On the Evolution of Cryptocurrency Market Efficiency

Abstract: This study examines whether the efficiency of cryptocurrency markets (Bitcoin and Ethereum) evolve over time based on Lo’s (2004) adaptive market hypothesis (AMH). In particular, we measure the degree of market efficiency using a generalized least squares-based time-varying model that does not depend on sample size, unlike previous studies that used conventional methods. The empirical results show that (1) the degree of market efficiency varies with time in the markets, (2) Bitcoin’s market efficiency level is higher than that of Ethereum over most periods, and (3) a market with high market liquidity has been evolving. We conclude that the results support the AMH for the most established cryptocurrency market.

Keywords: Cryptocurrency Markets; Adaptive Market Hypothesis; Efficient Market Hypothesis; GLS-Based Time-Varying Model Approach; Degree of Market Efficiency.

JEL Classification Numbers: G12; G14.

1 Introduction

Since Nakamoto’s (2008) description of a digital cryptocurrency named Bitcoin, cryptocurrency markets have expanded, and their total market capitalization reached USD 800 billion by January 2018. However, these markets have subsequently experienced a crisis, and their total market capitalization decreased to USD 100 billion by the end of 2018.111The historical data for total market capitalization are available at the web page of CoinMarketCap (https://coinmarketcap.com/charts/). As such, the changes in market capitalization suggest that investors treat cryptocurrencies as an asset – but this does not necessarily mean they do not also treat it as, say, a currency. Further, economists consider investigating the efficiency of the cryptocurrency market in the sense of Fama (1970) to be essential for evaluating the price mechanism of financial markets. Therefore, several recent studies on cryptocurrency markets have aimed to determine whether these markets are efficient.

There exists a large body of literature on the weak-form of Fama’s (1970) efficient market hypothesis (EMH) for cryptocurrency markets, especially the Bitcoin market.222As described in Malkiel (1992, p. 739), markets are said to be efficient in the weak-form sense if the information set only includes the history of prices or returns. However, the market efficiency of cryptocurrency has been a subject of controversy between the proponents and opponents of the EMH. For example, Urquhart (2016), Nadarajah and Chu (2017), Bariviera (2017), Khuntia and Pattanayak (2018), Kristoufek (2018), Tiwari et al. (2018), and Dimitrova et al. (2019) conclude that the Bitcoin market is almost efficient. In contrast, Yonghong et al. (2018), Cheah et al. (2018), Al-Yahyaee et al. (2018), and Vidal-Tomás et al. (2019) present empirical results that do not support the EMH for this market. We suspect that one of the reasons for this controversy is that market efficiency varies over time. In this context, Lo (2004) proposes the adaptive market hypothesis (AMH) as an evolutionary alternative to the EMH, reinforcing the view that the market evolves over time, as does market efficiency. The most important implication of the AMH is that market efficiency can arise from time to time due to changing market conditions such as behavioral bias, structural change, and external events. Specifically, Lo estimates the time-varying first-order autocorrelation of returns on the U.S. stock market using 60-month rolling windows and shows that stock market efficiency continuously evolves over time. His empirical results suggest that the AMH may be supported by not only the stock market but also other financial markets.

To examine the AMH, two approaches have been adopted in the literature. The first is based on a conventional statistical test to examine the AMH under the split samples or the rolling-window method. In practice, Urquhart (2016), Nadarajah and Chu (2017), Khuntia and Pattanayak (2018), Kristoufek (2018), Chu et al. (2019), Dimitrova et al. (2019), and Vidal-Tomás et al. (2019) employ conventional statistical tests under the split samples to examine the AMH for the Bitcoin market. In particular, Khuntia and Pattanayak (2018) and Chu et al. (2019) are related to this study because they employ a family of Domínguez and Lobato’s (2003) test statistics to explore whether the Bitcoin price follows the martingale difference sequences. Khuntia and Pattanayak (2018) show the time-varying return predictability in the Bitcoin market using a family of Domínguez and Lobato’s (2003) test statistics in a rolling-window framework and conclude that market efficiency evolves with time and validates the AMH in bitcoin market. Chu et al. (2019) test the AMH in a similar manner to Khuntia and Pattanayak (2018) using high-frequency data and find that the AMH is supported in the Bitcoin market.

However, these methods have the underlying empirical problem of choosing an optimal window width for the test statistics. Unlike these methods, a GLS-based time-varying model, which is the second approach to examining the AMH, has the superior property that it does not depend on sample size. In this approach, the degree of market efficiency is measured together with its statistical inference. Some studies employ a generalized least squares (GLS)-based time-varying model to estimate the degree of market efficiency on the international stock markets.333See Ito et al. (2014, 2016) and Noda (2016) for details. Noda (2016) tests the AMH using Japanese stock market data and concludes that the degree of market efficiency varies with time.

