Collateral Unchained: Rehypothecation networks, concentration and systemic effects

Abstract

We study how network structure affects the dynamics of collateral in presence of rehypothecation. We build a simple model wherein banks interact via chains of repo contracts and use their proprietary collateral or re-use the collateral obtained by other banks via reverse repos. In this framework, we show that total collateral volume and its velocity are affected by characteristics of the network like the length of rehypothecation chains, the presence or not of chains having a cyclic structure, the direction of collateral flows, the density of the network. In addition, we show that structures where collateral flows are concentrated among few nodes (like in core-periphery networks) allow large increases in collateral volumes already with small network density. Furthermore, we introduce in the model collateral hoarding rates determined according to a Value-at-Risk (VaR) criterion, and we then study the emergence of collateral hoarding cascades in different networks. Our results highlight that network structures with highly concentrated collateral flows are also more exposed to large collateral hoarding cascades following local shocks. These networks are therefore characterized by a trade-off between liquidity and systemic risk.

Keywords: Rehypothecation, Collateral, Repo Contracts, Networks, Liquidity, Collateral-Hoarding Effects, Systemic Risk.

JEL Codes: G01, G11, G32, G33.

1 Introduction

This paper investigates the collateral dynamics when banks are connected in a network of financial contracts and they have the ability to rehypothecate the collateral along chains of contracts. Collateral is of increasing importance for the functioning of the global financial system. One reason for this is that the non-bank/bank nexus has become considerably more complex over the past two decades, in part because the separation between hedge funds, mutual funds, insurance companies, banks, and broker/dealers has become blurred as a result of financial innovation and deregulation (Singh, , 2016; Pozsar and Singh, , 2011). Another reason for the significant increase in collateral volumes (comparable to M2 until the recent financial crisis, see e.g. Singh, , 2011) has been the diffusion of rehypothecation agreements. The role of collateral in lending agreements is to protect the lender against a borrower’s default. Rehypothecation111Throughout this paper, the terms “re-use”, “rehypothecation”, and “re-pledge” are interchangeable. consists in the right of the lender to re-use the collateral to secure another transaction in the future (see Monnet, , 2011).

Rehypothecation of collateral has clear advantages for liquidity in modern financial systems (see Financial Stability Board, 2017b, ). In particular, it allows parties to increase the availability of assets to secure their loans, since a given pool of collateral can be re-used to support different financial transactions. As a result, rehypothecation increases the funding liquidity of agents (see Brunnermeier and Pedersen, , 2008). At the same time, rehypothecation also implies risks for market players. First, one risk associated with the additional funding liquidity allowed by rehypothecation can be the building-up of excessive leverage in the market (see e.g. Bottazzi et al., , 2012; Singh, , 2012; Capel and Levels, , 2014). Second, rehypothecation implies that several agents are counting on the same set of collateral to secure their transactions. It follows that rehypothecation may represent yet another channel through which agents’ balance sheets become interlocked222See for Battiston et al., (2016) for an account of the sources of banks’ interconnectedness in financial systems., and thus a source of distress propagation and of systemic risk. For instance in the face of idiosyncratic shocks, some institutions may start to precautionarily hoard collateral, which in turn constrains the availability of collateral and its re-use for the downstream institutions in chains of repledges. This may consequently lead to an inefficient market freeze if participants lack the necessary assets to secure their loans (Leitner, , 2011; Monnet, , 2011; Gorton and Metrick, , 2012). The latter is the distress channel we focus on in this paper.

To analyze economic benefits and systemic consequences of rehypothecation, we develop a model of collateral dynamics over a network of repurchase agreements (repos) across banks. To keep the model as simple as possible we abstract from many features of markets with collateral, and we assume that the amount of collateral available for repo financing is set as a constant fraction of total collateral available to each agent. The latter includes the proprietary collateral endowment of each bank as well as the collateral obtained from other banks via reverse repos. Although simple, our model allows us to highlight what features of rephypothecation network topology determine (i) the overall volume of collateral in the market, and (ii) the velocity of collateral (Singh, , 2011). We show that both variables are an increasing function of the length of open chains. However, for a given length, cyclic chains (i.e. those where banks are organized in a closed chain of repo contracts) produce higher collateral than a-cyclic chains. Furthermore, we show that the direction of collateral flows also matters. In particular, concentrating collateral flows among few nodes organized in a cyclic chain allows large increases in collateral volume and in velocity even with small chains’ length. Finally, we investigate total collateral under some typical network architectures, which capture different modes of organization of financial relations in markets, and in particular different degrees of heterogeneity in the distribution of repo contracts and of collateral flows. We show that total collateral is an increasing function of the density of financial contracts both in the random network (where heterogeneity is mild) and in the core-periphery network (where heterogeneity is high). However, core-periphery structures allow for a faster increase in collateral.

The above-explained model with exogenous levels of collateral hoarding rates is useful to analyse the effects of network topology on collateral flows. At the same time it is unfit to study the systemic risk implications of rehypothecation as hoarding behaviour could also reflect the liquidity position of agents in the network. We thus extend the basic model, to introduce hoarding behaviour that accounts for liquidity risk. More precisely, we assume that hoarding rates are set according to a Value-at-Risk (VaR) criterion, aimed at minimizing liquidity default risk. In this framework, we show that the equilibrium hoarding rate of each bank is a function of the hoarding rates and the collateral levels of the banks at which it is directly and indirectly connected. This introduces important collateral hoarding externalities in the dynamics, as an increase in hoarding at some banks may indirectly cause higher hoarding at other banks even not directly connected to it. We then use the extended model to study the impact on total collateral losses of small uncertainty shocks hitting a fraction of banks in the network, and how those losses vary with the structure of the rehypothecation networks. We show that core-periphery structures are the most exposed to large collateral losses when shocks hit the central nodes in the network, i.e. the one concentrating collateral flows. As, core-periphery are also the structures that generate larger collateral volumes, our results highlight that these structures are characterized by a trade-off between liquidity and systemic risk.

Our work contributes to the recent theoretical literature on the consequences of collateral rehypothecation (see e.g. Bottazzi et al., , 2012; Andolfatto et al., , 2017; Gottardi et al., , 2017; Singh, , 2016). This literature has highlighted the role of rehypothecation in determining repo rates (e.g. Bottazzi et al., , 2012), or in softening borrowing constraints of market participants and in shaping the interactions in repo markets (Gottardi et al., , 2017; Andolfatto et al., , 2017) or, finally, it has contributed to evaluate some welfare aspects of policies aimed at regulating rehypotheaction (Andolfatto et al., , 2017). However, to the best of our knowledge, our paper is the first to study the role of the structure of the network of collateral exchanges and to explore how different network structures determine overall collateral volumes and velocity. Furthermore, our work contributes also to the literature on liquidity hoarding cascades, and it is particular related to the work of Gai et al., (2011). However, different from this work, our model introduces hoarding rates that are responsive to the liquidity position of the single bank and to the position occupied in the network. In addition, it shows that liquidity hoarding dynamics can have quite different consequences depending on the particular structure of the network.

The paper is organized as follows. Section 2 introduces the basic definitions used throughout the paper and the model with fixed hoarding rates. Section 3 studies in detail how the structure of rehypothecation networks determines collateral volume and its velocity. Next, Section 4 extends the model to feature time-varyng hoarding rates determined according to a VaR criterion. Section 5 uses the latter model to study collateral hoarding cascades in different rehypothecation networks. Finally, Section 6 concludes, also by discussing some implications of our work.

2 A model of collateral dynamics on networks

In this section we build the network model that we then use the analyse the ability of the financial system to generate endogenous collateral in presence of rehypothecation and, next, to study the dynamics of collateral hoarding cascades in presence of shocks. We start with basic definitions that we shall use throughout the paper. We then introduce the laws governing collateral dynamics in presence of rehypothecation and of fixed hoarding coefficients by banks.

