An Analysis of

Attacks on Blockchain Consensus (DRAFT)

Abstract

We present and validate a novel mathematical model of the blockchain mining process and use it to conduct an economic evaluation of the double-spend attack, which is fundamental to all blockchain systems. Our analysis focuses on the value of transactions that can be secured under a conventional double-spend attack, both with and without a concurrent eclipse attack. We account for an attacker capable of increasing profits by targeting multiple merchants simultaneously. Our model quantifies the importance of several factors that determine the attack’s success, including confirmation depth, attacker mining power, and a confirmation deadline set by the merchant. In general, the security of a transaction against a double-spend attack increases roughly logarithmically with the depth of the block, made easier by the increasing potential profits, but more difficult by the increasing proof of work required. We find that a merchant requiring a single confirmation is protected against attackers that possess as much as 10% of the mining power, but only provided that the total value of goods at risk for double-spend is less than 100 BTC. A merchant that requires a much longer 55 confirmations (9 hours) will prevent an attacker from breaking even unless he possesses more than of the current mining power, or the value of goods at risk exceeds 1M BTC.

1 Introduction

00footnotetext: This work’s copyright is owned by the authors. A non-exclusive license to distribute the pdf has been given to arxiv.org. Last revised 2016-11-20.Despite the widespread adoption of blockchain-based digital currencies like Bitcoin [16], there exists little guidance on the actual value of goods or services that can be secured against double-spend attacks using blockchain transactions. The need for understanding the risk has always been of paramount importance to merchants; and the need is now shared by an increasing number of services that leverage blockchain transactions for settlement. For example, sidechains [1] and the Lightning Network [18] may be deployed shortly, and the security of each depends heavily on the underlying security of the Bitcoin transactions from which they are bootstrapped. Yet, all earlier studies of the economics of double-spend attacks fall short because of the simplicity of their model and resulting inability to capture the full complexity of the problem. In the present work, we derive a novel, continuous-time model for the double-spend attack, and use it to evaluate the economics of the conventional attack; we also use it to evaluate the attack in the presence of a concurrent eclipse attack [13], in which adversaries occlude a targeted peer’s view of the majority’s blockchain.

Double-spend attacks cannot be prevented in blockchain currencies because they are subject to the FLP impossibility result[10], which says, informally, that consensus cannot be reached in distributed systems that do not set a deadline for when messages (i.e., new blocks) can be received. The primary mitigating defense against double-spends is for the merchant to wait for a transaction to receive confirmations (i.e., blocks are added after the block in which it originally appeared) before releasing goods to a customer. Nakamoto derived the probability of success for that defense, but the result is limited because it considers neither the cost of the attack, nor the revenue that the attacker stands to gain. Moreover, although it has been shown that the eclipse attack makes double-spending easier [13], no prior work has yet quantified the security of a merchant’s transactions in such a case where her view of the blockchain is obstructed.

Contributions. We contribute a novel economic evaluation of double-spend attacks in Bitcoin that could easily be extended to similar blockchain currencies such as Litecoin[14] or Zerocash [22]. We derive and validate equations for the value of transactions that can be secured against a double-spending adversary, who controls any portion of the mining power less than a majority. We also evaluate the double-spend attack when conducted contemporaneously with the eclipse attack.

Our results quantify Bitcoin’s security as a currency. We show that the correct attacker model considers not just the attacker’s mining power and transaction confirmation depth , but also the attacker’s potential reward, or goods at risk, which can be conservatively estimated by a merchant as the summed value of coin in the confirmation blocks that is exchanged between individuals (turnover)[15, 19]. We find that blockchain security against double-spend attacks increases roughly logarithmically with block depth, made easier by increasing goods at risk, but more difficult by the increasing proof of work required. Our model also quantifies the synergistic value of a concurrent eclipse attack.

For example, when the summed turnover for a transaction’s first confirmation block is as high as 100 BTC, we determine that a single confirmation is protected against attackers that can increase the current mining power by no more than . Waiting for significantly more confirmations increases a transaction’s security considerably. With 55 confirmations and aggregate turnover of up to 1M BTC, a transaction can be protected from a double-spend attack as long as the attacker possesses less than of the current mining power. We also demonstrate quantifiably that if merchants impose a conservative confirmation deadline, then a concurrent eclipse attack can only make double-spends more profitable if the attacker possesses less than 35% of the mining power or if the merchant requires fewer than 10 confirmations.

2 Background and Related Work

Using a blockchain as a method for distributed consensus was first proposed by Nakamoto as part of his or her development of the Bitcoin digital currency [16]. Blockchains allow for an open group of peers to reach consensus, while mitigating Sybil attacks[7] and the limitations imposed by the FLP impossibility result [10] through a mining process. We refer the uninitiated reader to Appendix 0.A for a detailed overview of blockchain consensus and Bitcoin. Additionally, several articles are available that offer summaries of broader Bitcoin research issues[25, 4, 6]. Below, we summarize two particularly relevant attacks, and then summarize why our contributions are distinct from related work.

2.1 Relevant Attacks

Double spending. A fundamental attack against Bitcoin is the double-spend attack [16], which works as follows. An attacker creates a transaction that moves funds to a merchant’s address. After the transaction appears in the newest block on the main branch, the attacker takes possession of the purchased goods. Using his mining power, the attacker then immediately releases two blocks, with a transaction in the first that moves the funds to a second attacker-owned address. Now the attacker has the goods and his coin back. To defend against the attack, a merchant can refuse to release goods to a Bitcoin-paying customer until blocks have been added to the blockchain including the first block containing a transaction moving coin to the merchant’s address. Nakamoto calculated the probability of the attack succeeding assuming that the miner controlled a given fraction of the mining power [16]; for a given fraction, the probability of success decreases exponentially as increases.

