The phase transition in

bounded-size Achlioptas processes

Abstract

Perhaps the best understood phase transition is that in the component structure of the uniform random graph process introduced by Erdős and Rényi around 1960. Since the model is so fundamental, it is very interesting to know which features of this phase transition are specific to the model, and which are ‘universal’, at least within some larger class of processes (a ‘universality class’). Achlioptas process, a class of variants of the Erdős–Rényi process that are easy to define but difficult to analyze, have been extensively studied from this point of view. Here, settling a number of conjectures and open problems, we show that all ‘bounded-size’ Achlioptas processes share (in a strong sense) all the key features of the Erdős–Rényi phase transition. We do not expect this to hold for Achlioptas processes in general.

1 Introduction

1.1 Summary

In this paper we study the percolation phase transition in Achlioptas processes, which have become a key example for random graph processes with dependencies between the edges. Starting with an empty graph on vertices, in each step two potential edges are chosen uniformly at random. One of these two edges is then added to the evolving graph according to some rule, where the choice may only depend on the sizes of the components containing the four endvertices.111Here we are describing Achlioptas processes with ‘size rules’. This is by far the most natural and most studied type of Achlioptas process, but occasionally more general rules are considered. For the widely studied class of bounded-size rules (where all component sizes larger than some constant are treated the same), the location and existence of the percolation phase transition is nowadays well-understood. However, despite many partial results during the last decade (see, e.g., [10, 56, 32, 35, 7, 48, 6, 5, 21]), our understanding of the finer details of the phase transition has remained incomplete, in particular concerning the size of the largest component.

Our main results resolve the finite-size scaling behaviour of percolation in all bounded-size Achlioptas processes. We show that for any such rule the phase transition is qualitatively the same as that of the classical Erdős–Rényi random graph process in a very precise sense: the width of the ‘critical window’ (or ‘scaling window’) is the same, and so is the asymptotic behaviour of the size of the largest component above and below this window, as well as the tail behaviour of the component size distribution throughout the phase transition. In particular, when as but , we show that, with probability tending to as , the size of the largest component after steps satisfies

where are rule-dependent constants (in the Erdős–Rényi case we have and ). These and our related results for the component size distribution settle a number of conjectures and open problems from [55, 32, 19, 35, 6, 21]. In the language of mathematical physics, they establish that all bounded-size Achlioptas processes fall in the same ‘universality class’ (we do not expect this to be true for general Achlioptas processes). Such strong results (which fully identify the phase transition of the largest component and the critical window) are known for very few random graph models.

Our proof deals with the edge–dependencies present in bounded-size Achlioptas processes via a mixture of combinatorial multi-round exposure arguments, the differential equation method, PDE theory, and coupling arguments. This eventually enables us to analyze the phase transition via branching process arguments.

1.2 Background and outline results

In the last 15 years or so there has been a great deal of interest in studying evolving network models, i.e., random graphs in which edges (and perhaps also vertices) are randomly added step-by-step, rather than generated in a single round. Although the original motivation, especially for the Barabási–Albert model [4], was more realistic modelling of networks in the real world, by now evolving models are studied in their own right as mathematical objects, in particular to see how they differ from static models. Many properties of these models have been studied, starting with the degree distribution. In many cases one of the most interesting features is a phase transition where a ‘giant’ (linear-sized) component emerges as a density parameter increases beyond a critical value.

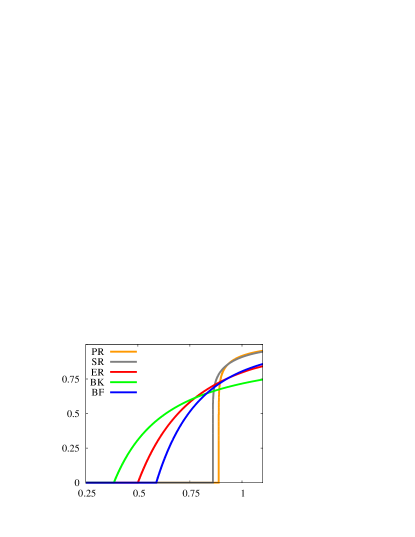

One family of evolving random-graph models that has attracted a great deal of interdisciplinary interest (see, e.g., [1, 20, 47, 26, 9, 56, 48, 5]) is that of Achlioptas processes, proposed by Dimitris Achlioptas at a Fields Institute workshop in 2000. These ‘power of two choices’ variants of the Erdős–Rényi random graph process can be described as follows. Starting with an empty graph on vertices and no edges, in each step two potential edges are chosen uniformly at random from all possible edges (or from those not already present). One of these edges is selected according to some ‘decision rule’ and added to the evolving graph. Note that the distribution of the graph after steps depends on the rule used, and that always adding gives the classical Erdős–Rényi random graph process (exactly or approximately, depending on the precise definitions). Figure 1 gives a crude picture of the phase transition for a range of rules. In general, the study of Achlioptas processes is complicated by the fact that there are non-trivial dependencies between the choices in different rounds. Indeed, this makes the major tools and techniques for studying the phase transition unavailable (such as tree-counting [23, 11, 38, 13], branching processes [37, 14, 15, 17], or random walks [2, 40, 42, 16]), since these crucially exploit independence.

The non-standard features of Achlioptas processes have made them an important testbed for developing new robust methods in the context of random graphs with dependencies, and for gaining a deeper understanding of the phase transition phenomenon. Here the class of bounded-size rules has received considerable attention (see, e.g, [10, 56, 32, 35, 7, 48, 6, 5, 21]): the decision of these rules is based only on the sizes of the components containing the endvertices of the two potential edges and , with the restriction that all component sizes larger than some given cut-off are treated in the same way (i.e., the rule only ‘sees’ the truncated sizes ). Perhaps the simplest example is the Bohman–Frieze process (BF), the bounded-size rule with cut-off in which the edge is added if and only if (see, e.g., [9, 32, 35]). Figure 1 suggests that while the BF rule delays percolation compared to the classical Erdős–Rényi random graph process (ER), it leaves the essential nature of the phase transition unchanged. In this paper we make this rigorous for all bounded-size rules, by showing that these exhibit Erdős–Rényi-like behaviour (see Theorem 1.1). Although very few rigorous results are known for rules which are not bounded-size (see [50, 51]), as suggested in Figure 1 these seem to have very different behaviour in general.

The study of bounded-size Achlioptas processes is guided by the typical questions from percolation theory (and random graph theory). Indeed, given any new model, the first question one asks is whether there is a phase transition in the component structure, and where it is located. This was answered in a pioneering paper by Spencer and Wormald [56] (and for a large subclass by Bohman and Kravitz [10]) using a blend of combinatorics, differential equations and probabilistic arguments. They showed that for any bounded-size rule there is a rule-dependent critical time at which the phase transition happens, i.e., at which the largest component goes from being of order to order . More precisely, writing, as usual, for the number of vertices in the th largest component of a graph , Spencer and Wormald showed that for any fixed , whp (with high probability, i.e., with probability tending to as ) we have222Here and throughout we ignore the irrelevant rounding to integers in the number of edges, writing for .

| (1.1) |

where is given by the blowup point of a certain finite system of differential equations (in the Erdős–Rényi process (1.1) holds with , see also Remark 2.1). Let denote the number of vertices of which are in components of size , and let

| (1.2) |

where the first sum is over all components of and is the number of vertices in . Thus is the th moment of the size of the component containing a randomly chosen vertex. The susceptibility is of particular interest since in many classical percolation models its analogue diverges precisely at the critical point. Spencer and Wormald [56] showed that this holds also for bounded-size Achlioptas processes: the limit of diverges at the critical time .