2.1 Definitions

Consider a set of financial institutions (“banks” for brevity in the following). Banks invest into an external asset, that yields an exogenously fixed return , and that can also be used as a collateral. In, addition they lend to each other by using only secured loans that involve exchange of collateral as in Singh, (2011).333See also Aguiar et al., (2016) for a more comprehensive discussion of the structure of collateral flows. More precisely, we assume that all debt contracts are “repo” contracts, they are thus secured by collateral. A “repo” or “repurchase agreement”, is the sale of securities together with an agreement for the seller to buy back the securities at a later date.444 The repurchase price should be greater than the original sale price, the difference effectively representing interest, and sometimes called the repo rate. A “reverse repo” is the same contract from the point of view of the buyer. The haircut rate of a repo, that we denote as , is a percentage that is subtracted from the market value of an asset that is being used in a repo transaction.555The size of the haircut usually reflects the perceived risk associated with holding the asset. To collect funds via repo contracts each bank () can use the collateral that has in its “box”. The box includes both the proprietary collateral or the collateral obtained via reverse-repos, which can then be re-pledged or rehypothecated for further repo transations. Repo transactions among banks using proprietary and non-properietary collateral give rise to a directed network , that we shall label “rehypothecation network”. To explain in details the dynamics of collateral in each bank’s box and the timing of the events occurring through the network it is useful to define the following notations:

-

•

: the total amount of collateral flowing out of bank ’s box at each step, i.e. the total amount of collateral that the bank uses to obtain loans from other banks.

-

•

: the total amount of (re-pledgeable) collateral remaining inside the box.

-

•

: the total amount of (pledgeable) collateral flowing into the box of the bank . At every step, the collateral that flows into the box must equal the collateral that remains in the box plus the collateral that flows out of the box. Hence, we have . Notice that includes both proprietary as well as non-proprietary assets received from other banks.

-

•

: the value of the proprietary collateral of the bank . This means the bank is the original owner of .

-

•

: the borrowers’ set of bank , i.e. the banks that obtained funding from via repos and thus provided collateral to . In the rehypothecation network, is also the “in-neighborhood” of .

-

•

: the lenders’ set of bank , i.e. the banks that obtained collateral from and thus provided funding to . In the rehypothecation network, is also the “out-neighborhood” of .

-

•

Unless specified otherwise, each of the above mentioned symbols written without indices denotes the vector of the same variable for all the banks in the system, for instance , and similarly for the other quantities.

Furthermore, let the variable capture the direction of collateral flow from the bank to the bank . In particular, for every pair of banks and , if bank has given collateral to bank and otherwise. Two additional variables related to the direction of collateral flows are the “out-degree” of a bank , , which measures the total number of outgoing links of the bank, and thus the number of banks to whom bank provided collateral to. Likewise, the “in-degree” of a bank , , is the total number of banks that provided collateral to .

Finally, we assume that each bank hoards a fraction of the collateral it has in the box. More precisely, for every monetary unit of collateral, the bank will keep inside its box and give away . Moreover, to keep the model simple we assume that each bank homogeneously spreads its non-hoarded collateral across its lenders. Let be the share of bank ’s outgoing collateral flowing into the box of the bank . If (i.e. ), then all shares are equal to zero. If the lender’s set is not void, , that is if , then for the total outgoing collateral pledged or re-pledged by bank , it holds:

since the shares satisfy the constraint . Notice, that this means that each non-zero column of the matrix of shares associated with the network is summing to 1. In addition, recall that collateral is spread homogenously across lenders. This implies that

and that the elements of the matrix can be expressed as

| (1) |

2.2 Collateral dynamics

To describe collateral dynamics in our model let us assume, in line with Bottazzi et al., (2012) that the amount of collateral that can be re-hypothecated never exceeds the haircutted amount of collateral. Furthermore, let us assume for simplicity that the haircut rate is the same for all banks. On these grounds, we can write the following expression for the dynamics of , the total amount collateral flowing out of the box of the bank :

| (2) |

where is the proprietary amount of outgoing collateral of the bank . The parameter accounts for the fraction that is not hoarded. The second term of the equation captures the amount of collateral received by from its borrowers and that is re-pledged. Notice that bank can only re-pledge a fraction of what it receives, where accounts for the fraction remaining after the haircut is applied, and accounts for what is not hoarded. Finally, is an indicator equal to one if bank engages in at least one repo contract so that its out-degree is positive and equal to zero otherwise (i.e and zero otherwise).

Similarly, the dynamics of the total amount of re-pledgeable collateral remaining inside the box of the bank is described by the following equation

| (3) |

where is the initial remaining collateral.

Uses and re-use of collateral in our model are fully described by the recursive process explained by the above two equations. Notice that both Equation (2) and (3) imply that at the initial step every bank gives away of collateral to its outgoing neighbors and keeps inside its box. In addition, for an amount of that the bank receives from a neighbour , it re-pledges and hoards an amount . However, only the amount of this hoarded collateral is further re-pledgeable to obtain further funding later, because the haircutted amount of collateral, , is kept in a segregated account that can be only accessed in the case of a credit event (see Bottazzi et al., , 2012, for details).

We can also determine the expression of total amount of re-pledgeable collateral flowing into the box of each bank :

| (4) |

The last equation makes clear that the total collateral flow in the box of a bank, includes the proprietary assets (i.e. ) as well as re-pledgeable non-proprietary assets (i.e. ) received from other banks via reverse repos. Notice that and that . Substituting the latter expression in equation (4) we obtain a system of equations in the variables :

| (5) |

So far we have not said anything about timing in our model. However, the possibility of collateral use and re-use changes over time as the inflows and outflows of collateral in a bank’s box change over time as a consequence of the different uses and re-uses of collateral made by other banks in the network. In addition, the very possibility of re-using collateral is clearly constrained by the maturity of a repo contract . In what follows, we shall assume that the maturity of repo contracts is longer than the time scale of the rehypothecation process.666Notice that in many cases, the rehypothecation process ends already after a small number of steps, typically smaller than the number of banks in the system. In addition, the effective duration of the rehypothecation process exponentially decreases with the levels of the non-hoarding rates and of the haircut rates (see also next section).

Moreover we shall focus on equilibrium collateral. This equilibrium corresponds to the amount of collateral flow generated by the system over an infinite amount of steps of collateral uses and re-uses. Finally, we shall focus henceforth only on the equilibrium value of the outflowing collateral (equilibrium collateral henceforth). Indeed, first, via Equation 4 remaining collateral is also determined in equilibrium once the amount of outflowing collateral and the initial proprietary collateral are known. Second, outflowing collateral is a very interesting variable in our model, as it captures each bank’s contribution to overall collateral flows, and thus to overall funding liquidity in the market.

To find the equilibrium of outflowing collateral, let us start by writing equation (2) in matrix form

| (6) |

where the the elements is the adjacency matrix of the rehypothecation network , with elements defined as:

Given the network of collateral flows , the haircut rate , and the vector of non-hoarding rates , we can obtain the equilibrium value of by solving equation (6) as follows:

| (7) |

with is the identity matrix of size , . The above equation indicates that equilibrium collateral will in general be a function of the of the entire topology of the rehypothecation network and of the vector of non-hoarding rates . In the next sections we first study the role of the network topology in affecting collateral flows and in determining different levels of equilibrium collateral.

