduction of would not achieve (11) but a slower decay (see Appendix C).

III.7 The cost and value of information

Information and payoffs embody the two sides of the exploration/exploitation dilemma for multi-armed bandits. The expressions (9), (10) and (11) allow to quantify the trade-offs in the optimal behaviors achieved by Info-p and Info-id, respectively.

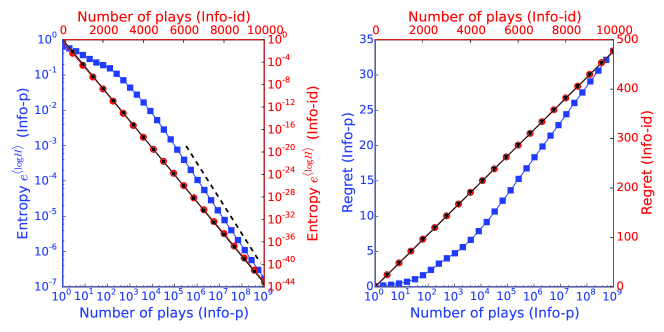

The three relations above show that for Info-id. Since regret is proportional to , we conclude that the rate of decay is proportional to the average regret, i.e. the exponential rate (11) implies a regret linear in , as confirmed by numerical simulations (see Fig. 3).

A very different trade-off underlies the Info-p optimal regret. Indeed, for , the dominant contribution in (10) comes from the last term and implies a power-law decay of the entropy. In particular, if the Lai-Robbins bound (2) is saturated then . The information on the identity of the best arm is therefore reducing much more slowly as compared to Info-id.

The behaviors above clearly illustrate the costs in regret of reducing . However, information about has a definite value that can be exploited to increase payoffs. In particular, if we start playing with some a priori information on the identity of the best arm, i.e. , general distortion-type arguments [8, 10] suggest that payoffs should increase as reduces.

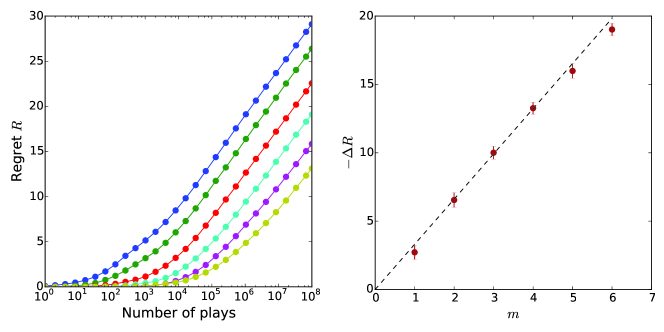

We quantify the value of information by measuring the variation in payoff as a function of . To generate the initial a priori information, we first play the bandit using Info-id until is achieved. Then, we switch to Info-p to compute the regret obtained with those pre-trained priors. Fig. 4 confirms that information on has indeed a positive value, and shows the rate-distortion curve for the variation of regret vs the initial entropy .

The rate-distortion curve in Fig. 4 is rationalized as follows (see Appendix D for details). The Info-id “pre-training” required to reach lasts for steps (see (11)). Since and are both for Info-id, the typical prior resulting from the pre-training is equivalent to the unlikely (for Info-p) situation of a comparable number of plays and for the two arms. Info-p will then play a very long stretch on the first arm until its typical decision boundary (7) is reached. The corresponding reduction in average regret is proportional to the logarithm of the length of the stretch, i.e. . We conclude that , as observed in Fig. 4.

IV Conclusion

We investigated the multi-armed bandit problem [32] with the purpose of gaining insights on Infomax approaches, which postulate a functional role for the acquisition and transmission of information. We introduced two Infomax strategies of decision, and evaluated their performance using known results on optimal decisions for multi-armed bandits.

The first strategy, Info-id, optimally acquires information on the identity of the best arm of the bandit but has a large, asymptotically linear regret. Note that the identity of the best arm is the quantity actually needed for the choice of the arm to play. Therefore, the first natural candidate for an Infomax approach is Info-id, which however performs poorly due to excessive exploration.