Once the existence and location of the phase transition have been established, one typically asks about finer details of the phase transition, in particular about the size of the largest component. For the Bohman–Frieze process this was addressed in an influential paper by Janson and Spencer [32], using a mix of coupling arguments, the theory of inhomogeneous random graphs, and asymptotic analysis of differential equations. They showed that there is a constant such that we whp have linear growth of the form

| (1.3) |

as , which resembles the Erdős–Rényi behaviour (where and ). Using work of the present authors [48] and PDE theory, this was extended to certain BF-like rules by Drmota, Kang and Panagiotou [21], but the general case remained open until now. Regarding the asymptotics in (1.3), note that is held fixed as ; only after taking the limit in do we allow .

The next questions one typically asks concern the ‘finite-size scaling’, i.e., behaviour as a function of , usually with a focus on the size of the largest component as at various rates. For the ‘critical window’ (with ) of bounded-size rules this was resolved by Bhamidi, Budhiraja and Wang [7, 6], using coupling arguments, Aldous’ multiplicative coalescent, and inhomogeneous random graph theory. However, the size of the largest component outside this window has surprisingly remained open, despite considerable attention. For example, two papers [5, 54] were solely devoted to the study of in the usually easier subcritical phase ( with ), but both obtained suboptimal upper bounds (a similar remark applies to the susceptibility, see [6]). In contrast, there is no rigorous work about in the more interesting weakly supercritical phase ( with but ), making the size of the largest component perhaps the most important open problem in the context of bounded-size rules.

Of course, there are many further questions that one can ask about the phase transition, and here one central theme is: how similar are Achlioptas processes to the Erdős–Rényi reference model? For example, concerning vertices in ‘small’ components of size , tree counting shows that in the latter model we have

| (1.4) |

as and (ignoring technicalities), where . Due to the dependencies between the edges explicit formulae are not available for bounded-size rules, which motivates the development of new robust methods that recover the tree-like Erdős–Rényi asymptotics in such more complicated settings. Here Kang, Perkins and Spencer [35] presented an interesting PDE-based argument for the Bohman–Frieze process, but this contains an error (see their erratum [36]) which does not seem to be fixable. Subsequently, partial results have been proved by Drmota, Kang and Panagiotou [21] for a restricted class of BF-like rules.

In this paper we answer the percolation questions discussed above for all bounded-size Achlioptas processes, settling a number of open problems and conjectures concerning the phase transition. We first present a simplified version of our main results, writing , and to avoid clutter. In a nutshell, (1.5)–(1.9) of Theorem 1.1 determine the finite-size scaling behaviour of the largest component, the susceptibility and the small components. Informally speaking, all these key statistics have, up to rule-specific constants, the same asymptotic behaviour as in the Erdős–Rényi process, including the same ‘critical exponents’ (in ER we have , , , and , see also Remark 2.1). In particular, (1.7)–(1.8) show that the unique ‘giant component’ initially grows at a linear rate, as illustrated by Figure 1.

Theorem 1.1.

Let be a bounded-size rule with critical time as in (1.1). There are rule-dependent positive constants and such that the following holds for any satisfying and as .

-

1.

(Subcritical phase) For any fixed and , whp we have

(1.5) (1.6) -

2.

(Supercritical phase) Whp we have

(1.7) (1.8) -

3.

(Small components) Suppose that and satisfy , , and . Then whp we have

(1.9) (Here we do not assume that .)

In each case, what we actually prove is stronger (e.g., relaxing to ); see Section 2. To the best of our knowledge, analogous precise results, giving sharp estimates for the size of the largest component in the entire sub- and super-critical phases (see also Remark 1.3), are known only for the Erdős–Rényi model [11, 38], random regular graphs [41], the configuration model [46], and the (supercritical) hypercube [24].

Remark 1.2 (Notation).

Here and throughout we use the following standard notation for probabilistic asymptotics, where is a sequence of random variables and a function. ‘ whp’ means that there is some such that whp . This is equivalent to , where in general denotes a quantity that, after dividing by , tends to 0 in probability. Similarly, ‘ whp’ simply means . ‘’ means that is bounded in probability. Finally, we use as shorthand for .

Remark 1.3 (Critical window).

The natural benchmark for our results is the classical Erdős–Rényi random graph process (which, as discussed, is also a bounded-size Achlioptas process). In their seminal 1960 paper, Erdős and Rényi [23] determined the asymptotics of the number of vertices in the largest component after steps for fixed . In 1984, Bollobás [11] initiated the study of ‘zooming in’ on the critical point, i.e, of the case , which has nowadays emerged into a powerful paradigm. In particular, assuming and , Bollobás identified the characteristic features of the phase transition. Namely, in the subcritical phase there are many ‘large’ components of size , similar to (1.5). In the supercritical phase there is a unique ‘giant component’ of size , whereas all other components are much smaller, similar to (1.7)–(1.8). In 1990, Łuczak [38] sharpened the assumptions of [11] to the optimal condition and (also used by Theorem 1.1), thus fully identifying the phase transition picture. Indeed, a separation between the sub- and super-critical phases requires , which is equivalent to (see also Remark 1.3). Informally speaking, Theorem 1.1 shows that the characteristic Erdős–Rényi features are robust in the sense that they remain valid for all bounded-size Achlioptas processes.

One main novelty of our proof approach is a combinatorial multi-round exposure argument around the critical point . From a technical perspective this allows us to avoid arguments where the process is approximated (in some time interval) by a simpler process, which would introduce various error terms. Such approximations are key in all previous work on this problem [56, 10, 32, 35, 7, 48, 6, 5, 54, 21]. Near the critical we are able to track the exact evolution of our bounded-size Achlioptas process . This more direct control is key for our very precise results, in particular concerning the finite-size scaling behaviour as . In this context our high-level proof strategy for step is roughly as follows: (i) we first track the evolution of up to step for some tiny constant , (ii) we then reveal information about the steps in two stages (a type of a two-round exposure), and (iii) we analyze the second exposure round using branching process arguments. The key is to find a suitable two-round exposure method in step (ii). Of course, even having found this, since there are dependencies between the edges, the technicalities of our approach are naturally quite involved (based on a blend of techniques, including the differential equation method, PDE theory, and branching process analysis); see Section 3 for a detailed overview of our arguments.

So far we have discussed bounded-size rules. One of the first concrete rules suggested was the product rule (PR), where we select the potential edge minimizing the product of the sizes of the components it joins. This rule belongs to the class of size rules, which make their decisions based only on the sizes of the components containing the endvertices of (note that PR is not a bounded-size rule). The original question of Achlioptas from around 2000 was whether one can delay the phase transition beyond using an appropriate rule, and Bollobás quickly suggested the product rule as most likely to do this. In fact, this question (which with hindsight is not too hard) was answered affirmatively by Bohman and Frieze [9] using a much simpler rule (a minor variant of the BF rule). Under the influence of statistical mechanics, the focus quickly shifted from the location of the critical time to the qualitative behaviour of the phase transition (see, e.g., [55]). In this context the product rule has received considerable attention; the simulation-based Figure 1 shows why: for this rule the growth of the largest component seems very abrupt, i.e., much steeper than in the Erdős–Rényi process. In fact, based on extensive numerical data, Achlioptas, D’Souza and Spencer conjectured in Science [1] that, for the product rule, the size of the largest component whp ‘jumps’ from to in steps of the process, a phenomenon known as ‘explosive percolation’. Although this claim was supported by many papers in the physics literature (see the references in [47, 48, 26, 20]), we proved in [47, 48] that no Achlioptas process can ‘jump’, i.e., that they all have continuous phase transitions. Nevertheless, the product rule (like other similar rules) still seems to have an extremely steep phase transition; we believe that for some , in contrast to the ‘linear growth’ (1.7) of bounded-size rules; see also [20]. Despite much attention, general size rules have largely remained resistant to rigorous analysis; see [50, 51] for some partial results. Our simulations and heuristics [49] strongly suggest that can even be nonconvergent in some cases.