3 Rehypothecation networks and endogenous collateral

We shall now describe how the structure of the rehypothecation network affects collateral flows and equilibrium collateral determined according to the model developed in the previous section. To perform our investigation it is useful to define some aggregate indicators mesuring the performance of a network in affecting collateral flows. The first one is the aggregate amount of outgoing collateral, , or “total collateral” henceforth, which is defined as:

| (8) |

In addition, we also introduce the multiplier of the aggregate amount of proprietary collateral777See Financial Stability Board, 2017a for discussions of other collateral re-use measures., , or “collateral multiplier”, henceforth. It is defined as:

| (9) |

where is the total outflowing proprietary collateral. Throughout the paper, we shall focus on and when analyzing collateral creation allowed by a given network . Notice that captures the aggregate flow of collateral provided by banks in the financial system. A higher (lower) amount of this flow indicates a more liquid market, i.e. one where agents can easily find collateral to secure their financial transactions. Furthermore, notice that the denominator on the right hand side of equation (9) is the aggregate amount of initial ouflowing collateral. Accordingly, captures the velocity of collateral when rehypothecation is allowed (see also Singh, , 2011). Again, a higher value of indicates a more liquid market, and in particular one where the same set of collateral can secure a larger set of secured lending contracts. In that respect, we shall also say that a rehypothecation network generates “endogenous collateral” whenever the collateral multiplier associated with it is larger () Clearly, both performance indicator are affected by the hoarding behavior of banks in the network. To simplify the analysis in this section we shall assume the non-hoarding and hoarding rates are fixed, so that and , . In Section 4, we shall remove this restriction, and we shall discuss how banks set these coefficients endogenously, according to a VaR criterion in presence of liquidity shocks.

We shall begin our analysis by providing stylized examples and by stating proposition that show how the aggregate amount of collateral going out of the boxes of all banks, , and the multiplier of collateral, , are influenced by some key characteristics of rehypothecation networks, like the length of rehypothecation chains, the presence of cyclic chains, or the direction of collateral flows. In additions, these results shed light on the core mechanisms driving the generation of endogenous collateral and of collateral hoarding cascades in more complex network architectures.

3.1 Length of chains and network cycles

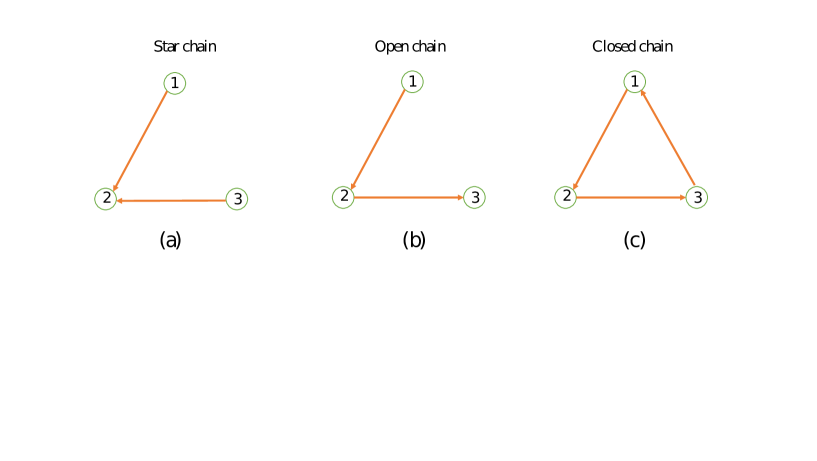

Let us start with simple examples of chains composed by three banks as shown in Figure 1: panel (a) a star chain, panel (b) an open chain or “a-cyclic” chain, and panel (c) a closed chain or a “cycle”.

Star chains

In the first case (i.e. the star chain in Figure 1 (a)), B2 receives collateral from B1 and B3, and then it does not re-use it. We will show that without rehypothecation, there is no endogenous collateral created in the system. Before discussing the example, we denote by the cumulated amount of collateral ougoing from the box of the bank after times. In addition, indicates total collateral after times and the corresponding multiplier.888Notice that mentioned in equation (7) is equilibrium collateral, and it corresponds to the amount of outflowing collateral when . At , the initial total amounts of collateral outgoing from the boxes of B1, B2, B3 are

| (10) |

At , remains constant since there is no re-use of collateral. We can write

| (11) |

where

It follows that total collateral in the example of Figure 1 (a) is always equal to the sum of the initial prorietary collateral outflowing from banks’ boxes and thus, that there is no creation of endogenous collateral. That is, we get:

| (12) |

and

| (13) |

A-cyclic chains

We now consider the second example represented by the open chain or a-cyclic chain in Figure 1 (b). In this case B2 can re-use the collateral that it receives from B1. In presence of rehypothecation the network generates endogenous collateral, . However, the possibilities of endogenous collateral creation are constrained by the length of the open chain (and equal to 2 in the example shown in the figure). At , the initial amounts of collateral outgoing from the boxes of B1, B2, B3 are

| (14) |

At , bank will re-use a fraction of an additional (re-pledgeable) collateral that it has received from the bank at time . Therefore, the amounts of collateral outgoing from the boxes of B1, B2, B3 are

| (15) |

which in matrix form reads

| (16) |

where now

Since all elements of are equal to zero for all , we get that the equilibrium values of total outflowing collateral and of the corresponding multiplier are:

In addition,

| (17) |

and

| (18) |

Notice that the above collateral multiplier is larger than 1 as long as and .

Cyclic chains

We now consider the third case when rehypothecation processes among banks create a closed chain or a “cycle”, like the one in Figure 1 (c). Notice that in the above example every bank has a positive out-degree, i.e. and accordingly, (cf. Section 2.2). We will now show that the creation of endogenous collateral is no longer constrained by the length of the chain, and thus that in the end total collateral and the multipliers are larger than in previous example.

At , the initial total amounts of outgoing collateral are:

| (19) |

Furthermore, at , each bank will re-use a fraction of the additional re-pledgeable collateral that it has received from other banks at the previous time. We thus get:

| (20) |

and in matrix form

| (21) |

where

Notice that , , are respectively the additional amounts of collateral that banks , , and receive from all other banks. Moreover, at , each bank will again re-use a fraction of the additional re-pledgeable collateral that it has received from other banks at time . Therefore,

| (22) |

which in matrix form reads

| (23) |

In general, at , i.e. after times of collateral re-uses, the cumulated amounts of outgoing collateral are:

| (24) |

Expressed differently,

| (25) |

Clearly, the additional collateral in the system is now equal to

Finally, when , we obtain the equilibrium values for and for . Their expressions are the following:

| (26) |

and

| (27) |

To conclude, it is interesting to notice that, as long as and are homogenous across banks, we have the following ranking and .