The second strategy, Info-p, shifts the balance towards exploitation by gathering information on the highest expected reward among the arms. That pushes to play more frequently the estimated best arm in the bandit. We showed that this strategy yields asymptotically optimal regrets and compares favorably with state-of-the-art methods. The Info-p balance between exploration and exploitation produces a relatively slow acquisition of information on the identity of the best arm, which should be contrasted with the exponential decay achieved by Info-id. The striking differences between Info-p and Info-id clearly demonstrate that the nature of information acquired by Infomax critically matters.

Info-p, like other Infomax approaches, uses information as a proxy, namely of cumulative payoffs for multi-armed bandits. As already mentioned in the Introduction, the advantage is that the proxy has general applicability and that the process of acquisition of information is one-step in time (and greedy in the choice among the options). The first point is important because situations where optimal policies are known are very rare. The second point is relevant because optimal policies often involve extended forecasts in the future, as shown by the example of the Gittins index (1). Such calculations can a priori be formulated as dynamic programming yet in practice the size of the space to sample makes them unfeasible for computers and a fortiori for neural systems or single cells. It is therefore quite non-trivial that optimality on cumulative payoffs can be achieved by an Infomax approach for an appropriate quantity. That constitutes the general lesson drawn here : information in natural or artificial systems could be acquired on quantities that are not immediately recognizable as functionally relevant but could actually allow for effective functional trade-offs.

Acknowledgements.

We are grateful to Boris Shraiman and Eric Siggia for illuminating discussions. MV acknowledges ICTP for hospitality and support. This work was supported by a grant from the Simons Foundation (#340106, Massimo Vergassola).Appendix A Fast Info-p numerical simulations

Info-p is slowed down by posterior distributions (3) sharply peaking around their mean, and accuracy demands progressively finer discretization. To speed up the algorithm, we remark that the Lai-Robbins bound (2) implies that a typical play consists of long stretches of plays of the best arm interspaced with occasional plays of suboptimal ones. Suppose then the Info-p policy selects the best (with largest sample mean) arm for play. We can exactly bound the minimal length of consecutive plays of the best arm as follows : Set the stretch size to some initial guess ; Consider the worst-case scenario of losses throughout the entire stretch ; If the Info-p policy chooses a sub-optimal arm at the end of the stretch, halve the stretch size until the best arm is chosen ; If the Info-p policy chooses the best arm at the end of stretch, double the stretch size until a sub-optimal arm is chosen ; Dissect dichotomically as in binary search algorithms [42] the intervals identified as above. Note that the worst-case scenario of consecutive losses ensures that a lower bound on the stretch length is obtained and the numerical technique is thereby exact.

Once the length of consecutive plays is identified, we generate a random variable for the number of wins during the stretch and update the posterior only once, by using the fact that distributions (3) are conjugate priors for Bernoulli likelihood functions [4]. Discretization of the state space is adaptive and refined as the number of plays increases so as to ensure proper accuracy. We employed a similar procedure for simulations of proportional betting (see B).

Appendix B Proportional betting

Kelly’s proportional betting [5] (also called Thompson sampling in the machine learning community) is a randomized policy that was recently shown to be asymptotically optimal [40]. At each step, the algorithm plays an arm with a probability proportional to its probability to be the best among the arms in the bandit.

Our arguments for showing the optimality of Info-p (see main text) are easily adapted to confirm that proportional betting is indeed optimal. The probabilities for each arm to be the best are denoted . For two arms, in the asymptotic limit and large, we typically have and with and , which again (as for Info-p) leads to .

Since proportional betting is a randomized algorithm, the technique used for the Fast Info-p algorithm (see Appendix A) does not carry over. In the asymptotic limit, the probability that one of the arms is the best is very close to unity. This probability, say , depends primarily on the number of plays of the inferior arms and changes negligibly as the first arm is played. Using this observation, the following approximate algorithm gives very reliable results: the best arm is played for a stretch whose size is randomly chosen from an exponential distribution of mean . Immediately after the stretch, one of the inferior arms is chosen with probabilities . This scheme is exact under the assumption that does not change during the stretch and we found it to be very reliable for the reasons mentioned above. The numerical method is analogous to the Gillespie algorithm used to simulate chemical kinetics [46].