As such, this study examines the AMH on cryptocurrency markets from the viewpoint of market efficiency based on two representative cryptocurrencies, Bitcoin and Ethereum. We choose these currencies because their market capitalization accounts for a large portion of the total market capitalization in the cryptocurrency markets. We first estimate the degree of market efficiency using the GLS-based time-varying model with statistical inferences. Second, we analyze the changes in their degrees of market efficiency over time and whether they show different efficiencies depending on trading volume and market capitalization. Finally, we explore what types of markets support the AMH based on the degree of market efficiency, independent of sample size.

This paper is organized as follows. Section 2 presents our method to study market efficiency varying over time based on a GLS-based time-varying model of Ito et al. (2014, 2016, 2017). Section 3 describes the daily prices of cryptocurrencies (Bitcoin and Ethereum) to calculate the returns and presents preliminary unit root test results. Section 4 shows our empirical results and discusses whether the AMH is supported in the cryptocurrency markets from the viewpoint of time-varying market efficiency. Section 5 concludes the article.

2 Method

2.1 GLS-Based Time-Varying AR Model

We employ a GLS-based time-varying autoregressive (TV-AR) model from Ito et al. (2014, 2016, 2017) to analyze financial data whose data-generating process is time-varying. The conventional AR model,

has been frequently used to analyze the time series of the returns of assets, where satisfies , , and . While ’s are assumed to be constant in standard time series analyses, we assume that the coefficients of the AR model change over time. We thus apply a GLS-based TV-AR model to analyze cryptocurrency markets because financial markets have been facing structural changes for several reasons, such as economic/political crises.444See Lim and Brooks Lim and Brooks (2011) for details.

A GLS-based TV-AR model is expressed as follows:

| (1) |

where satisfies , , and . Furthermore, we assume that parameter dynamics restrict the parameters when we estimate a GLS-based TV-AR model using such data, in particular,

| (2) |

where satisfies , and . We solve a system of simultaneous equations using Equations (1) and (2).

According to Ito et al. (2014, 2016, 2017), a GLS-based TV-AR model has two major advantages over the conventional Bayesian method (e.g., Kalman filtering and smoothing). First, this method is fairly simple and the calculation is fast. Unlike the conventional Bayesian method, no iteration by Markov chain Monte Carlo (MCMC) algorithms is required. Second, prior distributions of parameters are unnecessary when we employ a GLS-based TV-AR model. We can thus employ conventional statistical inferences (e.g., residual-based bootstrap method) on the time-varying estimates to conduct statistical inferences.

2.2 Time-Varying Degree of Market Efficiency

We first calculate the time-varying impulse responses from TV-AR coefficients over each period. We then calculate the confidence intervals for each coefficient based on the estimated covariance matrix. While the concept of a GLS-based TV-AR model is quite simple, two caveats exist: (1) a GLS-based TV-AR model is only an approximation of the real data-generating process, which is supposed to be a complex nonstationary process; and (2) we assume the estimated stationary model index by period , which is stationary, as a local approximation of the underlying complex process.

We define the time-varying degree of market efficiency based on Ito et al. (2014, 2016) as follows:

| (3) |

We measure the deviation from the zero coefficients on the corresponding time-varying moving-average model to the TV-AR model. Hence, this implies that large deviations of from zero are evidence of market inefficiency. We know that that degree crucially depends on sampling errors. Thus, we construct confidence intervals for ’s on the condition that the market is efficient. We find the market at time period is inefficient when exceeds the upper limit at the period of the intervals.

Specifically, the interval is constructed as follows. We first identify the returns with the residuals of a TV-AR() estimation under the above hypothesis that all coefficients are zero. Second, samples are extracted as an empirical distribution of the residuals. Third, we fit a TV-AR model to the bootstrap samples and derive sets of estimates. The bootstrap samples of are then computed from the estimates. Finally, we construct confidence intervals from the bootstrap samples. Therefore, the bootstrap is conducted under the null hypothesis of zero autocorrelation. The estimates of the degree of efficiency exceed the 99% confidence intervals, which implies a rejection of the null hypothesis of no return autocorrelation at the 1% significance level.