3.2 Direction of collateral flows, collateral sinks and cycles’ length

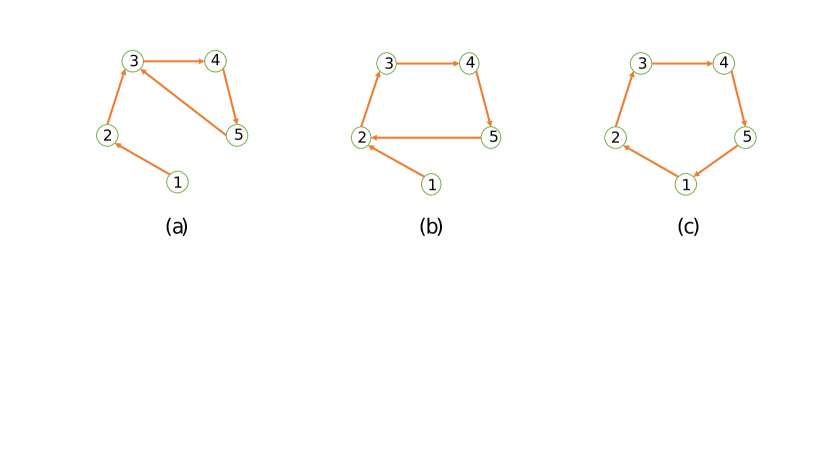

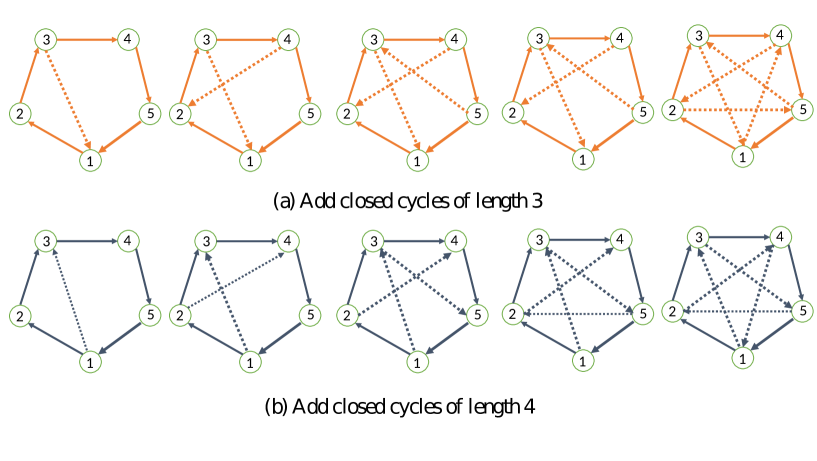

The above examples have clarified what are the fundamental properties that a rehypothecation network must have in order to create endogenous collateral, and thus additional liquidity in the system. In particular, the second example (the a-cyclic chain) makes clear that the possibilities of additional collateral creation are determined by the length of the repledging chains among banks. However, the presence of cycles in networks, like the third example above, allows one to go beyond that, and to maximize the amount of collateral creation. Furthermore, in presence of cyclic networks the direction of collateral flows also matters. In particular, networks wherein collateral flows all end up in a cycle will ceteris paribus create more endogenous collateral than networks where some collateral leaks out from cycles and sinks in some nodes of the system. To better clarify the foregoing statement, we consider in Figure 2, three example networks of five nodes with the same number of links. In addition, in these networks, all out-degrees are positive, and consequently collateral from each node will flow into a cycle after going through some directed edges999It is also possible to show that, as long as all agents have positive out-degree, collateral flows will end up in a cycle after a finite number of steps. For the sake of brevity we do not report this proposition and the related proof. However, it is available from the authors upon request., and there is no leakage from the cycle. The only difference among the three networks is in the length of cycles. Nevertheless, we will show that as long as non-hoarding rates are constant and homogeneous, the three networks generate the same equilibrium total collateral and the have the same equilibrium multiplier. This is summarized in the following proposition.

Proposition 1.

Let . For the networks in panels of Figure (2) .

Proof.

See appendix. ∎

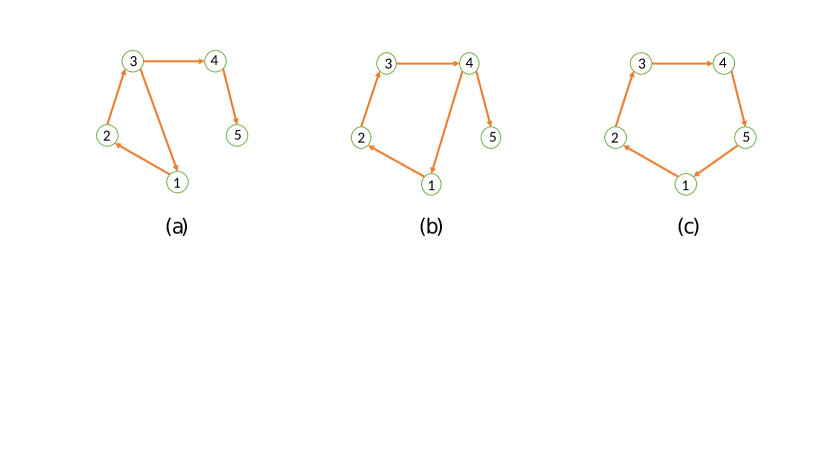

Let us next consider three other examples of rehypothecation process among five banks, the ones in Figure (3). The difference with examples of Figure 2 is that now in panels (a) and (b) one node (i.e. node 5) has zero out-degree. In addition, the network structure in these two panels imply that some collateral leaks out of a cycle and gets stuck at the node with zero out-degree, which then plays the role of “collateral sink”. The consequence is that the three networks will generate different amounts of total equilibrium collateral. This is stated in the following proposition.

Proposition 2.

Let . For the networks in panels of Figure 3,

Proof.

See appendix. ∎

The above two propositions deliver interesting implications about the role of networks’ topology in determining total collateral flows. First, Proposition 2 shows that the total amount of collateral is maximized when the longest possible cycle in the network has been created (a cycle of length 5 in example (c) of Figure 3). At the same time, proposition 1 shows that cycles’ length is irrelevant when collateral sinks are not present in the network and all banks have positive out-degree, i.e. they have at least one repo with some other bank in the system. It also follows that in that case, it might be advantageous frow the viewpoint of total creation of collateral in the network to concentrate collateral flows among few nodes that have a cyclic chain among them. These results provide key insights to understand the behaviour of collateral flows in different network architectures that we shall discuss in the next section. They are also central to understand some of the results about collateral hoarding cascades that we will expose in Section 5.

The next two propositions generalize the above results to any network architecture. The first of them shows that adding an arbitrary number of links to a cycle of length equal to the size of the network does not change neither total collateral nor the value of the multiplier. The second one identifies the upper bounds for the equilibrium values of total collateral and of the collateral multiplier and shows that these upper limits are attained as long as every bank has at least one outgoing link in the network.

Proposition 3.

Consider a rehypothecation network of size . Let and . Adding arbitrary links to an initial cycle of size does not change the values of and . More in general, as long as there is the presence of the largest cycle, and remain unchanged as the density inside that cycle increases.

Proof.

See the appendix. ∎

Proposition 4.

Consider a rehypothecation network of size . Let and . If then equilibrium values of and are equal to the following upper limits:

and

Proof.

See the appendix. ∎

3.3 Network architecture and collateral creation

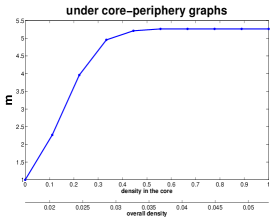

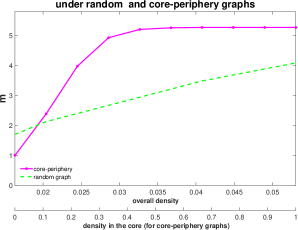

We now address the issue of how does the network structure more in general affects collateral creation. We shall focus on three very different classes of network structures. These classes represent general archetypes of networks in the literature, and they also capture some idealized modes of organization of financial contracts in the market. The first class consists of the closed k-regular graphs of size , , wherein each node has in-coming neighbors as well as out-going neighbors. This archetype corresponds to a market where repo contracts are homogenously spread across banks, so that each bank has exactly the same number of repos and of reverse repos. We consider different types of closed regular graphs of varying levels of density . Special cases of this structure are the cycle of size (where ) and the complete network (), wherein each bank has a repo with every other bank in the network (and vice-versa) and where the number of incoming and outgoing links is the same for all banks and equal to . The second class consists of the random graphs , in which there is a mild degree of heterogeneity in the distribution of financial contracts across banks. Here, the probability of a directed link (and thus of the existence of repo) between every two nodes is equal to the density () of the network. Notice that as the random graph converges to the complete graph. Finally, the third class we examine here consists of core-periphery networks, , where (i) the number of nodes in the core, , is fixed; (ii) each node in the periphery has only out-going links, and all point to nodes in the core; (iii) nodes in the core are also randomly connected among themselves with the probability (), and there are no directed links from the core to the periphery nodes. Notice that the latter type of structure exacerbates heterogeneity in the distribution of financial contracts and it centralizes collateral flows among nodes in the core. This structure is also interesting from an empirical viewpoint as high concentration of collateral flows is often observed in actual markets (see e.g. Singh, , 2011).

We begin our analysis of the three structures by characterizing the behaviour of endogenous collateral formation in the closed k-regular graphs.

Proposition 5.