Appendix C Theoretical analysis of information on the identity of the best arm

The goal of this Section is to provide further details about optimal information on the identity of the best arm and the related Info-id policy. The policy greedily maximizes the reduction in log-entropy, , where is the entropy of the unknown identity of the best arm in the bandit. As in the main text, we shall consider the case of a two-armed bandit with probabilities of success and (). Generalizations to bandits with more than two arms are straightforward.

The estimated values of the probabilities of success in a given sample of plays are denoted by and , respectively. Their posterior distributions are given by (3). The sample mean of is indicated by .

We denote by the estimated probability for the first arm to be the best. For a two-armed bandit, and is given by (8). The entropy of the unknown identity of the best arm is : . In the asymptotic limit , when the arms have each been played many times, the sample means are typically close to their respective true values . Large deviation theory [8] states that the th posterior and its cumulative distribution are both dominated by the exponential factor . The probability is then close to unity and the entropy is well approximated by (9).

When , the integrals in (8) and (9) can be calculated by Laplace method and have three contributions :

(I) The region . There, we have and by large deviations theory [8]. Integrating over and using that the dominant contribution comes from , we obtain : .

(II) The region of ’s between and . Its contribution is by large deviations theory. Equating to zero the derivative of with respect to and using the definition of the Kullback-Leibler divergence , we obtain that the extremum is located at

| (12) |

where .

(III) Finally, the contribution from the rightmost region of ’s is dominated by and reads : .

In summary, the asymptotic expression of the entropy is

| (13) |

where are subdominant prefactors.

The expression (13) still depends on and , which are controlled by the policy of play. The fastest possible rate of acquisition of information is obtained by taking the extremum over and with the constraint . Suppose for now (as we shall demonstrate later) that the dominant contribution in (13) is the last one :

| (14) |

The maximum possible rate of reduction of log-entropy is then calculated as follows. If we denote , and differentiate the exponent in (14) with respect to , we obtain the relation

| (15) |

which defines the optimal value . Using the explicit expression of the Kullback-Leibler divergence :

| (16) |

The optimal proportion of plays on the arms follows from (12) :

| (17) |

The decay of the log-entropy averaged over the statistical realizations follows from (14) and (15) :

| (18) |

where and is defined in (16). Note that the average of the log-entropy gives the typical behavior over the realizations, while the entropy itself or its higher powers are determined by large-deviation fluctuations. That leads to anomalous exponents as a function of the power considered. The appropriate statistic for the information gathered in a typical realization is .

The final piece of our analysis is to check that the claimed maximum exponent in (14) is indeed larger than the other two potential candidates and in (13) :

| (19) |

We concentrate on the first relation in (19) ; the second one follows by symmetry. The convexity of in the second argument implies :

| (20) |

where we used the explicit expression of the Kullback-Leibler divergence to calculate the partial derivative at with respect to the second argument. Multiplying by both sides of (20) and using (17), it follows that

| (21) |

The ratio , due to (15), and , due to (17). We conclude that :

| (22) |

To prove (19), it only remains to show that

| (23) |

which follows from the inequality between the Kullback-Leibler divergence and the distance of two distributions (see eqs. 6,7 in [45]). This completes the proof.

C.1 A strategy that maximizes reduction in entropy

Does the Info-id policy (which is greedy in its choice of the arm and one-step in time) attain the maximum rate (18) ? The aim of this subsection is to give a positive answer to this question.

The Info-d policy selects the arm of the bandit which offers the largest expected reduction in log-entropy

| (24) |

where correspond to loss/win and denotes the average with respect to the posterior probability distribution. To calculate , we use the transformations:

| (25) |

Let us calculate the expected variation (24) upon playing the first arm, :

| (26) | |||

| (27) | |||

| (28) |

The first asymptotic equality (26) follows from (14) and (25). The second line (27) is obtained by expanding to first order in its Taylor series for both arguments, which is legitimate as . Finally, for the third line (28) we ignore subdominant terms . Notice that the sum of the third and the fourth terms in (28) vanishes due to (12).

