Personalized Robo-Advising:

Enhancing Investment through Client Interaction111We are grateful for constructive comments from Peter Carr, Anthony Ledford, Charles-Albert Lehalle, Alberto Rossi, and seminar participants at Vanguard, the Robo-Advising Day at Georgetown University’s Center for Financial Markets and Policy, the University of Southern California, Boston University, the New England Statistics Symposium, the CFS Workshop on AI/ML in Financial Services, the Oxford-Man Institute, the NUS Quantitative Finance Series, the Brooklyn Quant Experience Lecture Series, the ACPR Workshop on Robo-Advising, the New Ideas in Quantitative Finance Workshop at Stony Brook University, the 2019 SIAM-FM Annual Meeting, the 2019 ICIAM, and the 2020 INFORMS Annual Meeting.

Abstract

Automated investment managers, or robo-advisors, have emerged as an alternative to traditional financial advisors. The viability of robo-advisors crucially depends on their ability to offer personalized financial advice. We introduce a novel framework, in which a robo-advisor interacts with a client to solve an adaptive mean-variance portfolio optimization problem. The risk-return tradeoff adapts to the client’s risk profile, which depends on idiosyncratic characteristics, market returns, and economic conditions. We show that the optimal investment strategy includes both myopic and intertemporal hedging terms which are impacted by the dynamics of the client’s risk profile. We characterize the optimal portfolio personalization via a tradeoff faced by the robo-advisor between receiving client information in a timely manner and mitigating behavioral biases in the risk profile communicated by the client. We argue that the optimal portfolio’s Sharpe ratio and return distribution improve if the robo-advisor counters the client’s tendency to reduce market exposure during economic contractions when the market risk-return tradeoff is more favorable.

1 Introduction

Automated investment managers, commonly referred to as robo-advisors, have gained widespread popularity in recent years. The value of assets under management by robo-advisors is the highest in the United States, exceeding $600 billion in 2019. Major robo-advising firms include Vanguard Personal Advisor Services, with about $140 billion of assets under management, Schwab Intelligent Portfolios ($40bn), Wealthfront ($20bn), and Betterment ($18bn). Robo-advisors are also on the rise in other parts of the world, managing over $100 billion in Europe, and exhibiting rapid growth in Asia where the assets under management exceed $75 billion solely in China (Statista (2020)).

The first robo-advisors were launched in the wake of the 2008 financial crisis and the ensuing loss of trust in established financial services institutions. Examples of pioneering robo-advising firms are Betterment and Wealthfront, which began offering services formerly considered exclusive to the general public, including individuals who did not meet the minimum investment levels of traditional financial advisors. In the years that followed, industry incumbents - such as Vanguard and Charles Schwab - followed suit and began offering their own robo-advising services, taking advantage of their existing customer bases to quickly gain a large market share. With the focus of most robo-advisors being on passive long-term portfolio management, the rise of robo-advising since the financial crisis has also been compounded by the seismic shift towards passive investing and low cost exchange-traded funds.222See https://www.cnbc.com/2018/09/14/the-trillion-dollar-etf-boom-triggered-by-the-financial-crisis.html

Robo-advising is a term that encompasses various forms of digital financial advice for investment management and trading. A recent survey paper by D’Acunto and Rossi (2020) distinguishes between digital tools and services that aid in active, short-term trading, with the client actively involved in the strategy implementation, and robo-advisors that focus on long-term passive investing where the level of delegation is higher. We develop a framework for automated investment management which belongs to the latter category, where the robo-advisor uses quantitative methods and algorithms to manage the client’s portfolio. We explore how the robo-advisor can use features of the client’s risk profile to determine a frequency of interaction with the client that ensures a high level of portfolio personalization.333Robo-advisors are fiduciaries under the Investment Advisers Act of 1940, and as such are subject to the duty of acting in the client’s best interest. We also analyze the dilemma faced by the robo-advisor in either catering to the client’s wishes, i.e., investing in accordance with the client’s risk profile, or going against the client’s wishes in order to seek better investment performance.

In our framework, the robo-advisor interacts repeatedly with the client to learn about changes in her risk profile. This risk profile is characterized by a risk aversion process, which captures three fundamental aspects of individual investor behavior. First, the client’s risk aversion is sensitive to the passage of time, consistent with empirical research that has identified a positive and potentially nonlinear trend in risk aversion as a function of age (see, e.g., Brooks et al. (2018) and Hallahan et al. (2004)). This type of time-dependence has also been used in the construction of Target Date Funds, which are widely used retirement portfolios that reduce equity risk as the client gets closer to retirement.444Target Date Funds are similar to the “set-and-forget” portfolios offered by the first generation of robo-advisors, where changes in allocation over time are solely based on the client’s age. While TDFs have virtually stayed the same since their inception over a quarter century ago, the technology-driven personalized advice of robo-advisors has continued to evolve. Second, risk aversion is impacted by idiosyncratic shocks, such as a change in disposable income or an increase in the client’s educational level or financial literacy (see, e.g, Hallahan et al. (2004) and Allgood and Walstad (2016)). These shocks in particular capture changes in unobservable factors driving the client’s risk aversion, consistent with empirical studies that have identified a substantial variation in idiosyncratic risk preferences that are unexplained by consumer attributes and demographic characteristics (see, e.g., Guiso and Paiella (2008); Sahm (2012), and Van de Venter et al. (2012)). Third, the client’s risk aversion depends on realized market returns and prevailing economic conditions. Specifically, the countercyclical nature of risk aversion has been extensively documented in the literature (see Bucciol and Miniaci (2018), Cohn et al. (2015), and Guiso et al. (2018), among others, for recent empirical and experimental evidence).

The robo-advisor adopts a multi-period mean-variance investment criterion with a finite investment horizon. It is worth noting that most robo-advising firms employ asset allocation algorithms based on mean-variance analysis, citing, among other things, its tractability and the intuitive interpretation of the risk-return tradeoff (see, for instance, Beketov et al. (2018)). While these robo-advising algorithms assume the risk-return tradeoff coefficient to be constant throughout the investment period, and statically reoptimize the portfolio in response to change in the client’s risk profile, our framework enables the robo-advisor to adapt the portfolio strategy to its own model of the client’s risk aversion process. Such a model is constructed from two sources of information. First, the robo-advisor observes both realized market returns and changes in the state of the economy, and continuously updates its model to reflect this information. Second, at times of interaction with the client, the robo-advisor receives information about the idiosyncratic component of the client’s risk aversion.

