Regularized Jacobi iteration for decentralized convex optimization with separable constraints

Abstract

We consider multi-agent, convex optimization programs subject to separable constraints, where the constraint function of each agent involves only its local decision vector, while the decision vectors of all agents are coupled via a common objective function. We focus on a regularized variant of the so called Jacobi algorithm for decentralized computation in such problems. We first consider the case where the objective function is quadratic, and provide a fixed-point theoretic analysis showing that the algorithm converges to a minimizer of the centralized problem. Moreover, we quantify the potential benefits of such an iterative scheme by comparing it against a scaled projected gradient algorithm. We then consider the general case and show that all limit points of the proposed iteration are optimal solutions of the centralized problem. The efficacy of the proposed algorithm is illustrated by applying it to the problem of optimal charging of electric vehicles, where, as opposed to earlier approaches, we show convergence to an optimal charging scheme for a finite, possibly large, number of vehicles.

Index Terms:

Decentralized optimization, Jacobi algorithm, iterative methods, optimal charging control, electric vehicles.I Introduction

Optimization in multi-agent systems has attracted significant attention in the control and operations research communities, due to its applicability to different domains, e.g., energy systems [1], [2], mobility systems [3], [4], [5], robotic networks [6], etc. In this paper we focus on a specific class of multi-agent optimization programs that are convex and are subject to constraints that are separable, i.e., the constraint function of each agent involves only its local decision vector. The agents’ decision vectors are, however, coupled by means of a common objective function. The considered structure, although specific, captures a wide class of engineering problems, like the electric vehicle optimal charging problem studied in this paper. Solving such problems in a centralized fashion would require agents to share their local constraint functions with each other, while even if this was possible it would unnecessarily increase the computational burden.

To allow for a computationally tractable solution, while accounting for information sharing issues, we adopt an iterative, decentralized perspective, where agents perform local computations in parallel, and then exchange with each other their new solutions, or broadcast them to some central authority that sends an update to each agent. Admittedly, distributed optimization offers a more general communication setup, however, the fact that agents decision vectors are coupled via the objective function poses additional difficulties, preventing the use of standard distributed algorithms [7], [8]. Even upon an epigraphic reformulation, the resulting problem will not exhibit the structure typically encountered in distributed optimization since the resulting coupling constraint will not necessarily be of “budget” form as required, e.g., in [9].

I-A Related work

From a cooperative optimization point of view, algorithms for decentralized solutions to convex optimization problems with separable constraints can be found in [10, 11], and references therein. Two main algorithmic directions can be distinguished, both of them relying on an iterative process. The first one is based on each agent performing at every iteration a local gradient descent step, while keeping the decision variables of all other agents fixed to the values communicated at the previous iteration [12, 13, 14]. Under certain structural assumptions (differentiability of the objective function and Lipschitz continuity of its gradient), it is shown that this scheme converges to some minimizer of the centralized problem, for an appropriately chosen gradient step-size.

The second direction for decentralized optimization involves mainly the so called Jacobi algorithm, which serves as an alternative to gradient algorithms. The Gauss-Seidel algorithm exhibits similarities with the Jacobi one, but is not of parallelizable nature [15], unless a coloring scheme is adopted (see Section 1.2.4 in [10]). Under the Jacobi algorithmic setup, at every iteration, instead of performing a gradient step, each agent minimizes the common objective function subject to its local constraints, while keeping the decision vectors of all other agents fixed to their values at the previous iteration. A regularized version of the Jacobi algorithm has been proposed in [16, 17], and more recently in [18, 19]. Other parallelizable iterative methods are proposed in [4, 20, 21], where, however, partially separable cost functions are considered.

From a non-cooperative perspective there has recently been a notable research activity using tools from mean-field and aggregative game theory. Under a deterministic, discrete-time setting like the one considered in the present paper, [3, 5, 22] deal with the non-cooperative counterpart of our work, for the case of quadratic objective functions. In all cases, the considered algorithm is shown to converge not to a minimizer, but to an approximate Nash equilibrium of a related game, and to an exact Nash equilibrium in the limiting case where the number of agents tends to infinity. The recent work of [23] shows convergence to an exact Nash equilibrium for a finite number of agents.

I-B Contributions of this work and organization of the paper

In this paper we adopt a cooperative point of view, and consider a regularized Jacobi algorithm similar to the one in [16, 17]. Our contributions can be summarized as follows:

-

1.

We establish an equivalence between the set of minimizers of the problem under study and the set of fixed-points of the mapping induced by the considered regularized Jacobi algorithm.

-

2.