We conclude that

| (29) |

Similarly to (29), when the outcome of the play on the first arm is a win :

| (30) | |||

| (31) |

where a cancellation similar to the one in (28) simplified the final expression (31). We are thereby left with

| (32) |

Finally, combining (29) and (32), we obtain that

| (33) |

By symmetry, . We conclude that the decision boundary of Info-id matches the condition (15) and the policy indeed gathers information on the identity of the best arm at the maximum possible rate.

C.2 Why the variation of log-entropy rather than entropy?

We stressed in the main text that Info-id is based on the expected variation of the log-entropy, as in (24), and not the expected variation of the entropy. The reason is that the expected variation of the dominant term in (13) happens to vanish for the entropy. The choice of the arm to play is then based on subdominant terms, which yields a suboptimal rate as compared to (18). The purpose of this subsection is to clarify this point.

Let us consider the expected variation of the entropy upon playing the th arm :

| (34) |

and consider first the third term (14) (which is the one that gives the fastest possible decay (18)). Using again the transformations (25), its expected variation upon playing the first arm is

| (35) |

Note that the exponents in the first two terms on the right-hand side of (C.2) are related to the objects that we calculated in the previous subsection. Using (29) and (32), it follows then from (C.2) that

| (36) |

If the two terms (29) and (32) at the exponent in (36) were small, then one would Taylor expand the exponentials and conclude that the variation of the entropy and the log-entropy are proportional. However, that is not the case because (29) and (32) are . By inserting the explicit form of the Kulback-Leibler divergence , the first and second terms on the right-hand side of (36) actually reduce to and , respectively. Therefore, the expected variation in the dominant term of the entropy turns out to vanish.

To determine the policy determined by the maximization of the expected decrease of entropy, we need then to consider subdominant terms in (13). Let us start with the first one :

| (37) |

By Taylor expanding the Kullback-Leibler divergence as we have done previously, one can check that the right-hand side in (37) is proportional to the right-hand side in (36) and the expected variation for this term vanishes as well.

The only non-vanishing contribution upon playing the first arm stems from the second term in (13) :

| (38) |

Expanding again to first order in Taylor series, we get

| (39) | ||||

| (40) |

The terms in the curly braces have and only as ratios and tend to non-vanishing constants in the asymptotic limit. The asymptotic behavior is therefore dominated by the exponential decay in . The expected variation upon playing the second arm of the bandit is obtained by interchanging indices. We conclude that

| (41) |

It follows from (41) that the behavior of the policy based on the maximization of the expected reduction of entropy depends on the balance between subdominant terms and that the decision boundary satisfies the relation

| (42) |

It remains to show that the decay of the average log-entropy generated by the policy (42) is still given by the third term in (13) with the exponent evaluated at (and not as for the optimal policy (15)). The inequality to be proved is :

| (43) |

with . The convexity in the second argument of the Kullback-Leibler divergence gives

| (44) | ||||

| (45) |

Summing up the two inequalities above and using (42), the required relation is obtained.

In summary, the policy that maximizes the reduction of entropy (rather than the reduction of log-entropy) yields

| (46) |

The decay is slower than for the optimal value (15), which was derived by extremizing over to obtain the optimal value . In Figure 5, we confirm the theoretical predictions and compare the regret and the entropy for the two algorithms.

Appendix D Quantifying the value of information

The value of information is the reduction in the average regret obtained when some a priori information is available. In this section, we provide details on the theoretical argument sketched in the main text. The initial entropy of the identity of the best arm is supposed to be .

As mentioned in the main text, the “pre-training” with Info-id lasts for steps. Since (14) implies that , the number of steps satisfies with given by (16).

During the pre-training, the two arms are played and times. Their respective proportions are controlled by the expression (17). In particular, . Note that scales linearly with and is therefore much bigger than for typical Info-p statistics, where it would scale logarithmically with .