In general, a merchant may wait blocks before releasing goods, which can thwart an attacker. But choosing the minimum value of that secures a transaction is an unresolved issue. The core Bitcoin client shows that a transaction is unconfirmed until it is 6 blocks deep in the blockchain[3], and the advice from researchers to policymakers can be vague; e.g., “for very large transactions, coin owners might want to wait for a larger number of block confirmations” [5].

Eclipse attacks. Heilman et al. showed that Bitcoin’s p2p network peer discovery mechanism is vulnerable to eclipse attacks [13], which occlude a victim peer’s view of the blockchain. For example, if an adversary controls a botnet, he can fill a peer’s table of possible neighbors, resulting in a very high chance the victim will connect only to the attacker. Alternatively, the eclipse can involve controlling a victim’s local connection to the Internet.

Heilman et al. also showed that eclipse attacks can be used as a tool to increase the effectiveness of the double-spend attack on a merchant. First, the attacker eclipses the merchant’s view of the blockchain. Then, he sends the merchant a seemingly honest transaction , which contains the payment for a good. Third, the attacker sends to the miners a faulty transaction that moves the funds elsewhere. Next, he creates and sends a series of blocks to the victim merchant such that is part of the first block. Finally, he continues the eclipse until the real blockchain has progressed by at least blocks. At that point, he has both the goods and the Bitcoin that the merchant intended to keep.

2.2 Related Work

Nakamoto derived the double-spend attack’s success probability in the original Bitcoin paper [16]. The main limitation of this approach is that it fails to include attack cost, which would place the severity of an attack in a real world context. Moreover, the model itself is also overly simplified in that it models the creation of an entire sequence of blocks as a single Poisson process. Accordingly, we cannot rely on the accuracy of the model for large numbers of consecutive blocks, which is necessary for determining the security of high-value transactions.

In their paper introducing the GHOST protocol [23], Sompolinsky et al. extended Nakamoto’s model by incorporating network delays and by allowing the expected block creation time to deviate from the 10-minute average used today. With this model, they showed that double-spend attacks become more effective as either the block size or block creation rate increase (when GHOST is not used). With a trivial change, our work could also vary the expected block creation time. A less trivial (but quite interesting) change would allow us to also model network delays.

Sapirshtein et al. [21] first observed that some double-spend attacks can be carried out essentially cost-free in the presence of a concurrent selfish mining [9] attack. More recent work extends the scope of double-spends that can benefit from selfish mining to cases where the attacker is capable of pre-mining blocks on a secret branch at little or no opportunity cost [24] and possibly also under a concurrent eclipse attack [11]. The papers identify the optimal mining strategy for an attacker and quantify the advantage that he can expect to have over the merchant in terms of pre-mined blocks. This analysis is complementary to ours; it is possible to relatively easily incorporate the pre-mining advantage into our model by simply changing the attacker’s block target from to . We note that pre-mining in the context of the eclipse attack may not be feasible since an eclipse cannot generally be carried out for an indefinite period of time. Nevertheless, we intend to update both of our double-spend analyses to account for cost-free pre-mining in future work.

The objective of Rosenfeld [20] is most similar to ours and his analysis is a great improvement over the 6-block rule. However, his model cannot be applied to the concurrent eclipse attack scenario and he makes several simplifying assumptions that render the results for the conventional double-spend attack less accurate than ours, particularly as the number of required confirmations, , grows (we compare quantitatively in Fig. 3). Additionally, his approach — as well as all of those cited above — models only the order of block creation and not block mining time explicitly. As a result, it is difficult to extend his results to model cost in circumstances where the attacker is given a specific deadline (as we have done in our eclipse attack analysis) or where an attacker drops out because the honest miners have already won. We develop a richer, continuous-time model that explicitly accounts for attacker cost as a function of mining duration.

Heilman et al. offered a detailed analysis of the mechanics of an eclipse attack, as well as several protocol-level defenses to the attack. But they attempted no analysis of an attacker’s economic incentives. As a result, it remains unclear what minimum number of confirmations, , are sufficient to secure a given value of purchased goods. In this paper, we derive a model for the profit received by an adversary who launches an eclipse attack, and use it to determine the attacker’s break-even point for various values of .

3 Analysis of Double-spend and Eclipse Attacks

In this section, we compute the security of a transaction against a double-spend attack, both with and without a concurrent eclipse attack, in cases where the transacted coin is used as payment for goods or services, which we call goods at risk. Specifically, we are able to determine the fraction of mining power required by an attacker to profitably double-spend a transaction given the value of goods at risk and transaction confirmation blocks required by the target (merchant, service, etc.). As we explain below, is conservatively estimated as not just the Bitcoin value of goods sold by a single merchant, but as the sum amount of coins transferred between entities (turnover) by all transactions in the confirmation blocks. Our guiding principle is that a resource is secure from an attack only if it is worth less than the attack’s cost. We find that because of the well-behaved statistical properties of mining times and transparency of transaction values, Bitcoin is particularly amenable to such an analysis.

Attack cases. In this section, we analyze two double-spend attack strategies. Case 1 assumes that the attacker is capable of eclipsing the merchant while conducting a double-spend attack. Case 2 assumes that the attacker elects not to employ an eclipse attack (or equivalently, fails in an attempt to do so). Assuming that the merchant follows our mitigation guidelines, we provide bounds on the expected break-even point for the attacker in both cases. We find that there are two distinct attack regimes where one case dominates the other based on the attacker’s share of the mining power . When and remains relatively low, Case 1 affords the attacker a lower break-even point. The opposite is true for and large , where Case 2 dominates.