Let and . A closed-k regular rehypothecation network of size , and a density , always returns the same equilibrium values of total collateral and of collateral multiplier for any density . The equilibrium values are given by the limits stated in Proposition 4.

The above statement follows directly from Proposition 3 above. A closed k-regular of density already embeds the longest possible cycle that is possible to create in a network of size . Accordingly adding further links does not bring any change in equilibrium values of total collateral and of the multipliers, which are always equal to the upper bounds stated in Proposition 4. In contrast to the close k-regular graph, the random network and of core-periphery networks display some variation in total collateral and in the multiplier with for increasing levels of density. The following proposition characterizes the behavior of the latter two variables in these two network structures.101010In the next proposition we determine the equilibrium for bank’s collaterals in the case of an average system, that is instead of considering each single sample of collateral networks we consider the expected value of the amount of collateral for each banks, and solve only for a single average system. For all cases, numerical evidence strongly supports the analytical results.

Proposition 6.

Let and , then:

-

1.

A random graph of size creates more equilibrium collateral and a higher multiplier with higher level of density .

-

2.

A core-periphery graph of of size creates more equilibrium collateral and a higher multiplier with higher level of density of the core.

-

3.

For any graph density , such that a core-periphery graph of creates more equilibrium collateral and a higher multiplier than random graphs for any .

-

4.

As the overall density in the random graph (or the density of the core in the core-periphery graph) goes to 1, the equilibrium values of total collateral and the multiplier converge to the limits stated in Proposition 4.

Proof.

See the appendix. ∎

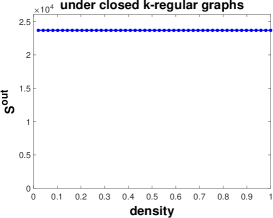

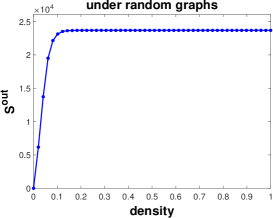

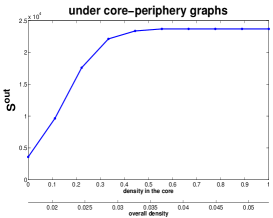

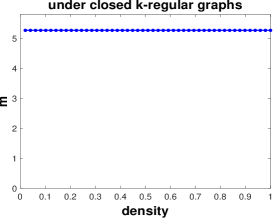

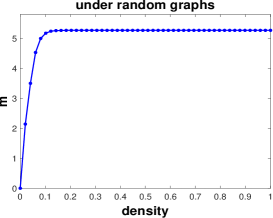

The plots in Figures 4 and 5 help to visualize the results contained in the last two propositions. The plots show equilibrium values of total collateral and of the multiplier resulting from numerical simulations111111The numerical simulation is implemented with , , , and for all banks. using each of the three network topologies examined above (closed k-regular, random graph, and core-periphery) and with different levels density (of for the core-periphery). First, the plots show that both total collateral and the multiplier do not change with the level of density in the closed k-regular graph (plot (a) in both figures). In contrast, both variables increase with the level of density in the random graph and in the core-periphery network (respectively, panels (b) and (c) of the two figures), before eventually converging to the same value of the close k-regular graph (and determined by the expressions in Proposition 4). The main intuition for the latter result is that increasing the level of density (in the overall network or in the core) increases both the number and the length of cycles in the network121212In addition, for the random graph, the number of nodes with positive out-degree also increases with density.. These two factors have a positive impact on endogenous collateral creation in the network, as we explained in Section 3.2. However, when the longest possible cycle in the network (for the random graph) or in the core (for the core-periphery graph) adding further links does not longer increase endogenous collateral. Furthermore, both the third statement of Proposition 6 and the plots in the figures indicate the core-perihery network generates a much higher total collateral than the random graph already with small increases in density. For instance the inspection of Figure 6 reveals that already with banks in the network a tiny increase in overall density (from to ) has the effect of more than doubling the value of the multiplier (from to almost ). In contrast, a much larger change in density is required to produce a similar effect in the random graph. This result generalizes the insights discussed in the previous section (cf. Proposition 1). Once all banks have positive out-degree and they are thus all contributing with outflowing collateral, concentrating all collateral flows in a small cycle (like the one in the core) already generates the largest possible total collateral. This result has also implications for markets organization, as it indicates that concentrating collateral flows among few nodes has great advantages for the velocity of collateral and thus for the overall liquidity of the market. At the same time, in the next section we shall show that - when liquidity hoarding externalities are present - networks with highly concentrated collateral flows are also more exposed to larger collateral hoarding cascades following small local shocks.

4 Value at Risk and Collateral Hoarding

So far we have worked with the assumption that non-hoarding rates were constant across time and homogeneous across banks. This has simplified the analysis and it has allowed us to highlight the role of the characteristics of network topology in determining collateral flows in the financial system. At the same time, this hypothesis is also quite restrictive as banks’ hoarding and non-hoarding might be responsive to the liquidity risk situation of banks and, accordingly, also by the level of available collateral (see e.g. Acharya and Merrouche, , 2010; Berrospide, , 2012; de Haan and van den End, , 2013). In addition, recent accounts of collateral dynamics (Singh, , 2012) have documented the sizeable reduction in velocity of collateral in the aftermath of the last financial crisis as a result of increased collateral hoarding by banks. To account for these important phenomena in this section we extend the basic model presented in Section 2 to introduce time-varying non-hoarding rates determined by liquidity risk considerations.

Again, to keep the model as simple as possible we abstract from many important aspects concerning the liquidity position of the banks. We assume that all funding is secured. For every bank let be its net liquidity position. Recall that the amount of pledgeable collateral of bank that can be used to get external funds with a haircut is . At the same time, if , a fraction of this amount of collateral is already pledged (i.e. an amount of ). The net liquidity position of the bank is thus given by:

| (28) |

where are payments due within the periods, i.e. liquidity shocks, which are assumed to be a i.i.d. normally distributed random variable with mean and standard deviation . The notation emphasizes the fact that the total collateral position of a bank depends also on the fractions of non-hoarded collateral of all banks in the network . Notice that the above equation implies that the more borrowers of hoard collateral, the lower is the value of collateral , and thus the higher the need to hoard collateral for .

Let us start by observing that if the liquidity shock is large enough, bank defaults (i.e. ). This occurs when

Given the assumption on the random variable , the default of is an event occurring with probability

Furthermore, following Adrian and Shin, (2010) and Adrian and Shin, (2014), we assume that each bank employs a Value-at-Risk (VaR) strategy to determine the fraction of collateral to hoard, so that the above probability of default is not higher than a target (where ). If we assume that returns on external assets held by are higher than the repo rate, then each bank will decide the optimal fraction such that

| (29) |

Given that are a i.i.d. normally distributed random variable we have

| (30) |

where erf is Gauss error function defined as

| (31) |

Under the VaR constraint bank sets the share of hoarded collateral at the level such that

| (32) |

| (33) |

| (34) |

where argerf is the inverse error function defined in such that

| (35) |

Equation (34) indicates that is a decreasing function of the VaR target , of the uncertainty about the liquidity shock (captured by ), of the mean of the liquidity shock , and of the haircut rate . Moreover, it is an increasing function of value of the collateral as well as of the shares of non-hoarded collateral of other banks in the network. Denote

| (36) |

we then obtain the following final expression for the optimal under the assumption of normally-distributed liquidity shocks.

| (37) |

Notice that the endogenous level of non-hoarding, , depends now not only on the uncertainty about but also on the haircut rate , as well as on the value of the collateral . The interdependence between and implies that each bank will adjust its hoarding preference (i.e. hold more or less collateral) in anticipation of expected “losses” or “gains” in its total amount of collateral. It also follows that a change in hoarding rates at bank will induce a change in hoarding rates at banks to which is connected to.