Since the suboptimal arm has been vastly overplayed in comparison with the typical Info-p statistics, once the algorithm switches to Info-p after the pre-training, a long stretch of plays of the best arm will ensue. The length of the stretch is estimated by calculating the time taken to reach the Info-p decision boundary, i.e. . In the absence of any pre-training, a stretch of length would lead to an average regret (see the Lai-Robbins bound (2) in the main text). We conclude that the expected difference in regret between the case with prior information and the case without, is given by

| (47) |

with and the function defined by (17). The agreement with numerical simulations is shown in Fig. 4. Small deviations are ascribed to finite-size effects, e.g. the Info-p decision boundary that we used to determine the length of the initial stretch is only asymptotically valid, as evidenced in Fig. 2 (upper left panel).

References

- [1] C. E. Shannon. The mathematical theory of communication. Bell Sys Tech J,, 27:379–423, 1948.

- [2] R. G. Gallager. Information Theory and Reliable Communication. Wiley, New York, 1968.

- [3] M. Mézard and A. Montanari. Information, Physics and Computation. Oxford University Press, Oxford, 2009.

- [4] D. J. C. MacKay. Information Theory, Inference and Learning Algorithms. Cambridge University Press, 2003.

- [5] J. L. Kelly. A new interpretation of information rate. Bell System Technical Journal, 35:917–926, 1956.

- [6] R. A. Howard. Information value theory. IEEE Trans Systems Science and Cybernetics, 2:22–26, 1966.

- [7] A. Barron and T. M. Cover. A bound on the financial value of information. IEEE Trans Inf Theory, 34:1097–1100, 1988.

- [8] T. M. Cover and J. A. Thomas. Elements of Information Theory. Wiley, New York, second edition, 2006.

- [9] C. T. Bergstrom and M. Lachmann. Shannon information and biological fitness. Proceedings of the IEEE Workshop on Information Theory, 2004.

- [10] W. Bialek. Biophysics: Searching for Principles. Princeton University Press, 2012.

- [11] E. Kussell and S. Leibler. Phenotypic diversity, population growth, and information in fluctuating environments. Science, 309:2075–2078, 2005.

- [12] M. C. Donaldson-Matasci, C. T. Bergstrom, and M. Lachmann. The fitness value of information. Oikos, 119:219–230, 2010.

- [13] O. Rivoire and S. Leibler. The value of information for populations in varying environments. J Stat Phys, 142:1124–1166, 2011.

- [14] H. B. Barlow. Possible principles underlying the transformation of sensory messages, chapter 13. MIT Press, 1961.

- [15] S. B. Laughlin. The role of sensory adaptation in the retina. J. Exp. Biol, 146:39–62, 1989.

- [16] J. J. Atick and A. N. Redlich. What does the retina know about natural scenes? Neural Computation, 4:196–210, 1992.

- [17] F. Rieke, D. Warland, R. Stevenick, and W. Bialek. Spikes: Exploring the Neural Code. Bradford Book, 1999.

- [18] P. Dayan and L. F. Abbott. Theoretical Neuroscience: Computational and Mathematical Modeling of Neural Systems. MIT Press, Cambridge, 2001.

- [19] R. Cheong, A. Rhee, C. J. Wang, I. Nemenman, and A. Levchenko. Information transduction capacity of noisy biochemical signaling networks. Science, 334:354–358, 2011.

- [20] A. A. Margolin, I. Nemenman, K. Basso, C. Wiggins, G. Stolovitzky, and R. D. Favera. Aracne: An algorithm for the reconstruction of gene regulatory networks in a mammalian cellular context. BMC Bioinformatics, 7, 2006. Supp 1.

- [21] P. François and E. D. Siggia. Predicting embryonic patterning using mutual entropy fitness and in silico evolution. Development, 137:2385–2395, 2010.

- [22] I. Nemenman. Information theory and adaptation. Chapman and Hall/CRC Mathematical and Computational Biology. CRC Press, 2012.