For the case where the objective function is quadratic we follow a fixed-point theoretic analysis and show convergence to an optimal solution of the centralized problem counterpart. As opposed to [16, 17], we provide an explicit calculation of the regularization coefficient that ensures convergence, and show that the convergence properties of this approach outperform the ones of scaled projected gradient algorithms. As such, our algorithm not only serves as the cooperative counterpart of [23], but also enjoys superior convergence properties.

- 3.

-

4.

We extend the results of [3, 5, 22] on electric vehicle charging control, achieving convergence to an optimal charging scheme with a finite number of vehicles. This serves also as an extension of [4], where convergence to the optimal objective value and not to the optimal charging solution was provided.

The results obtained here extend significantly our earlier work in [24], where only the case of quadratic functions was considered, omitting various proofs due to space limitations, and no formal comparison with the gradient methods was provided.

The rest of the paper is organized as follows. Section II introduces the problem under study and states the proposed algorithm. In Section III we provide the main convergence result for the case where the objective function is quadratic, and a comparison with scaled projected gradient methods. Section IV provides a convergence analysis for the general case of differentiable objective function, while the proof is deferred to the Appendix. Section V provides application of the developed scheme to the problem of optimal charging of electric vehicles and includes an extensive simulation study, while Section VI concludes the paper and outlines some directions for future research.

II Decentralized problem formulation

II-A Problem statement

We consider the following multi-agent constrained optimization problem

| (1) | ||||

| subject to | ||||

| (2) |

where each agent , , has a local decision vector and a local constraint set , and cooperates to determine a minimizer of , which couples its decision vector with those of the other agents.

We study, in particular, the case when the following assumption holds.

Assumption 1.

The objective function is given by

where with , is symmetric and positive definite () and . Moreover, the sets , , are non-empty, compact and convex.

Note that is assumed to be symmetric without loss of generality; in the opposite case it could be split in a symmetric and an antisymmetric part, with the latter giving rise to terms that simplify each other.

Remark 1 (Problem generalization).

The considered framework allows for objective functions of the form , where the are convex functions that depend on the local decision vectors only, , and may be useful to encode a utility function for each agent. In this case an epigraphic reformulation can be exploited to bring the cost back to be quadratic, while preserving constraint separability. More precisely, by introducing an additional local variable, say , in the decision vector of agent , the local constraint set can be defined as , while the objective function can be rewritten as , which is quadratic in .

Under Assumption 1, given that function is continuously differentiable and convex and the constraint set is non-empty and compact, by the Weierstrass’ theorem ([10, Proposition A8, p. ]), admits at least one optimal solution. However, does not necessarily admit a unique minimizer.

With a slight abuse of notation, for each , , let be the objective function in (1) as a function of the decision vector of agent , when the decision vectors of all other agents are fixed to . We will occasionally also write instead of . We will use these notations interchangeably, but the interpretation will always be clear from the context.

II-B Regularized Jacobi algorithm

Solving problem in a centralized fashion is not always possible since agents may not be willing to share , . Moreover, even if this was the case, solving in one shot might be computationally challenging. To overcome this and account for information sharing issues, motivated by the particular structure of with separable constraint sets, we follow a decentralized, iterative approach as described in Algorithm 1.

Initially, each agent , , starts with some value , such that is feasible and constitutes an estimate of what the minimizer of might be (step 3, Algorithm 1). At iteration , each agent receives the values of all other agents (step 5, Algorithm 1) from the central authority, and updates the estimate of its own decision vector by solving a local minimization problem (step 6, Algorithm 1). The performance criterion in this local problem is a linear combination of the objective , where the variables of all other agents apart from the -th one are fixed to their values at iteration , and a quadratic regularization term, penalizing the difference between the decision vector and the value of agent’s own variable at iteration , i.e., . The relative importance of these two terms is dictated by the regularization coefficient , which plays a key role in determining the convergence properties of Algorithm 1. Note that under Assumption 1, and due to the presence of the quadratic penalty term, the resulting problem is strictly convex with respect to , and hence admits a unique minimizer.

Remark 2 (Information exchange).

To implement Algorithm 1, at iteration , it is needed that some central authority, or common processing node, collects and broadcasts the current solution of each agent to all others, and that the agents have knowledge of the common objective function so that each of them can compute (alternatively the central authority can broadcast it to each agent , ). However, in the case where objective functions that are coupled only through the average of some variables, the central authority needs to broadcast only the average value. Each agent will then be able to compute by subtracting from the average the value of its local decision vector at iteration , i.e., . The reader is referred to the case study of Section V for an application that exhibits this structure.

III Main convergence result

In this section we analyze Algorithm 1 and show that, for an appropriate choice of the regularization coefficient , the algorithm converges to a minimizer of .

