Spatio-temporal analysis of regional unemployment rates: A comparison of model based approaches

Abstract

This study aims to analyze the methodologies that can be used to estimate the total number of unemployed, as well as the unemployment rates for 28 regions of Portugal, designated as NUTS III regions, using model based approaches as compared to the direct estimation methods currently employed by INE (National Statistical Institute of Portugal). Model based methods, often known as small area estimation methods (Rao, 2003), "borrow strength" from neighbouring regions and in doing so, aim to compensate for the small sample sizes often observed in these areas. Consequently, it is generally accepted that model based methods tend to produce estimates which have lesser variation. Other benefit in employing model based methods is the possibility of including auxiliary information in the form of variables of interest and latent random structures. This study focuses on the application of Bayesian hierarchical models to the Portuguese Labor Force Survey data from the 1st quarter of 2011 to the 4th quarter of 2013. Three different data modeling strategies are considered and compared: Modeling of the total unemployed through Poisson, Binomial and Negative Binomial models; modeling of rates using a Beta model; and modeling of the three states of the labor market (employed, unemployed and inactive) by a Multinomial model. The implementation of these models is based on the Integrated Nested Laplace Approximation (INLA) approach, except for the Multinomial model which is implemented based on the method of Monte Carlo Markov Chain (MCMC). Finally, a comparison of the performance of these models, as well as the comparison of the results with those obtained by direct estimation methods at NUTS III level are given.

Keywords: Unemployment estimation; Model based methods; Bayesian hierarchical models

1 Introduction

The calculation of official estimates of the labor market that are published quarterly by the INE is based on a direct method from the sample of the Portuguese Labor Force Survey. These estimates are available at national level and NUTS II regions of Portugal. NUTS is the classification of territorial units for statistics (see Appendix for a better understanding). Currently, as established by Eurostat, knowledge of the labor market requires reliable estimates for the total of unemployed people and the unemployment rate at more disaggregated levels, particularly at NUTS III level. However, due to the small size of these areas, there is insufficient information on some of the variables of interest to obtain estimates with acceptable accuracy using the direct method.

In this sense, and because increasing the sample size imposes excessive costs, we intend to study alternative methods with the aim of getting more accurate estimates for these regions. In fact, the accuracy of the estimates obtained in this context is deemed very important since it directly affects the local policy actions.

This issue is part of the small area estimation. Rao (2003) provides a good theoretical introduction to this problem and discusses some estimation techniques based on mixed generalized models. Pfeffermann (2002), Jiang & Lahiri (2006a, 2006b) make a good review of developments to date.

This has been an area in full development and application, especially after the incorporation of spatial and temporal random effects, which brought a major improvement in the estimates produced. Choundry & Rao (1989), Rao & Yu (1994), Singh et al (2005) and Lopez-Vizcaino et al (2015) are responsible for some of these developments. Chambers et al (2016) give alternative semiparametric methods based on M-quantile regression.

Datta & Ghosh (1991) use a Bayesian approach for the estimation in small areas. One advantage of using this approach is the flexibility in modeling different types of variables of interest and different structures in the random effects using the same computational methods.

Recently, there has been considerable developments on space-time Bayesian hierarchical models employed in small area estimation within the context of disease (Best et al, 2005). In this paper, we explore the application of these models and adopt them for the estimation of unemployment in the NUTS III regions, using data from the Portuguese Labor Force Survey from the 1st quarter of 2011 to the 4th quarter of 2013.

We consider three different modeling strategies: the modeling of the total number of unemployed people through the Poisson, Binomial, and Negative Binomial models; modeling the unemployment rate using a Beta model; and the simultaneous modeling of the total of the three categories of the labor market (employment, unemployment and inactivity) using a Multinomial model.

2 The data

The region under study (Portugal Continental) is partitioned into 28 NUTS III regions, indexed by . We did not include the autonomous regions because they coincide with the NUTS II regions for which estimates are already available with acceptable accuracy.

We use the Portuguese Labor Force Survey data from the 1st quarter of 2011 to the 4th quarter of 2013 in order to produce accurate estimates for the labor market indicators in the last quarter. Each quarter is denoted by . We did not use more recent data because there was a change in the sampling design during 2014 and that could affect the temporal analysis.

We are interested in the total unemployed population, and the unemployment rate of the population by NUTS III regions, which is denoted by and . We denote the respective sample values by and . The unemployment rate is given by the ratio of active people who are unemployed, as defined by the European regulation of the Labor Force Survey.

The models developed to make estimation in small areas gain special importance with the inclusion of variables of interest, which we call covariates. In this study, the covariates are divided into 5 groups: population structure, economy, labor market, companies and type of economic activity. Some of these covariates are regional and are static in time whereas others are available per quarter and thus are also of dynamic nature. We will make the distinction and classify these sets of covariates into regional, temporal and spatio-temporal covariates. These selected covariates are as follows:

-

1.

Population structure: a) Proportion of individuals in the sample of the Labor Force Survey that are female and aged between 24 and 34 years (SA6, regional and quarterly); b) Proportion of individuals in the sample of the Labor Force Survey that are female and over 49 years (SA8, regional and quarterly).