Attack target. Throughout most of this section we proceed under the assumption that the attacker targets a single merchant, which is not strictly true. First, the target need not be an individual at all; the attacker could instead target blockchain-based services. Second, he could exploit multiple targets simultaneously. We discus the ramifications of the former in Section 4 and the latter presently. Simultaneous attacks increase the attacker’s potential profit by allowing for multiple double-spends to be placed in a single block. Moreover, even if a merchant requires confirmations, the attacker might be lucky to find other merchants requiring only one, which means that the attacker could potentially profit from all blocks. The potential profit in a block can be bounded by the sum of all Bitcoin transferred, or turned over, between distinct entities. We call the aggregate turnover value for blocks the -maximal goods because it represents the maximum Bitcoin value of goods that could be exploited by the attacker in the confirmation blocks. Several past works have evaluated metrics for estimating that value[19, 15]. Thus, we can model the simultaneous attack scenario by letting the goods at risk, , be equal to the -maximal goods.

Mitigation measures. We assume that the merchant will take certain precautions. First, because the attacker is capable of profiting from the -maximal goods, the merchant will set adaptively based on the turnover of each block as it is added to the blockchain. Specifically, she will only release goods after confirmations if the expected cost to an attacker exceeds the -maximal goods. Second, when the merchant is concerned about a simultaneous eclipse attack, she will impose a deadline for the receipt of all confirmations. It is always possible to double-spend against an eclipsed merchant — only the attack duration varies based on the attacker’s fraction of mining power — thus serves to increase the attacker’s cost by increasing his loss rate. Because is set dynamically, would most naturally be defined as a linear function of .

3.1 Attacker model

We make the following simplifying assumptions about the attack environment as well as the attacker’s capabilities and behaviors.

-

•

The attacker’s mining power constitutes a fraction of the total mining power. When , the attacker holds a majority of the mining power, in which case Bitcoin cannot secure any transaction.

-

•

The network is correctly calibrated so that a block is produced roughly once every 10 minutes given the current mining power, which is generally true in the real system. Bitcoin adjusts its difficulty once every 2,016 blocks (about every two weeks), and we assume these attacks have no affect on the difficulty while they are run.

-

•

The eclipse attack succeeds without fail. An eclipse attack is likely to incur some cost, but we do not include it because that cost is hard to estimate. For example, in the most general scenario, a botnet might be required [13]. On the other hand, if a merchant is physically accessible and has only a single, unsecured wireless link to the Internet, eclipse attacks are much simpler and much less costly. We also assume the attacker does not launch a denial-of-service attack on honest miners.

Attacker strategy Case 1: The attacker launches an eclipse attack against one or more merchants. He diverts his mining power, , from the main branch to mining an alternate fraudulent branch that contains in the earliest block a transaction that moves coins to the merchant; the blocks are sent to the merchant as they are mined. Once the attacker reaches blocks on the fraudulent branch, the merchant releases the goods to the attacker. The attacker ceases to mine on the fraudulent branch, and waits until the main branch grows longer than the fraudulent branch. He then ceases to eclipse the merchant, allowing her to realize that the actual longest branch does not contain the transaction that transferred coin to her.

In principle, the attacker has an unlimited amount of time to produce the blocks he uses to unlock the goods from the merchant. He is limited only by the amount of time he is able to eclipse the merchant and the time his is willing to divert his mining power away from the main branch. However, the merchant will likely suspect that she is being eclipsed if the actual time it takes for her to receive blocks is drastically different than the expected time (roughly 10 minutes per block). Therefore, we propose that the merchant refuse to hand over the goods if the blocks are not received by her deadline , a parameter that we described in our discussion of mitigation measures. Given this change in policy, the attacker will naturally adjust to cease mining on the fraudulent branch once he either mines blocks or the deadline has passed. For this case, we do not consider the possibility that the attacker attempts to replace the main branch with his false branch, thus we assume that the coinbase rewards earned on the fraudulent branch are useless.

Attacker strategy Case 2: No eclipse attack is leveraged, but the attacker again possesses fraction of the total mining power. This time, after releasing the transaction that pays coin to the merchant, he races to mine blocks on a secret fraudulent branch that does not contain the transaction in any of its blocks. Meanwhile, the rest of the miners have picked up the payment transaction and added it to the main branch on which they mine. The merchant will release the goods once the main branch reaches length . The attacker does not release any of his blocks until the fraudulent branch has reached length , at which point he releases all block simultaneously. If the fraudulent branch is longer than the main branch, then the attacker will have successfully double-spent the coins that he originally transferred to the merchant.

A persistent attacker could conceivably continue to mine indefinitely, even after the main branch far surpasses the fraudulent branch. There will remain, in any case, a non-zero probability of success. However, one of Nakamoto’s fundamental results is that there will be an exponentially diminishing probability of success with every block that the attacker falls behind [16]. Moreover, the cumulative cost will eventually become prohibitive to any rational attacker. Therefore, we assume the attacker will eventually quit if he remains behind for a sufficiently long period of time. Determining the optimal drop out point is left for future work; here we arbitrarily assume that the attacker will drop out if the main branch mines blocks before he can. This choice has the desirable property (for the attacker) that the expected cost for any outcome will not exceed the cost he was willing to incur for a successful attempt.