We show that the optimal stock market allocation consists of two components. The first component is akin to the standard single-period Markowitz strategy but also takes into account the expected return and variance of the optimal strategy throughout the investment period. The second component is intertemporal hedging demand, which depends on the relation between the current market return and future portfolio returns. A novel feature of our model is that this relation is driven by the client’s dynamic risk profile, in contrast to extant literature (e.g., Liu (2007) and Basak and Chabakauri (2010)) where it depends only on the correlation between market returns and changes in a stochastic state variable. To understand why hedging demand arises in our model, consider the case where positive (negative) market returns have a tempering (inflating) effect on the client’s risk aversion process. A positive market return thus leads to increased future investment and higher anticipated portfolio returns, whereas a negative return has the opposite effect. This positive relation between market returns and future portfolio returns amplifies the effect of the current allocation on the variance of terminal wealth. As a result, for a client whose risk aversion is negatively correlated with market returns, there is a negative hedging demand, i.e., the robo-advisor reduces her market exposure relative to a client whose risk aversion is not sensitive to market returns.

We show the existence of a tradeoff between the rate of information acquisition from the client and the accuracy of the acquired information. On the one hand, if interaction does not occur at all times, the robo-advisor may not always have access to up-to-date information about the client’s risk profile. On the other hand, information communicated to the robo-advisor may not be representative of the client’s true risk aversion, as the client is subject to behavioral biases, such as trend-chasing.555See Kahneman and Riepe (1998) for a discussion of common behavioral biases and strategies to overcome them. For example, if recent market returns have exceeded expectations, the client may feel overly exuberant and communicate a risk aversion value that is lower than her actual risk aversion. Vice versa, following a market underperformance, the client may feel overly pessimistic and exaggerate her risk aversion when communicating with the robo-advisor. The suboptimality of high interaction frequencies then hinges on the fact that reducing the frequency of interaction mitigates the effect of client’s biases. The rationale is that over longer time periods, fluctuations in realized market returns average out. Such a behavioral pattern is consistent with the notion of myopic loss aversion introduced in Benartzi and Thaler (1995), which refers to the empirical phenomenon that market underperformance has a stronger impact on risk aversion than market overperformance.

We introduce a measure of portfolio personalization to analyze the aforementioned tradeoff. This measure is defined in terms of the difference between the client’s actual risk aversion and the robo-advisor estimate of it. The lower this measure, the closer the investment strategy implemented by the robo-advisor is to the strategy matching the client’s risk profile. We show that for a fixed level of behavioral bias, quantified as the client’s sensitivity to market return fluctuations, this measure is minimized by a unique interaction frequency. Such a frequency allows the robo-advisor to strike a balance between obtaining information from the client in a timely manner and ensuring that the communicated information is not overly biased by recent market returns. Our result is supported by existing practices of robo-advising firms, which encourage clients to refrain from making frequent changes to their risk profiles, and even limit their ability to do so.666Wealthfront provides the following guidelines: “Our software limits our clients to one risk-score change per month. We encourage people who attempt more than three risk-score changes over the course of a year to try another investment manager.” We also show that the optimal interaction frequency is decreasing in the amount of behavioral bias, and increasing in the rate at which the idiosyncratic component of the client’s risk aversion changes. Therefore, a higher level of personalization is achieved for clients with limited behavioral biases and stable risk profiles.

We compare the investment performance of strategies that invest the same proportion of wealth in the stock market during periods of economic growth but differ in their market exposure during contractions. We show analytically that the Sharpe ratio of such strategies is generally increasing in the proportion of wealth allocated to the stock market in a state of contraction, when the market risk-return tradeoff is more favorable.777Since the seminal work of Fama and French (1989), it has been extensively documented that the market risk-return tradeoff is countercyclical, i.e., higher at business cycle troughs than peaks. Because the client typically has a countercyclical risk aversion process, she would lean towards reducing market exposure during economic contractions and, as a result, attain a lower Sharpe ratio from her investment. The question that then arises is to what extent, if any, the robo-advisor should deviate from the strategy implied by the client’s risk profile in order to improve the investment performance. We show that the Sharpe ratio of the optimal portfolio is concave with respect to the change in the market allocation when the economy moves to a state of contraction. This means that the Sharpe ratio drops more if the allocation is reduced, compared to how much it improves if the allocation is increased by the same amount. Our analysis thus suggests that a good middle ground for the robo-advisor is to rebalance the portfolio and maintain prespecified weights throughout the business cycle. This investment pattern is also in line with the long-term investment principle of riding out business cycles, and further reinforced by the fact that, in practice, it is difficult to detect changes in economic regimes and thus estimate the prevailing market risk-return tradeoff.

The remainder of the paper is organized as follows. In Section 2, we briefly review the related literature. In Section 3, we introduce our robo-advising framework. In Section 4, we present the solution to the associated optimal investment problem. In Section 5, we introduce and study performance metrics for the robo-advisor’s investment strategy. Section 6 offers concluding remarks. Appendix A contains theoretical and computational properties of the optimal investment strategy. Appendix B and Appendix C contain proofs and auxiliary results related to Sections 4 and 5, respectively.

2 Literature Review

Our study contributes to the growing literature on robo-advising. D’Acunto and Rossi (2020) describe the main components of robo-advising systems and propose a classification in terms of four main features: (i) portfolio personalization, (ii) client involvement, (iii) client discretion, and (iv) human interaction. We offer a quantitative framework that aligns with this classification and is consistent with that of the most prominent stand-alone robo-advising firms. We proceed to briefly describe each of the four features and how they fit into our framework.

(i) Portfolio personalization refers to the robo-advisor’s ability to offer financial advice tailored to the client’s needs. A common criticism of robo-advising is the lack of customization, with risk profiling based on information that is too limited.888Risk profiling can, in principle, be infinitely customizable. Barron’s 2019 annual ranking of robo-advisors (available at https://webreprints.djreprints.com/4642511400002.pdf) reports the latest growth in robo-advising to be in cash management, with robo-advisors aiming to become everyday money managers of their clients, in addition to long-term investment planners. Robo-advising firms already offer cash management services such as direct deposits of paychecks, automatic bill payments, and FDIC-insured checking and savings accounts. This implies increased access to data which can in turn be used by robo-advisors to improve investment recommendations. In our framework, the robo-advisor achieves portfolio personalization by soliciting information from the client. We do not explicitly model the process of collecting information, which can be based both on online questionnaires and on collection of client’s data from various sources (e.g. savings and spending behavior, asset and liabilities).

(ii) Client involvement refers to the client’s participation in the design of the investment strategy. At one end of the spectrum, there are robo-advisors that require the client to approve every single trading decision. In this case, the client is actively involved and the term robo-advisor is descriptive, because the client decides in what way to follow the advice provided. Our model lies at the other end of the spectrum, where the robo-advisor automatically manages the portfolio on the client’s behalf and for which the term robo-manager is more descriptive.

(iii) Client discretion is the client’s ability to override the robo-advisor’s recommendation. In our framework, the client’s behavioral biases can be viewed as the client overriding the robo-advisor’s recommendations. This is considered a low level of discretion. It is consistent with the operations of robo-advisors focusing on long-term investing, where the client is allowed to adjust the level of portfolio risk, but has no control over which parts of the investment portfolio are modified.

(iv) Human interaction refers to the degree of interaction between the client and a human-advisor. In our framework, there is no human contact which is also the case for automated robo-advisors that strive to minimize operating costs.

