Risk Sensitive Portfolio Optimization in a Jump Diffusion Model with Regimes

Abstract.

This article studies a portfolio optimization problem, where the market consisting of several stocks is modeled by a multi-dimensional jump diffusion process with age-dependent semi-Markov modulated coefficients. We study risk sensitive portfolio optimization on the finite time horizon. We study the problem by using a probabilistic approach to establish the existence and uniqueness of the classical solution to the corresponding Hamilton-Jacobi-Bellman (HJB) equation. We also implement a numerical scheme to investigate the behavior of solutions for different values of the initial portfolio wealth, the maturity, and the risk of aversion parameter.

Key words Portfolio optimization, jump diffusion market model, semi-Markov switching, risk sensitive criterion, finite horizon

AMSC: 91G10, 93E20, 60K15, 60H10

1. Introduction

Following the seminal work of Markowitz [14], the problem of optimization of an investor’s portfolio based on different criteria and market assumptions are being studied by several authors. In the mean-variance optimization approach, as done by Markowitz, either the expected value of the portfolio wealth is optimized by keeping the variance fixed, or the variance is minimized by keeping the expectation fixed. Though the Markowitz’s mean-variance approach to the portfolio optimization is immensely useful in practice, its scope is limited by the fact that only Gaussian distributions are completely determined by their first two moments. In a pioneering work, Merton [15], [16] has introduced the utility maximization to the optimal portfolio selection. Merton’s approach is based on applying the method of stochastic optimal control via an appropriate Hamilton-Jacobi- Bellman (HJB) equation. The corresponding optimal dynamic portfolio allocation can also be obtained from the same equation. Although this approach has greater mathematical tractability but does not capture the tradeoff between maximizing expectation and minimizing the variance of the portfolio value.

There is another approach, namely the risk sensitive optimization where a tradeoff between the long run expected growth rate and the asymptotic variance is captured in implicitly. The aforesaid utility maximization method can be employed to study the risk-sensitive optimization by choosing a parametric family of exponential utility functions. In such optimization, an appropriate value of the parameter is to be chosen by the investor depending on the investors degree of risk tolerance. We refer [1], [4], [5], [13] for this criterion under the geometric Brownian motion (GBM) market model.

Risk sensitive optimization of portfolio value in a more general type of market is also studied by various authors. The jump diffusion model is one of such generalizations which captures the discontinuity of asset dynamics. The empirical results support such models [3]. Terminal utility optimization problem under such a model assumption is studied in [12]. In all these references, it is assumed that the market parameters, i.e., the coefficients in the asset price dynamics, are either constant or deterministic functions of time. We study a class of models where these parameters are allowed to be finite state pure jump processes. We call each state of the coefficients as a regime and the dynamics, as a regime switching model. The regime switching can be of various types. It is known that for a Markov switching model, the sojourn or holding times in each state are distributed as exponential random variables, whereas the holding time can be any positive random variable for the semi-Markov case. Thus the class of semi-Markov processes subsumes the class of Markov chains. There are some statistical results in the literature (see [2], [11] and the references therein), which emphasize the advantage of the applicability of semi-Markov switching models over simple homogeneous Markov switching models. It is mainly useful to deal with the impact of a changing environment, which exhibits duration dependence. To understand this, consider a market situation where, if the volatility of a certain stock price remains low for longer than certain duration, then that observation discourages increasingly more traders to trade on that, depending on the length of the duration. In that case, this type of duration dependence mass-trading behavior might cause further low volume trading resulting in lack of volatility boost. In this type of market behavior, the density function of holding time of low volatility regime should exhibit heavier tail than exponential. It is important to note that, a Markov chain either time homogeneous or inhomogeneous, does not exhibit such age-dependent transition, whereas a generic semi-Markov process may exhibit this phenomenon. It motivates us to consider the age-dependent transition of the regimes.

Risk sensitive portfolio optimization in a GBM model with Markov regimes is studied in [7] whereas [6] studies the same problem in a semi-Markov modulated GBM model. In [6] the market parameters, , and are driven by a finite-state semi-Markov process , where and denote the drift and volatility parameters of the -th asset in the portfolio. Strictly speaking, the assumption that all the parameters from different assets are governed by a single semi-Markov process is rather restrictive. Ideally, those could be driven by independent or correlated processes in practice. Although two independent Markov processes jointly becomes a Markov process, the same phenomena is not true for semi-Markov processes. For this reason, the case of independent regimes are important where regimes are not Markov.