We start defining some matrices that will be used in the following: for all , let denote the -th block of , with row and column indices corresponding to , where . Denote then by a block diagonal matrix whose -th block is , and let denote the off (block) diagonal part of . Since is assumed to be symmetric, is symmetric as well and its eigenvalues are all real. Since has zero trace, at least one of its eigenvalues will be non-negative. As a result, , where denotes the maximum eigenvalue of .

We are now in a position to state one of the main results of this paper.

Theorem 1 provides an explicit bound on that ensures convergence. Such a bound is derived by a fixed-point theoretical approach. The preliminary results in Section III-A are instrumental to the proof of Theorem 1 in Section III-B, and hold for a more general class of objective functions than the quadratic ones in Assumption 1. Finally, in Section III-C we show that Algorithm 1 can be reinterpreted as a step of a scaled projected gradient algorithm, derive a bound on for convergence to some minimizer based on this reinterpretation, and show that the bound provided in Theorem 1 is tighter.

III-A Preliminary results

In this section we define appropriate mappings and establish connections between the set of minimizers of the optimization problem with separable constraint and the set of fixed-points of those mappings. Results hold for the class of objective functions specified in Assumption 2, which includes the quadratic objective functions in Assumption 1.

Assumption 2.

The function is continuously differentiable, and jointly convex with respect to all arguments. Moreover, the sets , , are non-empty, compact and convex.

III-A1 Minimizers and fixed-points definitions

By (1)-(2), the set of minimizers of is given by

| (3) |

Following the discussion below Assumption 1, is non-empty. Note that is not necessarily a singleton; this will be the case if is jointly strictly convex with respect to its arguments.

For each , , consider the mappings and , defined such that, for any ,

| (4) | ||||

| subject to | ||||

| (5) |

The mapping in (4) serves as a tie-break rule to select, in case admits multiple minimizers over , the one closer to with respect to the Euclidean norm. Note that, with a slight abuse of notation, in (4) and (5) we use equality instead of inclusion since the corresponding minimizers and , respectively, are unique. Note also that with in place of , (5) implies that the update step 6 in Algorithm 1 can be equivalently represented by .

Define also the mappings and , such that their components are given by and , respectively, for , i.e., and . The mappings and can be equivalently written as

| (6) | ||||

| subject to | ||||

| (7) |

where the terms inside the summation in (6) and (7) are decoupled. The set of fixed-points of and is, respectively, given by

| (8) | ||||

| (9) |

and can be equivalently characterized in terms of the individual components of and , as

| (10) | ||||

| (11) |

to facilitate the subsequent derivations.

III-A2 Connections between minimizers and fixed-points

We report here a fundamental optimality result, that we will often use in the sequel.

Proposition 1 ([10, Proposition 3.1]).

Under Assumption 2,

-

1.

if minimizes over , then , for all .

-

2.

if is also convex on , then the condition of the previous part is also sufficient for to minimize over , i.e., .

We start by showing that the set of minimizers of in (3) and the set of fixed-points of the mapping in (6) coincide. This is summarized in the following proposition.

Proposition 2.

Under Assumption 2, .

Proof.

1) : Fix any . For each , denote by . The fact that implies that is a minimizer of , for all . As a result, will be no greater than the values that may take over , and hence also for any values it may take if evaluated at , for any , i.e., , for all . The last statement can be equivalently written as

| (12) |

which means that satisfies the inequality in (6). Moreover is also optimal for the objective function in (6), since it results in zero cost. Hence, by (6), is a fixed-point of , which, by (10), implies that , thus concluding the first part of the proof.

2) : Fix any . By the definition of , and due to the inequality in (6) that is embedded in the definition of , we have that for all , . The last statement implies that, for all , is the minimizer of over . For all , by the first part of Proposition 1 (with in place of ) we then have that

| (13) |

where is the -th component of the gradient of , evaluated at . By (13), we then have that for all , , which, by setting , , can be written as , for all . By the second part of Proposition 1, and since is jointly convex with respect to all elements of , the last statement implies that is a minimizer of over , i.e., , thus concluding the second part of the proof. ∎

Note that the connection between minimizers, fixed-points and variational inequalities, similar to the ones that appear in the proof of Proposition 2 (e.g., see (13)), has been also investigated in [25], in the context of Nash equilibria in non-cooperative games.

We next show that the set of fixed-points of and the set of fixed-points of coincide. This is summarized in the following proposition.

Proposition 3.

Under Assumption 2, .

Proof.

1) : Fix any . By (10), this is equivalent to the fact that , for all , which, due to the definition of implies that, for all ,

| (14) |

This implies that minimizes over , hence, by the first part of Proposition 1 (with in place of ) we have that

| (15) |

where is the -th component of the gradient of , evaluated at .