We now investigate the existence of equilibria in non-hoarding rates. Let us start by noticing that Equation (37) indicates that, for every bank j, if , its hoarding can in general be expressed as:

| (38) |

where the variable defined by equation (36) captures the effects of uncertainty in on . Since , it follows that must be in . From equation (38), it follows that

| (39) |

Equivalently,

| (40) |

Recall that under the assumption that banks homogenously spread collateral across their lenders, we have

Therefore,

Next, denote by the matrix with size () where

| (41) |

The level of collateral is then obtained by solving the following equation

| (42) |

Finally, the non-hoarded rates can be obtained by substituting into equation (39).

In general, the solution to the system composed by the system of equations in (42) might not be unique. However, the following proposition establishes sufficient conditions for the uniqueness of the solution.

Proposition 7.

Let be a column vector size , given by

| (43) |

Define the matrix with size x as

| (44) |

If and where is the column vector capturing the effects of the net liquidity shock on hoarding preferences, then the system (42) has the unique solution131313Throughout this paper, for any two vectors X and Y of size n, then if :

| (45) |

Proof.

See the appendix. ∎

Finally, by substituting in (45) into equation (39), we obtain the solution to the equilibrium rates of non-hoarded collateral as follows

| (46) |

In the next section, we use the results obtained from the above proposition about the determination of equilibrium banks’ collateral and non-hoarding rates to study the emergence of collateral hoarding cascades under different network structures when some banks are hit by uncertainty shocks, captured by an increase in the variable .

5 Collateral hoarding cascades

We now use the VaR collateral hoarding model developed in the previous section to study how different structures of rehypothecation networks react when a fraction of banks in the network is hit by adverse shocks. In particular we focus on uncertainty shocks141414We also performed analysis of the impact of aggregate shocks to the value of collateral. However, results and the dynamics were similar to the one reported in the paper. that cause the variable in Equation (37) to increase to for some banks , where . The rise in uncertainty will lead those banks to increase their hoarding of collateral. In turn, this will trigger a cascade of hoarding effects at banks that are either directly or indirectly connected to the banks initially it by the uncertainty shock. Indeed, higher hoarding at bank will also cause a loss in the collateral flowing into bank’s neighbors. As a consequence, the latter banks will also increase their hoarding rates, causing further loss in collateral inflows at other banks in the system and thus further adjustments in hoarding rates at other banks in the system. The final result of the foregoing cascade will be a new equilibrium characterized, in general, by a lower level of total collateral in the system. On the grounds of the results stated in Proposition 45 we can determine the new equilibrium vector of collateral in the aftermath of the local uncertainty shock. More formally, let the new vector of uncertainty factors in the aftermath of the local uncertainty shock. By substituting into equations (45) and (43), we obtain the new equilibrium solution, , to at the end of the hoarding cascade as

| (47) |

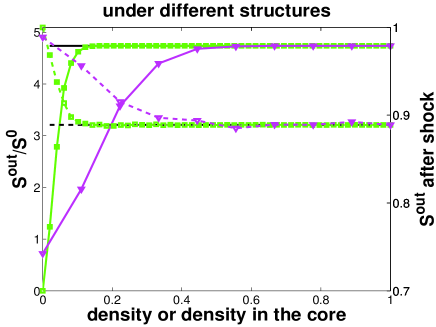

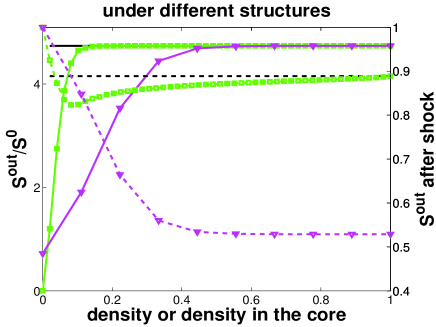

Let us now investigate how after-shock equilibrium collateral of behaves in different networks. The plots in Figure 7 show the pre-shock levels of the ratio between equilibrium total outflowing collateral and total proprietary collateral (left scale). Moreover, they show equilibrium total ouflowing collateral after the shock relative to its pre-shock value (right-scale). The two variables are plotted as functions of network density and for the three different structures examined in Section 3.3, namely the closed k-regular network , the random network , and the core-periphery network . The plots refers to numerical investigations of equilibrium collateral before and after a fraction of banks in the network experiences a increase in the uncertainty factor (so that ) and are performed under two different shocks scenarios. In the first of them (“random attack”, left-side plots) the banks hit by the uncertainty shock are randomly selected. In the second scenario (“targeted attack”, right-side plots) the shocked banks are selected according to their centrality151515We use “PageRank” centrality (see Newman, , 2010; Battiston et al., , 2012, for more details). However, the main conclusions still hold when the degree centrality is employed. in the network (in descending order).161616The other parameters of the simulation where set so that the number of banks is , and , , and for all banks. Notice that the second scenario is relevant only for the random network and for the core-periphery, as all nodes have the same centrality in the closed k-regular network.

The analysis of Figure 7 reveals first that - before the shock - the behaviour of total collateral under the three network structures is the same as the one discussed in Section 3.3 for the case of constant hoarding rates171717Indeed, all the results of Propositions 5 and 6 hold also in the model where hoarding rates are determined according to a VaR criterion. For the sake of brevity, we do not report here these propositions and the related proofs. However, they are available from the authors upon request.. Second, the effects of the local uncertainty shock vary with density only in the random network and in the core-periphery network. In contrast, the loss in total collateral does not change with density in the closed k-regular graph. Third, the overall impact of the shock is very different across the scenarios considered. In particular, the maximal impact is quite small (only a loss) for all the three structures in the random attack scenario. In addition, all the structure generate the same total loss as overall density converges to 1. In contrast, in the targeted attack scenario, the total loss generated in presence of a core-periphery network is much larger than in the other network structures (up to of the initial total collateral value) and increases with density.

Thus, the core-periphery network generates very large losses in collateral when central nodes are hit by local uncertainty shocks. Recall that those nodes are precisely the one concentrating collateral flows, and thus generating the large increases in endogenous collateral stressed in Section 3.3. It follows that the core-periphery network displays a trade-off between liquidity and systemic (liquidity) risk. On the one hand, concentrating collateral flows generates large gains in market liquidity already with a low density of the network. On the other hand, high concentration produces large liquidity losses when small local shock come across. Indeed, by concentrating collateral flows, more central nodes have also a larger impact on collateral at the peripheral nodes that have connections with them, and they thus trigger a must stronger adjustment in hoarding rates thereafter. Notice that these concentration effects underlying the large liquidity losses in the core-periphery network are much smaller in the random graph (where link heterogeneity is small). In addition, they are completely absent in the closed k-regular graph, where all nodes have the same centrality.

To conclude, it is useful to stress that the presence of liquidity hoarding externalities is central for the above results about the trade-off observed in the core-periphery networks. In other terms, targeted local shocks would have a small impact in core-periphery networks if hoarding rates were not responsive to changes in the liquidity positions of banks. To understand why, notice that with constant hoarding rates a loss in collateral value or an exogenous increase in hoarding rates at one bank will only have a -order effect at other banks directly or indirectly connected to it. And this is because the initial shock is dampened by haircut rates and hoarding rates at other banks along the chain. For instance, in the very simple case of the cycle (i.e. closed chain) displayed in Figure 1 (c) a shock to outflowing collateral at node 1 () will have an effect only of order on outflowing collateral at node 3 (see also Equation (22)). In contrast, in the case of VaR-determined hoarding rates, the effect can be large because it is reinforced by the process of agents’ revising their hoarding rates at each step along the rehypothecation chain.181818In particular, in the example of Figure 1 (c) with VaR-based hoarding rates the effect of a shock to on the outflowing collateral of node 3 be of the order