In general, a pure jump process need not be a semi-Markov process. In particular, the class of age-dependent processes (as in [8]) is much wider than the type of age independent semi-Markov processes studied in [6]. In a recent paper [9], option pricing is studied in a switching market where the regimes are assumed to be an age-dependent process. An age-dependent process on a finite state space is specified by its instantaneous transition rate , which is a collection of measurable functions where and . Indeed, embedding in , an age-dependent process on is defined as the strong solution to the following system of stochastic integral equations (SIEs)

| (1.1) |

where is the Poisson random measure with intensity , independent of , and

and for every , , using a strict total order on . In particular can be taken as lexicographic ordering. The existence of unique strong solution of the SIEs (1.1) follows from ([10], Chap. IV, p.231), since and are compactly supported in variable. We refer to [8] for a proof that indeed represents the instantaneous transition rate of .

In this paper, we consider a regime switching jump diffusion model of a financial market, where an observed Euclidean space valued pure jump process drives the regimes of every asset. Further, we assume that every component of that pure jump process is an age-dependent semi-Markov process and the components are independent. We study the finite horizon portfolio optimization via the risk sensitive criterion under the above market assumption. The optimization problem is solved by studying the corresponding HJB equation, where we employ the technique of separation of variables to reduce the HJB equation to a system of linear first order PDEs containing some non-local terms. In the reduced equation, the nature of non-locality is such that the standard theory of integro-pde is not applicable to establish the existence and uniqueness of the solution. In this paper, to show well-posedness of this PDE, a Volterra integral equation(IE) of the second kind is obtained and then the existence of a unique solution is shown. Then it is proved that the solution to the IE is a classical solution to the PDE under study. The uniqueness of the PDE is proved by showing that any classical solution also solves the IE. In the uniqueness part, we use conditioning with respect to the transition times of the underlying process. Besides, we also obtain the optimal portfolio selection as a continuous function of time and underlying switching process. The expression of this function does not involve the functional parameter . Thus the optimal selection is robust. Our approach of solving the PDE also enables us to develop a robust numerical procedure to compute the optimal portfolio wealth using a quadrature method.

The rest of the paper is organized as follows. In the next section, we give a rigorous description of the model of a financial market dynamics and then derive the wealth process of an investor’s portfolio. The problem of optimizing the portfolio wealth under the risk sensitive criterion on the finite time horizon is also stated in Section 2. In Section 3 we have established a characterization of the optimal wealth using the corresponding Hamilton-Jacobi-Bellman equation. An optimal portfolio strategy is also shown to exist in the class of Markov feedback control. Furthermore, an optimal feedback control is produced as a minimizer of a certain functional associated with the HJB equation. We illustrate the theoretical results by performing numerical experiments with an example and obtain some relevant results in Section 4. Section 5 contains some concluding remarks. The proofs of certain important lemmata are given in the Appendix.

2. Model Description

2.1. Model parameters

Let denote a finite subset of . Without loss of generality, we choose and as defined above (1.1). Consider for each , a continuously differentiable function in with and

Assume that for each , denotes a finite Borel measure on . Let , , and be continuous functions of the time variable for each , where and are the positive integers. We also consider a collection of measurable functions for each , .

We further introduce some more notations. Fix and and we denote , and , where is the -th component of function. For each , we denote . We use to denote transpose of a vector.

2.2. Asset price model

Let be a complete probability space. Let be a collection of many valued random variables, and be a collection of non negative random variables. Let be a standard -dimensional Brownian motion. We further assume that, on and on are two sets of Poisson random measures with intensities and respectively defined on the same probability space. We recall that denotes a finite Borel measure for each . It is important to note that the random variables, processes and measures are defined in such a way that they are independent. We denote the compensated measures by for and for . For each , let be the solution to (1.1) with replaced by , by , by , and by . In other words

| (2.1) | |||||

| (2.2) |

where and . We denote the tuple by and by . Hence, , and are independent. The process is a time homogeneous strong Markov process.

Let the filtration be the right continuous augmentation of the filtration generated by such that contains all the -null sets. We consider a frictionless market consisting of assets whose prices are denoted by and and are traded continuously. We model the hypothetical state of the assets at time by the pure jump process . The state of the asset indicates its mean growth rate and volatility. We assume

Thus the corresponding asset is (locally) risk free, which refers to the money market account with the floating interest rate at time corresponding to regime . The other asset prices are assumed to be given by the following stochastic differential equation

| (2.3) | ||||

These prices correspond to different risky assets. Therefore, represents the growth rate of the -th asset and the volatility matrix of the market. Here we further assume the following.