3.2 Case 1 Analysis: Eclipse-Based Double-Spend

We determine Bitcoin’s security with respect to an eclipse-based double-spend attack by quantifying a potential attacker’s economic break-even point. Break-even occurs when revenue less cost is zero:

| (1) |

We assume an attacker has fraction of total mining power, and the merchant will not release goods until a paying transaction is -blocks deep in the main chain. If the th block has not been announced by minutes, the sale is nullified.

Let be a random variable representing the time it takes for the attacker to mine the th block using mining power , and let

| (2) |

Here, represents the time it takes the attacker to reach blocks using mining power . Define to be the cost of an attack with duration minutes and deadline that uses mining power . To calculate cost, we assume that the miner will stop mining once he mines the blocks, but will continue to mine until the deadline if he is unsuccessful. Cost can be measured in terms of the opportunity cost for diverting the mining power from performing honest mining, that is, the attacker could have earned the block reward of from the main branch. Blocks are mined, we expect, every 10 minutes. Therefore

| (5) |

Mining is an example of a Poisson process because, under constant mining power, blocks are mined continuously and independently at a constant average rate. Therefore with . It is well known that the exponential distribution is a special case of the gamma distribution with shape parameter . Furthermore, the sum of gamma distributions with shape and the same rate is again gamma with rate and shape . Thus . Let be the density function for the distribution , and let be the CDF. It follows that

| (6) | |||||

Consider now the attacker’s revenue . If he succeeds in the attack, then he will earn revenue and will earn nothing otherwise. Formally,

| (7) |

The probability of his success is

| (8) |

Hence the expected revenue is given by

| (9) |

Using the fact that expected break-even occurs when we have our result for Case 1:

| (10) | |||||

3.3 Case 2 Analysis: Double-Spend Without The Eclipse Attack

In this case, we assume that an eclipse attack is not employed by the attacker. By comparing results to Case 1, we can determine which is the more effective attacker strategy. Recall that the attacker builds a fraudulent branch holding the double-spend transaction, and honest miners build the main branch holding the payment transaction. The attack succeeds if the fraudulent branch becomes the main branch. No deadline is enforced by the merchant. She does, however, enforce an embargo on goods until the payment transaction is -blocks deep.

Let be a random variable denoting the time it takes the attacker to mine the th block if he controls fraction of the total mining power. Similarly, define to be the time it takes the honest miners to mine block given that they control fraction of the mining power. Finally, define

| (11) |

and

| (12) |

to be the time it takes for the attacker and other miners, respectively, to mine blocks. For the attack to be a success, it must be the case that . We assume that the attacker will stop mining when he reaches blocks on the fraudulent branch or when the honest miners reach blocks on the main branch, whichever happens first.

Analogously to Section 3.2, we define as the cost to the attacker when he possesses mining power and the attacker and honest miners each mine for and minutes respectively:

| (15) |

Just like in Section 3.2, both and have gamma distributions, this time with rate parameters and , respectively. Specifically, and . Define and as in Section 3.2. It follows that

| (16) | |||||

To determine the attacker’s expected break-even point, we must also calculate his expected revenue. For any given , the attacker’s revenue when it took him minutes to mine blocks on the fraudulent branch while it took the other miners minutes to mine blocks on the main branch is given by

| (17) |

Revenue differs from that collected in Case 1 because the successful attacker will earn the coinbase reward for each block he mines. The probability of attack success is equal to

| (18) | |||||

Therefore, the expected revenue can be calculated as

| (19) | |||||

The expected break-even point is value of for which revenue minus cost is zero.

| (20) | ||||

| Substituting for revenue, | ||||

| (21) | ||||

| and rearranging, we have our result for Case 2 as follows: | ||||

| (22) | ||||

Note that Eq. 22 is fully expressed by substituting Eqs. 16 and 18.

4 Discussion

In this section, we use the derivations from the previous section to quantitatively compare attacker strategies and discuss implications for blockchain systems and their users. In addition to the assumptions outlined in Section 3, we fix the deadline at for Case 2, which implies that the merchant will release the goods only if the payment transaction receives confirmations within minutes. We discuss the practical ramifications of this choice later in this section.

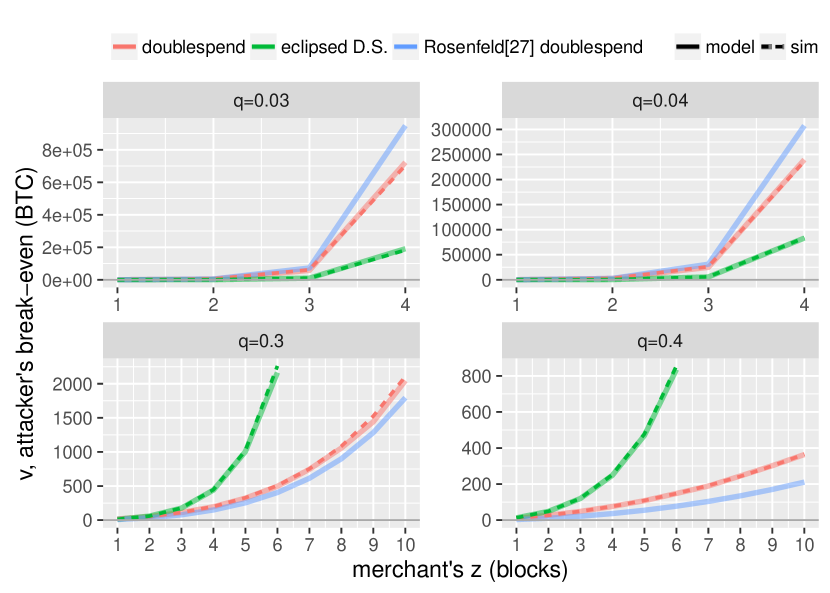

Accuracy of model. Fig. 1 compares Eqs. 10 and 22, the break-even value for a rational attacker performing a double-spend attack with and without eclipsing the merchant, respectively. In general, the break-even point increases with , and for lower values of the break-even point grows particularly rapidly. Thus we limit for small in order to more easily discern the differences between curves on the same axes. An alternative visualization of the equations appears in the appendix, Fig. 5. Fig. 1 also includes the results of an independent Monte Carlo (MC) simulation of both attacks, executed thousands of times for each point and is in very close agreement with our model.

