Binarsity: a penalization for one-hot encoded features in linear supervised learning

Abstract

This paper deals with the problem of large-scale linear supervised learning in settings where a large number of continuous features are available. We propose to combine the well-known trick of one-hot encoding of continuous features with a new penalization called binarsity. In each group of binary features coming from the one-hot encoding of a single raw continuous feature, this penalization uses total-variation regularization together with an extra linear constraint. This induces two interesting properties on the model weights of the one-hot encoded features: they are piecewise constant, and are eventually block sparse. Non-asymptotic oracle inequalities for generalized linear models are proposed. Moreover, under a sparse additive model assumption, we prove that our procedure matches the state-of-the-art in this setting. Numerical experiments illustrate the good performances of our approach on several datasets. It is also noteworthy that our method has a numerical complexity comparable to standard penalization.

Keywords. Supervised learning; Features binarization; Sparse additive modeling; Total-variation; Oracle inequalities; Proximal methods

1 Introduction

In many applications, datasets used for linear supervised learning contain a large number of continuous features, with a large number of samples. An example is web-marketing, where features are obtained from bag-of-words scaled using tf-idf [45], recorded during the visit of users on websites. A well-known trick [53, 35] in this setting is to replace each raw continuous feature by a set of binary features that one-hot encodes the interval containing it, among a list of intervals partitioning the raw feature range. This improves the linear decision function with respect to the raw continuous features space, and can therefore improve prediction. However, this trick is prone to over-fitting, since it increases significantly the number of features.

A new penalization.

To overcome this problem, we introduce a new penalization called binarsity, that penalizes the model weights learned from such grouped one-hot encodings (one group for each raw continuous feature). Since the binary features within these groups are naturally ordered, the binarsity penalization combines a group total-variation penalization, with an extra linear constraint in each group to avoid collinearity between the one-hot encodings. This penalization forces the weights of the model to be as constant (with respect to the order induced by the original feature) as possible within a group, by selecting a minimal number of relevant cut-points. Moreover, if the model weights are all equal within a group, then the full block of weights is zero, because of the extra linear constraint. This allows to perform raw feature selection.

High-dimensional linear supervised learning.

To address the high-dimensionality of features, sparse linear inference is now an ubiquitous technique for dimension reduction and variable selection, see for instance [14] and [28] among many others. The principle is to induce sparsity (large number of zeros) in the model weights, assuming that only a few features are actually helpful for the label prediction. The most popular way to induce sparsity in model weights is to add a -penalization (Lasso) term to the goodness-of-fit [48]. This typically leads to sparse parametrization of models, with a level of sparsity that depends on the strength of the penalization. Statistical properties of -penalization have been extensively investigated, see for instance [31, 56, 15, 9] for linear and generalized linear models and [22, 21, 17, 16] for compressed sensing, among others.

However, the Lasso ignores ordering of features. In [49], a structured sparse penalization is proposed, known as fused Lasso, which provides superior performance in recovering the true model in such applications where features are ordered in some meaningful way. It introduces a mixed penalization using a linear combination of the -norm and the total-variation penalization, thus enforcing sparsity in both the weights and their successive differences. Fused Lasso has achieved great success in some applications such as comparative genomic hybridization [42], image denoising [23], and prostate cancer analysis [49].

Features discretization and cuts.

For supervised learning, it is often useful to encode the input features in a new space to let the model focus on the relevant areas [53]. One of the basic encoding technique is feature discretization or feature quantization [35] that partitions the range of a continuous feature into intervals and relates these intervals with meaningful labels. Recent overviews of discretization techniques can be found in [35] or [25].

Obtaining the optimal discretization is a NP-hard problem [18], and an approximation can be easily obtained using a greedy approach, as proposed in decision trees: CART [13] and C4.5 [41], among others, that sequentially select pairs of features and cuts that minimize some purity measure (intra-variance, Gini index, information gain are the main examples). These approaches build decision functions that are therefore very simple, by looking only at a single feature at a time, and a single cut at a time. Ensemble methods (boosting [36], random forests [12]) improve this by combining such decisions trees, at the expense of models that are harder to interpret.

Main contribution.

This paper considers the setting of linear supervised learning. The main contribution of this paper is the idea to use a total-variation penalization, with an extra linear constraint, on the weights of a generalized linear model trained on a binarization of the raw continuous features, leading to a procedure that selects multiple cut-points per feature, looking at all features simultaneously. Our approach therefore increases the capacity of the considered generalized linear model: several weights are used for the binarized features instead of a single one for the raw feature. This leads to a more flexible decision function compared to the linear one: when looking at the decision function as a function of a single raw feature, it is now piecewise constant instead of linear, as illustrated in Figure 2 below.

Organization of the paper.

The proposed methodology is described in Section 2. Section 3 establishes an oracle inequality for generalized linear models and provides a convergence rate for our procedure in the particular case of a sparse additive model. Section 4 highlights the results of the method on various datasets and compares its performances to well known classification algorithms. Finally, we discuss the obtained results in Section 5.

Notations.

Throughout the paper, for every we denote by the usual -quasi norm of a vector namely , and . We also denote , where stands for the cardinality of a finite set . For , we denote by the Hadamard product For any and any we denote as the vector in satisfying for and for . We write, for short, (resp. ) for the vector of having all coordinates equal to one (resp. zero). Finally, we denote by the set of sub-differentials of the function , namely if , if and .

2 The proposed method

Consider a supervised training dataset containing features and labels , that are independent and identically distributed samples of with unknown distribution . Let us denote the features matrix vertically stacking the samples of raw features. Let be the -th feature column of .

Binarization.