The above classification is qualitative in nature. The quantitative components of our framework are constructed to resemble the algorithmic principles of actual robo-advisors. Beketov et al. (2018) provide an industry overview based on the analysis of over 200 robo-advisors globally. Their study shows that a large majority of robo-advisors use an asset allocation framework based on mean-variance analysis, with the asset universe consisting of low cost exchange-traded funds. They also show that risk profiling of clients is primarily done using online questionnaires.

Rossi and Utkus (2019a) conduct an extensive survey to study the “needs and wants” of individuals when they hire financial advisors. They show that for traditionally-advised clients, algorithm aversion and the inability to interact with a human are the main obstacles for switching to robo-advising, while robo-advised clients do not have the same need for trust and access to expert opinion. Our model lends theoretical support to the notion that robo-advisors may be less suitable for algorithmic-averse clients. Namely, the robo-advisor can improve the portfolio performance by going against the wishes of the client, i.e., by investing in a way that may seem counterintuitive to the client. Doing so is more challenging for a robo-advisor than for a human-advisor, because market returns are random, and an algorithmic-averse client will be less forgiving to the robo-advisor in the event of adverse market returns.

From a methodological perspective, our work contributes to the literature on time-inconsistent stochastic control (Björk and Murgoci (2013)). Other related works include Li and Ng (2010) who solve a multi-period version of the classical Markowitz problem, and Basak and Chabakauri (2010) who solve a continuous-time version of the same problem. Björk et al. (2014) solve the dynamic mean-variance problem in continuous time, with the mean-variance utility function applied to returns as in the classical single-period mean-variance analysis. A recent study of Dai et al. (2019) further develops a dynamic mean-variance framework based on log-returns, with the aim of generating policies conforming with conventional investment wisdom. In all of these works, the risk-return tradeoff is assumed to be constant throughout the investment horizon. By contrast, in our model, the risk-return tradeoff coefficient is stochastic, with explicitly modeled dynamics that can be used to generate investment policies tailored to the client’s risk profile.

Our paper is also related to the literature on portfolio optimization models where the security price dynamics are driven by stochastic factors. Unlike Liu (2007) and Basak and Chabakauri (2010), intertemporal hedging demand does not arise because of dependence between the stochastic factor and market returns, which are assumed to be uncorrelated in our model. Rather, intertemporal hedging terms appear because of the correlation between market returns and future changes in the investor’s risk aversion. Additionally, the stochastic factor itself impacts the client’s risk aversion dynamics, which in turn determine the optimal allocation. It is widely agreed upon that risk aversion varies with the business cycle, and this characteristic is highly relevant for robo-advising where a significant challenge is to keep clients invested in the stock market during economic downturns.999The seminal work of Campbell and Cochrane (1999) provides an asset pricing framework that rationalizes the countercyclicality of both risk aversion and the market risk-return tradeoff; see, also, Lettau and Ludvigson (2010) for a survey of the literature and extensive empirical evidence.

3 Modeling Framework

Our robo-advising framework has four main components: (i) a regime switching model of market returns, (ii) a mechanism of interaction between the client and the robo-advisor, (iii) a dynamic model for the client’s risk preferences, and (iv) an optimal investment criterion. We describe each of these components in Sections 3.1-3.4.

3.1 Market and Wealth Dynamics

The market consists of a risk-free money market account, , and a risky asset, , whose dynamics are described by the equations

where and is a given constant. The risky asset is representative of the overall stock market, and for this reason we will refer to returns of the risky asset as market returns.

The above dynamics are modulated by an observable state process, , which captures macroeconomic conditions affecting interest rates and market returns (cf. Hamilton (1989)). We assume the economic state variable to be a time-homogeneous Markov chain with transition matrix , taking values in a finite set , for some . Conditioned on , the risk-free interest rate is constant, while the risky asset’s return, , admits a probability density function which depends only on the current economic state , and has mean and variance .

For notational simplicity, we omit the dependence on the economic state. Hence, we use in place of , and denote its state-dependent mean and variance by and , respectively. Similarly, we use in place of , and let . We denote by the excess return of the risky asset over the risk-free rate, which has state-dependent mean and variance given by and , respectively.

We denote by the wealth of the client at time , allocated between the risky asset and the money market account, and use to denote the amount invested in the risky asset. For a given self-financing trading strategy , the wealth process follows the dynamics

| (3.1) |

The initial wealth, , and the initial state of the economy, , are assumed to be non-random. The random variables and are defined on a probability space , which additionally supports a sequence of independent real-valued random variables. This source of randomness captures idiosyncratic changes to the client’s risk preferences. Moreover, is independent of and . We use to denote the filtration generated by the three stochastic processes in our model:

| (3.2) |

where , , and . We will use analogous notation to denote the paths of other stochastic processes throughout the paper.

Remark 3.1.

In our discrete-time model, the price of the risky asset is not restricted from becoming negative. However, at any given time the optimal investment strategy presented in Section 4 does not depend on the current price of the risky asset, but only on the first two moments of its returns distribution. Hence, for the optimal investment problem to be well-defined, it is sufficient to assume the existence of a returns process with a finite variance as described above. ∎

3.2 Interaction between Client and Robo-Advisor

A key component of the proposed framework is the interaction between the client and the robo-advisor. Following an initial interaction at the beginning of the investment process, the client and the robo-advisor interact repeatedly throughout the investment period. At each interaction time, the client translates the information communicated by the client into a numerical value, herein referred to as a risk aversion parameter. In our quantitative framework, we abstract from the construction of such a mapping, effectively assuming that the client communicates directly a single risk aversion parameter to the robo-advisor.101010The majority of robo-advisors elicit risk preferences by means of online questionnaires (Beketov et al. (2018)). The client is presented with questions regarding, e.g., demographics, investment goals, education and financial literacy, and potential reactions to hypothetical gambles and market events. We refer to Charness et al. (2013) for an outline of the pros and cons of different methods used to assess risk preferences, and Cox and Harrion (2008) for a more comprehensive overview. Note that between consecutive interaction times, the robo-advisor receives no input from the client.

The interaction schedule, denoted by , is an increasing sequence of stopping times with respect to the filtration , defined in (3.2). That is, , , and , for any . Hence, interaction can be triggered by any combination of client-specific events, changes in the state of the economy, and market events such as a cascade of negative market returns.

The rule used to determine the interaction schedule is decided at the beginning of the investment process, and used throughout it. For future reference, we also define the process , where

is the last interaction time prior to and including time .

3.3 Client’s Risk Aversion Process

We first introduce the client’s actual risk aversion process, , which is an -valued stochastic process adapted to the filtration defined in (3.2). This means that at time , the client’s risk aversion may have shifted from its initial value due to changes in economic regimes, , and realized market returns , as well as because of idiosyncratic shocks to the client’s risk aversion, .

We also introduce the -adapted process , where is the risk aversion parameter communicated by the client at the most recent interaction time, . Observe that the process depends on the interaction schedule and, by construction, it remains constant between consecutive interaction times where no new information comes from the client, i.e., .