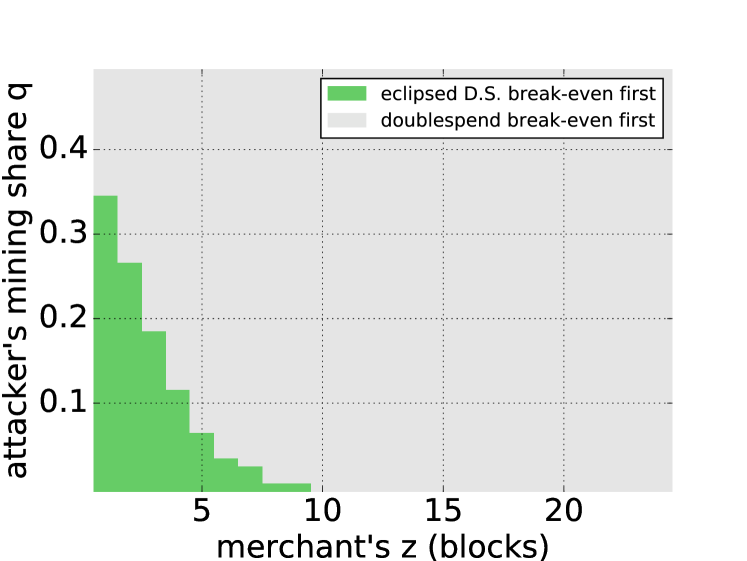

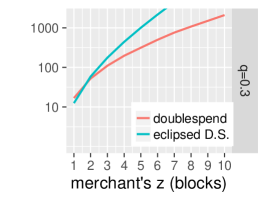

Better to eclipse or not? Whether using an eclipse attack is an advantage to the attacker depends on both and . Fig. 2 shows that the concurrent eclipse attack of Case 1 affords the attacker with a lower break-even point (which is advantageous) than Case 2 for relatively low values of ; the advantage holds for fewer values of as increases. Indeed, once or , Case 2 always offers a lower break-even point than Case 1. The precise regime where one case dominates the other depends on the choice of deadline in Case 1. A longer deadline will decrease the cost for the attacker, which will lower his break-even point, and tend to enlarge the green region in Fig. 2. Nevertheless, we expect that Case 2 will always dominate Case 1 for large because the fraudulent chain replaces the main chain in the latter case, earning the attacker the cumulative block reward.

Comparison to Rosenfeld[20]. Rosenfeld offers a model for that is directly comparable to what we call Case 2 (double-spend without the eclipse attack), but his model is not capable of addressing Case 1. In terms of our notation, his model yields the bound , where is a discrete model111Specifically, Eq. 1 in [20]. of the attacker’s probability of success given and . Fig. 1 plots his model next to ours as well as our independent Monte Carlo simulation results. His model provides a reasonable fit for , but is not accurate otherwise; the error in Rosenfeld’s model tends to increase with . For example, when and , his model over-shoots the MC results by almost 35%, and when and his model underestimates the true break-even point by over 40%.

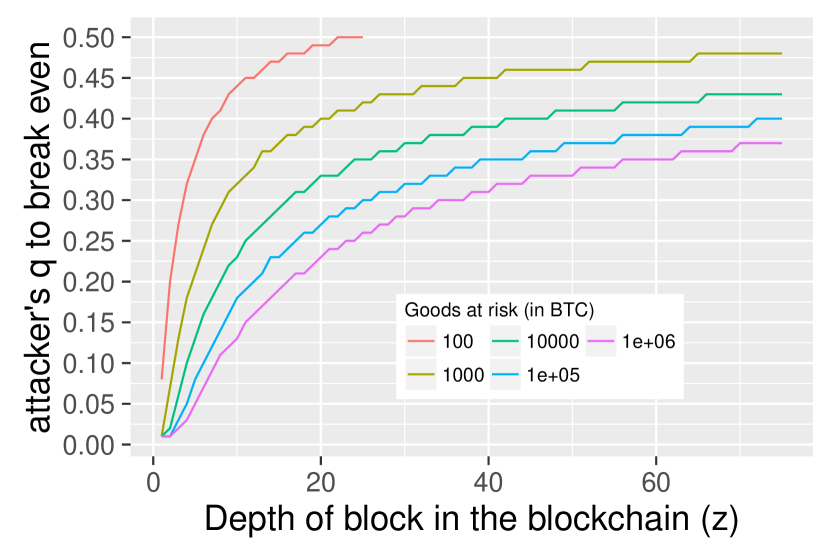

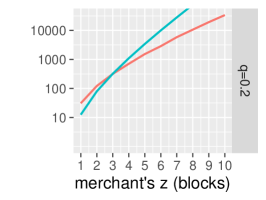

Revenue required to break even. In general, double-spending attacks are more efficient with higher mining power and goods at risk . Higher means less risk of losing, and higher means greater potential profit. Each curve in Fig. 3 represents a single value for goods at risk and shows how the mining power necessary for the attacker to break even varies with 222In Fig. 3, Case 1 values are easily generated directly from Eq. 10; the equation contains no integrals and most scientific software packages can deliver values from the gamma distribution. In contrast, Case 2 involves a somewhat difficult integration (with no analytical solution), and numerical integration packages fail for portions of our parameter space. We instead used Monte Carlo integration — a distinct technique from the Monte Carlo simulation discussed above — to generate points from Eq. 22. For each pair of values and , the minimum value from the most effective double-spend attack strategy is reported in the plot (the case that breaks even for lowest value ).