Assumptions :

-

(A1)

For each and , we assume .

-

(A2)

For each and , we further assume .

-

(A3)

Let denote the diffusion matrix. Assume that there exists a such that for each and , , where denotes the Euclidean norm.

The next lemma asserts the existence and uniqueness of the solution to the SDE (2.3). The proof is deferred to the appendix.

Lemma 2.1.

Under the assumption (A2) the equation (2.3) has a strong solution, which is adapted, a.s. unique and an rcll process.

Remark 2.2.

We note that (A1) and (A2) follow for the special case where

By (A3) the diffusion matrix is uniformly positive definite, which ensures that is invertible. We will use this condition in Section 3. This condition also implies that .

2.3. Portfolio value process

Consider an investor who is employing a self-financing portfolio of the above assets starting with a positive wealth. If the portfolio at time comprises of number of units of -th asset for every , then for each the value of the portfolio at time is given by

We allow be real valued, i.e., borrowing from the money market and short selling of assets are allowed. We further assume that is an adapted, rcll process for each . Then the self-financing condition implies that

If are such that remains positive, we can set , the fraction of investment in the -th asset. Then we have and hence . We call as the portfolio strategy of risky assets at time . Then the wealth process, , now onward denoted by , takes the form

Thus we would consider the following SDE for the value process,

| (2.4) |

where . Note that, some additional assumptions on are needed for ensuring a positive strong solution of (2.3).

Remark 2.3.

As before, we need to assume that is such that for each , and , to ensure a positive solution to (2.3). For some technical reasons we require a stronger condition on . We would require that the the portfolio should be chosen from

| (2.5) |

It is clear from the definition and the above derivation that , the portfolio wealth process, is a controlled process. Let be a convex set containing the origin, denoting the range of portfolio. The range is determined based on the investment restrictions. For example, in the case of unrestricted short selling. The restrictions on short selling makes , where for . Clearly, for , correspond to no short selling.

Definition 2.4.

Proposition 2.5.

Under (A1) and with admissible control , (i) the SDE (2.3) has an almost sure unique positive strong solution, (ii) the solution has finite moments of all positive and negative orders, which are also bounded on uniformly in .

Proof.

(i) We first note that, since and satisfies Definition 2.4(iii),

where and is the -th column of the matrix . Again using (A1) and the finiteness of the measure , the integration of the above upper bound with respect to has finite expectation. This implies that . Therefore in the similar line of the proof of Lemma 2.1, we can show, under the assumption (A1) and the admissibility of , (2.3) has an a.s. unique positive rcll solution, which is an adapted process, and the solution is given by

| (2.6) |

(ii) We first consider the first order moment. To prove for each , has a bounded expectation, we first note that the right hand side can be written as a product of a conditionally log-normal random variable and , where both are conditionally independent, given the process . We further note that the log-normal random variable has bounded parameters on uniformly in . Therefore it is sufficient to check if

is bounded on , for all . By applying Lemma A.1, one can show that the above expectation is bounded on . Thus has bounded expectation on , uniformly in . Now for the moments of general order, we note that for any can also be written in a similar form of (2.3) where each of the integrals inside the exponential would be multiplied by the constant . Thus the rest of the proof follows in a similar line of that of first order case, given above.∎

Our goal is to study a risk sensitive optimal control problem on the above wealth process. We would see in the next section that, in order to obtain a classical solution to the corresponding HJB equation, to be defined shortly, certain regularity of the conditional c.d.f of holding time of is needed. We devote the next subsection to establishing some smoothness of relevant density functions.

2.4. Regularity properties of holding time distributions

Let be the time of -th transition of the -th component of , whereas and . We define the function as and let and for each with for all and . Set

We assume further conditions on the transition rate so that the unconditional transition probability matrix is irreducible.