Let , for all , , and notice that , where is the gradient of , evaluated at . The latter is due to the fact that the gradient of the quadratic penalty term vanishes at . By (15), we then have that, for all ,

| (16) |

Since is strictly convex with respect to its first argument, by the second part of Proposition 1 (with in place of ), (16) implies that, for all , is the unique minimizer of over , i.e.,

| (17) |

By (5), (17) is equivalent to , for all , thus concluding the first part of the proof.

2) : Fix any . By (11) this is equivalent to the fact that , for all , which, by the definition of in (5), implies that, for all ,

| (18) |

Let again . Equation (18) implies then that, for all , minimizes over , and by the first part of Proposition 1 (with in place of ) leads to

| (19) |

where is the -th component of the gradient of , evaluated at .

Notice that , where is the gradient of , evaluated at , since the gradient of with respect to vanishes at . Therefore, for all , (19) leads to

| (20) |

Since is convex with respect to its first argument, by the second part of Proposition 1, (20) implies that minimizes over . In other words, , for all . This in turn implies that, for all ,

| (21) |

The last inequality shows that satisfies the inequality in (6) in the definition of . Moreover, it minimizes the objective function in (6), since it results in zero cost. Therefore, we have , thus concluding the second part of the proof. ∎

A direct consequence of Propositions 2 and 3 is that the set of minimizers of coincides with the set of fixed-points of the mapping . This is summarized in the following corollary.

Corollary 1.

Under Assumption 2, .

III-B Proof of Theorem 1

Step 6 of Algorithm 1 can be equivalently written as , which entails that , i.e., one iteration of Algorithm 1 for the multi-agent system corresponds to a Picard-Banach iteration of the mapping (see [26] (Chapter 1.2) for a definition).

Since the set of fixed-points of is non-empty (it coincides with due to Corollary 1), we just need to prove that is firmly non-expansive (see [27] (Section 1) for a definition in general Hilbert spaces). If that is the case, then, by the results of [27, 28], we have that the Picard-Banach iteration converges to a fixed-point of , for any initial condition , . By Corollary 1 this fixed-point will also be a minimizer of .

We next show that if , then, the mapping is indeed firmly non-expansive with respect to , i.e.,

| (22) |

thus concluding the proof of Theorem 1.

Under Assumption 1, the mapping in (7) is given by

| (23) |

Notice the slight abuse of notation in (23), where the weighted identity matrix in the second and the third equality are not of the same dimension. Let denote the unconstrained minimizer of (23). We then have that

| (24) |

where denotes the projection, with respect to , of on . Note that is always positive definite for , so that its inverse exists, and the projection is well defined.

We have that

| (25) |

where the first inequality follows from the definition of a firmly non-expansive mapping and the fact that any projection mapping is firmly non-expansive (see Proposition 4.8 in [29]). The second equality is due to the definition , and the last one follows after performing the matrix multiplication.

III-C Connection with gradient algorithms

Recalling the formulation in (23) and (24), , , in step 6 of Algorithm 1 can be equivalently written as a scaled projected gradient step as follows:

| (27) |

where, the first equality follows recalling the definition of and of , and the last equality is obtained scaling by . As one can see the gradient of the original cost appears from the definition of , plays the role of the gradient step-size, and is the scaling matrix (see [10, Section 3.3.3]).

Notice that is symmetric with , as a result of having the same property. Therefore, for any , the scaling matrix satisfies the positivity condition

| (28) |

Under (28), by Proposition 3.7, p. 217 of [10] we have that the scaled projected gradient iteration (27) converges to some minimizer of for a sufficiently small step-size . This step-size is, however, not quantified in [10]; we perform this in the sequel since it provides the means to compare our methodology with a scaled projected gradient algorithm.

We can write in (27) as the unique solution to the following quadratic minimization program:

| (29) |

By optimality of , and since results in zero objective value, we have that

| (30) |

By (28) and (30) (notice that ), we thus have that

| (31) |

By the Descent Lemma (Lemma 2.1 in [10]), for the quadratic objective function of Assumption 1 we obtain that

| (32) |

where denotes the maximum eigenvalue of , which equals half of the Lipschitz constant of the gradient of . By (32) and (31) we then have that

| (33) |

If , (33) implies that . Based on this montonicity condition, and following the proof of Proposition 3.3, p. 214, of [10] for the unscaled gradient method, it can be then shown that (27) is a convergent iteration to some minimizer of .