1.3 Organization

The rest of the paper is organized as follows. In Section 2 we define the class of models that we shall work with, which is more general than that of bounded-size Achlioptas process. Then we give our detailed results for the size of the largest component, the number of vertices in small components, and the susceptibility (these imply Theorem 1.1). In Section 3 we give an overview of the proofs, highlighting the key ideas and techniques – the reader mainly interested in the ideas of the proofs may wish to read this section first. In Section 4 we formally introduce the proof setup, including the two-round exposure, and establish some preparatory results. Sections 5 and 6 are the core of the paper; here we relate the component size distribution of to a certain branching process, and estimate the first two moments of . In Section 7 we then establish our main results for , and , by exploiting the technical work of Sections 4–6 and the branching process results proved with Svante Janson in [31]. In Section 8 we discuss some extensions and several open problems. Finally, Appendix A contains some results and calculations that are omitted from the main text, and Appendix B gives a brief glossary of notation.

1.4 Acknowledgements

The authors thank Costante Bellettini and Luc Nguyen for helpful comments on analytic solutions to PDEs, and Svante Janson for useful feedback on the branching process analysis contained in an earlier version of this paper (based on large deviation arguments using a uniform local limit theorem together with uniform Laplace method estimates). We also thank Joel Spencer for his continued interest and encouragement.

2 Statement of the results

In this section we state our main results in full, and also give further details of the most relevant earlier results for comparison. In informal language, we show that in any bounded-size Achlioptas process, the phase transition ‘looks like’ that in the Erdős–Rényi reference model (with respect to many key statistics). In mathematical physics jargon this loosely says that all bounded-size rules belong to the same ‘universality class’ (while certain constants may differ, the behaviour is essentially the same). In a nutshell, our three main contributions are as follows, always considering an arbitrary bounded-size rule.

-

(1)

We determine the asymptotic size of the largest component in the sub- and super-critical phases, i.e., step with and (see Theorems 2.7 and 2.8), and show uniqueness of the ‘giant’ component in the supercritical phase. We recover the characteristic Erdős–Rényi features showing, for example, that whp we have for some (rule-dependent) analytic function with as .

-

(2)

We determine the whp asymptotics of the number of vertices in components of size as approximately (see Theorems 2.9 and 2.12). Informally speaking, in all bounded-size rules the number of vertices in small components thus exhibits Erdős–Rényi tree-like behaviour, including polynomial decay at criticality (the case ).

-

(3)

We determine the whp asymptotics of the subcritical susceptibility as (see Theorem 2.16). Thus the ‘critical exponents’ associated to the susceptibility are the same for any bounded-size rule as in the Erdős–Rényi case.

So far we have largely ignored that Achlioptas processes evolve over time. Indeed, Theorem 1.1 deals with the ‘static behaviour’ of some particular step , i.e., whp properties of the random graph . However, we are also (perhaps even more) interested in the ‘dynamic behaviour’ of the evolving graph, i.e., whp properties of the random graph process . Our results accommodate this: Theorems 2.8, 2.12 and 2.16 apply simultaneously to every step outside of the critical window, i.e., every step with and .

Remark 2.1.

When comparing our statements with results for the classical Erdős–Rényi process, the reader should keep in mind that corresponds to the uniform size model with edges. In particular, results for step should be compared to the binomial model with edge probability .

Remark 2.2.

Occasionally we write for , and for .

Remark 2.3.

For , we say that a function is (real) analytic if for every there is an and a power series with radius of convergence at least such that and coincide on . This implies that is infinitely differentiable, but not vice versa. A function defined on some domain including is (real) analytic on if is analytic. The definition for functions of several variables is analogous.

2.1 Bounded-size -vertex rules

All our results apply to (the bounded-size case of) a class of processes that generalize Achlioptas processes. As in [47, 48] we call these -vertex rules. Informally, in each step we sample random vertices (instead of two random edges), and according to some rule then add one of the possible edges between them to the evolving graph.

Formally, an -vertex size rule yields for each a random sequence of graphs with vertex set , as follows. is the empty graph with no edges. In each step we draw vertices from independently and uniformly at random, and then, writing for the sizes of the components containing in , we obtain by adding the edge to , where the rule deterministically selects the edge (between the vertices in ) based only on the component sizes. Thus we may think of as a function from to . Note that may contain loops and multiple edges; formally, it is a multigraph. However, there will be rather few of these and they do not affect the component structure, so the reader will lose nothing thinking of as a simple graph.

As the reader can guess, a bounded-size -vertex rule with cut-off is then an -vertex size rule where all component sizes larger than are treated in the same way. Following the literature (and to avoid clutter in the proofs), we introduce the convention that a component has size if it has size at least . We define the set

of all ‘observable’ component sizes. Thus any bounded-size rule with cut-off corresponds to a function . Of course, is a bounded-size -vertex rule if it satisfies the definition above for some .

For the purpose of this paper, results for -vertex rules routinely transfer to processes with small variations in the definition (since we only consider at most, say, steps, exploiting that by [48]). As in [48] this includes, for example, each time picking an -tuple of distinct vertices, or picking (the ends of) randomly selected (distinct) edges not already present. We thus recover the original Achlioptas processes as -vertex rules where always selects one of the pairs and . Since we are aiming for strong results here, one has to be a little careful with this reduction; an explicit argument is given in Appendix A.1.

Remark 2.4.

In the results below, a number of rule-dependent constants and functions appear. To avoid repetition, we briefly describe the key ones here. Firstly, for each rule there is a set of component sizes that can be produced by the rule. For large enough , we have if and only if is a multiple of the period of the rule; see Section 4.6. For all Achlioptas processes, and , so the indicator functions appearing in many results play no role in this case. Secondly, for each rule there is a function describing the exponential rate of decay of the component size distribution at time (step ), as in Theorem 2.9. This function is (real) analytic on a neighbourhood of , with and . Hence as .

2.2 Size of the largest component

In this subsection we discuss our results for the size of the largest component in bounded-size rules, which are much in the spirit of the pioneering work of Bollobás [11] and Łuczak [38] for the Erdős–Rényi model. Here Theorem 2.8 is perhaps our most important single result: it establishes the asymptotics of in the sub- and super-critical phases (i.e., all steps with and ). These asymptotics are as in the Erdős–Rényi case, up to rule-specific constants.

One of the most basic questions about the phase transition in any random graph model is: how large is the largest component just after the transition? From the general continuity results of [48] it follows for bounded-size rules that converges to a deterministic ‘scaling limit’ (see also [51]). More concretely, there exists a continuous function such that for each we have

| (2.1) |

where denotes convergence in probability (i.e., for every whp we have ). In fact, it also follows that for and otherwise, see [56, 10, 50]. Of course, due to our interest in the size of the largest component, this raises the natural question: what are the asymptotics of the scaling limit ? For some bounded-size rules, Janson and Spencer [32] and Drmota, Kang and Panagiotou [21] showed that as , where . However, for Erdős–Rényi random graphs much stronger properties are known: is analytic on . In particular, it has a power series expansion of the form

for having positive radius of convergence (in fact, ). Our next theorem shows that all bounded-size rules have these typical Erdős–Rényi properties (up to rule specific constants), confirming natural conjectures of Janson and Spencer [32] and Borgs and Spencer [19] (and the folklore conjecture that initially grows at a linear rate).

Theorem 2.5 (Linear growth of the scaling limit).

Informally, (2.1) and (2.2) show that the initial growth of the largest component is linear for any bounded-size rule, i.e., roughly that for some rule-dependent constant (see also Figure 1).

Remark 2.6.

The proof shows that for we have for a certain branching process defined in Section 5.2.

The convergent power series expansion (2.2) improves and extends results of Janson and Spencer [32] for the Bohman–Frieze process (with a second order error term), and one of the main results of Drmota, Kang and Panagiotou [21] for a restricted class of bounded-size rules (they establish for BF-like rules). Theorem 2.5 also shows that is discontinuous at (recall that for ), which in mathematical physics is a key feature of a ‘second order’ phase transition.