From the plot we can see that, for low values of , even attackers with limited mining power can break even for low values of goods at risk. On the other hand, as the merchant increases , the required mining power increases rapidly for low . For example, an attack with 1M BTC goods at risk (purple curve) can be successful with relatively low mining power, , as long as the merchant keeps less than 25. But a lower value , such as 1K BTC (yellow curve), would require the attacker to possess mining power for the same value .

Determining value of goods at risk. The attacker’s potential profit has a strong impact on his break-even point, and that profit is directly related to the goods at risk . Thus, it is imperative that the merchant understand the scope of the attack. If she is confident that a potential attacker will target her alone, then the goods at risk can safely be assumed to be equal to the value of the goods she is personally trading for coin. On the other hand, if she would like to be conservative, then the merchant must assume that the attacker is capable of capturing the aggregate turnover in all confirmation blocks, which is the -maximal goods at risk.

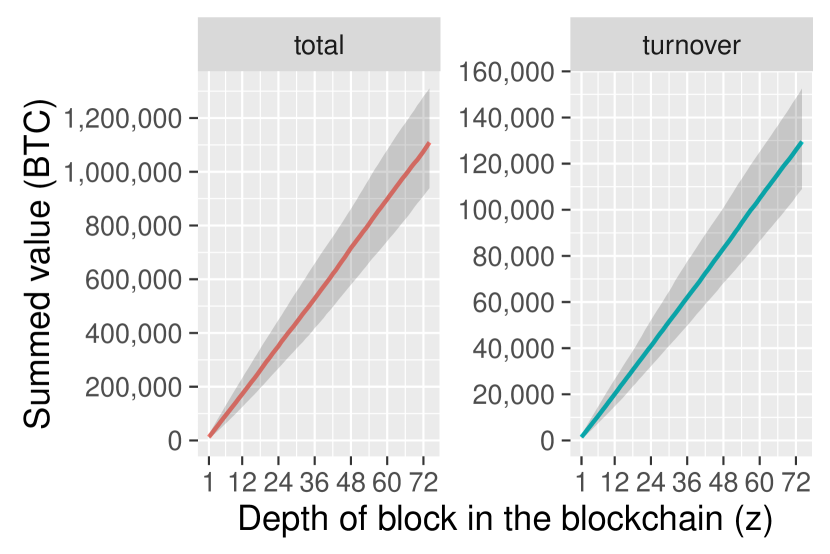

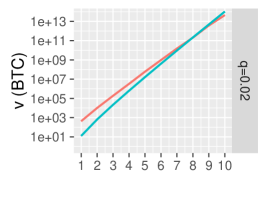

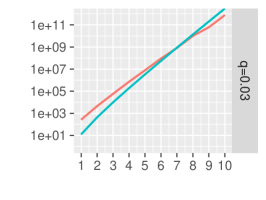

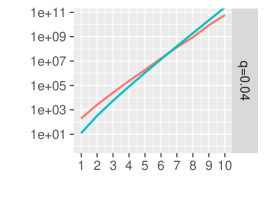

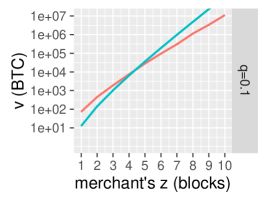

Fig. 4 shows the actual median aggregate total and turnover values for consecutively mined blocks during the month of July 2016 (data source: blockchain.info). Each point should be thought of as the typical sum of all outputs for the transactions or typical turnover value for the given number of consecutive blocks. The plot shows that the merchant can significantly bound the attacker’s potential revenue by measuring turnover as opposed to using total block output value. Aggregate turnover values can be used in conjunction with Fig. 3 to determine the merchant’s security against an attacker who is capable of capturing the -maximal goods. For example, if the merchant requires confirmations, and the observed aggregate -block turnover is similar to the median aggregate turnover of 10K BTC, then she can be confident that she is protected against double-spends from an attacker with .

Attacks by new miners. Thus far we have assumed that the attacker is a defecting miner, but it is also possible that a third party may bring new mining power to these attacks (purchased or, for example, stolen via a botnet), which we call expansion. Recall that we assume the hash difficulty remains the same during the attack, so regardless of how the attacker garners mining power, he is always capable of mining the same expected number of blocks in a given period of time. An attacker who expands the mining power does not change our earlier analysis in Case 1 because the attacker is mining on a fraudulent branch that will never actually be publicly released. Therefore the salient factors, opportunity cost and mining rate, do not change. However the analysis does change for Case 2 because the attacker must compete with the other miners to grow his fraudulent branch longer than the main branch. For example, when an attacker with 1/3 of the existing mining power defects, he can expect to mine approximately of all mined blocks. In contrast, when expanding the mining power by 1/3, the attacker only expects to mine blocks at approximately the rate of the rest of the miners. Our existing analysis models the former scenario, but can easily be adjusted to model the latter by changing the honest miner block creation rate from to .