III-C1 Comparison with the scaled projected gradient algorithm

In the scaled projected gradient algorithm it was shown that the step-size should be chosen so that , where denotes the maximum eigenvalue of . Instead, Theorem 1 requires . This latter is a less restrictive condition since . Indeed, let be the eigenvector corresponding to the eigenvalue . Then, we have

| (34) |

where the first equality follows from the fact that is the eigenvector corresponding to and the last inequality follows from . This implies that

| (35) |

where the last equality follows recalling the definition of the induced 2-norm of a symmetric square matrix.

III-C2 Dependence of the regularization coefficient on the number of agents

We next provide some examples on how and are affected by the structure of the matrix and by the number of agents . As one can expect, the more the diagonal part of is dominant with respect to the off diagonal part, the more the difference between and becomes significant: this is shown in Table I for some choices of (we assume , , for simplicity). Matrix is an matrix with all its elements being equal to .

Note that the condition on the regularization coefficient provided in Theorem 1 implicitly accounts through for how much the agents decisions are coupled in the objective function.

IV Extension to differentiable convex cost functions

In this section, we provide a convergence result for Algorithm 1 considering a more general setting as in Assumption 2 under the additional differentiability and Lipschitz continuity assumptions below.

Assumption 3.

The cost function is continuously differentiable. The gradient of is Lipschitz continuous on with Lipschitz constant , i.e., for all ,

| (36) |

The results in the following Lemma 1 and Theorem 2 are obtained relying on a different approach with respect to the one based on fixed-points and map properties exploited in the proof of Theorem 1. Their proofs are reported in the Appendix.

Lemma 1.

Theorem 2.

Note that the iterates generated by Algorithm 1 may not necessarily converge to a minimizer of , since may exhibit an oscillatory behavior; however, all its limit points achieve the optimal value.

By inspecting (38), it can be observed that as the number of agents tends to infinity, tends to infinity as well, since . This stems from the fact that Lipschitz constant in Lemma 1 depends on . This fact implies that the optimization problem at step 6 of Algorithm 1 tends to be numerically ill-conditioned as the number of agents tends to infinity; but this is also the case for the centralized problem . It should be also noted that in the other extreme situation of a single agent (), (38) implies that any is sufficient for the assertion of Theorem 2 to hold. This is in line with [10] (Proposition 4.1, p. 233), since step 6 of Algorithm 1 with , reduces to the standard proximal minimization. The fact that the higher , the higher needs to be for the statement of Theorem 2 to hold, can be intuitively justified by the fact that for any , , a higher will slow down the progress of the iterates , of agent towards its optimal value, so that all agents get “synchronized” in optimizing the common objective function with respect to their local decision vectors.

The approach adopted in Lemma 1 and Theorem 2 can also be applied when the cost function is quadratic, since Assumptions 2 and 3 are both satisfied under Assumption 1. The following Lemma applies to that case, and makes the Lipschitz constant in (1) explicit as a function of (see the Appendix for a proof).

Lemma 2.

As a consequence, Theorem 2 rewrites as follows.

Theorem 3.

Note that (39) implies that as the number of agents tends to infinity, tends to . The latter, however, does not necessarily imply that remains finite, since, in certain cases, may tend to infinity.

V Optimal charging of electric vehicles

V-A Problem setup

We consider the problem of optimizing the charging strategy for a fleet of plug-in electric vehicles (PEVs) over a finite horizon . Following [22, 5, 3], the PEV charging problem is given by the following optimization problem.

| (40) | |||

| subject to | |||

where is an electricity price coefficient at time , represents the non-PEV demand at time , is the charging rate of vehicle at time , represents a prescribed charging level to be reached by each vehicle at the end of the considered time horizon, and are bounds on the minimum and maximum value of , respectively. The objective function in (40) encodes the total electricity cost given by the demand (both PEVs and non-PEVs) multiplied by the price of electricity, which in turn depends linearly on the total demand through , thus giving rise to the quadratic function in (40). This linear dependency of price with respect to the total demand models the fact that agents/vehicles are price anticipating authorities, anticipating their consumption to have an effect on the electricity price (see [2] for further elaboration). Problem (40) can be rewritten in a more compact form as

| (41) | |||

where , and is a matrix with on its diagonal. , where denotes the Kronecker product, and is the identity matrix of appropriate dimension. Moreover, , with , and encodes the constraints of each vehicle , , in (40).

Problem (41) can be solved in a decentralized fashion by means of Algorithm 1. We compute the value of so as to satisfy (39) and, hence, to ensure convergence of the algorithm. Note that the objective function in (41) is not strictly convex as , and it exhibits a structure that allows for reduced information exchange as described in Remark 1. Indeed, at iteration of Algorithm 1, the central authority needs to collect the solution of each agent but it only has to broadcast . Each agent , , can then compute its objective as . Step 6 in Algorithm 1 for problem (41) reduces then to

V-B Simulation results

We consider first a fleet of PEVs, each of them having to reach a different level of charge , , at the end of a time horizon , corresponding to hourly steps. The bounds on are taken to be and , for all , . The non-PEV demand profile is retrieved from [3], whereas the price coefficient is , . Note that, as in [5], corresponds to normalized charging rate, which is then rescaled to be turned into reasonable power values. All optimization problems are solved using CPLEX [30].