3 Data

We utilize the daily prices of Bitcoin (BTC) and Ethereum (ETH) obtained from the CoinMarketCap website (https://coinmarketcap.com). The datasets of the two cryptocurrencies have different start dates: April 28, 2013, for BTC and August 7, 2015, for ETH. On the other hand, the end dates are the same for both cryptocurrencies (September 30, 2019). We take the log first difference of the time series of prices to obtain the returns of the cryptocurrencies.

(Table 1 around here)

Table 1 shows the descriptive analysis for the returns. We confirm that the standard deviation of returns on the BTC is lower than those of ETH. This means that the BTC is a more established and unrisked market than ETH because a lower standard deviation of returns indicates better liquidity. For estimations, all variables that appear in the moment conditions should be stationary. We apply the augmented Dickey–Fuller (ADF) test to confirm whether the variables satisfy the stationarity condition. The ADF test rejects the null hypothesis that the variables (all returns) contain a unit root at the 1% significance level.

4 Empirical Results

We apply the GLS-based TV-AR model from Ito et al. (2014, 2016, 2017) to obtain the degree of market efficiency. Note that we employ the Bayesian information criterion to select the optimal lag order for the stationary AR() model. Consequently, we choose the AR(6) model for both cryptocurrencies. We measure the cryptocurrency markets’ deviation from the efficient condition using Equation (3) because the degree is based on the spectral norm. The degree of market efficiency thus indicates how the market is different from an efficient market. If for time , the market is shown to be efficient at that time.

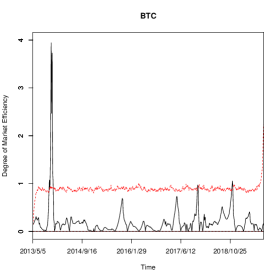

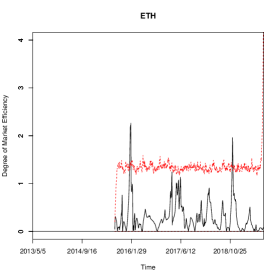

Figure 1 indicates the degree of market efficiency based on the above TV-AR models. We first find that the degrees of the BTC and ETH change over time. Figure 1 also demonstrates that the markets are inefficient during some crash or crisis periods. In practice, these correspond with the rapid price decreases of cryptocurrencies (December 2017 and November 2018) and a financial crisis due to “Mt. Gox” from November 2013 to February 2014.

(Figure 1 around here)

We confirm three significant differences among the cryptocurrencies in terms of their degrees of market efficiency. First, since August 14, 2015, BTC has been the most efficient cryptocurrency in the sense of the degree of market efficiency , being followed by ETH. The average of BTC and ETH are 0.19 and 0.30, respectively. We also compare the s over the same sample period because the periods are different between currencies. The average of BTC is 0.20 using the entire sample for reference. ETH’s fluctuates more widely than that of BTC. In fact, the standard deviations of the s of BTC and ETH are 0.18 and 0.32, respectively. Third, BTC’s was less volatile since the financial crisis due to “Mt. Gox” from November 2013 to February 2014, but that of ETH was not.

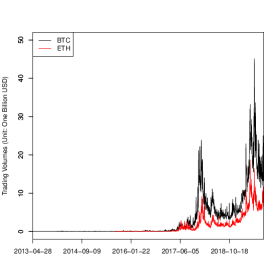

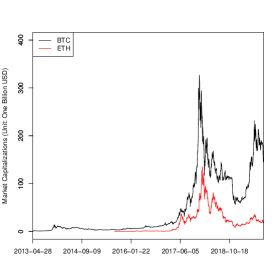

The differences between the BTC and ETH in terms of trading volumes, market capitalization, and percentage of total market capitalization (dominance) might explain these differences in the degree of market efficiency , as shown in Brauneis and Mestel (2018), Wei (2018), and Khuntia and Pattanayak (2020).

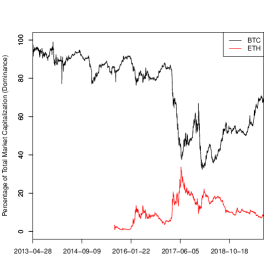

Figure 2 demonstrates that trading volumes and market capitalizations are quite different between BTC and ETH. Additionally, it is widely known that the market capitalization of BTC and ETH accounts for a large portion of the total market capitalization of the cryptocurrency market. Figure 3 indicates the changes in the percentage of total market capitalization (dominance) for BTC and ETH. We confirm that the degree of market efficiency of BTC and ETH declines when the dominance changes drastically (early 2017, late 2017, and late 2018). This means that the dominance and trade openness among cryptocurrencies may affect the market efficiency. Empirically, Khuntia and Pattanayak (2020) confirm the time-varying or adaptive behavior of long memory in the volatility of Bitcoin returns and conclude that the long memory of the volatility of returns can be explained by trading volume.555In a different context, Lim and Kim (2011) and Noda (2016) show that trade openness is associated with the market efficiency of stock markets.