The binarized matrix is a matrix with an extended number of columns, where the -th column is replaced by columns containing only zeros and ones. Its -th row is written

where . In order to simplify the presentation of our results, we assume in the paper that all raw features are continuous, so that they are transformed using the following one-hot encoding. For each raw feature , we consider a partition of intervals of , namely satisfying and for and define

for , and . An example is interquantiles intervals, namely and for , where denotes a quantile of order for . In practice, if there are ties in the estimated quantiles for a given feature, we simply choose the set of ordered unique values to construct the intervals. This principle of binarization is a well-known trick [25], that allows to improve over the linear decision function with respect to the raw feature space: it uses a larger number of model weights, for each interval of values for the feature considered in the binarization. If training data contains also unordered qualitative features, one-hot encoding with -penalization can be used for instance.

Goodness-of-fit.

Given a loss function , we consider the goodness-of-fit term

| (1) |

where and where we recall that . We then have , with corresponding to the group of coefficients weighting the binarized raw -th feature. We focus on generalized linear models [26], where the conditional distribution is assumed to be from a one-parameter exponential family distribution with a density of the form

| (2) |

with respect to a reference measure which is either the Lebesgue measure (e.g. in the Gaussian case) or the counting measure (e.g. in the logistic or Poisson cases), leading to a loss function of the form

The density described in (2) encompasses several distributions, see Table 1. The functions and are known, while the natural parameter function is unknown. The dispersion parameter is assumed to be known in what follows. It is also assumed that is three times continuously differentiable. It is standard to notice that

where stands for the derivative of . This formula explains how links the conditional expectation to the unknown . The results given in Section 3 rely on the following Assumption.

Assumption 1

Assume that is three times continuously differentiable, that there is such that for any and that there exist constants and such that and

This assumption is satisfied for most standard generalized linear models. In Table 1, we list some standard examples that fit in this framework, see also [51] and [44].

| Model | ||||||||

|---|---|---|---|---|---|---|---|---|

| Normal | ||||||||

| Logistic | 2 | |||||||

| Poisson | 1 |

Binarsity.

Several problems occur when using the binarization trick described above:

-

(P1)

The one-hot-encodings satisfy for , meaning that the columns of each block sum to , making not of full rank by construction.

-

(P2)

Choosing the number of intervals for binarization of each raw feature is not an easy task, as too many might lead to overfitting: the number of model-weights increases with each , leading to a over-parametrized model.

-

(P3)

Some of the raw features might not be relevant for the prediction task, so we want to select raw features from their one-hot encodings, namely induce block-sparsity in .

A usual way to deal with (P1) is to impose a linear constraint [1] in each block. In order to do so, let us introduce first and the vector . In our penalization term, we impose the linear constraint

| (3) |

for all . Note that if the are taken as interquantiles intervals, then for each , we have that for are equal and the constraint (3) becomes the standard constraint .

The trick to tackle (P2) is to remark that within each block, binary features are ordered. We use a within block total-variation penalization

where

| (4) |

with weights to be defined later, to keep the number of different values taken by to a minimal level.

Finally, dealing with (P3) is actually a by-product of dealing with (P1) and (P2). Indeed, if the raw feature is not-relevant, then should have all entries constant because of the penalization (4), and in this case all entries are zero, because of (3). We therefore introduce the following penalization, called binarsity

| (5) |

where the weights are defined in Section 3 below, and where

| (6) |

We consider the goodness-of-fit (1) penalized by (5), namely

| (7) |

An important fact is that this optimization problem is numerically cheap, as explained in the next paragraph. Figure 1 illustrates the effect of the binarsity penalization with a varying strength on an example.

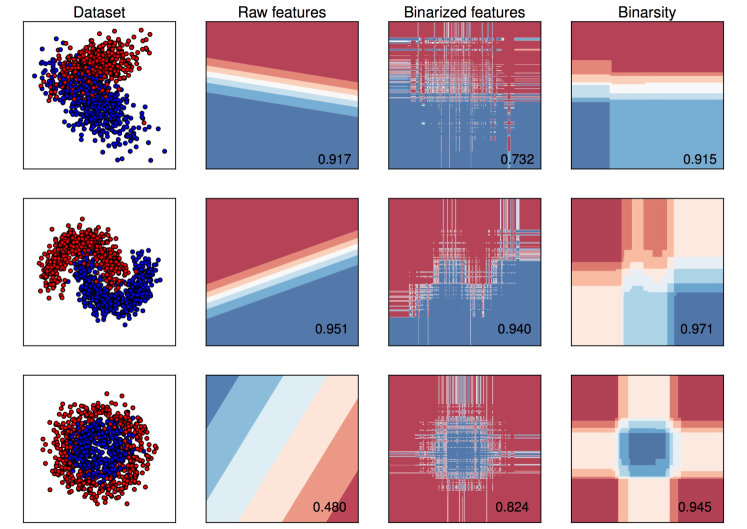

In Figure 2, we illustrate on a toy example, when , the decision boundaries obtained for logistic regression (LR) on raw features, LR on binarized features and LR on binarized features with the binarsity penalization.

Proximal operator of binarsity.

The proximal operator and proximal algorithms are important tools for non-smooth convex optimization, with important applications in the field of supervised learning with structured sparsity [4]. The proximal operator of a proper lower semi-continuous [8] convex function is defined by

Proximal operators can be interpreted as generalized projections. Namely, if is the indicator of a convex set given by

then is the projection operator onto . It turns out that the proximal operator of binarsity can be computed very efficiently, using an algorithm [19] that we modify in order to include weights . It applies in each group the proximal operator of the total-variation since binarsity penalization is block separable, followed by a simple projection onto the orthogonal of , see Algorithm 1 below. We refer to Algorithm 2 in Section 6.2 for the weighted total-variation proximal operator.