-

2.

Economy: a) Gross domestic product per capita (GDP, quarterly).

-

3.

Labor market: a) Proportion of unemployed people registered in the employment centers (IEFP, regional and quarterly).

-

4.

Companies: a) Number of enterprises per 100 inhabitants (regional).

-

5.

Type of economic activity: a) Proportion of population employed in the primary sector of activity (regional); b) Proportion of population employed in the secondary sector of activity (regional).

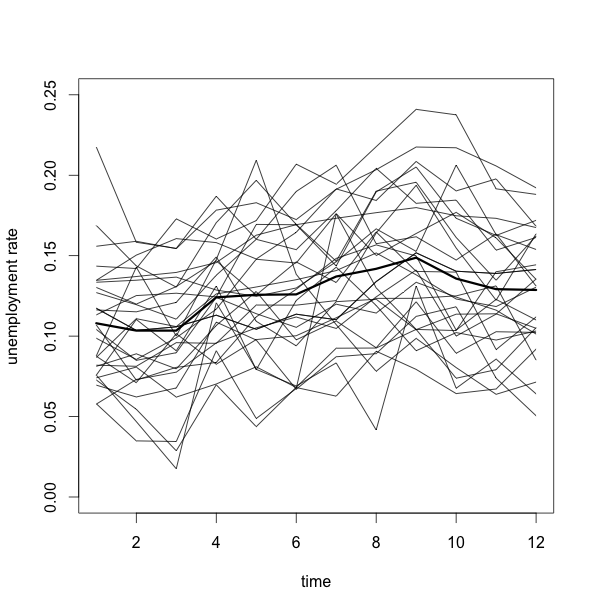

Figure 1 shows the evolution of the unemployment rate observed in the sample from the Portuguese Labor Force Survey from the 1st quarter of 2011 to the 4th quarter of 2013 in each of the 28 NUTS III . The bold represents the average unemployment rate. We can see that for all regions there was a slight increase in the unemployment rate during this period.

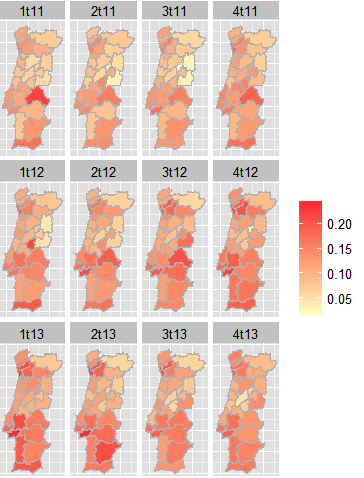

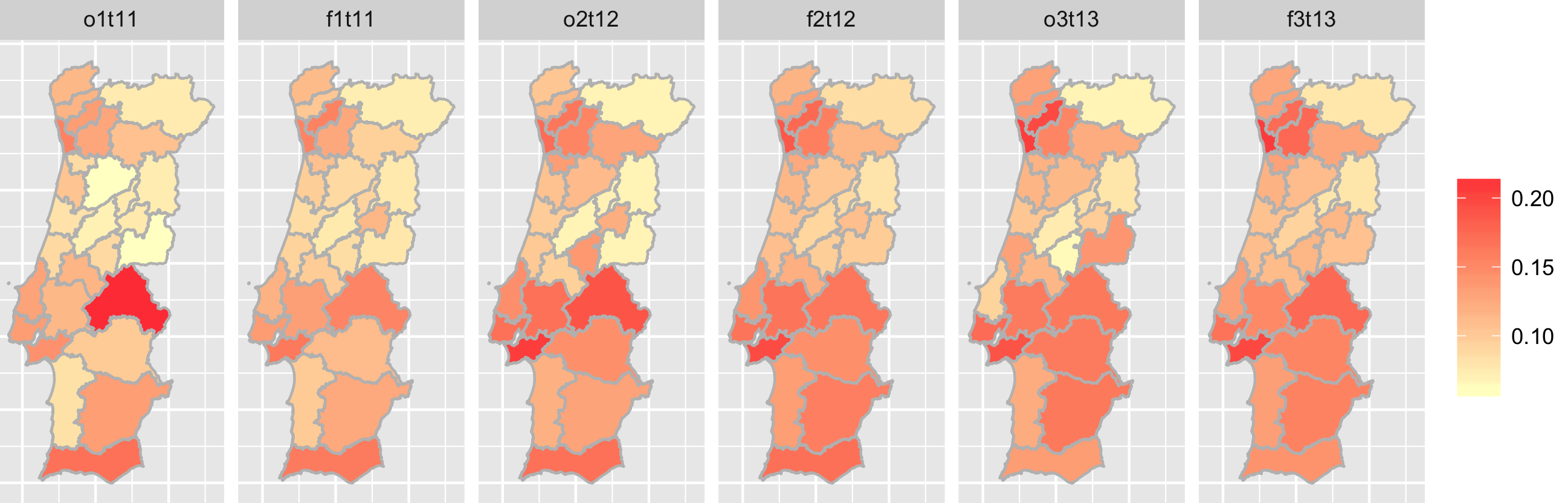

The map in Figure 2 shows the spatial and temporal distribution of the unemployment rate observed in the sample of Portuguese Labor Force Survey during the period under study. As we can see, this map suggests the existence of spatial and temporal dependence structures in the observed data.