The robo-advisor then constructs a model of the client’s risk aversion process, denoted by , and uses it to solve the optimal investment problem. While it is generally desirable for the model to accurately track the client’s actual risk aversion, , the two processes may not coincide due to the following reasons. First, the client and the robo-advisor may not interact at all times, so the robo-advisor does not always have access to up-to-date information about the client’s risk preferences. Specifically, while the robo-advisor observes both market returns and changes in the economic regime, it cannot observe in real time the idiosyncratic shocks to the client’s risk aversion. Second, even if interaction were to occur at all times, information communicated by the client may not be representative of the client’s true risk preferences due to her behavioral biases (see Section 5.1 for further details).

Formally, the risk aversion process is an -valued stochastic process adapted to the robo-advisor’s filtration, , which is generated by the random variables , defined as

| (3.3) | ||||

It then follows that at time , the risk aversion process may be written as

| (3.4) |

for a measurable function .

Remark 3.2.

The random variable in (3.3) can be decomposed as , where , and . This shows that the robo-advisor’s filtration has two sources of information. The first component, , reflects the fact that the robo-advisor has the ability to process all available information about the market and the economy. The second component, , is the result of its interaction with the client, and contains both the history of interaction times and the communicated risk aversion values. Under mild conditions, the robo-advisor’s filtration grows with the frequency of interaction, and, if interaction occurs at all times, it becomes equal to the filtration .111111For example, assume the interaction times to be given by , for some . If the sum of idiosyncratic shocks, is measurable with respect to the robo-advisor’s filtration, then increases to , as . ∎

3.4 Investment Criterion

The robo-advisor’s objective is to optimally invest the client’s wealth, taking into account the stochastic nature of the client’s risk preferences. For this purpose, we develop a dynamic version of the standard Markowitz (1952) mean-variance problem that adapts to the client’s changing risk preferences. We proceed to introduce this criterion, which we refer to as an adaptive mean-variance criterion.

Let be a fixed investment horizon. For each , , , and a control law , we consider the mean-variance functional

| (3.5) |

where, at time , the risk-return tradeoff is the robo-advisor’s model of the client’s risk aversion at this time, and is the simple return obtained by following the control law until the terminal date ,

| (3.6) |

The initial condition in (3.5) is given by and , and both the expectation and the variance are computed with respect to the probability measure . For future reference, we also introduce the probability measure .

Observe that the risk-return tradeoff does not depend on the client’s wealth. There are important reasons behind this assumption. First, it is consistent with the Markowitz mean-variance criterion, which is recovered as a special case of our model when there is a single investment period. Second, as we will see in Section 4, the optimal investment strategy turns out to be consistent with that of an investor exhibiting constant relative risk aversion (CRRA), i.e., whose proportion of wealth invested in the risky asset is independent of the wealth level.121212Empirical evidence suggests that CRRA is a good description of microeconomic behavior (see, e.g., extensive panel data studies carried out in Brunnermeier and Nagel (2008); Chiappori and Paiella (2011), and Sahm (2012)). However, the evidence is not universal. For instance, Calvet and Sodini (2014) and Guiso and Paiella (2008) reject CRRA in favor of decreasing relative risk aversion.

The objective functional (3.5), together with the risk aversion process (3.4), define a family of sequentially adaptive optimization problems, in the sense that at each time a new problem arises, with properties that depend on realized market returns, economic state changes, and client-communicated information, but with the same initially specified terminal date. Moreover, observe that it is the robo-advisor that solves the optimization problem, and the initial condition of each optimization problem fixes the value of the stochastic process that generates the robo-advisor’s filtration, as well as the value of the client’s wealth process.

The control law in (3.5), also referred to as a strategy or allocation, is such that for each , the control is a measurable real-valued function of the state variables and . Additionally, admissible control laws are assumed to be self-financing and to satisfy the square-integrability condition .

Remark 3.3.

We assume the investment horizon to be deterministic and fixed. A stochastic horizon can be captured through distributional assumptions on the risk aversion process . For example, the possibility of client death can be modeled by introducing a time-dependent probability of the risk aversion parameter becoming “infinite”. The probability would be increasing in , and infinity would be an absorbing state reached only in the event that the client dies. In the death-state, the client’s portfolio is liquidated and the client’s entire wealth is allocated to the risk-free asset. For the optimization problem described in this section, a non-zero value of would have the effect of tilting the risky asset allocation upward, because no more investing is possible after death. In the same vein as when accounting for client death, we may impose conditions on the dynamics of the risk aversion process that halt investment if certain market events or economic conditions occur. ∎

Remark 3.4.

There is a non-zero probability that the client’s wealth becomes negative. This can be either due to short-selling or to an extreme negative return of the risky asset (see Remark 3.1). Although the objective functional (3.5) and the optimal strategy presented in Section 4 are well-defined for negative wealth levels, they are not economically meaningful and, in practice, the robo-advisor would liquidate the client’s portfolio as soon as the wealth becomes negative.

In Appendix A.3, we modify the optimal strategy in a way that forces liquidation of the entire risky position if the wealth is negative. We show that the change in expectation and variance of the optimal portfolio’s return (given in (3.6)), resulting from imposing this liquidation condition, can be bounded by a term that is extremely small for plausible values of the model parameters. It then follows that forcing liquidation has a small impact on the value of the objective functional (3.5).

The liquidation condition is imposed ad hoc on the optimal strategy. Hence, it is myopic in the sense that the modified strategy coincides with the optimal strategy until the wealth achieves a negative value. In Appendix A.3, we also discuss how the optimal investment problem can be adjusted to handle portfolio constraints which are typically imposed by robo-advising firms, such as no borrowing and no short-selling. In that case, the constraints also affect the optimal strategy at times before they become binding, because of the dynamic nature of the optimization problem. ∎

Through the wealth dynamics (3.1), the mean-variance functional depends on the control law restricted to the time points and the robo-advisor chooses the control given future control decisions . Therefore, any candidate optimal control law is such that for each , , and ,

| (3.7) |

where is the set of control laws that coincide with after time . If a control law satisfying (3.7) exists, we define the corresponding value function at time as

| (3.8) |

It is worth noticing that when seeking an optimal control at time , the robo-advisor takes into account the dynamics of , i.e., the dynamics of the risk-return coefficient throughout the investment horizon, with only the current value being known. At the subsequent time , the dynamics of the remaining values are updated by the robo-advisor, and becomes known. If is a non-interaction time, this update is based only on information about market returns and economic states, while if is a time of interaction it also accounts for information received from the client.

4 Optimal Investment Strategy

We analyze the optimization problem defined by the sequence of objective functionals in (3.5) and the optimality criterion in (3.7). It is well known that, even if the risk-return tradeoff is constant through time, the family of optimization problems defined by (3.5) is time-inconsistent in the sense that the Bellman optimality principle does not hold. This means that if, at time , the control law maximizes the objective functional , then, at time , the restriction of to the time points may not maximize . We refer to Björk and Murgoci (2013) and references therein for a general framework of time-inconsistent stochastic control in discrete time.