Assumption: (A4) The matrix is irreducible,

for all

From the definition of and the assumptions on , we observe , for all . We also note that hold for all . For a fixed , let . Hence and . It is shown in [8] that is the instantaneous transition rate function of the semi-Markov process , i.e.,

Furthermore, is the conditional c.d.f of the holding time of and is the conditional probability that transits to from given the fact that it is at for a duration of . Let the remaining life of -th component i.e., the time period from time after which the -th component of would have the subsequent transition. Note that is independent of every component of other than -th one. We denote the conditional c.d.f and p.d.f of given and as and respectively. It is important to note that this c.d.f does not depend on , mainly because is time-homogeneous. We also notice that is the duration of stagnancy of at present state before it moves to another. From now we denote by and the corresponding conditional expectation as . Let be the component of , where the subsequent transition happens. Therefore, represents the conditional probability of observing next transition to occur at the -th component given that and . We find the expressions of the c.d.f and the probability defined above and obtain some properties in the following lemma. The proof is deferred to the appendix. In order to state the lemma, we introduce some more notations. We define an open set

and a linear operator

where dom(), the domain of is the subspace of such that for each dom() above limit exists for every and , and is a vector with each component .

Lemma 2.6.

Consider as given above.

(i) For each ,

(ii) Let be the conditional c.d.f of given and . Then

| (2.7) |

and is in variable.

(iii)

| (2.8) |

is differentiable with respect to .

(iv) and are in dom() . Furthermore,

(v) .

2.5. Optimal Control Problem

In this paper we consider a risk sensitive optimization criterion of the terminal portfolio wealth corresponding to a portfolio , that is given by

which is to be maximized over all admissible portfolio strategies with constant risk aversion parameter . Since logarithm is increasing, it suffices to consider the following cost function

which is to be minimized. For all , let

| (2.9) |

where the infimum is taken over all admissible strategies as in Definition 2.4. Hence, corresponds to the optimal value.

Let be an admissible strategy such that it has the following form for some measurable . We call such controls as Markov feedback control. Then the augmented process is Markov where, are as in (2.1), (2.2), (2.3). We note that for any measurable , the equation (2.3) may not have a strong solution. However, we will show the existence of a Markov feedback control which is optimal and under which (2.3) has an a.s. unique strong solution.

Let be the infinitesimal generator of , and be a function with compact support, then we have

| (2.10) |

where the linear operator is given by , , and is the standard basis of . For a given , by abuse of notation, we write , when for all . We consider the following HJB equation

| (2.11) |

with the terminal condition

| (2.12) |

To study the HJB equation we now define following classes of functions

Definition 2.7.

Let be such that for every the following hold:

-

(i)

is twice continuously differentiable with respect to for all and is in dom() for each ,,

-

(ii)

for fixed , ,

-

(iii)

for each , is in .

3. Hamilton-Jacobi-Bellman Equation

We look for a solution to (2.11)-(2.12) of the form

| (3.1) |

where . Clearly, the left hand side of (3.1) is in class . We will establish the following result in first two subsections.

Substitution of (3.1) into (2.11), yields

| (3.2) |

for each with the condition

| (3.3) |

where the map is given by

| (3.4) |

the infimum of a family of continuous functions

It is important to note that the linear first order equation (3.2) is nonlocal due to the presence of the term in the equation. It implies that depends on the value of at the point , which does not lie in the neighbourhood of . We now define a classical solution to (3.2)-(3.3) below.

Definition 3.2.

Remark 3.3.

It is interesting to note that other than the terminal condition (3.3), no additional boundary conditions are imposed. The remaining part of the boundary is . We note from (2.2) that, , for all . Hence does not cross the boundary. Thus the value of solution on the boundary is obtained from the terminal condition (3.3).

Remark 3.5.

Note that Theorem 3.1 may be treated as a corollary of Theorem 3.4 in view of the substitution (3.1) and subsequent analysis. Thus it suffices to establish Theorem 3.4. We establish Theorem 3.4 in the subsection 3.2 via a study of an integral equation which is presented in subsection 3.1. The following result would be useful to establish well-posedness of (3.2)-(3.3).

Proposition 3.6.

Consider the map , given by, (3.4). Then under (A3), we have

-

(i)

is continuous, negative valued and bounded below;

-

(ii)

is in both and for each ;

-

(iii)

For every , there exists a unique such that and is continuous in ;

-

(iv)

is admissible.

Proof.

(i) We recall that, , the range of portfolio includes the origin. Therefore

Thus is negative valued. By the continuity assumptions on and , for fixed and each , , and are bounded on . Let be such that

We also observe that for each ,

using the finiteness of the measure . Also, (A3) gives Hence by using the above mentioned bounds, we can write, , where

Since is independent of and as , is bounded below. Now we will show that for fixed and , is a strictly convex function of variable . For fixed and , let denote the Hessian matrix for . Then -th element of ,

Since is in , is bounded below by a positive . Hence, in addition to that using (A3), there exists such that is a positive definite matrix and this proves the strict convexity of on variable . Therefore is a non-empty convex compact set. Hence, is a compact-valued correspondence. Since is negative, from (3.4), we can write

We also note that is jointly continuous. Since is continuous, then it follows from the Maximum Theorem ([18],Th. ) that is continuous with respect to . Hence (i) is proved.