Proposition 1

A proof of Proposition 1 is given in Section 6.1. Algorithm 1 leads to a very fast numerical routine, see Section 4. The next section provides a theoretical analysis of our algorithm with an oracle inequality for the prediction error, together with a convergence rate in the particular case of a sparse additive model.

3 Theoretical guarantees

We now investigate the statistical properties of (8) where the weights in the binarsity penalization have the form

for all , see Theorem 1 for a precise definition of . Note that corresponds to the proportion of ones in the sub-matrix obtained by deleting the first columns in the -th binarized block matrix In particular, we have for all . We consider the risk measure defined by

which is standard with generalized linear models [51].

3.1 A general oracle inequality

We aim at evaluating how “close” to the minimal possible expected risk our estimated function with given by (8) is. To measure this closeness, we establish a non-asymptotic oracle inequality with a fast rate of convergence considering the excess risk of , namely . To derive this inequality, we consider for technical reasons the following problem instead of (7):

| (8) |

where

This constraint is standard in literature for the proof of oracle inequalities for sparse generalized linear models, see for instance [51], and is discussed in details below.

We also impose a restricted eigenvalue assumption on For all let be the concatenation of the support sets relative to the total-variation penalization, that is

Similarly, we denote the complementary of The restricted eigenvalue condition is defined as follow.

Assumption 2

Let be a concatenation of index sets such that

| (9) |

where is a positive integer. Define

with

| (10) |

We assume that the following condition holds

| (11) |

for any satisfying (9).

The set is a cone composed by all vectors with a support “close” to . Theorem 1 gives a risk bound for the estimator .

Theorem 1

The proof of Theorem 1 is given in Section 6.3 below. Note that the “variance” term or “complexity” term in the oracle inequality satisfies

| (13) |

The value characterizes the sparsity of the vector , given by

It counts the number of non-equal consecutive values of . If is block-sparse, namely whenever where (meaning that few raw features are useful for prediction), then , which means that is controlled by the block sparsity .

The oracle inequality from Theorem 1 is stated uniformly for vectors satisfying for all and . Writing this oracle inequality under the assumption meets the standard way of stating sparse oracle inequalities, see e.g. [14]. Note that is introduced in Assumption 2 and corresponds to a maximal sparsity for which the matrix satisfies the restricted eigenvalue assumption. Also, the oracle inequality stated in Theorem 1 stands for vectors such that , which is natural since the binarsity penalization imposes these extra linear constraints.

The assumption that is a technical one, that allows to establish a connection, via the notion of self-concordance, see [3], between the empirical squared -norm and the empirical Kullback divergence (see Lemma 5 in Section 6.3). It corresponds to a technical constraint which is commonly used in literature for the proof of oracle inequalities for sparse generalized linear models, see for instance [51], a recent contribution for the particular case of Poisson regression being [30]. Also, note that

| (14) |

where . The first inequality in (14) comes from the fact that the entries of are in , and it entails that whenever . The second inequality in (14) entails that can be upper bounded by , and therefore the constraint becomes only a box constraint on , which depends on the dimensionality of the features through only. The fact that the procedure depends on , and that the oracle inequality stated in Theorem 1 depends linearly on is commonly found in literature about sparse generalized linear models, see [51, 3, 30]. However, the constraint is a technicality which is not used in the numerical experiments provided in Section 4 below.

3.2 Sparse linear additive regression

Theorem 1 allows to study a particular case, namely an additive model, see e.g. [27, 29] and in particular a sparse additive linear model, which is of particular interest in high-dimensional statistics, see [38, 43, 14]. We prove in Theorem 2 below that our procedure matches the convergence rates previously known from literature. In this setting, we work under the following assumptions.

Assumption 3

We assume to simplify that for all . We consider the Gaussian setting with the least-squares loss, namely , and (noise variance) in Equation (2), with , in Assumption 1. Moreover, we assume that has the following sparse additive structure

for , where are -Lipschitz functions, namely satisfying for any , and where is a set of active features (sparsity means that ). Also, we assume the following identifiability condition

for all .

Assumption 3 contains identifiability and smoothness requirements that are standard when studying additive models, see e.g. [38]. We restrict the functions to be Lipschitz and not smoother, since our procedure produces a piecewise constant decision function with respect to each , that can approximate optimally only Lipschitz functions. For more regular functions, our procedure would lead to suboptimal rates, see also the discussion below the statement of Theorem 2.

Theorem 2

The proof of Theorem 2 is given in Section 6.8 below. It is an easy consequence of Theorem 1 under the sparse additive model assumption. It uses Assumption 2 with , since is the minimizer of the bias for each , see the proof of Theorem 2 for details.

The rate of convergence is, up to constants and logarithmic terms, of order Recalling that we work under a Lipschitz assumption, namely Hölder smoothness of order , the scaling of this rate w.r.t. to is with , which matches the one-dimensional minimax rate. This rate matches the one obtained in [14], see Chapter 8 p. 272, where the rate is derived under a smoothness assumption, namely . Hence, Theorem 2 shows that, in the particular case of a sparse additive model, our procedure matches in terms of convergence rate the state of the art. Further improvements could consider more general smoothness (beyond Lipschitz) and adaptation with respect to the regularity, at the cost of a more complicated procedure which is beyond the scope of this paper.