3 Bayesian models for counts and proportions

In this problem we are interested in estimating the effect of selected variables on the number of unemployed individuals and the unemployment rate, taking into account the temporal and spatial correlations.

One of the most general and useful ways of specifiying this problem is to employ hierarchical generalized linear model set up, in which the data are linked to covariates and spatial-temporal random effects through an appropriately chosen likelihood and a link function which is linear on the covariates and the random effects.

We denote the vector of designated regional covariates by , the temporal covariates by and the vector of spatio-temporal covariates by .

While modeling unemployment numbers, we generically assume that

where is a generic probability mass function. We look at this model considering specific probability mass functions, such as Poisson and Binomial, among others. The state parameters depend on covariates and on structured and unstructured random factors through appropriate link functions.

The unemployment rate is also hierarchically modeled in a similar way. We assume that

where is a properly chosen probability density function and are the state parameters.

In the following sections we look at different variations of these hierarchical structures with different link functions.

Let us consider , the chosen link function which depends on the assumed model for the data. We assume for the modeling of the total and for the modeling of the rates. For each model, we consider the following linear predictor

| (1) |

where are constants that can be included in the linear predictor during adjustment. The vectors , and correspond respectively to vectors of the covariates coefficients , and . Components represent unstructured random effects, which assume

and the components represent the structured random effects that can be written as where is modeled as a intrinsic conditional autoregressive (ICAR) process proposed by Besag et al (1991) and is modeled as a first order random walk (AR (1)). Blangiardo et al (2013) succinctly describe both the ICAR and AR (1) processes.

We assume the following prior distributions for the regression parameters

For the hyperparameters we assume

We assume the following models for the distribution of the observed data: Poisson, Binomial, and Negative Binomial for the total of unemployed, Beta for the unemployment rate and Multinomial for the total of the three states of the labor market (employment, unemployment and inactivity).

3.1 Poisson model

This is perhaps the most frequently used model for counting data in small areas, especially in epidemiology. If we consider that is the mean of the total number of unemployed people, we can assume that

Therefore

In this case, the link function is the logarithmic function (log = ). The NUTS III regions have different sample dimensions, so the variation of the total unemployment is affected. To remove this effect, we need to add an term, which is given by the number of individuals in the sample in each NUTS III region.

3.2 Negative Binomial model

The Negative Binomial model may be used as an alternative to the Poisson model, especially when the sample variance is much higher than the sample mean. When this happens, we say that there is over-dispersion in the data. In this case, we can assume that

The probability mass function is given by

where is the gamma function.

The most convenient way to connect to the linear predictor is through the . Also in this case, the term described in the Poisson model is considered.

3.3 Binomial model

When measuring the total unemployed, we may also consider that there is a finite population in the area j. In this case, we assume that this population is the number of active individuals in the area j, which is denoted by , assuming that it is fixed and known. We can then consider a Binomial model for the total number of unemployed given the observed active population. So, given the population unemployment rate ,

which means that

In this case, the most usual link function is the logit function given by .

We expect that the fit of this model will be close to the fit of the Poisson model in the regions with a big number of active people and a small unemployment rate.

3.4 Beta model

The Beta distribution is one of the most commonly used model for rates and proportions. We can assume that the unemployment rate follows a Beta distribution and using the parameterization proposed by Ferrari and Cribari-Neto (2004), we denote by

The probability mass function is given by

where and .

In this case, there are several possible choices for the link function, but the most common is the logit function .

3.5 Multinomial model

The Multinomial logistic regression model is an extension of the Binomial logistic regression model and is used when the variable of interest is multi-category. In this case, it may interest us to model the three categories of the labor market (employment, unemployment and inactivity), giving us the unemployment rate which can be expressed by the ratio between the unemployed and the active people (the sum of the unemployed and employed).

One advantage of the Multinomial model in this problem is the consistency obtained between the three categories of the labor market. The estimated total employment, unemployment and inactivity coincides with the total population. In addition, the same model provides estimates for the rate of employment, unemployment and inactivity.

Assuming that is the vector of the total in the three categories of the labor market, the Multinomial model can be written as

where is the number of individuals in the area j and quarter t, and is the vector of proportions of employed, unemployed and inactive, where .

The probability mass function is given by

where

The most common link function is the log of , defined as , .

4 Application to the Portuguese Labor Force Survey data

4.1 Results

This section provides the results of applying five models for the estimation of the total unemployed and unemployment rate to the NUTS III regions of Portugal.

The Poisson, Binomial, Negative Binomial and Beta models were implemented using the R package R-INLA, while the Multinomial model was implemented based on MCMC methods using the R package R2OpenBUGS.