Unfortunately, the convergence result (2.1) tells us very little about the size of the largest component just before the phase transition (recall that for ). For the Erdős–Rényi process it is well-known that in the subcritical phase, for any we roughly have whenever , see, e.g., [11, 38]. For bounded-size rules there are several partial results [56, 35, 5, 54] for , but none are as strong as the aforementioned Bollobás–Łuczak results from [11, 38]. For the subcritical phase, our next theorem establishes the full Erdős–Rényi-type behaviour for all bounded-size rules (in a strong form). Theorem 2.7 confirms a conjecture of Kang, Perkins and Spencer [35], and resolves a problem of Bhamidi, Budhiraja and Wang [6], both concerning upper bounds of the form .

Theorem 2.7 (Largest subcritical components).

Here, as usual, means that for any there are such that for . See Remark 2.4 for the interpretation of the function . Since , this result shows in crude terms that the largest components have around the same size for some rule-dependent constant .

Theorem 2.7 is best possible: the assumption cannot be relaxed – inside the critical window the sizes of the largest components are not concentrated, see [5]. Furthermore, as discussed in [15], the error term is sharp in the Erdős–Rényi case (where and as ). Theorem 2.7 improves several previous results on the size of the largest subcritical component due to Wormald and Spencer [56], Kang, Perkins and Spencer [35], Bhamidi, Budhiraja and Wang [5] and Sen [54]. Most notably, in the weakly subcritical phase with the main results of [5, 54] are as follows: for bounded-size rules [5] establishes bounds of the form for , which in [54] was sharpened for the Bohman–Frieze rule to for . The key difference is that (2.3) provides matching bounds (the harder lower bounds were missing in previous work) all the way down to the critical window. Here the difference between and matters.

For the supercritical phase, (2.1) and Theorem 2.5 apply only for fixed , showing roughly that . Of course, it is much more interesting to ‘zoom in’ on the critical point , and study the size of the largest component when . Despite being very prominent and interesting in the classical Erdős–Rényi model, see, e.g., [11, 38, 40, 15, 12, 28], the weakly supercritical phase of bounded-size rules has remained resistant to rigorous analysis for more than a decade. The following theorem closes this gap in our understanding of the phase transition, establishing the typical Erdős–Rényi characteristics for all bounded-size rules. Informally, (2.5)–(2.6) state that (whp) we have whenever satisfies and (note that as ). In particular, in view of (2.2) this means that, in all bounded-size rules, just after the critical window the unique ‘giant component’ already grows with linear rate (i.e., that whp , see Figure 1).

Theorem 2.8 (Size of the largest component).

Let be a bounded-size -vertex rule. Let the critical time and the functions be as in (1.1) and Theorems 2.5 and 2.7. There is a constant such that the following holds for any function with as 333As usual we assume , but we do not write this as it is not formally needed: any statements involving that we prove are asymptotic (for example any ‘whp’ statement), and so we need consider only large enough that . and any fixed . Setting , whp the following inequalities hold in all steps .

-

1.

(Subcritical phase) If satisfies and , then

(2.4) -

2.

(Supercritical phase) If satisfies and , then we have

(2.5) (2.6)

Note that we consider step in (2.4) and step in (2.5)–(2.6). This parametrization may look strange, but it allows us to conveniently make whp statements about the random graph process . Indeed, (2.4)–(2.6) whp hold simultaneously in every step outside of the critical window, i.e., every step with and . This is much stronger than a whp statement for some particular step , i.e., for the random graph . For this reason, the subcritical part of Theorem 2.8 does not follow from Theorem 2.7. With this discussion in mind, one can argue that Theorem 2.8 describes the ‘dynamic behaviour’ of the phase transition in bounded-size Achlioptas processes.

2.3 Small components

During the last decade, a widely used heuristic for many ‘mean-field’ random graph models is that most ‘small’ components are trees (or tree-like). The rigorous foundations of this heuristic can ultimately be traced back to the classical Erdős–Rényi model, where it has been key in the discovery (and study) of the phase transition phenomenon, see [23, 11, 38]. As there are explicit counting formulae for trees, by exploiting the (approximate) independence between the edges this easily gives the asymptotics of in the Erdős–Rényi process, see (1.4).

For bounded-size rules, the classical tree-counting approach breaks down due to the dependencies between the edges. However, Spencer and Wormald [55, 56] already observed around 2001 that can be approximated via the differential equation method [58, 59]; their proof implicitly exploits that the main contribution again comes from trees, see also [50]. In particular, for the more general class of bounded-size -vertex rules it is nowadays routine to prove that for any and we have

| (2.7) |

where the functions are the unique solution of an associated system of differential equations ( depends only on with , see Lemmas 4.3 and 4.4). In fact, a byproduct of [56, 50] is that the have exponential decay of the form for , with . To sum up, in view of (1.4) and (2.7) the precise asymptotics of is an interesting problem (for the special case this was asked by Spencer and Wormald as early as 2001, see [55]). This requires the development of new proof techniques, which recover the Erdős–Rényi tree–asymptotics in random graph models with dependencies.

This challenging direction of research was pursued by Kang, Perkins and Spencer [35, 36] and Drmota, Kang and Panagiotou [21], who obtained some partial results for bounded-size rules, using PDE-theory and an auxiliary result from [48]. However, they only recovered the exponential rate of decay (i.e., that for small and large ) for a restricted class of rules which are Bohman–Frieze like. We sidestep both shortcomings by directly relating with an associated branching processes, see Remark 2.11. Indeed, the next theorem completely resolves the asymptotic behaviour of for all bounded-size -vertex rules. Note that below we have and for rule-dependent constants , so (2.8) qualitatively recovers the full Erdős–Rényi tree-like behaviour of (1.4). A more quantitative informal summary of (2.7) and (2.8) is that whp for large and small (ignoring technicalities).

Theorem 2.9 (Differential equation asymptotics).

Let be a bounded-size -vertex rule. Let the critical time and the functions be as in (1.1) and (2.7), and the set of reachable component sizes as in (4.63). There exist a constant and non-negative analytic functions and on such that

| (2.8) |

uniformly in and , with and . Furthermore, and for and as in (2.1) and Theorem 2.5.

Remark 2.10.

There is a constant such that for all .

Remark 2.11.

The proof shows that for we have for a certain branching process defined in Section 5.2.

The above multiplicative error is best possible for Erdős–Rényi (where , and , so that and as ). Moreover, the detailed asymptotics of (2.8) resolves conjectures of Kang, Perkins and Spencer [34] and Drmota, Kang and Panagiotou [21]. The indicator may look somewhat puzzling; its presence is due to the generality of -vertex rules – see Remark 2.4 and Section 4.6. In the Achlioptas process case we have , i.e., all component sizes are possible, and so the indicator may be omitted.

Although (2.8) is very satisfactory for the ‘idealized’ component size distribution , we cannot simply combine it with (2.7) to obtain the results we would like for the component size distribution of the random graph process , which is of course our main object of interest. The problem is that (2.7) only applies for and fixed , whereas we would like to consider and . In other words, we would like variants of (2.7) which allow us (i) to study large component sizes with , and (ii) to ‘zoom in’ on the critical , i.e., study with . The next theorem accommodates both features: it shows that holds for a wide range of sizes and steps . Note that there is some such that the assumptions on below, and hence (2.9)–(2.10), hold for any , with the allowed range of increasing as . (Aiming at simplicity, here we have not tried to optimize the range; see also Theorem 7.2, Corollary 5.17 and Section 6.3.1. Note that we allow for .)

Theorem 2.12 (Number of vertices in small components).

Let be a bounded-size -vertex rule. Let the critical time be as in (1.1), and the functions as in Theorem 2.5 and (2.7), and define where is as in Theorem 2.9. There is a constant such that, with probability , the following inequalities hold for all steps and sizes such that satisfies :

| (2.9) | ||||

| (2.10) |

where .

Remark 2.13.

The multiplicative error term in (2.9) allows for very precise asymptotic results in combination with (2.8). Indeed, whp, for all steps and sizes satisfying , we have444In this and similar formulae, the implicit constant is uniform over the choice of and .