(ii) Follows from the continuity of .

(iii) The set of minimizers is defined by

Again by using ([18],Th. ), is upper semi-continuous. Since is strictly convex in , for each and there exist only one element in . By abuse of notation, we denote that element by itself. Since a single-valued upper semi-continuous correspondence is continuous, is a continuous function.

(iv) Since is continuous in , there exists a positive constant such that for all , . Thus is bounded. Since does not depend on , the Lipschitz conditions of Theorem 1.19 of [17] are satisfied. Again since is bounded, all growth conditions are also satisfied. Therefore Definition 2.4(ii) is satisfied and this completes the proof. ∎

3.1. Volterra Integral equation

In order to study (3.2)-(3.3) we consider the following integral equation with the previous notations and for all

| (3.5) |

Equation (3.1) is a Volterra integral equation of second kind. We note that the boundary of has many facets. For , we directly obtain from (3.1), . Hence no additional terminal conditions are required. Although the values of in facets are not directly followed but can be obtained by solving the integral equation on the facets.

Proposition 3.7.

(i) The integral equation (3.1) has a unique solution in , and (ii) the solution is in the dom().

Proof.

(i) We first observe that the solution to the integral equation (3.1) is a fixed point of the operator , where

It is easy to check that for each is bounded continuous. Now

where , since the row sum of conditional probability matrix is and by Proposition 3.6(i). Since is strictly less than , (2.7) implies that , for all . Hence . Therefore, is a contraction. Thus a direct application of Banach fixed point theorem ensures the existence and uniqueness of the solution to (3.1).

(ii) We denote the unique solution by . Next we show that dom. To this end, it is sufficient to show that . The first term of is in dom, which follows from Lemma 2.6 (iv) and Proposition 3.6 (ii). Now to show that the remaining term

is also in the dom() for any , we need to check if the following limit

exists and, the limit is continuous in . If the limit exists, the limiting value is clearly . By a suitable substitution of variables in the integral, the expression in the above limit can be rewritten, using (2.8), as

| (3.6) | |||||

By Lemma 2.6 (iv), is in . Thus is bounded on by a positive constant . Hence by the mean value theorem on , the integrand of the first integral of (3.6) is uniformly bounded. Therefore, using the bounded convergence theorem, the integral converges as . The second integral of (3.6) converges as the integrand is continuous at . Now we compute

using Lemma 2.6 (iii). From (A.9) we know , therefore can be rewritten using (2.8) as

| (3.7) |

Clearly, (3.1) is in . Hence is in the dom(). Hence the right hand side of (3.1) is in the dom() for any . Thus (ii) holds. ∎

3.2. The linear first order equation

Proof.

Let be the solutions of the integral equation (3.1). Then by substituting in (3.1), (3.3) follows. Using the results from the proof of Lemma 2.6, Proposition 3.7, Lemma 2.6(iv) and (3.1), we have

Using (3.1) and the equality in Lemma 2.6(v), the right hand side of above equation can be rewritten as

Hence satisfies (3.2). ∎

Proposition 3.9.

Proof.

If the PDE (3.2) has a classical solution , then is also in the domain of , where is the infinitesimal generator of the Markov family starting from (say). Then we have from (3.2)

| (3.8) |

Consider

Then by Itô’s formula,

where is a local martingale with respect to , the usual filtration generated by . Thus from (3.8) is a local martingale. From definition of , a.s. Thus is a martingale. Therefore by using (3.3), we obtain

using the Markov property of . Thus

| (3.9) |

By conditioning on the component of where the transition happens,

| (3.10) | |||||

where is described in subsection 2.4 below (A4). Next by conditioning on we rewrite

Since is constant on provided , the above expression is equal to

From (3.10) and the above expression, the desired result follows. ∎

3.3. Optimal portfolio and verification theorem

Now we are in a position to derive the expression of optimal portfolio value under risk sensitive criterion. The optimal value is given by

| (3.11) |

where the function is defined in (2.9) and is the unique classical solution to (3.2) - (3.3) obtained in Theorem 3.4.

Remark 3.10.