When the Multinomial regression model was combined with the predictor given in (1), some convergence problems arose, due to its complexity. For this reason, the effects and were replaced by the unstructured area and time effects and , where it was assumed

with the following prior information

Due to the differences in the model structure and the computational methods used for the Multinomial model, the comparative analysis of results for this model should be done with some extra care.

The posterior mean of the parameters and hyperparameters of each model as well as the standard deviation and the quantile 2.5 % and 97.5 % are presented in Tables 1, 2, 3, 4 and 5. We can see that the covariates GDP and secondary sector are not significant for any of the models applied. However, the value obtained for Deviance Information Criterion (DIC) increases considerably without the inclusion of these variables, so we decided to include them.

We observe that the IEFP is significant in all of the models applied, as expected. The number of enterprises per 100 000 inhabitants has a negative effect on the increase of unemployment. The population structure has also a significant effect. The proportion of individuals that are female and aged between 24 and 34 years has a positive effect on the increase of unemployment. On the other hand, the proportion of individuals that are female and over 49 years has a negative effect. These tendencies are probably due to young unemployment in the first case and to the fact that the age group +49 includes most of the inactive people, in the second case.

| Poisson | ||||

| Mean | SD | 2.5Q | 97.5Q | |

| (Intercept) | -2,83 | 0,01 | -2,85 | -2,81 |

| Companies | -0,01 | 0,02 | -0,05 | 0,02 |

| Primary sector | -0,02 | 0,72 | -1,45 | 1,40 |

| Secondary sector | 0,02 | 0,21 | -0,39 | 0,43 |

| GDP | 0,00 | 0,00 | 0,00 | 0,00 |

| IEFP | 10,05 | 0,96 | 8,17 | 11,93 |

| SA6 | 4,30 | 1,34 | 1,65 | 6,93 |

| SA8 | -1,55 | 0,57 | -2,65 | -0,42 |

| 25047,76 | 20819,39 | 3297,22 | 79744,21 | |

| 25,77 | 9,52 | 11,91 | 48,78 | |

| 22082,79 | 19692,19 | 2213,88 | 73957,91 | |

| Negative Binomial | ||||

| Mean | SD | 2.5Q | 97.5Q | |

| (Intercept) | -2,83 | 0,01 | -2,86 | -2,81 |

| Companies | -0,01 | 0,02 | -0,05 | 0,02 |

| Primary sector | 0,13 | 0,73 | -1,33 | 1,57 |

| Secondary sector | -0,04 | 0,23 | -0,48 | 0,41 |

| GDP | 0,00 | 0,00 | 0,00 | 0,00 |

| IEFP | 10,20 | 1,48 | 7,28 | 13,09 |

| SA6 | 3,97 | 2,01 | 0,02 | 7,91 |

| SA8 | -2,11 | 0,73 | -3,54 | -0,67 |

| 48,57 | 5,44 | 38,69 | 60,05 | |

| 22946,14 | 20085,32 | 2453,14 | 75579,11 | |