Moreover, the empirical results are consistent with Urquhart (2016), who shows that market efficiency improves after late 2013 when using sub-sample estimation. In particular, we find that the degree of market efficiency of BTC sometimes declines relatively (e.g., late 2015, early 2017, and early 2018), but it does not achieve the level of an absolutely inefficient market with the exception of a period of rapid price decrease in late 2018. Conversely, that of ETH fluctuates widely and often reaches the level of absolute inefficiency (e.g., early 2016, mid-2017, and late 2018). This implies that the BTC market reflects shock, whereas the ETH market does not. Thus, the empirical results support the AMH on the more qualified cryptocurrency market as shown in Khuntia and Pattanayak (2018) and Chu et al. (2019), which examine the AMH on the Bitcoin market.

5 Concluding Remarks

In this study, we investigate whether the cryptocurrency markets (Bitcoin and Ethereum) evolve over time, based on Lo’s (2004) AMH. Particularly, we estimate the degree of market efficiency based on a GLS-based time-varying model of Ito et al. (2014, 2016, 2017). The empirical results show that (1) cryptocurrency market efficiency varies with time, (2) the market efficiency of the BTC is higher than that of the Ethereum in most periods, and (3) the market has been evolving with high market liquidity. Therefore, we conclude that the empirical results support the AMH for the more established cryptocurrency market.

Acknowledgments

The author would like to thank the Co-Editor, David Peel, an anonymous referee, Mikio Ito, Tatsuma Wada, and the conference participants at the 94th Annual Conference of the Western Economic Association International for their helpful comments and suggestions. The author is also grateful for the financial assistance provided by the Murata Science Foundation and the Japan Society for the Promotion of Science Grant in Aid for Scientific Research, under grant numbers 17K03809, 17K03863, 18K01734, and 19K13747. All data and programs used are available upon request.

References

- Al-Yahyaee et al. (2018) Al-Yahyaee, K. H., Mensi, W., and Yoon, S. M. (2018), “Efficiency, Multifractality, and the Long-Memory Property of the Bitcoin Market: A Comparative Analysis with Stock, Currency, and Gold Markets,” Finance Research Letters, 27, 228–234.

- Bariviera (2017) Bariviera, A. F. (2017), “The Inefficiency of Bitcoin Revisited: A Dynamic Approach,” Economics Letters, 161, 1–4.

- Brauneis and Mestel (2018) Brauneis, A. and Mestel, R. (2018), “Price Discovery of Cryptocurrencies: Bitcoin and Beyond,” Economics Letters, 165, 58–61.

- Cheah et al. (2018) Cheah, E.-T., Mishra, T., Parhi, M., and Zhang, Z. (2018), “Long Memory Interdependency and Inefficiency in Bitcoin Markets,” Economics Letters, 167, 18–25.

- Chu et al. (2019) Chu, J., Zhang, Y., and Chan, S. (2019), “The Adaptive Market Hypothesis in the High Frequency Cryptocurrency Market,” International Review of Financial Analysis, 64, 221–231.

- Dimitrova et al. (2019) Dimitrova, V., Fernández-Martínez, M., Sánchez-Granero, M., and Trinidad Segovia, J. (2019), “Some Comments on Bitcoin Market (in)Efficiency,” PLOS ONE, 14.

- Domínguez and Lobato (2003) Domínguez, M. A. and Lobato, I. N. (2003), “Testing the Martingale Difference Hypothesis,” Econometric Reviews, 22, 351–377.

- Fama (1970) Fama, E. F. (1970), “Efficient Capital Markets: A Review of Theory and Empirical Work,” Journal of Finance, 25, 383–417.

- Ito et al. (2014) Ito, M., Noda, A., and Wada, T. (2014), “International Stock Market Efficiency: A Non-Bayesian Time-Varying Model Approach,” Applied Economics, 46, 2744–2754.

- Ito et al. (2016) — (2016), “The Evolution of Stock Market Efficiency in the US: A Non-Bayesian Time-Varying Model Approach,” Applied Economics, 48, 621–635.

- Ito et al. (2017) — (2017), “An Alternative Estimation Method of a Time-Varying Parameter Model,” [arXiv:1707.06837], Available at https://arxiv.org/pdf/1707.06837.pdf.