As standard in this literature, we view the optimization problem in (3.7) as a multi-player game, where the player at each time is thought of as a future self of the client. Player then wishes to maximize the objective functional , but decides only the strategy at time , while are determined by her future selves. The resulting optimal control strategy, , is the subgame perfect equilibrium of this game, and can be computed using backward induction. At time , the equilibrium control is obtained by maximizing over , which is a standard single-period optimization problem. For , the equilibrium control is then obtained by letting player choose to maximize , given that player will use , for .

In Appendix B, we derive an extended Hamilton-Jacobi-Bellman (HJB) system of equations satisfied by the value function of the optimization problem. The following result presents the solution to this system, which is the optimal investment strategy for an interaction schedule and a risk aversion process of the general form, respectively introduced in Sections 3.2 and 3.3.

Proposition 4.1.

The dynamic optimization problem (3.7) admits a solution of the form

for and . The optimal proportion of wealth allocated to the risky asset is given by

| (4.1) |

where we recall that and have been defined in Section 3.1, and

| (4.2) |

is the terminal value of one dollar invested in the optimal strategy at time .

The above proposition characterizes the structure of the optimal strategy. It shows that the optimal allocation, i.e., the relative fraction of wealth allocated to each asset, is independent of the wealth level. In Appendix A, we use backward induction to develop an explicit representation of the optimal strategy, and discuss the computational complexity of this procedure. As a byproduct, we obtain formulas for the expected value and variance of the optimal portfolio’s return, which in turn can be used to compute the value function (3.8).

It is evident from (4.1) that the optimal strategy can be decomposed into two terms. The first term resembles the standard single-period Markowitz strategy, . However, rather than depending only on statistics of the market return between and , it also accounts for the return achieved by the optimal portfolio between times and . The second term in the decomposition is the intertemporal hedging demand, which can be rewritten as

where the first term captures the contribution of dynamic risk aversion. To analyze this term, it is convenient to first rewrite it as

which shows that its sign depends predominantly on the covariance between , i.e., the current excess market return, and , i.e., the future expected portfolio return. This covariance is generally positive, resulting in a negative hedging demand. To see this, observe that we generally expect an above average market return, , to push down the future risk aversion values ; this, in turn, implies a positive relation between and future risky asset allocations . As a result, the expectation , achieved through the allocations , is larger following a positive value of . Altogether, the current market return and the future expected portfolio return thus move in the same direction, amplifying the effect of the current market return on the variance of the terminal wealth and leading to a negative hedging demand.

This is akin to the intertemporal hedging term in Basak and Chabakauri (2010), which arises because of covariation between market returns and the state variable. In their setting, the hedging demand would vanish if market returns and changes in the state variable were uncorrelated, in which case trading in the risky asset cannot hedge fluctuations in the state variable. In our setting, the hedging demand is driven by the dynamic risk aversion process that links current market return with future portfolio returns. This hedging demand appears even though the market returns in our model are conditionally independent of changes in the state variable.131313Conditionally on the value of , the market return is independent of .

Next, we consider the special case where intertemporal hedging due to dynamic risk aversion vanishes, i.e., when future risk aversion values are conditionally independent of the current market return. In this case, the optimal allocation strategy admits a more explicit expression, given only in terms of the first two moments of the return variables and .

Corollary 4.2.

Given , assume the risk aversion values to be independent of the market return . The optimal proportion of wealth allocated to the risky asset at time is given by

where and .

The optimal allocation given in the corollary can alternatively be written as141414An extension of formula (4.3) can be derived for the general model considered in Proposition 4.1 (see Appendix B).

| (4.3) | ||||

which allows to pin down the relation with the optimal investment strategy in the classical mean-variance setup. Specifically, it is proportional to the single-period Markowitz strategy, , i.e., the optimal allocation of a myopic investor whose objective functional spans a single period. This fraction depends on the current economic conditions, and the client’s current risk aversion. The proportionality factor in (4.3) depends on the future return of the investment strategy, , which in turn depends on both future economic conditions and the client’s future risk aversion dynamics. Consistently with intuition, this factor is increasing in the first moment of and decreasing in its second moment. In the final time period, the proportionality factor is equal to one and the optimal allocation is given explicitly by the Markowitz strategy in this time period.

5 Performance of the Robo-Advising Framework

We analyze the investment performance of the proposed robo-advising framework. Our analysis will be based on a specific model that fits into the general framework, and which we introduce in Section 5.1. In Section 5.2, we consider the interplay between interaction and portfolio personalization, and show the existence of a tradeoff between the rate of information acquisition from the client and the effect of the client’s behavioral biases. In Section 5.3, we explore how the optimal investment strategy is affected by transitions between economic states and the associated changes in the client’s risk aversion. We also discuss whether the robo-advisor should cater to client wishes or go against them to improve the investment performance.

5.1 A Robo-Advising Model

In the following paragraphs, we specify each component of the framework introduced in Sections 3.1-3.4.

Market Dynamics.

The risky asset has conditionally Gaussian returns. That is, given the economic state at time , the return has a Gaussian distribution with mean and variance .

State Process Dynamics.

We assume a two-state economy . This choice is supported by the methodology of the National Bureau of Economic Research (NBER), which splits business cycles into periods of economic expansions and contractions.151515The work of Chauvet and Hamilton (2006) shows that a Markov switching model successfully identifies NBER’s business cycle turning points. We use to denote the state of economic growth and to denote the state of recession. We use to denote the transition probability matrix, so that is the probability that the economy transits from state to state in a single time step.

Interaction Schedule.

The sequence of interaction times is deterministic and equally spaced. The interaction schedule is then characterized by a fixed integer parameter , with . The two extreme cases are , which corresponds to communication of risk preferences at all times, and , which corresponds to risk preferences communicated only at the beginning of the investment process.

Client’s Risk Aversion.

The client’s risk aversion process, , is of the form

| (5.1) |

The first component, , is deterministic and time-varying. For example, the specification captures the empirical observation that risk aversion increases with age, with the parameter specifies the rate of increase.

The second component, , depends on the client’s personal circumstances and has stochastic dynamics, , where is an i.i.d. sequence of random variables. Specifically, with probability , where and is an i.i.d. sequence of standard Gaussian random variables, and with probability . This component captures idiosyncratic shocks to the client’s risk aversion, which are unrelated to economic state transitions and market dynamics. The multiplicative innovation terms are independent and with unit mean, making a martingale, devoid of a predictable component.

The third component, , is given by , where is a possibly time-varying function of the current economic state. This component captures the empirical fact that risk aversion varies with the business cycle.

Client’s Behavioral Bias.