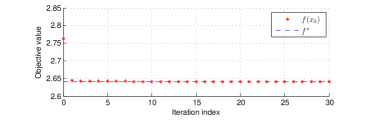

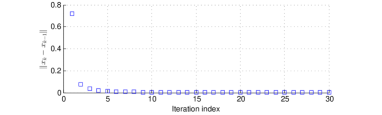

For comparison purposes, problem (41) is solved first in a centralized fashion, achieving an optimal objective value . It is then solved in a decentralized fashion by means of Algorithm 1, setting . Note that for (39) to be satisfied, we should have . In Figure 1a the objective value achieved at iteration of Algorithm 1 is depicted, whereas Figure 1b shows . After 30 iterations the difference between the decentralized and the centralized objective is , thus achieving numerical convergence.

optimal value (dashed line) of the centralized problem counterpart.

| 0 | 0.05 | 0.075 | 0.1 | 0.1478 | 0.2 | 0.4 | |

|---|---|---|---|---|---|---|---|

| - | - | 10 | 16 | 27 | 37 | 77 |

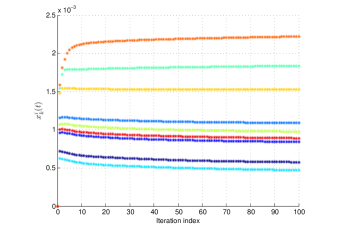

Figure 2 depicts the PEV, non-PEV, and total demand along the considered time horizon. As it can be seen, the PEV demand is optimized so that the over-night valley of the non-PEV demand is nearly filled-up. Note that due to the constraints in (41), it is not possible to further increase the PEV demand during the time interval between 1 and 4.

Considering the same setting, we perform a parametric analysis, running Algorithm 1 for different values of . In Table II the number of iterations needed to achieve a relative error between the decentralized and the centralized objective value is reported. It can be observed that, as increases, numerical convergence requires more iterations. Note that if we choose a value of that does not satisfy (39), Algorithm 1 does not always converge (see the first two rows of Table II, for and ). For some values of numerical convergence is achieved (e.g., rows 3 and 4 of Table II); however, this is not guaranteed by our analysis.

We consider now a fleet of PEVs, and modify the required charging level such that , for all , and set the bounds on to and , for all , . All the other parameters are left unchanged with respect to the previous set-up. FAfter 30 iterations the difference between the decentralized and the centralized objective is , thus achieving numerical convergence. However, with the new set of parameters, the peak of the PEV demand is designed so as to fill the over-night valley of the non-PEV demand.

It should be noted that our algorithm converges to a minimizer of (40), which is the cooperative problem counterpart of [22, 5, 3], with a finite number of agents/vehicles (see Figure 3), as opposed to the aforementioned references, where convergence to a Nash equilibrium at the limiting case of an infinite population of agents is established. Note also that the algorithm proposed in [4] ensures convergence to the optimal value with a finite number of agents, but not to the optimal solution.

VI Concluding remarks

In this paper, we investigated convergence of a decentralized, regularized Jacobi algorithm for multi-agent, convex optimization programs with a common objective and subject to separable constraints. It was shown that in the case where the objective function is quadratic the algorithm converges to some minimizer of the centralized problem via fixed point arguments. In the more general case of a convex but not necessarily quadratic cost, we were able to show that all limit points of the proposed algorithm are minimizers of the centralized problem. The efficacy of the proposed algorithm was illustrated by applying it to the problem of optimal charging of electric vehicles, achieving convergence with a finite number of vehicles. Current work concentrates on investigating the rate of convergence for general convex functions, exploiting the recent fixed-point theoretic results of [31].

Appendix A Algorithm analysis for differentiable convex objective functions

We report some identities which hold directly from the definition of and its gradient, that will be exploited in the following.

| (42) | ||||

| (43) | ||||

| (44) |

where by the notation (similarly for ), we imply that the gradient of is evaluated at , where for each , , the appropriate component of is employed. Similar is the interpretation of the various gradient terms appearing in the subsequent derivations.