| 32,77 | 14,26 | 13,08 | 68,00 | |

| 22641,11 | 19924,30 | 2405,53 | 74957,89 | |

| Binomial | ||||

| Mean | SD | 2.5Q | 97.5Q | |

| (Intercept) | -1,97 | 0,01 | -2,00 | -1,95 |

| Companies | -0,04 | 0,02 | -0,07 | 0,00 |

| Primary sector | 0,54 | 1,01 | -1,47 | 2,52 |

| Secondary sector | -0,11 | 0,28 | -0,67 | 0,45 |

| GDP | 0,00 | 0,00 | 0,00 | 0,00 |

| IEFP | 12,63 | 1,11 | 10,47 | 14,81 |

| SA6 | 4,38 | 1,47 | 1,50 | 7,26 |

| SA8 | -1,11 | 0,64 | -2,37 | 0,16 |

| 20736,79 | 19243,68 | 2070,46 | 71553,26 | |

| 11,77 | 3,90 | 5,70 | 20,85 | |

| 19143,06 | 18555,71 | 1460,60 | 68268,97 | |

| Beta | ||||

| Mean | SD | 2.5Q | 97.5Q | |

| (Intercept) | -1,98 | 0,01 | -2,00 | -1,95 |

| Companies | -0,03 | 0,03 | -0,08 | 0,02 |

| Primary sector | 0,69 | 1,09 | -1,50 | 2,83 |

| Secondary sector | -0,20 | 0,31 | -0,82 | 0,42 |

| GDP | 0,00 | 0,00 | 0,00 | 0,00 |

| IEFP | 12,22 | 1,82 | 8,64 | 15,78 |

| SA6 | 0,85 | 1,84 | -2,77 | 4,47 |

| SA8 | -2,37 | 0,68 | -3,70 | -1,03 |

| 206,61 | 16,80 | 174,43 | 240,37 | |

| 20012,58 | 19075,29 | 1750,73 | 70491,89 | |

| 11,33 | 4,61 | 5,40 | 23,02 | |

| 20497,48 | 19404,83 | 1715,97 | 71768,00 | |

| Multinomial | ||||

| Mean | SD | 2.5Q | 97.5Q | |

| (Intercpet) | -1,74 | 0,26 | -2,16 | -1,20 |

| Companies | 0,01 | 0,02 | -0,04 | 0,05 |

| Primary sector | 3,99 | 5,38 | -1,04 | 14,94 |

| Secondary sector | -0,77 | 0,77 | -2,27 | 0,19 |

| GDP | 0,00 | 0,00 | 0,00 | 0,00 |

| IEFP | 8,93 | 1,59 | 6,02 | 12,00 |

| SA6 | 4,77 | 1,44 | 1,97 | 7,58 |

| SA8 | -2,38 | 0,64 | -3,74 | -1,22 |

| 2206,25 | 2979,60 | 3,32 | 9519,00 | |

| 33,57 | 24,87 | 1,77 | 78,11 | |

All the considered models give very good fit to the data and their temporal predictions are also satisfactory. Here we report on several model fitting aspects of the Binomial model. Similar results for the other models are given in the Supplementary Material.

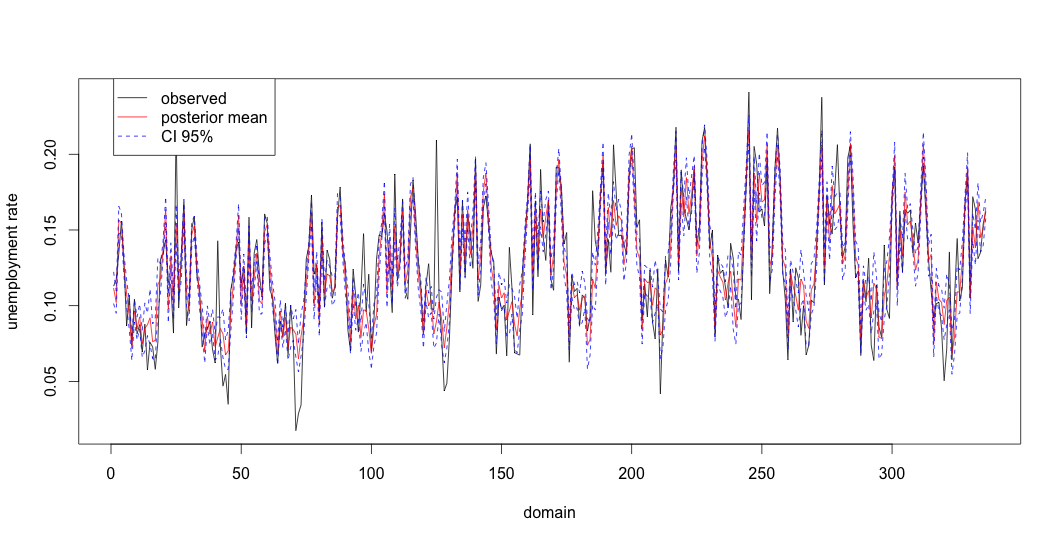

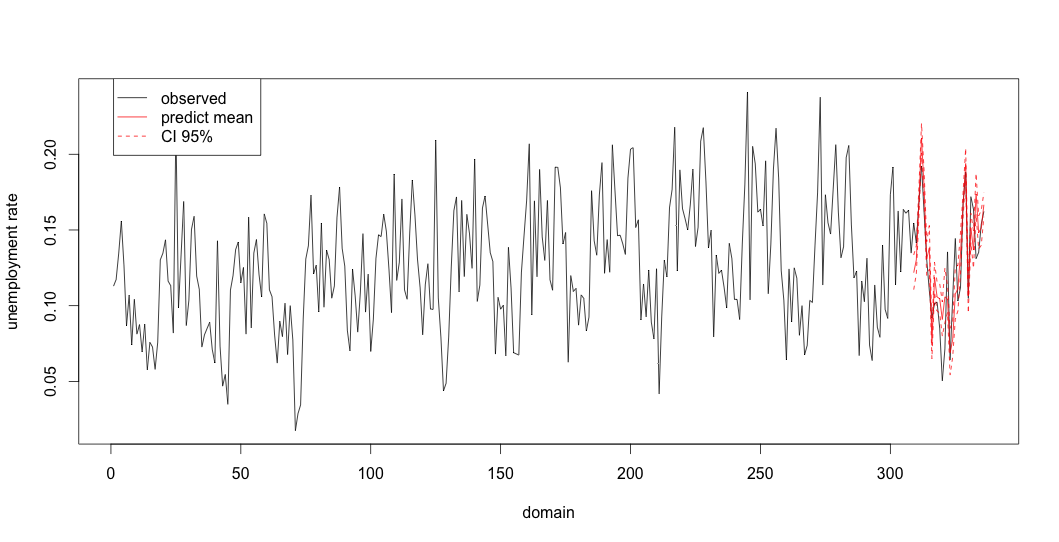

Figure 3 a) gives the observed and adjusted values from the Binomial model together with their 95% credible intervals, whereas figure 3 b) gives the predictions to the 4th quarter of 2013 together with their 95% credible intervals. We see that the adjusted values are very close to the observed ones. The domains are sorted at first by quarter and then by region. This is the reason for the identical behavior in each 28 domains (corresponding to the NUTS III regions). The graphs show a slight increase on the unemployment rate until the 1st quarter of 2013 and then a decrease until the 4th quarter of 2013.