4 Numerical experiments

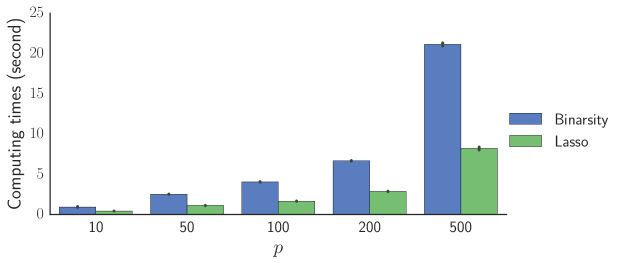

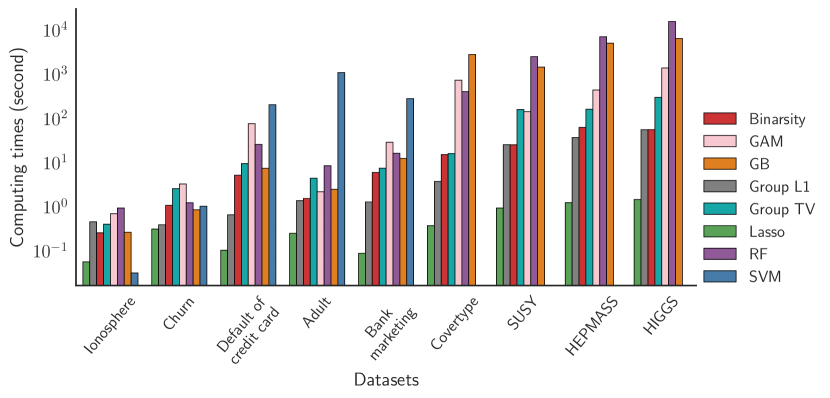

In this section, we first illustrate the fact that the binarsity penalization is roughly only two times slower than basic -penalization, see the timings in Figure 3. We then compare binarsity to a large number of baselines, see Table 2, using 9 classical binary classification datasets obtained from the UCI Machine Learning Repository [34], see Table 3.

| Name | Description | Reference |

|---|---|---|

| Lasso | Logistic regression (LR) with penalization | [50] |

| Group L1 | LR with group penalization | [37] |

| Group TV | LR with group total-variation penalization | |

| SVM | Support vector machine with radial basis kernel | [46] |

| GAM | Generalized additive model | [27] |

| RF | Random forest classifier | [12] |

| GB | Gradient boosting | [24] |

| Dataset | #Samples | #Features | Reference |

|---|---|---|---|

| Ionosphere | 351 | 34 | [47] |

| Churn | 3333 | 21 | [34] |

| Default of credit card | 30000 | 24 | [54] |

| Adult | 32561 | 14 | [32] |

| Bank marketing | 45211 | 17 | [39] |

| Covertype | 550088 | 10 | [10] |

| SUSY | 5000000 | 18 | [7] |

| HEPMASS | 10500000 | 28 | [6] |

| HIGGS | 11000000 | 24 | [7] |

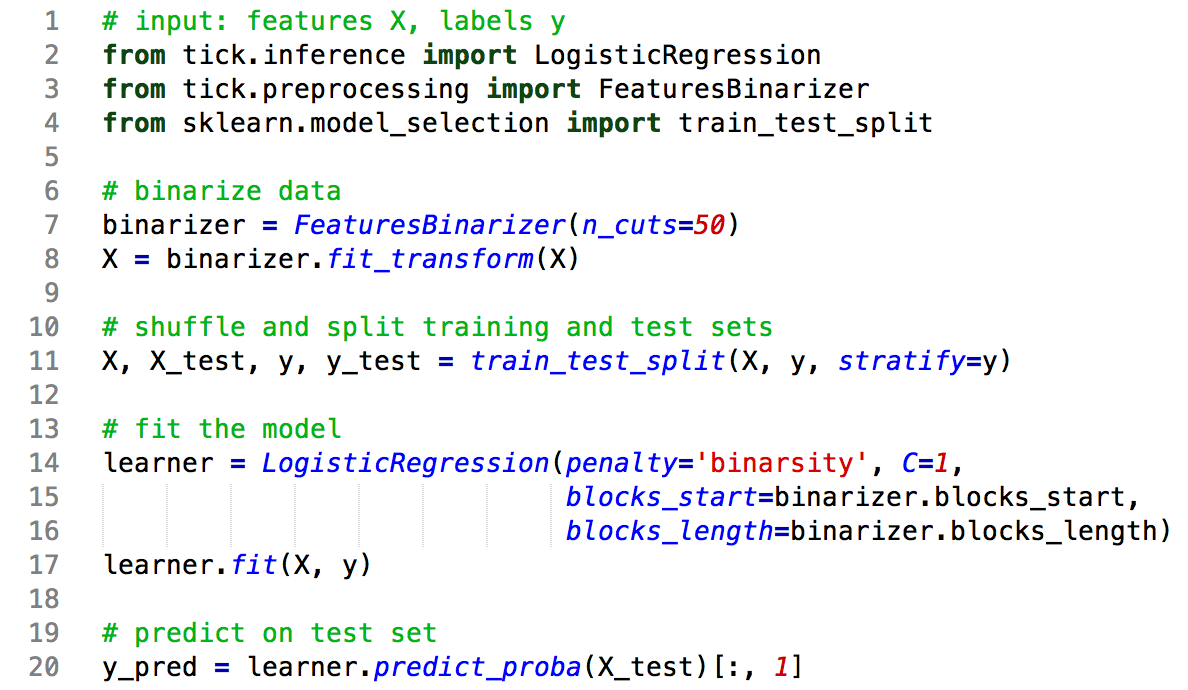

For each method, we randomly split all datasets into a training and a test set (30% for testing), and all hyper-parameters are tuned on the training set using -fold cross-validation with . For support vector machine with radial basis kernel (SVM), random forests (RF) and gradient boosting (GB), we use the reference implementations from the scikit-learn library [40], and we use the LogisticGAM procedure from the pygam library444https://github.com/dswah/pyGAM for the GAM baseline. The binarsity penalization is proposed in the tick library [5], we provide sample code for its use in Figure 4. Logistic regression with no penalization or ridge penalization gave similar or lower scores for all considered datasets, and are therefore not reported in our experiments.