Coinbase and fees. Bitcoin’s security is critically related to the reward for mining. On July 9, 2016, the rewarded coinbase halved from to . All of our analysis assumes that . In 2020, Bitcoin’s security against double-spends will decrease further since the coinbase reward will halve again. A lower block reward absent higher fees or a significant increase in Bitcoin’s fiat-exchange value will make it cheaper for attackers to procure a higher percentage of the mining power. Hence, if conditions remain the same except for a decrease in coinbase reward, then merchants will need to wait for more confirmations before releasing goods.

Setting the deadline. Our mitigation measures recommend that the merchant set a deadline when she suspects that there is risk of a concurrent eclipse and double-spend attack. Lower values of increase the break-even value for the attacker, which increases security. The downside to securing goods with a shorter deadline is that honest customers may not succeed in meeting the deadline due to the inherent randomness of block discovery. For example, according to actual block mining data we collected from 2016, only about 60% of consecutive blocks of length actually arrived within a deadline of minutes. Therefore, it is wise for the merchant and customer to agree on a contingency plan for cases where the deadline is missed. In many cases the customer will trust the merchant to issue a refund. In more adversarial settings, a third-party escrow service can be used to enforce a fair exchange of coin before the goods are released [17]. If neither solution is acceptable, then the deadline should be relaxed so that the chances the entire mining community miss it are very small.

Advice to Bitcoin merchants. Because it is impossible to know how many merchants will be targeted simultaneously, we recommend that merchants always choose equal to the -maximal goods they observe for the blocks beginning with the one that confirms their transaction. Merchants are best off setting to address one of two cases. (1) Least conservatively, merchants could trust powerful miners to not carry out double-spend attacks, and assume that the common case is an attacker that has of the mining power. In this case, thwarts attackers when goods at risk are below 100 BTC, even under an eclipse attack. (2) Very conservatively, merchants can require confirmations (a little over 9 hours), which protects them against an attacker controlling of the mining power even with goods at risk worth as much as 1M BTC (currently about $700M).

Applications to off-chain and side-chain protocols. In its full generality, our analysis quantifies the security of an exchange of some off-blockchain quantity for Bitcoin. For most of this section, we have imagined a merchant trading physical goods or services. But our results apply equally to many systems that rely on or assume a stable blockchain, including sidechains [1], micropayment channels such as the Lightning Network [18] and TumbleBit [12], and the XIM decentralized mix service [2].

All these alternate protocols require a certain transaction, , be confirmed in a Bitcoin block that locks or moves coin while in use by the other protocol. If the Bitcoin miners subsequently switch to a branch that doesn’t include (or worse, includes a transaction that prohibits ’s validity in future blocks), then a reorganization of the alternate protocol’s blockchain or transaction is required, resulting in havoc. Unfortunately, due to the FLP impossibility result [10], it is always possible for an attacker with sufficient resources to force a reorganization. And so in all cases, these protocols vaguely recommend the block containing the transaction reach a sufficient depth. For example, Back et al [1] recommends that “a typical confirmation period would be on the order of a day or two.” Sasson [22] recommends that users with “sensitive transactions only spend coins relative to blocks further back in the ledger”.

Using our analysis, the confirmation depth required for can be more precisely calculated, and the risk of the reorganization can be quantified as follows. First, participants wait for to be confirmed in a block. Then as confirmations accumulate, participants can use a resource like figure Fig. 3 (which can be constructed for arbitrary parameter combinations using Eqs. 10 and 22) to determine the their security (in terms of attacker mining power ) given the current goods at risk. Eventually, they should settle on confirmations such that the security is considered to be sufficiently high for their purposes.

5 Conclusion

We have presented a novel economic model of Bitcoin double spend attacks that incorporates the depth of the block containing the transaction of interest, the attacker’s mining power, goods at risk, and coinbase reward. Based on this model, we have shown that the security of a transaction increases roughly logarithmically with the number of confirmations that it receives, where an attacker benefits from the increasing goods at risk but is also throttled by the increasing proof of work required. Additionally, we have demonstrated that, if merchants impose a conservative confirmation deadline, the eclipse attack does not increase an attacker’s profit when his share of the mining power is less than 35% or more than 10 confirmations are required.

References

- [1] Back, A., Corallo, M., Dashjr, L., Mark, F., Maxwell, G., Miller, A., Poelstra, A., Timón, J., Wuille, P.: Enabling Blockchain Innovations with Pegged Sidechains. http://www.opensciencereview.com/papers/123/enablingblockchain-innovations-with-pegged-sidechains (October 2014)

- [2] Bissias, G., Ozisik, A.P., Levine, B.N., Liberatore, M.: Sybil-Resistant Mixing for Bitcoin. In: Proc. ACM Workshop on Privacy in the Electronic Society (November 2014), http://forensics.umass.edu/pubs/bissias.wpes.2014.pdf

- [3] Confirmation. https://en.bitcoin.it/wiki/Confirmation (February 2015)

- [4] Bonneau, J., Miller, A., Clark, J., Narayanan, A., Kroll, J., Felten, E.: Sok: Research perspectives and challenges for bitcoin and cryptocurrencies. In: IEEE S&P. pp. 104–121 (May 2015), http://doi.org/10.1109/SP.2015.14

- [5] Bonneau, J.: How long does it take for a bitcoin transaction to be confirmed? https://coincenter.org/2015/11/what-does-it-mean-for-a-bitcoin-transaction-to-be-confirmed/ (November 2015)

- [6] Croman, K., et al.: On Scaling Decentralized Blockchains . In: Workshop on Bitcoin and Blockchain Research (Feb 2016)

- [7] Douceur, J.: The Sybil Attack. In: Proc. Intl Wkshp on Peer-to-Peer Systems (IPTPS) (Mar 2002)