Proof of Lemma 1

Fix any , with , , and . We then have that

| (45) |

where the first equality is obtained by exchanging the gradient and the summation order, since the gradient is a linear operator, the second equality is due to the fact that, for each , , all components of (similarly for ) will be zero apart from the -th one that will be , and the last equality is achieved by performing the summation and evaluating the quantity in the parentheses at . We then have that

| (46) |

where the first expression follows from (45), the first inequality is due to fact that, as a consequence of Assumption 3, for each , the -th component of the gradient is Lipschitz continuous with a Lipschitz constant upper-bounded by , i.e., , for all . The last inequality follows by noticing that . Combining (45) and the inequality above leads then to (1), and hence concludes the proof.

Proof of Theorem 2

From step 6 of Algorithm 1 and by the definition of in (7), we have that . Therefore, is optimal for the objective function that appears in the right-hand side of (7), hence we have that, for all ,

| (47) |

Since , setting and rearranging some terms, we have that

| (48) |

By convexity of due to Assumption 3, we have that

| (49) |

Combining (48) and (A), and after rearranging some terms, we obtain that

| (50) |

which in view of (42) and (44) can be rewritten as

| (51) |

Since and due to (7), by the first part of Proposition 1, with the objective function at the right-hand side of (7) in place of , we obtain that

| (52) |

Note that is the gradient of the objective function at the right-hand side of (7), evaluated at . Adding the term in both sides of (52), we obtain that

By the Cauchy-Schwarz inequality, and due to Lemma 1, which holds under Assumption 3, we have that

| (53) |

which in view of (43) can be rewritten as

| (54) |

By (A) and (54), we then have that

| (55) |

If we choose the regularization coefficient according to (38), then the term in (A) is multiplied by a negative constant, and hence (A) shows that is a non-increasing sequence, i.e., for all , .

Moreover, by (A) and for a given , we have that

| (56) |

Notice that due to the fact that is non-increasing. If is chosen then according to (38), and letting , the last statement implies that , thus , and hence

| (57) |

However, by (A), and under the choice of in (38), we have that is a monotonically decreasing sequence, i.e., for all , but for the case where for some . The latter case implies that there exists such that . Since , the last statement implies that is a fixed-point of , and, due to Corollary 1, will be a minimizer of .

Consider now the former case, where is a monotonically decreasing sequence. Since for all , and is compact due to Assumption 3, is bounded below. Therefore, the sequence is convergent. Consider any convergent subsequence of and denote by its limit point. By (57), we then have that converges to as well. The latter, together with the fact that is continuous implies that , i.e., is a fixed-point of . Note that since is single-valued as an effect of being strictly convex due to the presence of the regularization term, continuity follows from 5.22 in [32] (p. 162) if the objective function in (7) is continuous differentiable, the set is compact, and the minimum in (7) as a function of is continuous. Continuous differentiability and compactness emanate from Assumption 3, whereas it is shown in Exercise 1.19 in [32] (p. 18) that, under the stated assumptions and since the constraint set does not depend on , the minimum is a continuous function of . Hence, is continuous and as shown above belongs to its fixed-points. Due to the equivalence between the fixed-points of and the minimizers of shown in Corollary 1, the limit point of is also a minimizer of , hence , thus concluding the proof.

It should be noted that the last part of the proof is motivated by the arguments in p. 214, Chapter 3 of [10].

Proof of Lemma 2

Under Assumption 1, and by the definition of , we have that for any , , where in the last step we used the fact that . By the last statement we then have that Following an analogous derivation with in place of , we have that . Therefore,

| (58) |

thus concluding the proof.

References

- [1] F. Bagagiolo, D. Bauso, Mean-field games and dynamic demand management in power grids, Dynamic Games and Applications 4 (2) (2014) 155–176.

- [2] B. Gharesifard, T. Basar, A. D. Dom nguez-Garc a, Price-based coordinated aggregation of networked distributed energy resources, IEEE Transactions on Automatic Control 61 (10) (2016) 2936–2946. doi:10.1109/TAC.2015.2504964.

- [3] Z. Ma, D. Callaway, I. Hiskens, Decentralized charging control of large populations of plug-in electric vehicles, IEEE Transactions on Control Systems Technology 21 (1) (2013) 67–78.

- [4] L. Gan, U. Topcu, S. Low, Optimal Decentralized Protocol for Electric Vehicle Charging, IEEE Transactions on Power Systems 28 (2) (2013) 940 – 951.

- [5] F. Parise, M. Colombino, S. Grammatico, J. Lygeros, Mean field constrained charging policy for large populations of plug-in electric vehicles, 2014, pp. 5101–5106.

- [6] M. Pavone, E. Frazzoli, F. Bullo, Decentralized Algorithms for Stochastic and Dynamic Vehicle Routing with General Demand Distribution, IEEE Conference on Decision and Control (2007) 4869 – 4874.