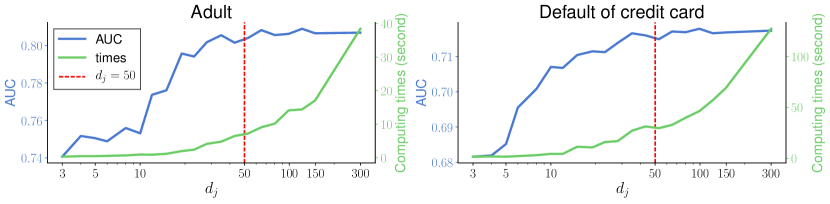

The binarsity penalization does not require a careful tuning of (number of bins for the one-hot encoding of raw feature ). Indeed, past a large enough value, increasing even further barely changes the results since the cut-points selected by the penalization do not change anymore. This is illustrated in Figure 5, where we observe that past bins, increasing even further does not affect the performance, and only leads to an increase of the training time. In all our experiments, we therefore fix for .

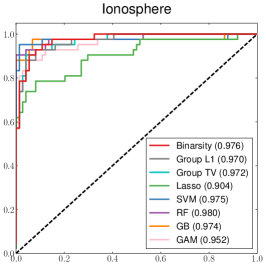

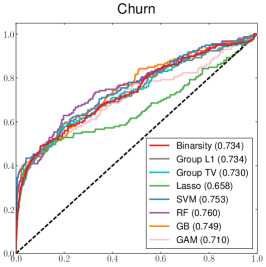

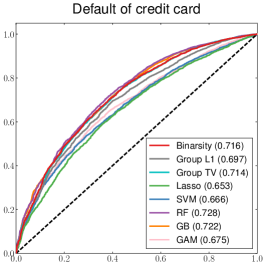

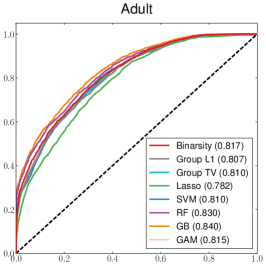

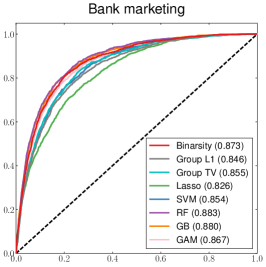

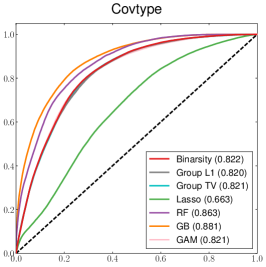

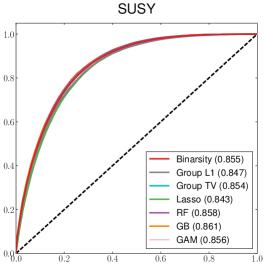

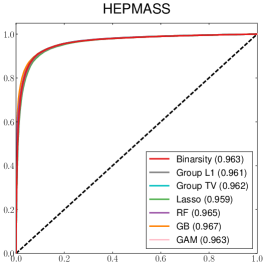

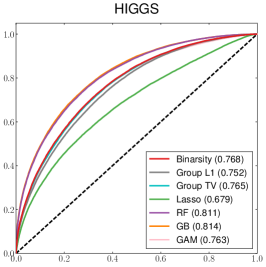

The results of all our experiments are reported in Figures 6 and 7. In Figure 6 we compare the performance of binarsity with the baselines on all 9 datasets, using ROC curves and the Area Under the Curve (AUC), while we report computing (training) timings in Figure 7. We observe that binarsity consistently outperforms Lasso, as well as Group L1: this highlights the importance of the TV norm within each group. The AUC of Group TV is always slightly below the one of binarsity, and more importantly it involves a much larger training time: convergence is slower for Group TV, since it does not use the linear constraint of binarsity, leading to a ill-conditioned problem (sum of binary features equals 1 in each block). Finally, binarsity outperforms also GAM and its performance is comparable in all considered examples to RF and GB, with computational timings that are orders of magnitude faster, see Figure 7. All these experiments illustrate that binarsity achieves an extremely competitive compromise between computational time and performance, compared to all considered baselines.

5 Conclusion

In this paper, we introduced the binarsity penalization for one-hot encodings of continuous features. We illustrated the good statistical properties of binarsity for generalized linear models by proving non-asymptotic oracle inequalities. We conducted extensive comparisons of binarsity with state-of-the-art algorithms for binary classification on several standard datasets. Experimental results illustrate that binarsity significantly outperforms Lasso, Group L1 and Group TV penalizations and also generalized additive models, while being competitive with random forests and boosting. Moreover, it can be trained orders of magnitude faster than boosting and other ensemble methods. Even more importantly, it provides interpretability. Indeed, in addition to the raw feature selection ability of binarsity, the method pinpoints significant cut-points for all continuous feature. This leads to a much more precise and deeper understanding of the model than the one provided by Lasso on raw features. These results illustrate the fact that binarsity achieves an extremely competitive compromise between computational time and performance, compared to all considered baselines.