We note that the study of (3.2)-(3.3) becomes much simpler if the coefficients are independent of time . For time homogeneous case, Proposition 3.6 is immediate. Furthermore, the proof of Theorem 3.4 does not need the results given in Proposition 3.7, Proposition 3.8, and Proposition 3.9. Indeed Theorem 3.4 can directly be proved by noting the smoothness of terminal condition.

We conclude this section with a proof of the verification theorem for optimal control problem (2.9). The main result is given in Theorem 3.12.

Proposition 3.11.

Proof.

(i) Consider an admissible Markov feedback control , where and , the classical solution to (2.11)-(2.12) as in (3.1). Now by Itô’s formula

| (3.12) |

We would first show that the right hand side is an martingale. Since is admissible, using definition 2.4(iii), it is sufficient to show, the following square integrability condition

to prove that the first term is a martingale. Again since , . Thus using the boundedness of the above would follow if

| (3.13) |

holds. Now we consider the second integral. Rewriting that term, we obtain

| (3.14) |

We first observe that , and this implies

Thus the integrand of (3.14) is a product of a bounded function and . Since , the Lévy measure of is a finite measure for each , to show (3.14) is an martingale, it is enough to verify (3.13). Similarly the third integral can be rewritten as

| (3.15) |

In (3.3) the integrand is a product of a bounded function with compact support and . Since, the compensator of is , (3.3) is also an martingale if (3.13) holds. Thus (3.13) is the sufficient condition for the right side of (3.3) to be a martingale. However (3.13) readily follows from the Proposition 2.5(ii) and an application of Tonelli’s Theorem.

Taking conditional expectation on both sides of (3.3) given and letting , we obtain

| (3.16) |

The above non-negativity follows, since is the classical solution to (2.11)-(2.12) and for all . Hence (2.9) and (3.3) imply result (i).

(ii) The right hand side of (3.3) becomes zero by considering and this completes the proof of (ii). ∎

Finally we show in the following theorem that as in Theorem 3.1 indeed gives the optimal performance under all admissible controls.

Theorem 3.12.

Let be as in Theorem 3.1 and . Then .

Proof.

We first note that in the proof of Proposition 3.11(i), we have only used the properties (ii) and (iii) of Definition 2.4 of the Markov control. Since these two properties are true for a generic admissible control , we can get as in Proposition 3.11(i).

for every admissible control . By taking infimum, we get . The other side of inequality is rather straight forward. Using Proposition 3.11(ii) and Theorem 3.6(iv), is admissible, and . Thus . Hence the result is proved.∎

Now we establish a characterisation of using the HJB equation in the following Proposition.

Proposition 3.13.

Proof.

Note that in the Proof of Proposition 3.11(i), to show that the right hand side of (3.3) is a martingale, we have only effectively used the fact that satisfies conditions (i),(ii) and (iii) of Definition 2.7. Hence for any and as in Proposition 3.6(iv),

| (3.17) |

is an martingale. Taking conditional expectation in (3.17), given and letting , we have

using . Now using nonnegativity of right side and Proposition 3.11(ii), we obtain .∎

4. Numerical Example

We have seen that the optimal portfolio value with risk sensitive criterion is given by (3.3) and (3.2) - (3.3). For illustration purpose, we are considering a simple model in which all the parameters for all assets are governed by a single semi-Markov process. Then if , and we denote that value as where and are the first components of , and respectively. Hence (3.9) implies provided and . In other words depends only on . In view of this, we may introduce a new function to denote . Therefore (3.2) gets reduced to

| (4.1) |

for every , , . We further assume that , i.e., the portfolio includes a single stock and a money market instrument. We also specify the state space , i.e., the semi-Markov process has three regimes. The drift coefficient, volatility and instantaneous interest rate at each regime are chosen as follows:

The transition rates for are assumed to be given by

where

Hence the holding time of the first component in each regime has the conditional probability density function and the conditional c.d.f . We also assumed and .

It is shown separately in [6] that the classical solution to (4.1) with , satisfies the following integral equation

| (4.2) |

which also follows from (3.1). Here we compute by discretization of above integral equation using an implicit step-by-step quadrature method as developed in [6]. We take , so . The discretization is given by

Therefore from (4) we get

| (4.3) |

where are weights, chosen as below

and

For a given initial portfolio value , from (3.3) and (4) we get

| (4.4) |

Thus the numerical approximation of risk sensitive optimal wealth is given by (4)-(4.4).