The map of the figure 4 allows for a better understanding of the regional difference between the observed and fitted values.

4.2 Diagnosis

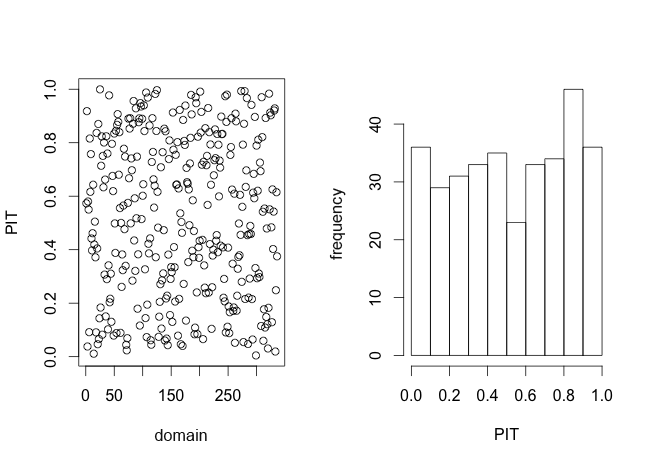

Some predictive measures can be used for an informal diagnostic, such as Conditional Predictive ordinates (CPO) and Probability Integral Transforms (PIT; Gelman et al, 2004). Measure is defined as where is the vector without observation , while the measures are obtained by . Unusually large or small values of this measure indicate possible outliers. Moreover, a histogram of the PIT value which is very different from the uniform distribution indicates that the model is questionable.

The implementation of these measures in an MCMC approach is very heavy and requires a high computational time. For this reason, we present only results for the models implemented with the INLA.

Figure 5 shows the graphs of the PIT values versus domain ( 336) and the histogram of the PIT values for Poisson, Binomial, Negative Binomial and Beta models. We see that the histogram for the PIT values based on the Poisson and Binomial models presents a fairly uniform behavior, but this is not the case with the Negative Binomial and Beta distributions. This suggests that these last two models may not be suitable for data in analysis.

The predictive quality of the models can be performed using a cross-validated logarithmic score given by the symmetric of the mean of the logarithm of CPO values (Martino and Rue, 2010). High CPO values indicate a better quality of prediction of the respective model. The logarithmic of the CPO values are given in table 6. Accordingly, the Beta model has the least predictive quality.

The diagnosis of the Multinomial model was based on graphical visualization and on Potential Scale Reduction Factor (Brooks and Gelman, 1997). No convergence problems were detected.

| log score | |

|---|---|

| Poisson | 3.33 |

| Negative Binomial | 3.51 |

| Binomial | 3.34 |

| Beta | -2.39 |

4.3 Comparison

In order to compare the studied models, we use the Deviance Information Criterion () proposed by Spiegehalter et al (2002). This is a criterion which aims to achieve a balance between the adequacy of a model and its complexity. It is defined by where is the posterior mean deviance of the model and is the effective number of parameters. The model with the smallest value of DIC is the one with a better balance between the model adjustment and complexity.

The values of , and are presented in table 7. The Multinomial model features a higher DIC value, but it should be noted that this model requires an adjustment of the total of employed, unemployed and inactive people, unlike the other models.

Among the models used for modeling of total, the Poisson model is the one with the lower value of DIC, which would suggest that it should be preferable to the Negative Binomial model. However, Geedipally et al (2013) explains that the value of this measure is affected by the parameterization of the model, which may influence the values obtained by the Negative Binomial and Beta models, since the software used permits different parameterizations in these cases.