6 Proofs

In this Section we gather the proofs of all the theoretical results proposed in the paper. Throughout this Section, we denote by the subdifferential mapping of a convex function

6.1 Proof of Proposition 1

Recall that the indicator function is given by (6). For any fixed we prove that is the composition of and namely

for all . Using Theorem 1 in [55], it is sufficient to show that for all we have

| (15) |

We have where stands for the projection onto the orthogonal of . This projection simply writes

Now, let us define the matrix by

| (16) |

We then remark that for all ,

| (17) |

Using subdifferential calculus (see details in the proof of Proposition 2 below), one has

Then, the linear constraint entails

which leads to (15) and concludes the proof of the Proposition.

6.2 Proximal operator of the weighted TV penalization

We recall in Algorithm 2 an algorithm provided in [2] for the computation of the proximal operator of the weighted total-variation penalization

| (18) |

A quick explanation of this algorithm is as follows. The algorithm runs forwardly through the input vector Using Karush-Kuhn-Tucker (KKT) optimality conditions [11], we have that at a location the weight stays constant whenever , where is a solution to a dual problem associated to the primal problem (18). If not possible, it goes back to the last location where a jump can be introduced in , validates the current segment until this location, starts a new segment, and continues.

6.3 Proof of Theorem 1

The proof relies on several technical properties that are described below. From now on, we consider , , and recalling that we introduce and

Let us now define the Kullback-Leibler divergence between the true probability density funtion defined in (2) and a candidate within the generalized linear model as follows

where is the joint distribution of given . We then have the following Lemma.

Lemma 1

The excess risk satisfies

where we recall that is the dispertion parameter of the generalized linear model, see (2).

Proof. If follows from the following simple computation

which proves the Lemma.

6.4 Optimality conditions

As explained in the following Proposition, a solution to problem (8) can be characterized using the Karush-Kuhn-Tucker (KKT) optimality conditions [11].

Proposition 2

A vector is an optimum of the objective function (8) if and only if there are subgradients and such that

where

| (19) |

and where we recall that is the support set of . The subgradient belongs to

For the generalized linear model, we have

| (20) |

where belongs to the normal cone of the ball

Proof. The function is differentiable, so the subdifferential of at a point is given by

where and

We have for all . Then, by applying some properties of the subdifferential calculus, we get

| (21) |

where for all . For generalized linear models, we rewrite

| (22) |

where is the indicator function of . Now, is an optimum of (22) if and only if . Recall that the subdifferential of is the normal cone of , namely

| (23) |

One has

| (24) |

so that together with (24) and (23) we obtain (20), which concludes the proof of Proposition 2.

6.5 Compatibility conditions

Let us define the block diagonal matrix with defined in (16). We denote its inverse which is defined by the lower triangular matrix with entries if and otherwise. We set , so that one has .

In order to prove Theorem 1, we need the following results which give a compatibility property [51, 52, 20] for the matrix , see Lemma 2 below and for the matrix , see Lemma 3 below. For any concatenation of subsets we set

| (25) |

for all with the convention that and .

Lemma 2

Proof. Using Proposition 3 in [20], we have

Using Hölder’s inequality for the right hand side of the last inequality gives

which completes the proof of the Lemma.

Lemma 3

6.6 Connection between the empirical Kullback-Leibler divergence and the empirical squared norm

The next Lemma is from [3] (see Lemma 1 herein).

Lemma 4

Let be a three times differentiable convex function such that for all for some Then, for all , one has

with .

This Lemma entails the following in our setting.

Lemma 5

Proof. Let us consider the function defined by , with to be defined later, which writes

We have

Using Assumption 1, we have where . Lemma 4 with gives

for all and leads to

An easy computation gives

and since obviously , we obtain

Now, choosing and combining Assumption 1 with Equation (14) gives

Hence, since is an increasing function on , we end up with

and since , we obtain

which concludes the proof of the Lemma.

6.7 Proof of Theorem 1

Let us recall that

for all and that

| (28) |

Proposition 2 above entails that there is , and such that

for all . This can be rewritten as

For any such that for all and , the monotony of the subdifferential mapping implies and , so that

| (29) |

Now, consider the function defined by

where will be defined later. We use again the same arguments as in the proof of Lemma 5. We differentiate three times with respect , so that

and in the way as in the proof of Lemma 5, we have , and Lemma 4 entails

for all . Taking and implies

| and |

Moreover, we have

Then, we deduce that

Then, with Equation (29), one has

| (30) |

As , it implies that

| (31) |

If it follows that

then Theorem 1 holds. From now on, let us assume that

| (32) |

We first derive a bound on Recall that (see beginning of Section 6.5). We focus on finding out a bound for On the one hand, one has

where is the -th column of the matrix Let us consider the event

so that, on , we have

| (33) |

On the other hand, from the definition of the subgradient (see Equation (19)), one can choose such that

for all and

for all . Using a triangle inequality and the fact that , we obtain

| (34) |

Combining inequalities (6.7) and (6.7), we get

on . Hence

This means that

| (35) |

see (10) and (27). Now, going back to (6.7) and taking into account (35), the compatibility of given in Equation (26) provides the following on the event :

Then

| (36) |

where is such that

for all and

Now, we find an upper bound for

Note that . Let us write and set for with the convention that and . Then

Therefore

| (37) |

Now, we use the connection between the empirical norm and Kullback-Leibler divergence. Indeed, using Lemma 5, we get

where we defined , so that combined with Equation (36), we obtain

This inequality entails the following upper bound

since whenever we have for some , then . Introducing , we note that

since for any . Finally, by using also (37), we end up with

which is the statement provided in Theorem 1. The only thing remaining is to control the probability of the event . This is given by the following:

Let and Note that conditionally on , the random variables are independent. It can be easily shown (see Theorem 5.10 in [33]) that the moment generating function of (copy of ) is given by

| (38) |

Applying Lemma 6.1 in [44], using (38) and Assumption 1, we can derive the following Chernoff-type bounds

| (39) |

where We have

therefore

| (40) |

So, using the weights given by (12) together with (39) and (40), we obtain that the probability of is smaller than This concludes the proof of the first part of Theorem 1.