At time , the risk aversion parameter communicated by the client at the most recent interaction time, , is of the form

| (5.2) |

where is a factor that inflates or deflates the client’s actual risk aversion, , based on recent market returns. Namely, the sum in the exponent is the cumulative excess return of the risky asset over its expected value, since the previous interaction time, . Because previous market returns have no predictive value for future market returns, given the state of the economy, the factor is representative of common behavioral biases, and the coefficient determines the magnitude of this effect.

We emphasize two important properties of the component . First, the convexity of the exponential function allows us to capture loss aversion: the upward risk aversion bias following a market underperformance is greater than the downward bias when the market exceeds expectations by the same amount (Tversky and Kahneman (1979)). Second, in a model with a single economic state , we have , which shows that the average effect of the behavioral bias decreases as the time between interaction increases,161616In a setup with multiple economic states we have, conditionally on , that . consistent with the notion of myopic loss aversion, introduced in Benartzi and Thaler (1995).

The bias may be interpreted as the client overriding the robo-advisor’s decisions. That is, at an interaction time , the robo-advisor proposes a portfolio tailored to the client’s characteristics, , but the client makes changes to the proposed allocation based on recent market returns. This results in a portfolio allocation consistent with a risk aversion coefficient . The effect of this override, which is driven by the client’s behavioral biases, prevails until the subsequent time of interaction, , when the client again adjusts the portfolio allocation proposed by the robo-advisor. This time, however, the adjustment is based on market returns realized in the time interval .

Robo-Advisor’s Model of Client’s Risk Aversion.

The risk aversion process is of the form

| (5.3) |

The component is the risk aversion parameter communicated by the client at the most recent interaction time, , and, in the robo-advisor’s model, it stays constant until the subsequent time of interaction, . On the other hand, the model is adjusted for the passage of time through the factor , and for changes in economic states through the ratio . The above equation can be written in an alternative form as

where we recall from (3.3) that is the information set of the robo-advisor at time . This shows that the robo-advisor’s view of the client risk aversion is equal to the expectation of client’s actual risk aversion times bias factor from the previous interaction time.

From the above expression it can be observed that interaction impacts the robo-advisor’s inferred value of the client’s risk aversion in two different ways. First, between interaction times, the expectation is not updated in response to changes in the idiosyncratic component of the client’s risk aversion, because such changes cannot be inferred from observables like market returns or economic indicators. Second, a higher interaction frequency comes at the expense of increased behavioral bias, tilting the robo-advisor’s model further away from the client’s actual risk aversion.

Calibration of Risk Aversion Process.

The multiplicative model introduced in this section provides a parsimonious description of the client’s risk aversion. Under this specification, the risk aversion is guaranteed to be non-negative, and its parameters can be estimated from historical portfolio allocations. We next sketch a calibration procedure for models of this form.

Consider a sequence of historical portfolio allocations for a set of self-directed investors. Such data is available to financial firms offering discount brokerage services, in particular the growing number of low-cost online brokerages.171717See, among others, the seminal work of Barber and Odean (2000) where such a data set is analyzed and Glaser and Weber (2009) for a more recent study using online brokerage data. Assume that the portfolio allocations are consistent with a myopic mean-variance criterion, for which there exists a one-to-one relationship between allocations and risk aversion levels. Then, the allocations can equivalently be viewed as historical sequences of implied risk aversion coefficients.

For a given client, the risk aversion model can be calibrated using the subset of investors that have demographic characteristics similar to the client.181818In practice, robo-advising firms manage a finite number of portfolios and group clients with similar profiles into risk categories. For instance, Wealthfront constructs a composite Risk Score ranging from 0.5 to 10, in increments of 0.5. Specifically, the three components of the risk aversion process (5.1) and the behavioral bias in (5.2) can be estimated using the following sequential procedure. First, the temporal component can be inferred from the initial portfolio composition chosen by investors at different life stages. For a personalized service, this component can also be used to incorporate a client-specific time-dependence of risk aversion. Adjusting for the effect of time, the average investment levels during each economic regime (e.g., periods of expansions and contractions - see Section 5.3) then provide information about the process component which depends on the economic state. Next, the extent of behavioral bias can be estimated from the relationship between market returns and subsequent changes in the portfolio’s market exposure.191919The literature on individual investor performance focuses to a large extent on biases and investor’s mistakes. For instance, Statman et al. (2006) study the role of investor overconfidence by examining the lead-lag relationship between market returns and trading volume. In addition, for a given client, data on financial literacy, investment experience, and cognitive abilities, can be used to adjust the estimated behavioral bias (see, e.g., studies by Oechssler et al. (1997) and Seasholes and Feng (2005)). Finally, after adjusting for the passage of time, economic regimes, and bias, the size and frequency of allocation changes made by investors provide information about the idiosyncratic component of the risk aversion process.

Sensitivity of Optimal Allocation to Idiosyncratic Shock and Behavioral Bias.

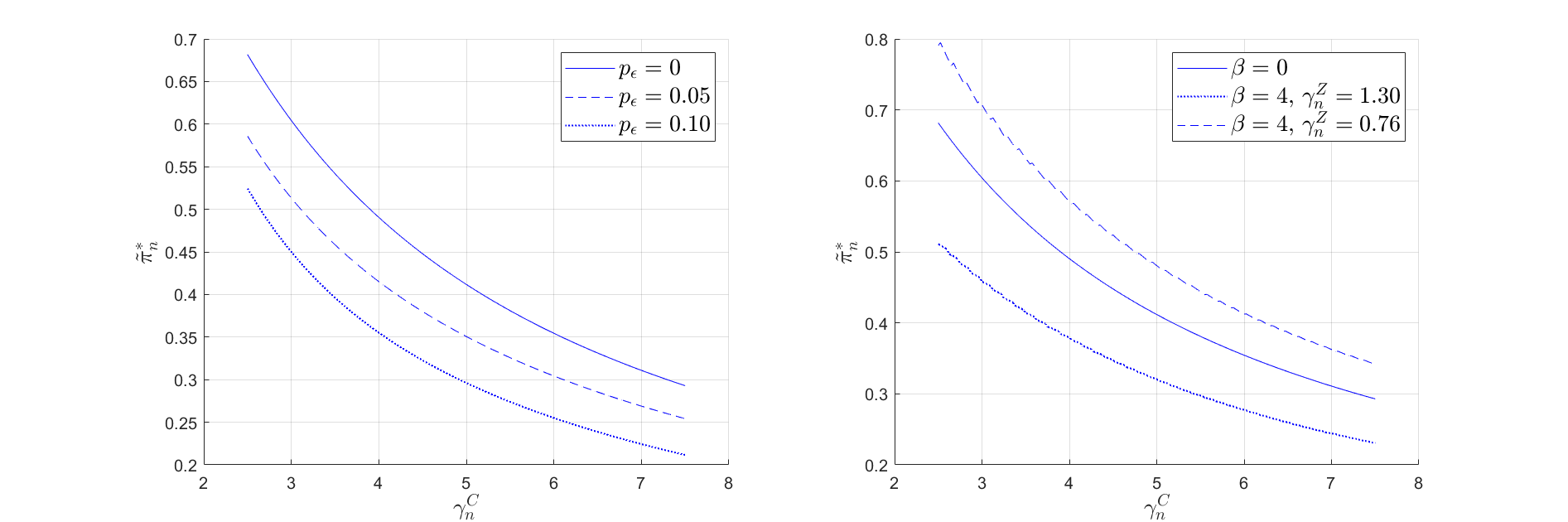

In Figure 1, we display how the optimal allocation in Proposition 4.1 depends on the variability of the idiosyncratic component of the client’s risk aversion and the client’s behavioral bias. The left panel shows that if the client’s idiosyncratic risk preferences fluctuate more due to a larger value of the parameter , then the optimal allocation deviates more from that of the benchmark case with no idiosyncratic shocks. The right panel shows that the client’s behavioral bias following a negative market return () has a stronger influence on the optimal allocation than the bias following a positive market return of the same magnitude (). This numerical finding is consistent with the notion of loss aversion, as discussed above.