In Proposition 3.6 we have seen that there exists a unique which gives and that we can find by using any convex optimization technique. Here we have used the interior-point method to find the optimal .

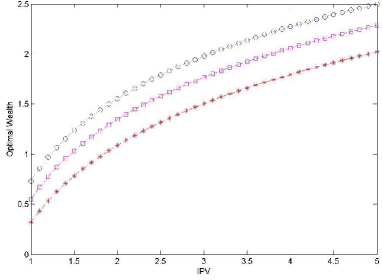

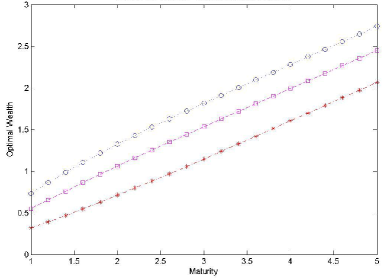

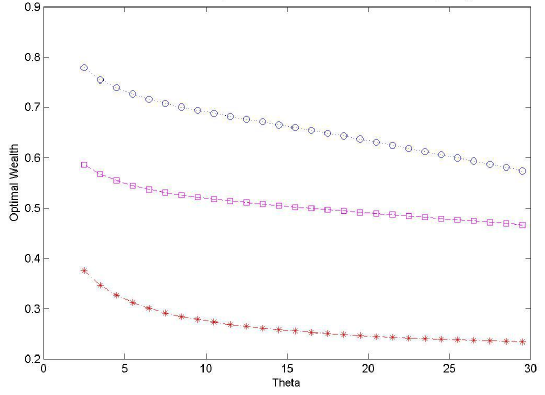

We use above mentioned numerical scheme to compute the risk sensitive optimal wealth function given in (4.4). In all figures each line corresponds to a particular value of . To be more precise the cross line corresponds to , whereas the box and circle lines are for and . Figure 1 describes the behavior of risk sensitive optimal wealth for different values of initial portfolio wealth and maturity. The left side plot in figure 1 shows that the optimal wealth is increasing and concave with the value of initial investment. This is due to the concavity of our objective function. On the other hand the right side plot shows linearity of the optimal wealth with respect to the the maturity of investment. We also note a strict hierarchy of optimal wealth according to the market parameter values at different regimes. However a detailed analysis based on series of numerical experiments may reveal some finer sensitivity results. We refrain to discuss those in this paper. Figure 2 shows the movement in risk sensitive optimal wealth for different values of risk aversion parameter. The plot shows the strict diminishing behavior of risk sensitive optimal wealth for increasing risk aversion parameter value. This observation is consistent to the common sense “no risk, no gain”.

5. Conclusion

In this paper a portfolio optimization problem, without any consumption and transaction cost, where stock prices are modelled by multi dimensional geometric jump diffusion market model with semi-Markov modulated coefficients is studied. We find the expression of optimal wealth for expected terminal utility method with risk sensitive criterion on finite time horizon. We have studied the existence of classical solution of HJB equation using a probabilistic approach. We have obtained the implicit expression of optimal portfolio. It is important to note that, the control is robust in the sense that the optimal control does not depend on the transition function of the regime. We have also implemented a numerical scheme to see the behavior of solutions with respect to initial portfolio value, maturity and risk of aversion parameter. The results of the numerical scheme are in agreement with the theory of financial market. The corresponding problem in infinite horizon is needs further investigation. This would require appropriate results on large deviation principle for semi-Markov processes which need to be carried out.

Appendix A Proof of Lemmata

Lemma A.1.

Let be a Poisson random measure on defined on the probability space with intensity , where is a finite measure. If , then there exists a positive constant such that

Proof.

We first note that is finite a.s. as . Therefore the integral can be written as , where are the point masses of on . To be more precise, for all . Therefore

| (A.1) |

Since are conditionally independent and identically distributed given , the right side is equal to

Now using , and , the above sum is equal to

Hence the proof. ∎

Proof of Lemma 2.1.

First we show the uniqueness by assuming that the SDE (2.3) admits a solution, , say, the stopping time . Using Itô Lemma (Theorem 1.16 of [17]) for we get,

Integrating both sides from 0 to yields,

where all the integrals have finite expectations almost surely by using (A2).

| (A.2) |

Thus any solution to (2.3) has the above expression. Under (A2), has finite expectation for any finite stopping time .