- [23] T. O. Sharpee, A. J. Calhoun, and S. H. Chalasani. Information theory of adaptation in neurons, behavior, and mood. Curr Opin Neurobiol, 25:47–53, 2014.

- [24] G. Tkacik, C. G. Callan Jr., and W. Bialek. Information flow and optimization in transcriptional control. Proc. Natl. Acad. Sci. USA, 105:12265–70, 2008.

- [25] G. Tkacik and A. M. Walczak. Information transmission in genetic regulatory networks: a review. J. Phys.: Condens. Matter, 23(15), 2011.

- [26] R. Linsker. Self-organization in a perceptual network. IEEE Computer, 21(3):105–117, 1988.

- [27] A. J. Bell and T. J. Sejnowski. An information-maximization approach to blind separation and blind deconvolution. Neural Computation, 7:1129–1159, 1995.

- [28] M. Vergassola, E. Villermaux, and B. Shraiman. Infotaxis as a strategy for searching without gradients. Nature, 445:406–409, 2007.

- [29] N. Tishby and D. Polani. Information theory of decisions and actions, pages 601–636. Springer, New York, 2011.

- [30] R. Sutton and A. Barto. Reinforcement Learning: An Introduction. MIT Press, Cambridge, 1998.

- [31] D. A. Berry and B. Fristedt. Bandit problems: sequential allocation of experiments. Springer, Dordrecht, 2001.

- [32] J. Gittins, K. Glazebrook, and R. Weber. Multi-armed Bandit Allocation Indices. John Wiley and Sons, second edition, 2011.

- [33] P. Whittle. Optimization over time, dynamic programming and stochastic control. Wiley Series in Probability and Statistics. 1982.

- [34] J. C. Gittins. Bandit processes and dynamic allocation indices. Journal of the Royal Stat. Soc. B, 6:148–177, 1995.

- [35] T. L. Lai and H. Robbins. Asymptotically efficient adaptive allocation rules. Advances in Applied Mathematics, 6:4–22, 1985.

- [36] A. N. Burnetas and M. N. Katehakis. Optimal adaptive policies for markov decision processes. Mathematics of Operations Research, 22(1), 1997.

- [37] P. Auer, N. Cesa-Bianchi, and P. Fischer. Finite-time analysis of the multi-armed bandit problem. Machine Learning Journal, 47:235–256, 2002.

- [38] O. Cappé, A. Garivier, O. Maillard, R. Munos, and G. Stoltz. Kullback-leibler upper confidence bounds for optimal sequential allocation. Annals of Statistics, 41(3):1516–1541, 2013.

- [39] J. Honda and A. Takemura. An asymptotically optimal bandit algorithm for bounded support models. Proceedings of the Annual Conference on Learning Theory (COLT), 2010.

- [40] E. Kaufmann, N. Korda, and R. Munos. Thompson Sampling: An Asymptotically Optimal Finite Time Analysis, volume 7568 of Lecture Notes in Computer Science, pages 199–213. Springer, Berlin Heidelberg, 2012.

- [41] J. Wyatt. Exploration and Inference in Learning form Reinforcement. Ph.D. thesis, University of Edinburgh, 1997.

- [42] W. H. Press, S. A. Teukolsky, W. T. Vettering, and B. P. Flannery. The Art of Scientific Computing Numerical Recipes in C. Cambridge University Press, second edition, 1992.

- [43] F. Chang and T. L. Lai. Optimal stopping and dynamic allocation. Advances in Applied Probability, 19(4):829–853, 1987.

- [44] T. L. Lai. Adaptive treatment allocation and the multi-armed bandit problem. Annals of Statistics, 15(3):1091–1114, 1987.

- [45] T. van Erven and O. Harremoes. Rényi divergence and kullback-leibler divergence. IEEE Transactions on Information Theory, 60(7):3797–3820, 2014.

- [46] D. T. Gillespie. Exact stochastic simulation of coupled chemical reactions. Journal of Physical Chemistry, 81(25), 1977.