- Khuntia and Pattanayak (2018) Khuntia, S. and Pattanayak, J. (2018), “Adaptive Market Hypothesis and Evolving Predictability of Bitcoin,” Economics Letters, 167, 26–28.

- Khuntia and Pattanayak (2020) — (2020), “Adaptive Long Memory in Volatility of Intra-day Bitcoin Returns and the Impact of Trading Volume,” Finance Research Letters, 32, 101077.

- Kristoufek (2018) Kristoufek, L. (2018), “On Bitcoin Markets (in)Efficiency and its Evolution,” Physica A: Statistical Mechanics and its Applications, 503, 257–262.

- Lim and Brooks (2011) Lim, K. P. and Brooks, R. (2011), “The Evolution of Stock Market Efficiency Over Time: A Survey of the Empirical Literature,” Journal of Economic Surveys, 25, 69–108.

- Lim and Kim (2011) Lim, K. P. and Kim, J. H. (2011), “Trade Openness and the Informational Efficiency of Emerging Stock Markets,” Economic Modelling, 28, 2228–2238.

- Lo (2004) Lo, A. W. (2004), “The Adaptive Markets Hypothesis: Market Efficiency from an Evolutionary Perspective,” Journal of Portfolio Management, 30, 15–29.

- Malkiel (1992) Malkiel, B. G. (1992), “Efficient Market Hypothesis,” in The New Palgrave Dictionary of Money & Finance, eds. Newman, P., Milgate, M., and Eatwell, J., MacMillan Press, pp. 739–744.

- Nadarajah and Chu (2017) Nadarajah, S. and Chu, J. (2017), “On the Inefficiency of Bitcoin,” Economics Letters, 150, 6–9.

- Nakamoto (2008) Nakamoto, S. (2008), “Bitcoin: A Peer-to-Peer Electronic Cash System,” Online Available at https://bitcoin.org/bitcoin.pdf.

- Noda (2016) Noda, A. (2016), “A Test of the Adaptive Market Hypothesis using a Time-Varying AR Model in Japan,” Finance Research Letters, 17, 66–71.

- Tiwari et al. (2018) Tiwari, A. K., Jana, R., Das, D., and Roubaud, D. (2018), “Informational Efficiency of Bitcoin–An Extension,” Economics Letters, 163, 106–109.

- Urquhart (2016) Urquhart, A. (2016), “The Inefficiency of Bitcoin,” Economics Letters, 148, 80–82.

- Vidal-Tomás et al. (2019) Vidal-Tomás, D., Ibáñez, A. M., and Farinós, J. E. (2019), “Weak Efficiency of the Cryptocurrency Market: a Market Portfolio Approach,” Applied Economics Letters, 26, 1627–1633.

- Wei (2018) Wei, W. C. (2018), “Liquidity and Market Efficiency in Cryptocurrencies,” Economics Letters, 168, 21–24.

- Yonghong et al. (2018) Yonghong, J., He, H., and Weihua, R. (2018), “Time-Varying Long-Term Memory in Bitcoin Market,” Finance Research Letters, 25, 280–284.

| Mean | SD | Min | Max | ADF | Lag | ||

|---|---|---|---|---|---|---|---|

| 0.0018 | 0.0431 | -0.2662 | 0.3575 | -34.5442 | 1 | 2346 | |

| 0.0028 | 0.0731 | -1.3021 | 0.4123 | -20.2283 | 2 | 1515 |

Notes:

-

(1)

“ADF” denotes the ADF test statistics and “Lag” denotes the lag order selected by the BIC.

-

(2)

In computing the ADF test, a model with a time trend and constant is assumed. The critical value at the 1% significance level for the ADF test is “”.

-

(3)

“” denotes the number of observations.

-

(4)

R version 3.6.3 was used to compute the statistics.

Notes:

-

(1)

The panels of the figure show the time-varying degree of market efficiency for BTC (left panel) and ETH (right panel).

-

(2)

The dashed red lines represent the 99% confidence intervals of the efficient market degrees.

-

(3)

We run bootstrap sampling 10,000 times to calculate the confidence intervals.

-

(4)

R version 3.6.3 was used to compute the estimates.

Notes:

-

(1)

The panels of the figure show trading volumes (left panel) and market capitalizations (right panel) for BTC and ETH.

-

(2)

The dataset is obtained from the web page of CoinMarketCap (https://coinmarketcap.com/).

-

(3)

R version 3.6.3 was used to compute the statistics.

Notes:

-

(1)

The dataset is obtained from the web page of CoinMarketCap (https://coinmarketcap.com/).

-

(2)

R version 3.6.3 was used to compute the statistics.