Furthermore, combining (2.10) with Remark 2.10, we see that, whp, for all we have

| (2.11) |

Thus, at criticalilty we have polynomial decay of the tail of the component size distribution, which is a prominent hallmark of the critical window. For bounded-size rules the asymptotics of (2.11) answers a question of Spencer and Wormald from 2001, see [55].

2.4 Susceptibility

The susceptibility is a key statistic of the phase transition, which has been widely studied in a range of random graph models (see, e.g. [18, 27, 25, 30, 33]). For example, in classical percolation theory the critical density coincides with the point where (the infinite analogue of) the susceptibility diverges, and in the Erdős–Rényi process it is folklore that for we have

| (2.12) |

More importantly, in the context of bounded-size Achlioptas processes the location of the phase transition is determined by the critical time where the susceptibility diverges, see [56, 10, 50]. This characterization is somewhat intuitive, since is the expected size of the component containing a randomly chosen vertex from , see (1.2). Of course, since , bounds on one of and imply bounds on the other. (For example, implies .) However, one only obtains weak results this way; proving that whp after the point at which blows up is far from trivial.

Turning to the susceptibility in bounded-size rules, using the differential equation method [58, 59, 57] and ideas from [56, 32, 50] it is nowadays routine to prove that for each and we have

| (2.13) |

where the functions are the unique solution of a certain system of differential equations (involving also ), with . (Recall that denotes the th moment of the size of the component containing a random vertex.) Motivated by ‘critical exponents’ from percolation theory and statical physics, the focus has thus shifted towards the finer behaviour of the susceptibility, i.e., the question at what rate blows up as (in the Erdős–Rényi case we have , see (2.12) and [22, 27]). Using asymptotic analysis of differential equations, Janson and Spencer [32] determined the scaling behaviour of and for the Bohman–Frieze rule. For and their argument was generalized by Bhamidi, Budhiraja and Wang [6] to all bounded-size rules. Based on branching process arguments, the next theorem establishes the asymptotic behaviour of for any (for the larger class of bounded-size -vertex rules). To avoid clutter below, we adopt the convention that the double factorial is equal to for . Recall from Remark 2.4 that for an Achlioptas processes .

Theorem 2.14 (Idealized susceptibility asymptotics).

In the language of mathematical physics (2.13) and (2.15) loosely say that, as , all bounded-size rules have the same susceptibility-related ‘critical exponents’ as the Erdős–Rényi process (where the constant is , since and by folklore results).

Remark 2.15.

The proof shows that for we have for a certain branching process defined in Section 5.2.

Next we ‘zoom in’ on the critical point , i.e., discuss the behaviour of the susceptibility when . Here the subcritical phase in the Erdős–Rényi case was resolved by Janson and Luczak [27], using martingale arguments, differential equations and correlation inequalities. For bounded-size rules Bhamidi, Budhiraja and Wang [6, 5] used martingales arguments and the differential equation method to prove results covering only part of the subcritical phase. In particular, for with their results apply only to and and only in the restricted range . Using very different methods, the next theorem resolves the scaling behaviour of the susceptibility in the entire subcritical phase. In particular, our result applies for any all the way up to the critical window, i.e., we only assume . Note that when , so (2.16) intuitively states that whp .

Theorem 2.16 (Subcritical susceptibility).

The assumption cannot be relaxed, since holds deterministically, cf. (1.2). In (2.16) we have not tried to optimize the error term for , since our main interest concerns the behaviour. The supercritical scaling of the susceptibility is less informative and interesting, since is typically dominated by the contribution from the largest component. In particular, for with we believe that whp for any bounded-size rule (for fixed this follows from Theorem 2.8), but we have not investigated this.

3 Proof overview

In this section we give an overview of the proof, with an emphasis on the structure of the argument. Loosely speaking, one of the key difficulties is that there are non-trivial dependencies between the choices in different rounds. To illustrate this, let us do the following thought experiment. Suppose that we change the vertices offered to the rule at one step, and as a consequence, the rule adds a different edge to the graph. This results in a graph with different component sizes. Hence, whenever the process samples vertices from these components in subsequent steps, the rule is presented with different component sizes. This may alter the decision of the rule, and hence the edge added, which can change further subsequent decisions, and so on. In other words, changes can propagate throughout the evolution of the process, which makes the analysis challenging.

For bounded-size rules we overcome this difficulty via the following high-level proof strategy. First, we track the evolution of the entire component size distribution during the initial steps, where is a small constant. Second, using the graph after steps as an anchor, for we reveal information about the steps via a two-round exposure argument (not the classical multi-round exposure used in random graph theory). We engineer this two-round exposure in a way that eventually allows us to analyze the component size distribution in step via a neighbourhood exploration process which closely mimics a branching process. Intuitively, this allows us to reduce most questions about the component size distribution to questions about certain branching processes. These branching processes are not of a standard form, but we are nevertheless able to analyze them (with some technical effort). This close coupling with a branching process is what allows us to obtain such precise results. In this argument the restriction to bounded-size rules is crucial, see Sections 4.1 and 4.3.2.

In the following subsections we further expand on the above ideas, still ignoring a number of technical details and difficulties. In Section 3.1 we outline our setup and the two-round exposure argument. Next, in Section 3.2 we explain the analysis of the component size distribution via exploration and branching processes. Finally, in Section 3.3 we turn to the key statistics , and , and briefly discuss how we eventually adapt approaches used to study the Erdős–Rényi model to bounded-size Achlioptas processes.

3.1 Setup and two-round exposure

In this subsection we discuss the main ideas used in our two-round exposure; see Section 4.1 for the technical details. Throughout we fix a bounded-size -vertex rule with cut-off (as defined in Section 2.1). Using the methods of [50], we start by tracking the evolution of the entire component size distribution up to step . More precisely, we show that the numbers of vertices in components of size can be approximated by deterministic functions (see Theorem 4.8 and Lemma 4.4).

Conditioning on the graph after steps, i.e., regarding it as given, we shall reveal information about steps in two rounds. We assume (as we may, since the variables are concentrated) that each is close to its expectation. We partition the vertex set of into , where contains all vertices that in the graph are in components of size at most (the labels and refer to ‘small’ and ‘large’ component sizes). Note that in any later step , since , every vertex is in a component of with size larger than , i.e., with size as far as the rule is concerned. Hence, when a vertex in is offered to , in order to know the decision made by we do not need to know which vertex in we are considering – as far as is concerned, all such vertices have the same component size . In our first exposure round we reveal everything about the vertices offered to in all steps except that whenever a vertex in is chosen, we do not reveal which vertex it is; as just observed, this information tells us what decisions will make. This allows us to track: (i) the edges added inside , (ii) the –endvertices of the edges added connecting to , and (iii) the number of edges added inside . (Formally this can be done via the differential equation method [58, 59, 57] and branching process techniques, see Section 4.2–4.3; note that (i)–(ii) track the evolution of the ‘-graph’ beyond the critical .) After this first exposure round we have revealed a subgraph of (called the ‘partial graph’ in Figure 3), consisting of all edges in , together with all edges in steps between and with both ends in . Furthermore, we know that consists of with certain edges added: a known number of – edges whose endpoints in are known, and a known number of – edges.

In the second exposure round the vertices in (corresponding to (ii) and (iii) above) are now chosen independently and uniformly at random from ; see the proof of Lemma 4.1 for the full details. Hence, after conditioning on the outcome of the first exposure round, the construction of from the ‘partial graph’ described above has a very simple form (see Figure 3 and Lemma 4.2). Indeed, for each – edge the so-far unknown –endpoint is replaced with a uniformly chosen random vertex from . Furthermore, we add a known number of uniformly chosen random edges to . This setup, consisting of many independent uniform random choices, is ideal for neighbourhood exploration and branching process techniques.