Let . Now if possible, assume . By letting in the above expression, we obtain that is exponential of a random variable which is finite for almost every . Thus . But for almost every . Hence non-positivity occurred only by jump. In other words for some . But that is contrary to the assumption on . Hence . Therefore, a.s. for all and is given by

| (A.3) |

Thus by equation (A), is an adapted and rcll process and is uniquely determined with the initial condition . Hence the solution is unique.

Proof of Lemma 2.6.

(i) One can compute the conditional c.d.f in the following way

| (A.4) | |||||

We also denote the derivative of by , given by

| (A.5) |

From the definition of we have,

| (A.6) | |||||

We also introduce a new variable . We denote the conditional c.d.f of given and as which is equal to .

It is easy to see that . To compute this probability we use a conditioning on . Thus

| (A.7) | |||||

(ii) From (A.6), one gets (2.7). Since is in , is in . Thus by fundamental theorem of calculus, is twice differentiable wrt .

(iii) Follows directly from (ii).

(iv) In order to show that and belong to we introduce a new function and . Consider another function

| (A.8) |

We note that is the derivative of with respect to and it is continuous. Now we show that is in . To this end we first show the existence of the following limit

By a suitable substitution of variable, the expression in the above limit is

Using (A.8) the above expression converges to as and the limit is continuous in . Thus

If is a differentiable function of , then

Hence

| (A.9) |

Since

it follows from Lemma 2.6 (i), (ii) and the above notations and . Hence and are in the dom(). Now operating on and using (A.5), (A.8) we have

Operating on

This completes the proof of (iv).

(v) Follows from a direct calculation.

∎

Acknowledgement: The authors are grateful to Mrinal K. Ghosh and Anup Biswas for very useful discussions.

References

- [1] Bielecki T. R. and Pliska S. R., Risk-Sensitive Dynamic Asset Management, App. Math. Optim., 39(1999), 337-360.

- [2] Bulla, Jan, and Ingo Bulla., Stylized facts of financial time series and hidden semi-Markov models. Computational Statistics & Data Analysis 51.4 (2006): 2192-2209.

- [3] Dungeya Mardi, McKenziea Michael and Smith L. Vanessa, Empirical evidence on jumps in the term structure of the US Treasury Market, Journal of Empirical Finance, 16 (2009) 430-445.

- [4] Fleming W. H. and Sheu S. J., Risk-sensitive control and an optimal investment model, Math. Finance, 10(2000), 197-213.

- [5] Fleming W. H. and Sheu S. J., Risk-sensitive control and an optimal investment model(II), Ann. Appl. Probab., 12(2002), 730-767.

- [6] Ghosh M. K., Goswami A., and Kumar, S., Portfolio Optimization in a Semi-Markov Modulated Market, Appl Math Optim, 60(2009), 275-296.

- [7] Ghosh M. K., Goswami, A., and Kumar, S., Portfolio Optimization in a Markov Modulated Market, Modern Trends in Controlled Stochastic Processes, 181-195, 2010.

- [8] Ghosh M. K. and Saha, S., Stochastic processes with age-dependent transition rates, Stoch. Ann. App. 29(2011), 511-522.

- [9] Goswami, A., Patel, J. and Shevgaonkar, P., A system of non-parabolic PDE and application to option pricing, Stoch. Anal. Appl. 34(2016), 893-905.

- [10] Ikeda, N., and S. Watanabe., Stochastic differential equations and diffusion processes. N orth-Holland, Amsterdam (1981).

- [11] Hunt J. and Devolder P., Semi-Markov regime switching interest rate models and minimal entropy measure, Physica A: Statistical Mechanics and its Applications 390, 15(2011), 3767-3781.

- [12] Kallsen Jan, Optimal portfolios for exponential Lévy processes. Math. Methods Oper. Res. 51 (2000), 357-374.

- [13] Lefebvre M. and Montulet P., Risk sensitive optimal investment policy, Internat. J. Systems. Sci., 22 (1994), 183-192.

- [14] Markowitz H., Portfolio Selection : Eficient Diversification of Investments, Wiley (1959).

- [15] Merton, C, Lifetime portfolio selection under uncertainty: the continuous case, Rev. Econ. Stat. 51 (1969), 247-257.

- [16] Merton, C, Optimal consumption and portfolio rules in a continuous-time model, J. Econ. Theory 3 (1971), 373-413.

- [17] Øksendal, B. and Sulem, A., Applied Stochastic Control of Jump Diffusions, Springer Berlin Heidelberg New York, 1st edition, 2005.

- [18] Sundaram, Rangarajan. K., A first course in optimization theory, Cambridge University Press, 1996.