Left panel: Impact of idiosyncratic risk aversion shocks, obtained by letting and . Right panel: Impact of behavioral bias, obtained by choosing and . These values of and correspond to a cumulative market return between two interaction times which is standard deviations above/below its expected value. The annualized market parameters in state are set to , , , and one time step in the model corresponds to one month. The investment horizon is months, and the time between interaction is months. We show the allocations prevailing one year after the start of the investment process, i.e., at time .

5.2 Interaction and Optimal Personalization

In our framework, the client and robo-advisor do not interact at all times and, thus, the robo-advisor is not always immediately aware of changes in the client’s risk profile. While a higher interaction frequency is the only way to reduce this information asymmetry, it also increases the amount of behavioral bias in the communicated information. The goal of this section is to analyze this tradeoff quantitatively.

We start by defining a measure of portfolio personalization. This measure depends on the relation between the client’s risk aversion process, , given by (5.1), and the robo-advisor’s model of the client’s risk aversion, , given by (5.3). Recall from Section 4 that at time , the optimal risky asset allocation is proportional to the risk tolerance parameter , and it is approximately proportional to for (see (4.3)). We therefore choose to define personalization in terms of the expected relative difference between the risk tolerance parameters and , averaged over the investment period. Specifically, for and , we introduce the personalization measure

| (5.4) |

A lower value of means a higher level of portfolio personalization. Full personalization is achieved if and only if and , which leads to . This is because the processes and coincide only in this case, when there is no behavioral bias and the client and the robo-advisor interact at all times. Although not explicitly highlighted in the notation, we note that the value of also depends on the parameters and , which govern the distribution of idiosyncratic risk aversion shocks.

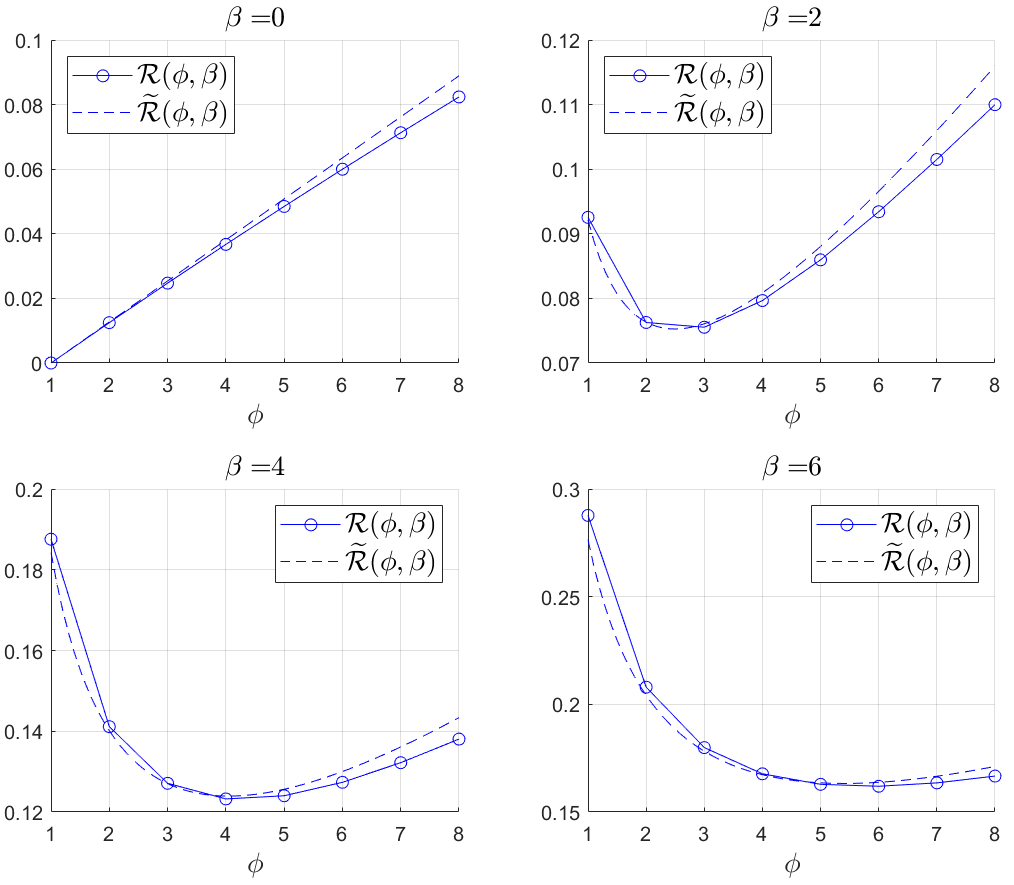

For a given value of , our objective is to study the dependence of the measure on . For this, we consider an approximation that is analytically more tractable than . In the following proposition, we characterize this approximation and show that it is minimized by a unique value of . In Figure 2, we show graphically that and are close, for different interaction frequencies and levels of behavioral bias.

Proposition 5.1.

Set . The following statements hold:

-

(i)

The measure satisfies the relation

(5.5) where (resp. ) is the largest (resp. smallest) multiple of that is less than (resp. greater than) or equal to , the error term is of order , and

-

(ii)

Let and be such that . Then, there exists a unique value of that minimizes .202020If , the values and are independent of . Specifically,

Furthermore, satisfies the monotonicity properties

(5.6)

The error term of order in the approximation (5.5) results from fixing the economic state throughout the investment period. Typically, transitions between economic states are infrequent (see (5.18) in Section 5.3) and the error term vanishes if the model consists of a single economic state. From the signs of the derivatives given in (5.6), it can be seen that if the economy transits to a state with a higher return volatility, i.e., if increases, the optimal time between consecutive interactions also increases. This is because the client’s behavioral bias is based on market return fluctuations, which are magnified if the return volatility is higher.