6 Concluding remarks

We have introduced and analyzed a simple model to study collateral flows over a network of repo contracts among banks. We have assumed that, to obtain secured funding, banks may pledge their proprietary collateral or re-pledge the collateral obtained by other banks via reverse repos. The latter practice is known as “rehypothecation” and it has clear advantages for market liquidity as it allows banks to secure more transactions with the same set of collateral. At the same time, re-pledging other banks’ collateral may also raise liquidity risk concerns, as several banks rely on the same collateral for their repo transactions. We have focused on investigating which characteristics of rehypothecation networks are key in order to increase the velocity of collateral flows, and thus increase the liquidity in the market. We have first assumed that banks hoard a constant fraction of their collateral. Under this hypothesis we have shown that characteristics of the network like the length of re-pledging chains, the presence of cyclic chains or the direction of collateral flows are key determinant of the level of endogenous collateral in the system, defined as a overall level of collateral larger than the initial proprietary endowments of banks. In particular, we have shown that the level of endogenous collateral increases with chains’ length. However, cyclic chains allow, ceteris paribus, for a larger endogenous collateral than a-cyclic chains of the same length. Finally, we have shown that endogenous collateral is large already with small cyclic chains if the banks involved centralize collateral flows. The foregoing features of network topology underlie the results about the determination of total collateral in more general network architectures. In particular, we showed that total collateral increases with density in the random network (displaying a mild heterogeneity in collateral flows across banks) and in the core-periphery networks (displaying high concentration of collateral flows). Nevertheless, core-periphery networks generate larger collateral than random networks already with smaller increase in the density of the network. The foregoing results have implications for the micro-structure of markets where collateral is important, as they highlight a new factor besides network density - i.e. concentration in collateral flows - that allows for significant gains in market liquidity. A market with highly concentrated collateral flows generates higher velocity of collateral, as it is thus more liquid, even if banks are not tied by a dense network of financial contracts.

Furthermore, we have extended the model to allow for endogenous levels of hoarding rates that depend on the liquidity position of each bank in the network. More precisely, we assumed that banks set their hoarding rates by adopting a Value-at-Risk criterion aimed at minimizing the risk of liquidity defaults. We have shown that, in these framework, hoarding rates of each single bank are in general dependent on other banks’ rates and collateral levels, a feature which introduces important collateral hoarding externalities in the analysis. We have then used the above framework to study the overall impact on collateral flows of local adverse shocks leading to an increase in payments’ uncertainty at some banks in the market, in particular investigating how the response may vary with the topology of the rehypothecation network. We have highlighted that core-periphery networks generate larger losses in overall collateral compared to other network structures (closed k-regular network, random network) when the nodes experiencing the shock are the most central nodes in the network, i.e. the ones concentrating collateral flows. This result has interesting implications for the regulatory analysis of markets with collateral, as it shows that the same network structures allowing for the largest increase in collateral velocity - i.e. core-periphery networks - are also the ones more exposed to largest collateral hoarding cascades in case of local shocks. A trade-off between liquidity and systemic (liquidity) risk thus emerges in those networks. In addition, our results also suggest that - in the presence of rehypothecation - regulatory liquidity and collateral requirements imposed to banks need to account for the structure of the network of lending contracts across banks. In particular, such requirements should both account for the systemic role (e.g. centrality) of the banks in the collateral flow network, as well as account for the whole topology of the network (e.g. for the presence of hierarchical structures such as the core-periphery architecture).

Our work could be extended at least in three ways. First, in these work we have abstracted from many important aspects of real-world secured lending markets, such as heterogeneous collateral quality and endogenous haircut rates. Introducing these elements could probably enrich our results. In particular, in the model the haircut rate affects the extent of rehypothecation. Accordingly, endogenous haircut rates that reflect different levels of counterparty risk can be an additional source of externalities in the model. Second, we have used the Value at Risk criterion to determine hoarding rates in our model. However, hoarding rates may also result from liquidity requirements imposed to banks. It would then be interesting to extend the model to study how different requirements that have been proposed so far may impact on market liquidity in presence of rehypothecation, and how these requirements should be designed in order to minimize the liquidity-systemic risk trade-off that we highlighted above. Finally, we have focused on bilateral repo contracts. However, it would be interesting to study how our results might change in presence of try-party repo structures, and in the presence of central clearing counterparties that interact with banks re-using their collateral.

Acknowledgments

We are indebted to Joseph E. Stiglitz, Stephen G. Cecchetti, Sérafin Jaramillo, Dilyara Salakhova, Marco D’Errico, Guido Caldarelli, for valuable comments and discussions that helped to improve the paper. We also thank participants to the various conferences where earlier versions of this paper were presented. These include the Second Conference on Network Models and Stress Testing for Financial Stability, Banco de México, September 26-27, 2017, the Conference on Complex System 2017 (CCS 2017), in Cancún, September 17-22, 2017, the first and second FINEXUS Conference, Zürich (January 2017, January 2018), the 22nd Workshop on Economic Science with Heterogeneous Interacting Agents (WEHIA 2017), Catholic University of Milan, June 12-14, 2017, and the 23rd Computing in Economics and Finance (CEF 2017), Fordham University, New York City, June 28-30, 2017. We also participants to seminars at the Jaume I University, Castellòn de la Plana (Spain) in November 2017 and to the Catholic University of Milan, in December 2017. All usual disclaimers apply. The authors gratefully acknowledge the financial support of the Horizon 2020 Framework Program of the European Union under the grant agreement No. 640772 - Project DOLFINS (Distributed Global Financial Systems for Society).

References

- Acharya and Merrouche, (2010) Acharya, V. and Merrouche, O. (2010). Precautionary hoarding of liquidity and inter-bank markets: Evidence from the sub-prime crisis. Working Paper 16395.

- Adrian and Shin, (2010) Adrian, T. and Shin, H. S. (2010). Liquidity and leverage. Journal of Financial Intermediation, 19(3):418–437.

- Adrian and Shin, (2014) Adrian, T. and Shin, H. S. (2014). Procyclical leverage and value-at-risk. Review of Financial Studies, 27(2):373– 403.

- Aguiar et al., (2016) Aguiar, A., Bookstaber, R., Kenett, D. Y., and Wipf, T. (2016). A map of collateral uses and flows. Journal of Financial Market Infrastructures, 5(2):1–28.

- Andolfatto et al., (2017) Andolfatto, D., Martin, F. M., and Zhang, S. (2017). Rehypothecation and liquidity. European Economic Review, 100:488–505.

- Battiston et al., (2016) Battiston, S., Farmer, J. D., Flache, A., Garlaschelli, D., Haldane, A. G., Heesterbeek, H., Hommes, C., Jaeger, C., May, R., and Scheffer, M. (2016). Complexity theory and financial regulation. Science, 351(6275):818–819.

- Battiston et al., (2012) Battiston, S., Puliga, M., Kaushik, R., Tasca, P., and Caldarelli, G. (2012). Debtrank: Too central to fail? financial networks, the fed and systemic risk. Scientific reports, 2:541.

- Berrospide, (2012) Berrospide, J. (2012). Precautionary hoarding of liquidity and inter-bank markets: Evidence from the sub-prime crisis. Working Paper.

- Bottazzi et al., (2012) Bottazzi, J.-M., Luque, J., and Páscoa, M. R. (2012). Securities market theory: Possession, repo and rehypothecation. Journal of Economic Theory, 147(2):477–500.

- Brunnermeier and Pedersen, (2008) Brunnermeier, M. K. and Pedersen, L. H. (2008). Market liquidity and funding liquidity. The Review of Financial Studies, 22(6):2201–2238.

- Capel and Levels, (2014) Capel, J. and Levels, A. (2014). Collateral optimisation, re-use and transformation: Developments in the dutch financial sector. DNB Occasional Studies, 12(5):1––54.

- de Haan and van den End, (2013) de Haan, L. and van den End, J. W. (2013). Banks’ responses to funding liquidity shocks: Lending adjustment, liquidity hoarding and fire sales. Journal of International Financial Markets, Institutions and Money, 26:152–174.