- [7] A. Nedic, A. Ozdaglar, P. Parrilo, Constrained consensus and optimization in multi-agent networks, IEEE Transactions on Automatic Control 55 (4) (2010) 922–938.

- [8] M. Zhu, S. Martinez, On distributed convex optimization under inequality and equality constraints, IEEE Transactions on Automatic Control 57 (1) (2012) 151–164.

- [9] J. Koshal, A. Nedich, U. Shanbhag, Multiuser optimization: distributed algorithms and error analysis, SIAM Journal on Optimization 21 (3) (2011) 1046–1081.

- [10] D. Bertsekas, J. Tsitsiklis, Parallel and distributed computation: Numerical methods, Athena Scientific (republished in 1997), 1989.

- [11] N. Parikh, S. Boyd, Proximal algorithms, Foundations and Trends in Optimization 1 (3) (2013) 123 – 231.

- [12] A. Goldstein, Convex programming in Hilbert space, Bulletin of American Mathematical Society 70 (1964) 709–710.

- [13] E. Levitin, B. Poljak, Costrained minimization methods, USSR Computational Mathematics and Physics (English transaltion) 1 (1965) 1–50.

- [14] D. Bertsekas, On the Goldstein-Levitin-Polyak gradient projection method, IEEE Transactions on Automatic Control 2 (1976) 174–184.

- [15] H. Attouch, J. Bolte, B. Svaiter, Convergence of descent methods for semi-algebraic and tame problems: proximal algorithms, forward? backward splitting, and regularized Gauss? Seidel methods, Mathematical Programming 127 (1) (2013) 91? 129.

- [16] G. Cohen, Optimization by decomposition and coordination: A unified approach, IEEE Transactions on automatic control 23 (2) (1978) 222–232.

- [17] G. Cohen, Auxiliary problem principle and decomposition of optimization problems, Journal of optimization Theory and Applications 32 (3) (1980) 277–305.

- [18] M. Patriksson, Decomposition methods for differentiable optimization problems over cartesian product sets, Computational optimization and applications 9 (1) (1998) 5–42.

- [19] D. Zhu, P. Marcotte, Coupling the auxiliary problem principle with descent methods of pseudoconvex programming, European journal of operational research 83 (3) (1995) 670–685.

- [20] P. Richtárik, M. Takáč, Parallel coordinate descent methods for big data optimization, Mathematical Programming 156 (1-2) (2016) 433–484.

- [21] I. Necoara, D. Clipici, Parallel random coordinate descent method for composite minimization: Convergence analysis and error bounds, SIAM Journal on Optimization 26 (1) (2016) 197–226.

- [22] S. Grammatico, F. Parise, M. Colombino, J. Lygeros, Decentralized convergence to nash equilibria in constrained deterministic mean field control, IEEE Transactions on Automatic Control 61 (11) (2016) 3315–3329. doi:10.1109/TAC.2015.2513368.

- [23] D. Paccagnan, M. Kamgarpour, J. Lygeros, On Aggregative and Mean Field Games with Applications to Electricity Markets, European Control Conference,.

- [24] L. Deori, K. Margellos, M. Prandini, On decentralized convex optimization in a multi-agent setting with separable constraints and its application to optimal charging of electric vehicles, in: 2016 IEEE 55th Conference on Decision and Control (CDC), 2016, pp. 6044–6049. doi:10.1109/CDC.2016.7799197.

- [25] F. Facchinei, A. Fischer, V. Piccialli, On generalized Nash games and variational inequalities, Operations Research Letters 35 (2) (2007) 159–164.

- [26] V. Berinde, Iterative Approximation of Fixed Points, Springer-Verlag Berlin Heidelberg, 2007.

- [27] P. Combettes, T. Pennanen, Generalized Mann iterates for constructing fixed points in Hilbert spaces, Journal of Mathematical Analysis and Applications 275 (2) (2002) 521? 536.

- [28] Z. Opial, Weak convergence of the sequence of successive approximations for nonexpansive mappings, Bulletin of American Mathematical Society 73 (4) (1967) 591–597.

- [29] H. Bauschke, P. Combettes, Convex analysis and monotone operator theory in Hilbert spaces, Springer, 2010.

-

[30]

IBM

ILOG CPLEX Optimizer (2015).

URL http://www-01.ibm.com/software/commerce/optimization/cplex-optimizer/index.html - [31] G. Banjac, K. Margellos, P. J. Goulart, On the convergence of a regularized jacobi algorithm for convex optimization, IEEE Transactions on Automatic Control, under review.

- [32] T. Rockafellar, R. Wets, Variational Analysis, Springer-Verlag Berlin Heidelberg, 1998.