- [8] Ethereum Homestead Documentation. http://ethdocs.org/en/latest/

- [9] Eyal, I., Sirer, E.G.: Majority Is Not Enough: Bitcoin Mining Is Vulnerable. Financial Cryptography pp. 436–454 (2014), http://doi.org/10.1007/978-3-662-45472-5_28

- [10] Fischer, M., Lynch, N., Paterson, M.: Impossibility of distributed consensus with one faulty process. JACM 32(2), 374–382 (1985)

- [11] Gervais, A., O. Karame, G., Wust, K., Glykantzis, V., Ritzdorf, H., Capkun, S.: On the Security and Performance of Proof of Work Blockchains. https://eprint.iacr.org/2016/555 (2016)

- [12] Heilman, E., Alshenibr, L., Baldimtsi, F., Scafuro, A., Goldberg, S.: Tumblebit: An untrusted bitcoin-compatible anonymous payment hub. Cryptology ePrint Archive, Report 2016/575 (2016), http://eprint.iacr.org/2016/575

- [13] Heilman, E., Kendler, A., Zohar, A., Goldberg, S.: Eclipse Attacks on Bitcoin’s Peer-to-peer Network. In: USENIX Security (2015)

- [14] Litecoin. http://litecoin.org/

- [15] Meiklejohn, S., Pomarole, M., Jordan, G., Levchenko, K., McCoy, D., Voelker, G., Savage, S.: A Fistful of Bitcoins: Characterizing Payments Among Men with No Names. In: Proc. ACM IMC. pp. 127–140 (2013), http://doi.acm.org/10.1145/2504730.2504747

- [16] Nakamoto, S.: Bitcoin: A Peer-to-Peer Electronic Cash System. https://bitcoin.org/bitcoin.pdf (May 2009)

- [17] Pagnia, H., Vogt, H., Gaertner, F.: Fair Exchange. The Computer Journal, vol. 46, num. 1, p. 55, 2003. 46(1), 55–78 (2003)

- [18] Poon, J., Dryja, T.: The Bitcoin Lightning Network: Scalable Off-Chain Instant Payments. http://www.lightning.network/lightning-network-paper.pdf (November 2015)

- [19] Ron, D., Shamir, A.: Quantitative analysis of the full bitcoin transaction graph. In: Proc. Financial Crypto. pp. 6–24 (Apr 2013), http://doi.org/10.1007/978-3-642-39884-1_2

- [20] Rosenfeld, M.: Analysis of hashrate-based double-spending. https://bitcoil.co.il/Doublespend.pdf (December 2012)

- [21] Sapirshtein, A., Sompolinsky, Y., Zohar, A.: Optimal Selfish Mining Strategies in Bitcoin. https://arxiv.org/pdf/1507.06183.pdf (July 2015)

- [22] Sasson, E.B., Chiesa, A., Garman, C., Green, M., Miers, I., Tromer, E., Virza, M.: Zerocash: Decentralized anonymous payments from bitcoin. In: IEEE S&P. pp. 459–474 (2014), http://dx.doi.org/10.1109/SP.2014.36

- [23] Sompolinsky, Y., Zohar, A.: Secure high-rate transaction processing in Bitcoin. Financial Cryptography and Data Security (2015), http://doi.org/10.1007/978-3-662-47854-7_32

- [24] Sompolinsky, Y., Zohar, A.: Bitcoin’s Security Model Revisited. https://arxiv.org/abs/1605.09193 (May 2016)

- [25] Tschorsch, F., Scheuermann, B.: Bitcoin and beyond: A technical survey on decentralized digital currencies. IEEE Communications Surveys Tutorials PP(99), 1–1 (2016)

Appendix 0.A Blockchain and Bitcoin Overview

The mining process places peers with significant computational power at an advantage, but overall, incentivizes miners to reach consensus. Bitcoin and follow-on currencies, such as Litecoin[14], Zerocash [22], Ethereum[8], and many others [4], also use the blockchain algorithm to manage an electronic payment system.

Bitcoins exist as balance in a set of accounts called addresses. Bitcoin users exchange money through transactions, which transfer Bitcoin from one set of address to another. Transactions are broadcast over Bitcoin’s p2p network where they are picked up by miners. Miners each independently agglomerate a set of transactions into a block, verify that the transactions are valid, and attempt to solve a predefined proof-of-work problem involving this block and all prior valid blocks. In Bitcoin, this process is dynamically calibrated to take approximately ten minutes per block. Under ordinary, non-adversarial, conditions, the first miner to solve the proof-of-work problem broadcasts her solution to the network, adding it to the ever-growing blockchain; the miners then start over, trying to add a new block containing the set of transactions that were not previously added.

A transaction appearing in a block is considered confirmed. When blocks have been added after the confirming block, the transaction is said to have received confirmations. If two miners discover a new block simultaneously, the blockchain will bifurcate. Miners will attempt to add to the branch with greatest cumulative proof-of-work. All miners will subsequently switch to mining on the first branch that grows longer. As incentive, all miners insert, as the first item in their block, a coinbase transaction, which is the protocol-defined creation of new coins and a transfer of those coins into a address of their choosing. In doing so, they have mined those coins and made the chosen address and its balance valid in future transactions. Miners also receive a small fraction of the face value of all transactions in the block that they successfully add to the blockchain; this transaction fee overhead serves to incentivize miners even after the last protocol-defined bitcoin is mined. Miners are commonly organized into mining pools, which allow many miners to pool together their resources. In these pools, rewards are split equitably according to the amount of resources they contributed to creating a block.