3.2 Component size distribution

To get a handle on the component size distribution of the graph after steps, we use neighbourhood exploration arguments to analyze the second exposure round described above. As usual, we start with a random vertex , and iteratively explore its neighbourhoods. Suppose for the moment that . Recalling the construction of from the partial graph , any vertex has neighbours in and , which arise (a) via random – edges and (b) via – edges with random –endpoints. Furthermore, each of the adjacent –components found in (b) potentially yields further –neighbours via – edges. Repeating this exploration iteratively, we eventually uncover the entire component of which contains the initial vertex . Treating (a) and (b) together as a single step, each time we ‘explore’ a vertex in we reach a random number of new vertices in , picking up a random number of vertices in along the way. As long as we have not used up too many vertices, the sequence of pairs giving the number of and vertices found in the th step will be close to a sequence of independent copies of some distribution that depends on the ‘time’ . We thus expect the neighbourhood exploration process to closely resemble a two-type branching process with offspring distribution , corresponding to and vertices. In this branching process, vertices in have no children (they are counted ‘in the middle’ of a step). Of course, we need to modify the start of the process to account for the possibility that the initial vertex is in . Writing for the (final modified) branching processes, it should seem plausible that the expected numbers of vertices in components of size and in components of size at least approximately satisfy

| (3.1) |

ignoring technicalities (see Sections 5.1–5.3 and 6.3.1 for the details).

In view of (3.1), we need to understand the behaviour of the branching process . Here one difficulty is that we only have very limited explicit knowledge about the offspring distribution . To partially remedy this, we prove that several key variables determined by the first exposure round have exponential tails (see, e.g., inequalities (4.28)–(4.29) and (4.32)–(4.33) of Theorems 4.8 and 4.10). Combining calculus with ODE and PDE techniques (the Cauchy–Kovalevskaya Theorem; see Appendix A.2), this allows us to eventually show that the probability generating function

| (3.2) |

is extremely well-behaved, i.e., (real) analytic in a neighbourhood of , say (see Sections 4.2–4.4 and 6.1). In a companion paper [31] written with Svante Janson (see also Section 6.2 and Appendix A.4), we show that the probability of generating particles is roughly of the form

| (3.3) |

Turning to the survival probability , for this the –vertices counted by are irrelevant (since these do not have children, the only possible exception being the first vertex). Combining a detailed analysis of with standard methods for single-type branching processes, we eventually show that , and (in [31]) that the survival probability of is roughly of the form

| (3.4) |

for small (see Sections 6.1–6.2, Appendix A.4 and [31] for the details).

In the above discussion we have ignored a number of technical issues. For example, in certain parts of the analysis we need to incorporate various approximation errors: simple coupling arguments would, e.g., break down for large component sizes. (Such errors are not an artifact of our analysis. For example, the number of isolated vertices changes with probability in each step, so after steps we indeed expect random fluctuations of order .) To deal with such errors we shall use (somewhat involved) domination arguments, exploiting that the exploration process usually finds ‘typical’ subsets of the underlying graph (see Section 5.3.2). Perhaps surprisingly, this allows us to employ dominating distributions that have probability generating functions which are extremely close to the ‘ideal’ one in (3.2): the dominating branching processes are effectively indistinguishable from the actual exploration process. In this context one of our main technical contributions is that we are able to carry out (with uniform error bounds) the point probability analysis (3.3) and the survival probability analysis (3.4) despite having only some ‘approximate information’ about the underlying (family of) offspring distributions. This is key for determining the asymptotic size of the largest component in the entire subcritical and supercritical phases.

3.3 Outline proofs of the main results

Using the setup (and technical preparation) outlined above, we prove our main results for , and by adapting approaches that work for the classical Erdős–Rényi random graph. Of course, in this more complicated setup many technical details become more involved. In this subsection we briefly outline the main high-level ideas that are spread across Sections 4–7 (the actual arguments are complicated, for example, by the fact that parts of the branching process analysis rely on Poissonized variants of ).

We start with the number of vertices in components of size . After conditioning on the outcome of the first exposure round, we first use McDiarmid’s bounded differences inequality [39] to show that whp is close to its expected value (here we exploit that the second exposure rounds consists of many independent random choices), and then approximate via the branching process results (3.1) and (3.3). The full details of this approach are given in Sections 5.2 and 7.1, and here we just mention one technical point: conditioning allows us to bring concentration inequalities into play, but we must then show that (except for unlikely ‘atypical’ outcomes) conditioning on the first exposure round does not substantially shift the expected value of .

Next we turn to the size of the largest component in the subcritical and supercritical phases, i.e., where the step satisfies . Intuitively, our arguments hinge on the fact that the expected component size distribution has an exponential cutoff after size , see (3.1) and (3.3). Indeed, (3.3) and suggest that for we roughly have

| (3.5) |

In the subcritical phase we have by (3.4). Using (3.1) we thus expect that for we have

By considering which sizes satisfy , this suggests that whp

We make this rigorous via the first- and second-moment methods, using a van den Berg–Kesten (BK)-inequality like argument for estimating the variance (see Sections 5.1.3, 6.3.1 and 7.2.1 for the details). Turning to the more interesting supercritical phase, where , note that the right hand side of (3.5) is for , and that by (3.4). Using (3.1) we thus expect that for we have

Applying the first- and second-moment methods we then show that whp for suitable , adapting a ‘typical exploration’ argument of Bollobás and the first author [17] for bounding the variance (see Sections 5.3.3, 6.3.1 and 7.2.2 for the details). Mimicking the Erdős–Rényi sprinkling argument from [23], we then show that whp most of these size components quickly join, i.e., form one big component in steps (see Sections 4.5 and 7.2.2). Using continuity of , this heuristically suggests that whp

ignoring technicalities (see Section 7.2.2 for the details).

For the subcritical susceptibility with we proceed similarly. Indeed, substituting the estimates (3.1) and (3.3) into the definition (1.2) of , since we expect that for we have

| (3.6) |

In fact, comparing the sum with an integral, we eventually find that for small (see Lemma 6.16). Applying the second-moment method we then show that whp , using a BK-inequality like argument for bounding the variance (see Sections 5.1.3, 6.3.2 and 7.3 for the details).

Finally, one non-standard feature of our arguments is that we can prove concentration of the size of the largest component in every step outside of the critical window (cf. Theorem 2.8). The idea is to fix a sequence of not-too-many steps that are close enough together that we expect

| (3.7) |

Since there are not too many steps in the sequence, we can show that whp is close to its expected value for every step in the sequence. By monotonicity, in all intermediate steps we have

which together with (3.7) establishes the desired concentration (related arguments are sometimes implicitly used in the context of the differential equation method). As we shall see in Section 7.2, the choice of the step sizes requires some care, since we need to take a union bound over all auxiliary steps, but this idea can be made to work by sharpening the second-order error terms of various intermediate estimates. A similar proof strategy applies to the susceptibility , which is also monotone (see Section 7.3 for the details).

4 Preparation and setup

In this section we formally introduce the proof setup, together with some preparatory results. Throughout we fix a bounded-size -vertex rule with cut-off , and study the graph after steps, where (or rather ) with . We refer to (or in general ) as ‘time’. As discussed in Section 3, we stop the process after the first steps, where is a small constant, and then analyze the evolution of the component structure from step to step via a two-round exposure argument. The main goals of this section are to formally introduce the two-round exposure, and to relate the second round of the exposure to a random graph model which is easier to analyze.

Turning to the details, for concreteness let

| (4.1) |

Set

| (4.2) |

and

| (4.3) |

ignoring from now on the irrelevant rounding to integers. After steps we partition the vertex set into and , where contains all vertices in components of having size at most . Here the labels and correspond to ‘small’ and ‘large’ component sizes. This partition is defined at step , and does not change as our graph evolves.