| Poisson | 2240.4 | 30.4 | 2210.0 |

|---|---|---|---|

| Negative Binomial | 2374.9 | 25.4 | 2349.5 |

| Binomial | 2241.4 | 32.5 | 2208.9 |

| Beta | -1607.4 | 31.1 | -1638.4 |

| Multinomial | 4976.0 | 81.5 | 4894.5 |

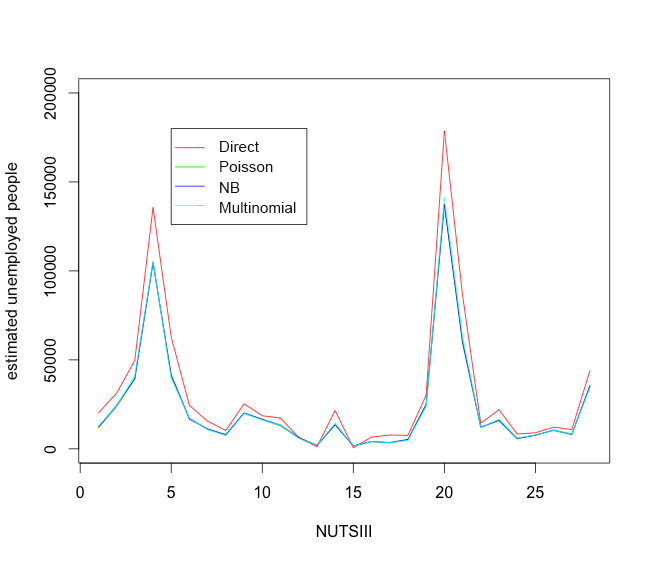

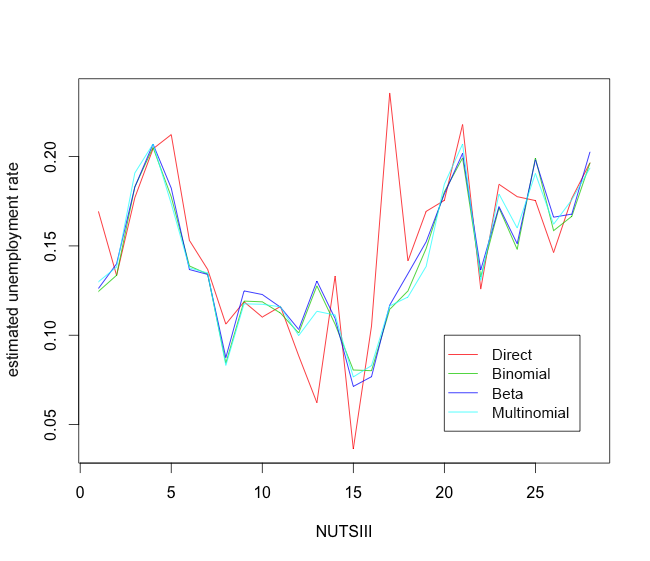

Figure 6 shows that the Poisson, Negative Binomial and Multinomial models produced very similar estimates for the total unemployed, while Binomial, Beta and Multinomial models produced similar estimates for unemployment rate. We can also note that these estimates are smoother than the estimates obtained by the direct method. This property is prominently displayed in the estimation of the unemployment rate, and justifies the fact that the estimates of the total produced by the models are lower than the estimates produced by the direct method for large values of unemployment, and higher for small values (regions 13 and 15).

Regions 4 and 20, which correspond to Grande Porto and Grande Lisboa, are those with the highest population size. This fact explains the high values of unemployment totals. On the other hand, regions 13 and 15, which correspond to Pinhal Interior Sul and Serra da Estrela, are those with the lowest population size. It is interesting to observe that the regions with the greatest difference between the unemployment rate estimated by the direct method and the rate estimated by the studied models are those with the lowest population sizes (Pinhal Interior Sul, Serra da Estrela and Beira Interior Sul), which are represented in the graph by the numbers 13, 15 and 17.

The Relative Root Mean Square Error (RRMSE) allows for a comparison of the models studied and the direct method. A lower value of RRMSE indicates a better balance between variability and bias. The graph of Figure 7 reveals a wide discrepancy between the direct method and the applied models.

Note that, for most models, the NUTS III region 15, which corresponds to Serra da Estrela (see Appendix), presents the highest value RRMSE. This result can be explained in part by the reduced population size of the region. The opposite is true for regions with high dimensional population such as Porto (Region 4), Grande Lisboa (region 20) and Algarve (region 28).

The high values of RRMSE of unemployment rate estimates by the direct method for regions 13, 15 and 17, can explain the big differences found between the methods in these regions (figure 10 b). These results reinforce the idea that the direct method is inadequate for the estimation in small areas. On the other hand, the models studied show a maximum value of RRMSE of the unemployment rate estimates that corresponds to almost half of the value obtained by the direct method.

5 Discussion

We studied the application of five spatio-temporal models within a bayesian approach for the estimation of both the total and the rate of unemployment of NUTS III regions. We realized that one of the features of model based methods is the smoothing of the variation across time and space. This feature brings these models closer to reality.

The estimates obtained by these models were reasonable when compared with the direct method, which presented higher values of RRMSE.

Models under study presented much lower values of RRMSE than the direct method for regions with a small population size. This feature shows that these models can be a good alternative to small area estimation and in particular for the NUTS III regions of Portugal.

The Negative Binomial and Beta models presented diagnostic problems in the analysis of empirical distribution of the PIT. A non uniform distribution of the PIT revealed that the predictive distribution is not coherent with the data.

Among the models under study, the Multinomial model seems to be the most suitable for this problem. The estimates obtained for the unemployment totals are similar to those obtained by the other models, but they produce estimates for the total of employed as well as inactive people simultaneously, in a way that is consistent with the population estimates. In this way, we can directly obtain the estimates of the employment and unemployment rates.

Acknowledgements

This work was supported by the project UID/MAT/00006/2013 and the PhD scholarship SFRH/BD/92728/2013 from Funda o para a Ci ncia e Tecnologia. Instituto Nacional de Estat stica and Centro de Estat stica e Aplica es da Universidade de Lisboa are the reception institutions. We would like to thank professor Ant nia Turkman for her help.