6.8 Proof of Theorem 2

First, let us note that in the least squares setting, we have for any where , and that , (noise variance) in Equation (2), and , . Theorem 1 provides

for any such that and . Since for all , we have and

| (41) |

for any , where we recall that . Also, recall that and for and . Also, we consider , where is defined, for any , as the minimizer of

over the set of vectors satisfying , and we put for . It is easy to see that the solution is given by

where we recall that . Note in particular that the identifiability assumption entails that . In order to control the bias term, an easy computation gives that, whenever

where we used the fact that is -Lipschitz, so that

Note that where . This entails that . So, using also (41), we end up with

which concludes the proof Theorem 2 using .

References

- [1] A. Agresti. Foundations of Linear and Generalized Linear Models. John Wiley & Sons, 2015.

- [2] M. Z. Alaya, S. Gaïffas, and A. Guilloux. Learning the intensity of time events with change-points. Information Theory, IEEE Transactions on, 61(9):5148–5171, 2015.

- [3] F. Bach. Self-concordant analysis for logistic regression. Electron. J. Statist., 4:384–414, 2010.

- [4] F. Bach, R. Jenatton, J. Mairal, and G. Obozinski. Optimization with sparsity-inducing penalties. Foundations and Trends® in Machine Learning, 4(1):1–106, 2012.

- [5] E. Bacry, M. Bompaire, S. Gaïffas, and S. Poulsen. tick: a Python library for statistical learning, with a particular emphasis on time-dependent modeling. ArXiv e-prints, July 2017.

- [6] P. Baldi, K. Cranmer, T. Faucett, P. Sadowski, and D. Whiteson. Parameterized neural networks for high-energy physics. The European Physical Journal C, 76(5):1–7, Apr 2016.

- [7] P. Baldi, P. Sadowski, and D. Whiteson. Searching for exotic particles in high-energy physics with deep learning. Nature communications, 5, 2014.

- [8] H. H. Bauschke and P. L. Combettes. Convex analysis and monotone operator theory in Hilbert spaces. CMS Books in Mathematics/Ouvrages de Mathématiques de la SMC. Springer, New York, 2011.

- [9] P. J. Bickel, Y. Ritov, and A. B. Tsybakov. Simultaneous analysis of Lasso and Dantzig selector. Ann. Statist., 37(4):1705–1732, 2009.

- [10] J. A. Blackard and D. J. Dean. Comparative accuracies of artificial neural networks and discriminant analysis in predicting forest cover types from cartographic variables. Computers and electronics in agriculture, 24(3):131–151, 1999.

- [11] S. Boyd and L. Vandenberghe. Convex optimization. Cambridge University Press, Cambridge, 2004.

- [12] L. Breiman. Random forests. Mach. Learn., 45(1):5–32, 2001.

- [13] L. Breiman, J. Friedman, R. Olshen, and C. Stone. Classification and Regression Trees. Wadsworth and Brooks, Monterey, CA, 1984.

- [14] P. Bühlmann and S. van De Geer. Statistics for high-dimensional data. Springer Series in Statistics. Springer, Heidelberg, 2011.

- [15] F. Bunea, A. Tsybakov, and M. Wegkamp. Sparsity oracle inequalities for the Lasso. Electron. J. Statist., 1:169–194, 2007.

- [16] E. J. Candès and M. B. Wakin. An Introduction To Compressive Sampling. Signal Processing Magazine, IEEE, 25(2):21–30, 2008.

- [17] E. J. Candès, M. B. Wakin, and S. P. Boyd. Enhancing sparsity by reweighted minimization. Journal of Fourier Analysis and Applications, 14(5):877–905, 2008.

- [18] B. Chlebus and S. H. Nguyen. On finding optimal discretizations for two attributes. In Lech Polkowski and Andrzej Skowron, editors, Rough Sets and Current Trends in Computing, volume 1424 of Lecture Notes in Computer Science, pages 537–544. Springer Berlin Heidelberg, 1998.

- [19] L. Condat. A Direct Algorithm for 1D Total Variation Denoising. IEEE Signal Processing Letters, 20(11):1054–1057, 2013.

- [20] A. S. Dalalyan, M. Hebiri, and J. Lederer. On the prediction performance of the Lasso. Bernoulli, 23(1):552–581, 2017.

- [21] D. L. Donoho and M. Elad. Optimally sparse representation in general (non-orthogonal) dictionaries via minimization. In PROC. NATL ACAD. SCI. USA 100 2197–202, 2002.

- [22] D. L. Donoho and X. Huo. Uncertainty principles and ideal atomic decomposition. Information Theory, IEEE Transactions on, 47(7):2845–2862, 2001.

- [23] J. Friedman, T. Hastie, H. Höfling, and R. Tibshirani. Pathwise coordinate optimization. Ann. Appl. Stat., 1(2):302–332, 2007.

- [24] J. H. Friedman. Stochastic gradient boosting. Computational Statistics & Data Analysis, 38(4):367–378, 2002.