In Section 4.1 we explain our two-round exposure argument in detail. Then, in Section 4.2, we use the differential equation method to track the number of vertices in small components, as well as parts of the evolution of the graphs induced by and . Next, in Section 4.3 we use branching process techniques to track the evolution of the –graph in more detail, which also yields exponential tail bounds for certain key quantities. In Section 4.4 we then use PDE theory to show that an associated generating function is analytic. In Section 4.5 we introduce a convenient form of the Erdős–Rényi sprinkling argument. Finally, in Section 4.6 we define and study the set of component sizes that the -vertex rule can produce, and the ‘period’ of the rule; for ‘edge-based’ rules such as Achlioptas processes these technicalities are not needed.

4.1 Two-round exposure and conditioning

Recall that we first condition on . Our aim now is to analyze the steps with . Recall that denotes the uniformly random -tuple of vertices offered to the rule in step . Given we expose the information about steps in two rounds. In the first exposure round , for every step we (i) reveal which vertices of are in and which in , and (ii) for those vertices in , we also reveal precisely which vertex is. In the second exposure round , for every step we reveal the choices of all so-far unrevealed vertices in .

The ‘added edges’, i.e., edges of , are of three types: – edges (where both endvertices are in ), – edges (where both endvertices are in , but still unrevealed after the first exposure round) and – edges (where the endvertex in is still unrevealed). To be pedantic, we formally mean pairs of vertices, allowing for loops and multiple edges; the term ‘edge’ allows for a more natural and intuitive discussion of the arguments. The following lemma encapsulates the key properties of the two-round exposure discussed informally in Section 3.1.

Lemma 4.1.

Given , the information revealed by the first exposure round is enough to make all decisions of , i.e., to determine for every the indices and such that and are joined by the rule . Furthermore, conditional on and on the first exposure round, all vertices revealed in the second exposure round are chosen independently and uniformly random from .

Proof.

The claim concerning the second exposure round is immediate, since in each step the vertices are chosen independently and uniformly random.

Turning to the first exposure round, we now make the heuristic arguments of Section 3.1 rigorous. For let be the set of edges of with both ends in (the edges added inside ), and let be the (multi-)set of vertices of in at least one – edge in (the set of endvertices of the added – edges). We claim that the information revealed in the first exposure round determines and for each . The proof is by induction on ; of course, .

Suppose then that and that the claim holds for . The information revealed in the first exposure round determines which of the vertices are in as opposed to , and precisely which vertices those in are. Let list the sizes of the components of containing , with all sizes larger than replaced by . We shall show that is determined by the information revealed in the first exposure round. By the definition of a bounded-size rule, determines the choice made by the rule , i.e., the indices and such that and are joined by in step , which is then enough to determine and , completing the proof by induction.

If , then is in a component of of size at least , so we know that , even without knowing the particular choice of . Suppose then that . Since we know and , we know the entire graph . Furthermore, we know exactly which components of are connected to in , namely those containing one or more vertices of . Let be the component of containing . If is not connected to in , then is also a component , whose size we know. If is connected to then in the component containing has size at least , so . This shows that is indeed known in all cases, completing the proof. ∎

Intuitively speaking, after the first exposure round , for we are left with a ‘marked’ auxiliary graph , as described in Figure 4. More precisely, for let be the ‘marked graph’ obtained as follows. Starting from , (i) insert all – edge added in steps , and (ii) for each – edge added in steps , add a ‘stub’ or ‘half-edge’ to its endvertex in . Thus, in the (temporary) notation of the proof above, is formed from by adding the edges in and stubs corresponding to the multiset . Each mark or stub represents an edge to a so-far unrevealed vertex in , and a –vertex can be incident to multiple stubs. For let denote the number of – edges (including loops and repeated edges) added in total in steps , so by definition

| (4.4) |

By Lemma 4.1 the information revealed in the first exposure round determines the graphs and the sequence . Furthermore, in the second exposure round we may generate from by replacing each stub associated to a vertex by an edge to a vertex chosen independently and uniformly at random from , and adding random – edges to , where the endvertices are chosen independently and uniformly random from .

Since our focus is on the component sizes of , the internal structure of the components of and is irrelevant; all we need to know is the size of each component, and how many stubs it contains. Any component of is either contained in (in which case ) or in . If then we say that has type if and contains stubs, i.e., is incident to – edges in , cf. Figure 4. As usual, for and , we write for the number of vertices of which are in components of size exactly . For , and , we write for the number of components of of type .555Note that counts vertices, and counts components; the different normalizations are convenient in different contexts. Thus

| (4.5) |

We may think of an added – edge as a component of type : it contains no vertices, but has two stubs associated to it. Hence the notation above; we let for .

For , let

| (4.6) |

This parameter list contains the essential information about . Given (a possible value of) , treating as deterministic we construct a random graph as follows: start with a graph consisting of type- components for all and , and components of size for all . Let be the set of vertices in components of the first type, and the set in components of the second type. Given , we then (i) connect each stub of to an independent random vertex in , and (ii) add random – edges to . By construction and Lemma 4.1 we have the following result.

Lemma 4.2 (Conditional equivalence).

Given , the random graph has the same component size distribution as conditioned on the parameter list . ∎

Our strategy for analyzing the component size distribution of will be as follows. In Sections 4.2–4.3 we will show that the random parameter list , which is revealed in the first exposure round, is concentrated, i.e., nearly deterministic. Then, in the second round (so having conditioned on ) we use the random model to construct . The advantage is that is very well suited to branching process approximation, since it is defined by a number of independent random choices.

Note for later that, by definition of the discrete variables, for we have

| (4.7) |

4.2 Differential equation approximation

In this subsection we study the (random) parameter list defined in (4.6). We shall track the evolution of several associated random variables, using Wormald’s differential equation method [58, 59] to show that their trajectories stay close to the solution of a certain associated system of ODEs (after suitable rescaling). In fact, we rely on a variant of this method due to the second author [57] in order to obtain sufficiently small approximation errors.

4.2.1 Small components

We start by tracking the number of vertices of which are in components of size , which we denote by . Here, as usual, ‘size ’ means size at least . The following result intuitively shows , where is a smooth (infinitely differentiable) function. Later we shall show that the , and the related functions appearing in the next few lemmas, are in fact analytic.

Lemma 4.3.

With probability at least we have

| (4.8) |

where the functions from to are smooth. They satisfy and , and are given by the unique solution to

| (4.9) |

for certain coefficients with .

Proof.

This follows from a nowadays standard (see e.g., [56, 10]) application of the differential equation method [58, 59], where the error term is due to a variant of the second author [57]. Let us briefly sketch the details.

Noting that edges connecting two vertices in components of size leave all with unchanged, it is easy to check from the definition of a bounded-size rule that if, in step , all vertices with lie in different components, then for each the number of vertices in components of size changes by , a deterministic quantity with . Furthermore, in step , the probability that at least two of the randomly chosen vertices lie in the same component of size at most is at most . So, if denotes the natural filtration associated to our random graph process, using it follows as in [56, 51] that

| (4.10) |

Since , and , a routine application of the differential equation method [57] (see, e.g., [56, 10, 48]) implies that (4.8) holds with probability at least , where the are the unique solution to (4.9).

Now we turn to properties of the functions . By induction on we see that the th derivatives exist for all and , i.e., that the are smooth. Since and , it follows from (4.8) that and . (This also follows directly from the differential equations, similar to Theorem 2.1 in [56].) Finally, and imply . ∎

For later reference we now extend the results of Lemma 4.3 to any fixed component size . One way to do this is to note that any bounded-size rule with cut-off can be interpreted as a bounded-size rule with cut-off , and apply Lemma 4.3 to this rule. This has the drawback that as varies, our formula for changes. In the next lemma we take a different approach which avoids this. The key point is that the functions in (4.11)–(4.12) below are the unique solution of a system of ODEs. Recall that .

Lemma 4.4.

Proof.