Note

This study is the responsibility of the authors and does not reflect the official opinions of Instituto Nacional de Estat stica.

Appendix

| NUTS III region | |||

|---|---|---|---|

| Code | Designation | NUTS II region | |

| 1 | 111 | Minho-Lima | Norte |

| 2 | 112 | C vado | |

| 3 | 113 | Ave | |

| 4 | 114 | Grande Porto | |

| 5 | 115 | T mega | |

| 6 | 116 | Entre Douro e Vouga | |

| 7 | 117 | Douro | |

| 8 | 118 | Alto Tr s-os-Montes | |

| 9 | 161 | Baixo Vouga | Centro |

| 10 | 162 | Baixo Mondego | |

| 11 | 163 | Pinhal Litoral | |

| 12 | 164 | Pinhal Interior Norte | |

| 13 | 166 | Pinhal Interior Sul | |

| 14 | 165 | D o-Laf es | |

| 15 | 167 | Serra da Estrela | |

| 16 | 168 | Beira Interior Norte | |

| 17 | 169 | Beira Interior Sul | |

| 18 | 16A | Cova da Beira | |

| 19 | 16B | Oeste | |

| 20 | 171 | Grande Lisboa | Lisboa |

| 21 | 172 | Pen nsula de Set bal | |

| 22 | 16C | M dio Tejo | Centro |

| 23 | 185 | Lez ria do Tejo | Alentejo |

| 24 | 181 | Alentejo Litoral | |

| 25 | 182 | Alto Alentejo | |

| 26 | 183 | Alentejo Central | |

| 27 | 184 | Baixo Alentejo | |

| 28 | 150 | Algarve | Algarve |

References

- [1] Besag J, York J, Mollie A. (1991) Bayesian image restoration, with two applications in spatial statistics. Ann Inst Stat Math, 43, 1-59.

- [2] Best N, Richardson S, Thomson A. (2005) A comparison of Bayesian spatial models for disease mapping. Statistical Methods in Medical Research,14, 35-59.

- [3] Blangiardo, M., Cameletti, M., Baio, G., Rue, H. (2013) Spatial and spatio-temporal models with R-INLA, Spatial and Spatio-temporal Epidemiology, 7, 39-55.

- [4] Brooks, S. P. and Gelman, A. (1997) General Methods for Monitoring Convergence of Iterative Simulations. Journal of Computational and Graphical Statistics, 7, 434-455.

- [5] Chambers,R., Salvati,N. and Tzavidis,N.(2016) Semiparametric small area estimation for binary outcomes with application to unemployment estimation for local authorities in the UK. J.R. Statisti. Soc. A 179 pp. 453-479.

- [6] Choundry, G. H., Rao, J.N.K. (1989) Small area estimation using models that combine time series and cross sectional data, Journal of Statistics Canada Symposium on Analysis of Data in Time, 67-74.

- [7] Datta, G. S. and Ghosh, M. (1991) Bayesian prediction in linear models: application to small area estimation. Ann. Statist., 19, 1748-1770.

- [8] Ferrari, S., Cribari-Neto, F. (2004) Beta Regression for Modelling Rates and Proportions. Journal of Applied Statistics, 31(7), 799-815.

- [9] Geedipally, S.R., Lord, D., Dhavala, S.S., (2014) A caution about using deviance information criterion while modeling traffic crashes. Safety Science 62, 495-498.

- [10] Gelman, A., Carlin, J., Stern, H., and Rubin, D. (2004) Bayesian Data Analysis, Second Edition, London. Chapman and Hall.

- [11] Jiang, J. and Lahiri, P. (2006a) Estimation of finite population domain means: A model-assisted empirical best prediction approach. J. Amer. Statist. Assoc. 101, 301-311.

- [12] Jiang, J. and Lahiri, P. (2006b) Mixed model prediction and small area estimation. Test 15, 1-96.

- [13] Lopez-Vizcaino, E., Lombardia, M. J., Morales, D. (2015) Small area estimation of labour force indicators under a multinomial model with correlated time and area effects, J. R. Statist. Soc. A.

- [14] Martino S. and Rue H. (2010) Case Studies in Bayesian Computation using INLA (2010) to appear in Complex data modeling and computationally intensive statistical methods (R-code).

- [15] Pfeffermann, D. (2002) Small area estimation: new developments and directions, Int. Statist. Rev., 70, 125-143.

- [16] Rao, J.N.K. (2003) Small area estimation, Wiley.

- [17] Rao, J. N. K., Yu, M. (1994) Small area estimation by combining time series and cross sectional data, Canadian Journal of Statistics, 22, 511-528.

- [18] Singh, B., Shukla, G., Kundu, D. (2005) Spatio-temporal models in small area estimation, Survey Methodology 31, 183-195.

- [19] Spiegelhalter, D., Best, N., Bradley, P., van der Linde, A. (2002) Bayesian measure of model complexity and fit (with discussion), Journal of the Royal Statistical Society, Series B, 64,4, 583-639.