- (13) Financial Stability Board (2017a). Non-cash collateral re-use: Measure and metrics. 25 January:1–17.

- (14) Financial Stability Board (2017b). Re-hypothecation and collateral re-use: Potential financial stability issues, market evolution and regulatory approaches. 25 January:1–42.

- Gai et al., (2011) Gai, P., Haldane, A., and Kapadia, S. (2011). Complexity, concentration and contagion. Journal of Monetary Economics, 58:453–470.

- Gorton and Metrick, (2012) Gorton, G. and Metrick, A. (2012). Securitized banking and the run on repo. Journal of Financial economics, 104(3):425–451.

- Gottardi et al., (2017) Gottardi, P., Maurin, V., and Monnet, C. (2017). A theory of repurchase agreements, collateral re-use, and repo intermediation. CESifo Working Paper Series 6579, CESifo Group Munich.

- Leitner, (2011) Leitner, Y. (2011). Why do markets freeze? Business Review, Federal Reserve Bank of Philadelphia, (Q2):12–19.

- Monnet, (2011) Monnet, C. (2011). Rehypothecation. Business Review, Federal Reserve Bank of Philadelphia, (Q4):18–25.

- Newman, (2010) Newman, M. (2010). Networks: an introduction. Oxford university press.

- Pozsar and Singh, (2011) Pozsar, Z. and Singh, M. (2011). The nonbank-bank nexus and the shadow banking system. Working Paper 11-289, International Monetary Fund.

- Singh, (2011) Singh, M. (2011). Velocity of pledged collateral: analysis and implications. IMF Working Paper 11/256.

- Singh, (2012) Singh, M. (2012). The (other) deleveraging. IMF Working Paper 12/179.

- Singh, (2016) Singh, M. (2016). Collateral and financial plumbing. Risk Books.

7 Appendix: Proofs of Propositions

Proof of proposition 1

Let us start by remarking that, in all cases shown in Figure (2), we have (), and thus () and

| (48) |

In the case of Figure 2 (b), the length of the closed cycle is 4, and now the dynamics of is governed by the following system

| (51) |

We obtain

| (52) |

with

In the third case, with the the closed cycle of length 5 (Figure 2 (c)), the dynamics of is governed by the following system

| (53) |

We obtain

| (54) |

with

It can be easily shown that given (i.e. under the condition of homogeneous hoarding), all panels in Figure (2) create the same amount of for all . This is because in all cases of we have the same dynamics and they also all have the same initial aggregate amount of outgoing collateral, i.e. . In addition, in all panels of Figure (2) we have that . Thus, at the fixed point solution to , is equal to .

Proof of proposition 2 In the case represented by Figure 3 (a), , therefore

| (55) |

The dynamics of will follow

| (56) |

It follows that

| (57) |

with

In the case represented by Figure 3 (b), we still have that

| (58) |

The dynamics of will follow

| (59) |

We obtain

| (60) |

with

Furthermore, in the case represented by Figure 3 (c), as shown in (48) and (54), we have

Thus

with

We can see that the main difference between Figure 3 (a) and Figure 3 (b) is mathematically expressed by the difference between and : in the former case, a part of the initial outgoing collateral from the bank is flowing into the cycle, while in the later case all outgoing collateral from the bank will stuck in the box of the bank and can not be re-used. In addition, comparing these cases to the one represented by Figure 3 (c), we can see that in Figure 3 (c) the initial outgoing collateral from each bank can be re-used infinitely. Defining , , and are respectively the total amount of outgoing collateral of all banks in Figures 3 (a), (b), and (c) after t times of using and re-using collateral, it can be proved by induction that . This implies that in contrast to the example illustrated in Figure (2), now longer cycles will generate more endogenous collateral.

Proof of proposition 3.

To illustrate this proposition, without loss of generality we show an example of closed cycle of length in Figure (8). We can add arbitrary links or cycles of length to the initial graph. In all examples shown in Figure (8), we always have that for every bank . Proposition (3) is therefore just a special case of Proposition 4, of which we will provide the proof later.

Proof of proposition 4.

First, since , hence (). Accordingly, we have and . Therefore,

In addition, since each column191919Now all columns are non-zero since for all . of the matrix of shares is summing to 1 and thus (), at the fixed point solution to , we always have

Equivalently,

Hence,

| (61) |

Proof of proposition 6.

Recall that under the basic model with homogeneous we have

where

Therefore,

| (62) |

where the notation stands for the expectation of . With the shares defined as in equation (1) in the main text, we have

| (63) |

with is the probability that and is the probability that .

Under random graphs with a probability of a link between any two nodes (i.e. ), for every it is easy to show that and . In addition, . That leads to

| (64) |

From equation (64) we have202020We use the approximation .

| (65) |

and the following approximation212121We use the approximation .

| (66) |

Thus,

| (67) |

Note that

| (68) |

Consequently,

| (69) |

and

| (70) |

Hence,

| (71) |

and

| (72) |

Moreover, we can easily show that the approximations for , , and are increasing functions of the network density . In addition, given in , these measures are also increasing functions of the size of the network, .

We now proceed with proving the second part of the proposition. We consider a core-periphery graphs in which: (i) the number of nodes in the core, , is fixed; (ii) each node in the periphery has only out-going links, and all point to nodes in the core; (iii) each node in the core are also randomly connected to each other with the probability , and there are no directed links from the core to the periphery nodes.

To begin, we first consider the behavior of nodes in the periphery part (Per). For every node in the periphery, we have

and

Therefore,

| (73) |

and

| (74) |

Equations (73) and (74) imply that the aggregate amounts of in-flowing and out-going collateral of all nodes in the periphery remain constant during rehypothecation process. This observation is intuitive since we assume that periphery banks are purely borrowers and therefore they do not receive collateral from other banks.

Moving on to the core part, for every bank in the core part (Core) we have

| (75) |

Taking the expectation from both sides, we have

| (76) |

Defining

| (77) |

then we have

| (78) |

Equations (77) and (75) respectively imply two important characteristics of the rehypothecation of collateral under the considered core-periphery structure, i.e. the concentration into the core part and the reuse of collateral among banks in the core.

In addition, since each non-zero column of the matrix of shares is summing to 1, it is easy to show that

| (79) |

Since nodes in the core are assumed to be randomly connected with the density , using the results obtained from random graphs we have

| (80) |

Note that, for every node in the core part

| (82) |

Therefore

| (83) |

and

| (84) |

| (85) |

which can be simplified as

| (86) |

Moreover, the expectation of the aggregate amount of initial out-going collateral is

| (87) |

As results,

| (88) |

and

| (89) |

Again, it can be shown that , and the approximation for are increasing functions of the density of the core . In addition, these three measures are also increasing functions of the size of the core part, , given in . Comparing the multiplier estimated for core-periphery graphs, as in equation (88) and with the one estimated for random graphs as in equation (71), we notice that the former is always larger than the latter, as long as , thus verifying the third part of the proposition. Finally, by inspecting equations (72) and (89) we verify the fourth and final part of the proposition.

Proof of proposition 45.

We will now provide detailed derivations for the equilibrium existence to non-hoarded parameters determined under the Value-at-Risk strategy. To begin, let us start with the following definitions:

Definition 1.

For each column vector , (where ), the elements of the matrix (size ) is defined as

| (90) |

We now show that the following system of equations

| (91) |

has a single unique solution if and , where is a column vector size , with

| (92) |

and

| (93) |

with the matrix of shares, , is defined as in equation (1) in the main text.

Notice that

| (94) |

| (95) |

Equivalently,

| (96) |

If is an invertible matrix, system (96) has a single unique solution

| (97) |

We now show the invertibility of by reductio ad absurdum. Suppose that is not invertible, then . Note that therefore if and only if is an eigenvalue of . However, since each non-zero column of is summing to 1, according to Perron-Frobenius theorem, the largest eigenvalue of can not be larger than 1.