The proof is a minor generalization of that of (4.8), so let us omit the details and only outline how the differential equations are obtained. For the equation (4.9) remains valid; here we may either interpret as , or include an equation for itself; this makes no difference. For , arguing as for (4.9) but now with ‘size ’ playing the role of size we have

| (4.14) |

where the are constants with . Recalling (4.9) and (4.13), the key observation is that each depends only on with . Hence standard results imply that the infinite system of differential equations (4.9) and (4.13)–(4.14) has a unique solution on . Mimicking the proof of Lemma 4.3, it then follows that the functions are smooth, with and . ∎

Recall that after steps we partition the set of vertices into , where contains all vertices in components of size at most . Our later arguments require that whp ; in the light of Lemma 4.3, to show this it is enough to show that . This is straightforward for ; for the key observation is that a new component of size is certainly formed in any step where all vertices lie in distinct components of size . Hence, via successive doublings, by time we create many components of size ; Lemma 4.5 makes this idea rigorous.

Lemma 4.5.

Define the functions as in Lemma 4.3. For all we have .

Proof.

As noted above, if is even then . Furthermore, if does not contain . Since , and , by the form of in (4.9) and (4.14) it readily follows for any integer that

| (4.15) |

We claim that, for every and , we have ; the proof is by induction on . For the base case , from (4.15) we have . Hence . For the induction step , we write to avoid clutter. It follows from (4.15) that for we have . Since by induction, we deduce that there is a such that for all . The first inequality in (4.15) implies that in , which readily implies for .

This completes the proof by noting that whenever . ∎

4.2.2 Random – edges

Next we focus on the evolution of , which counts the number of – edges added in steps .

Lemma 4.6.

With probability at least we have

| (4.16) |

where the function is smooth, with and . It is given by the unique solution to the differential equation (4.19).

Proof.

This follows again by a routine application of the differential equation method [57], so we only outline the argument. Formally, we use Lemma 4.3 to obtain bounds at step , and then track and from step onwards.

Analogous to (4.10) we consider , i.e., the conditional one-step expected change in . This time we need to consider vertices in components of size that are in separately from those in . Let

| (4.17) |

which corresponds to the idealized rescaled number of vertices in . Noting that for there are vertices in that are in components of of size (i.e., size at least ), let

| (4.18) |

corresponding to the idealized rescaled number of vertices in which are in components of size . Since is a bounded-size rule, is determined by the following information: the sizes of the components containing the vertices and, where , the information whether is in or not. (It does not matter whether any of these vertices lie in the same component or not). So, with and (4.4) in mind, it is straightforward to see that is given by the unique solution to

| (4.19) |

where if we have for the indices selected by the rule, and otherwise.

Now we turn to properties of . By Lemma 4.3, all are smooth, so is smooth by (4.19). Similarly, recalling and , we see that and . Now, if distinct vertices from are chosen, then a – edge is added. Hence , which implies for all , see Lemma 4.5. Finally, using and we deduce that , so by (4.1) we have for all . ∎

4.2.3 Components in

We now study the ‘marked graph’ defined in Section 4.1, see also Figure 4. For and , recall that counts the number of type- components in , i.e., components of which contain vertices from and have stubs (and so are incident to – edges in ). As usual, we expect that can be approximated by a smooth function , and our next goal is to derive a system of differential equations that these must satisfy. Note that (4.20) below only implies for fixed and (see Section 4.3.2 for an extension to all and ).

Lemma 4.7.

Proof.

As in the proof of Lemma 4.6 we only sketch the differential equation method [57] argument. Again, we use Lemma 4.3 to obtain bounds at step , and then track and from step onwards; here, as usual, .

Since , the ‘exceptional event’ that two of the random vertices lie in the same –component of with contributes at most, say, to . Hence, recalling the definition of , by considering the expected one-step changes of , it is not difficult to see that is a polynomial function of , the with , and the with and (edges connecting two vertices from or two vertices in –components with or leave unchanged). For later reference, we now spell out these differential equations explicitly. By (4.5), the initial conditions are

| (4.21) |

Turning to , set

| (4.22) |

From the relationship between and established in Section 4.1 (see Figure 4), a vertex in a type- component of is in a component of with size , where size means size . Recall that in step the rule connects with , where . In the following formulae we sum over all possibilities for , and always tacitly define

Bearing in mind that , similar arguments to those leading to (4.9) and (4.10) show that

| (4.23) |

where

| (4.24) |

corresponding to creating a new –component by adding an edge within ,

| (4.25) |

corresponding to adding a – edge to a –component, and

| (4.26) |

corresponding to destroying a –component by connecting one of its vertices in to something else. (The normalization is different for and since counts components, whereas counts vertices.)

Turning to properties of the , recall that the are smooth on . The key observation is that depends only on and , see (4.23)–(4.26). So, using , standard results imply that the infinite system of differential equations (4.21)–(4.23) has a unique solution on . Furthermore, by induction on (and ) we see that all the are times differentiable; thus the are smooth on . Finally, since , standard comparison arguments yield , say. ∎

4.3 Exploration tree approximation

In this subsection we continue studying the (random) parameter list defined in (4.6) of Section 4.1. More concretely, we shall track the evolution of several associated random variables using the exploration tree method developed in [50], which intuitively shows that these variables (i) are concentrated, and (ii) have exponential tails. This proof method is based on branching process approximation techniques, and it usually works in situations where the quantities in question can be determined by a subcritical neighbourhood exploration process.

4.3.1 Component size distribution

We first revisit the number of vertices of in components of size in the subcritical phase, which we studied in [50] for size rules (for bounded-size rules the quantity appearing in Theorem 1 of [50] is equal to by Theorem 15 of [50]). Since , Theorem 1 of [50] implies the following result, which applies to all component sizes and steps , showing concentration and exponential tail bounds.

Theorem 4.8.

Let be the functions defined in Lemma 4.4. There are constants with such that for , with probability at least , the following holds for all :

| (4.27) | |||

| (4.28) | |||

| (4.29) |

Furthermore, we have for all . ∎

Remark 4.9.

To be pedantic, the functions of Theorem 1 of [50] could potentially differ from those considered in Lemma 4.4. However, since both are defined without reference to , by (4.11) and (4.27) these must be equal. This justifies (with hindsight) our slight abuse of notation. Furthermore, from Lemmas 4.4 and 4.5 and the fact that , we see that

Let us briefly outline the high-level proof strategy from Section 2 of [50], which we will adapt to (as defined in Section 4.1) in a moment. The basic idea is to generalize slightly, and establish concentration starting from an initial graph . Using induction, it then suffices to prove concentration during an interval consisting of a small (linear) number of steps. For this purpose we use a two-phase666We use the word phase rather than round to avoid any confusion with the main two-round exposure argument described in Section 4.1. exposure argument: we first reveal which -tuples appear in the entire interval, and then expose their order (in which they are presented to the rule ). Given a vertex , via the first exposure phase we can severely restrict the set of components (of ) and tuples (that appear in the interval) which can influence the size of the component containing under the evolution of any size rule. Indeed, the only components/tuples which can possibly be relevant are those which can be reached from after adding all edges in each -tuple appearing in the first exposure phase. Of course, all these tuples and components can be determined by a neighbourhood exploration process. If the interval has length , then (since there are at most many -tuples containing any given vertex, each containing at most new vertices) it seems plausible that the expected size of the associated offspring distribution is at most roughly

| (4.30) |

where, as usual, denotes the susceptibility of the graph , i.e., the expected size of the component containing a random vertex.

In [50] our inductive argument hinges on the fact that the associated branching process remains subcritical (i.e., quickly dies out) as long as . In the first exposure phase this allows us to couple the neighbourhood exploration process with an ‘idealized’ branching process that is defined without reference to . In particular, this gives rise to a so-called exploration tree (see page 187 in [50]), which itself contains enough information to reconstruct all relevant tuples and components. In the second exposure phase we then reveal the order of the relevant tuples, using the rule to construct the component containing (see Section 2.4.3 in [50]). We can eventually establish tight concentration since, by the subcritical first phase, typically contains rather few components and tuples (see Lemma 14 in [50]). Finally, the above discussion also explains why the inductive argument breaks down around , since then a giant component emerges (in which case , so for any the branching process just described will be supercritical).

4.3.2 Distribution of the –components