- [25] S. Garcia, J. Luengo, J. A. Saez, V. Lopez, and F. Herrera. A survey of discretization techniques: Taxonomy and empirical analysis in supervised learning. IEEE Transactions on Knowledge and Data Engineering, 25(4):734–750, 2013.

- [26] P. J. Green and B. W. Silverman. Nonparametric regression and generalized linear models: a roughness penalty approach. Chapman and Hall, London, 1994.

- [27] T. Hastie and R. Tibshirani. Generalized additive models. Wiley Online Library, 1990.

- [28] T. Hastie, R. Tibshirani, and J. Friedman. The elements of statistical learning. Springer Series in Statistics. Springer-Verlag, New York, 2001.

- [29] Joel Horowitz, Jussi Klemelä, Enno Mammen, et al. Optimal estimation in additive regression models. Bernoulli, 12(2):271–298, 2006.

- [30] Stéphane Ivanoff, Franck Picard, and Vincent Rivoirard. Adaptive lasso and group-lasso for functional poisson regression. The Journal of Machine Learning Research, 17(1):1903–1948, 2016.

- [31] K. Knight and W. Fu. Asymptotics for Lasso-type estimators. Ann. Statist., 28(5):1356–1378, 2000.

- [32] R. Kohavi. Scaling up the accuracy of naive-Bayes classifiers: A decision-tree hybrid. In KDD, volume 96, pages 202–207, 1996.

- [33] E. L. Lehmann and G. Casella. Theory of point estimation. Springer texts in statistics. Springer, New York, 1998.

- [34] M. Lichman. UCI Machine Learning Repository, 2013.

- [35] H. Liu, F. Hussain, C. L. Tan, and M. Dash. Discretization: an enabling technique. Data Min. Knowl. Discov., 6(4):393–423, 2002.

- [36] G. Lugosi and N. Vayatis. On the Bayes-risk consistency of regularized boosting methods. Annals of Statistics, pages 30–55, 2004.

- [37] L. Meier, S. van De Geer, and P. Bühlmann. The group lasso for logistic regression. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 70(1):53–71, 2008.

- [38] Lukas Meier, Sara Van de Geer, Peter Bühlmann, et al. High-dimensional additive modeling. The Annals of Statistics, 37(6B):3779–3821, 2009.

- [39] S. Moro, P. Cortez, and P. Rita. A data-driven approach to predict the success of bank telemarketing. Decision Support Systems, 62:22–31, 2014.

- [40] F. Pedregosa, G. Varoquaux, A. Gramfort, V. Michel, B. Thirion, O. Grisel, M. Blondel, P. Prettenhofer, R. Weiss, V. Dubourg, J. Vanderplas, A. Passos, D. Cournapeau, M. Brucher, M. Perrot, and E. Duchesnay. Scikit-learn: Machine learning in Python. Journal of Machine Learning Research, 12:2825–2830, 2011.

- [41] J. R. Quinlan. C4.5: Programs for Machine Learning (Morgan Kaufmann Series in Machine Learning). Morgan Kaufmann, 1 edition, 1993.

- [42] F. Rapaport, E. Barillot, and J. P. Vert. Classification of arraycgh data using fused SVM. Bioinformatics, 24(13):i375–i382, 2008.

- [43] Pradeep Ravikumar, John Lafferty, Han Liu, and Larry Wasserman. Sparse additive models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 71(5):1009–1030, 2009.

- [44] P. Rigollet. Kullback Leibler aggregation and misspecified generalized linear models. Ann. Statist., 40(2):639–665, 2012.

- [45] M. A. Russell. Mining the Social Web: Data Mining Facebook, Twitter, LinkedIn, Google+, GitHub, and More. O’Reilly Media, 2013.

- [46] B. Schölkopf and A. J. Smola. Learning with kernels: support vector machines, regularization, optimization, and beyond. MIT press, 2002.

- [47] V. G. Sigillito, S. P. Wing, L. V. Hutton, and K. B. Baker. Classification of radar returns from the ionosphere using neural networks. Johns Hopkins APL Technical Digest, 10(3):262–266, 1989.

- [48] R. Tibshirani. Regression shrinkage and selection via the Lasso. J. Roy. Statist. Soc. Ser. B, 58(1):267–288, 1996.

- [49] R. Tibshirani, M. Saunders, S. Rosset, J. Zhu, and K. Knight. Sparsity and smoothness via the fused Lasso. J. R. Stat. Soc. Ser. B Stat. Methodol., 67(1):91–108, 2005.

- [50] Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society. Series B (Methodological), pages 267–288, 1996.

- [51] S. van de Geer. High-dimensional generalized linear models and the Lasso. Ann. Statist., 36(2):614–645, 2008.

- [52] S. van de Geer and J. Lederer. The Lasso, correlated design, and improved oracle inequalities, volume Volume 9 of Collections, pages 303–316. Institute of Mathematical Statistics, Beachwood, Ohio, USA, 2013.

- [53] J. Wu and S. Coggeshall. Foundations of Predictive Analytics (Chapman & Hall/CRC Data Mining and Knowledge Discovery Series). Chapman & Hall/CRC, 1st edition, 2012.

- [54] I. C. Yeh and C. H. Lien. The comparisons of data mining techniques for the predictive accuracy of probability of default of credit card clients. Expert Systems with Applications, 36(2):2473–2480, 2009.

- [55] Y. L. Yu. On decomposing the proximal map. In C.J.C. Burges, L. Bottou, M. Welling, Z. Ghahramani, and K.Q. Weinberger, editors, Advances in Neural Information Processing Systems 26, pages 91–99. 2013.

- [56] P. Zhao and B. Yu. On model selection consistency of Lasso. J. Mach. Learn. Res., 7:2541–2563, 2006.