The above proposition confirms two intuitive claims. First, in the absence of behavioral biases, i.e., , it is optimal for the robo-advisor to interact with the client at all times. Second, if there are no idiosyncratic risk aversion shocks, i.e., , then it is optimal to never interact. Most interestingly, if both and , then it may be suboptimal to interact at all times. This is because a higher frequency of interaction comes at the expense of increased behavioral bias in the communicated risk aversion parameter. Furthermore, the signs of the derivatives in (5.6) show that a larger value of increases the optimal time between consecutive interactions, while larger values of and imply a greater variance of idiosyncratic risk aversion shocks and push down the optimal time between interaction. In the proof of the proposition, we show that

which gives a sufficient condition for when it is optimal to refrain from interacting at all times.212121This condition is also close to being necessary. See Eq. (C.2) in Appendix C. In the above inequality, we compare the rate of change of the idiosyncratic risk-aversion component, as measured by , with the amount of behavioral bias, quantified by the product of the client’s sensitivity to market returns and the volatility of returns. If the latter is greater than the former, then the derivative of at is negative, i.e., it is suboptimal to interact at all times.

To ensure a high level of personalization, the robo-advisor must construct a process which is as close as possible to the client’s actual risk aversion process . A related measure of personalization may thus be directly built on the proximity of the investment strategy corresponding to and the strategy corresponding to . The latter is the strategy that achieves full personalization and can only be attained if interaction occurs at all times and there is no behavioral bias, in which case the two risk aversion processes coincide.

Denote by and the optimal allocations corresponding to and , respectively. In line with the definition of in (5.4), we introduce the measure

A smaller value of implies a higher level of personalization, and full personalization is achieved if and only if . We observe that the difference between and is not a simple function of the difference between and . Nevertheless, in Appendix C we establish a direct relation between the two measures and , namely,

| (5.7) |

which shows that a small difference between and translates into a small difference between the corresponding investment strategies. In the above equation, the first error term is due to the idiosyncratic component of the client’s risk aversion and it vanishes if . The second error term originates from the client’s behavioral bias and it is maximized at .

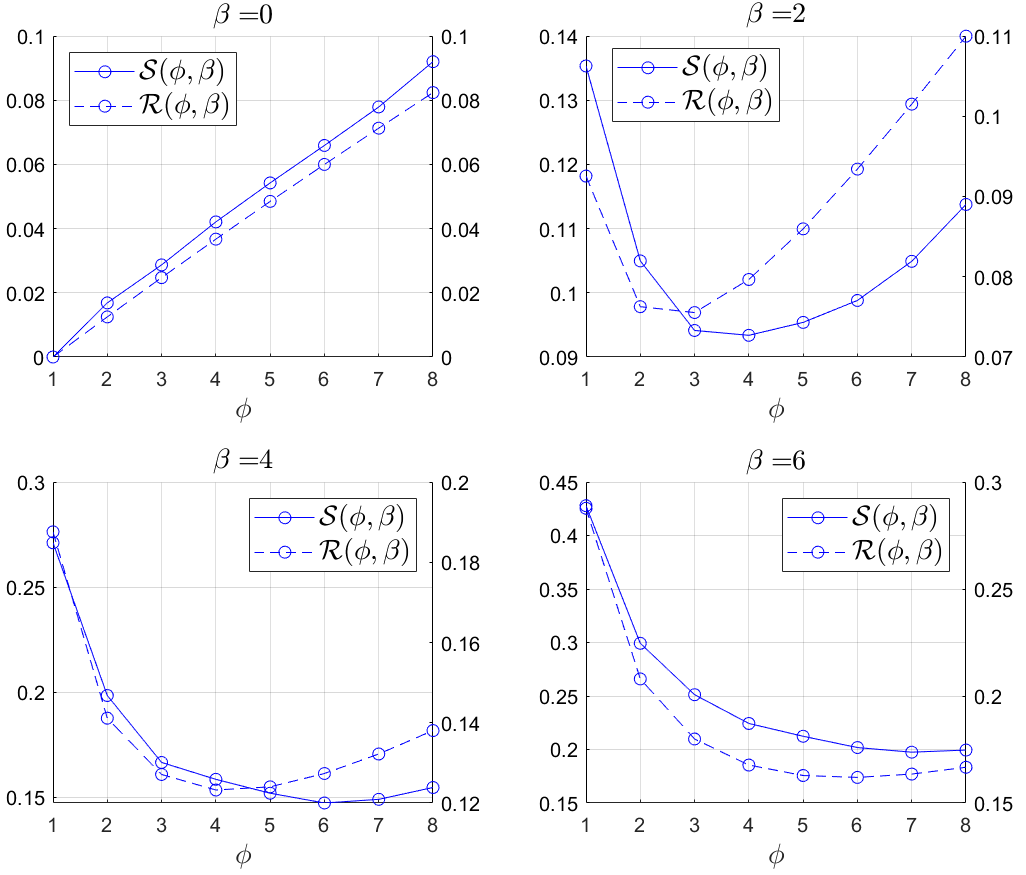

Figure 3 indicates that the value of that minimizes is a lower bound for the value of that minimizes . In other words, minimizing provides a conservative estimate for the time between interaction that minimizes the allocation difference . This is because underestimates the impact of the client’s behavior bias. Specifically, equals the average relative difference between and in any single time interval defined by two consecutive interaction times. Instead, the optimal allocation at any given time depends on all future allocations and, thus, on the future path of the client’s risk aversion. As a result, the behavioral bias in future investment decisions feeds into the investment decisions made at earlier times, and this is accounted for by the measure .

Remark 5.2.

Uniformly spaced interaction times yield a conservative estimate for the optimal interaction frequency. If the client were to interact with the robo-advisor at times triggered by market conditions, then we expect interaction to be more likely to occur after a period of extreme returns. The client would either be overly exuberant following a period of positive returns, or overly pessimistic after a period of negative returns. This magnifies the impact of the client’s behavioral bias, relative to a uniform interaction schedule, and would result in a larger value for . ∎

5.3 Economic Transitions, Risk Aversion, and Investment Performance

We analyze how the optimal investment strategy is affected by economic state transitions and the corresponding changes in the client’s risk aversion. To focus exclusively on the implications of economic transitions on investment decisions, we let the client’s risk aversion depend only on the current economic state. In this case, the risk aversion process in (5.3) takes the form . We calibrate this process so that the resulting optimal allocation is time-homogeneous, given the current economic state. Specifically, in Appendix C (see Proposition C.1) we show that, for a given and , there exists a unique risk aversion process such that the corresponding optimal allocation is given by

| (5.10) |

That is, in times of growth (), the client’s risky asset allocation is equal to ,222222For example, corresponds to the classical 60/40 portfolio composition. This strategy was popularized by Jack Bogle, the founder of Vanguard, and is commonly used as a benchmark in portfolio allocation. and when the economy transits to the recessionary regime (), the allocation changes to , where the value of determines the change in allocation.

It is well known from empirical studies that both the market Sharpe ratio and the risk aversion of retail investors are higher during periods of contractions. Consequently, retail investors may shift wealth away from the risky asset precisely when the benefit of investing, as measured by the expected reward per unit risk, is higher.232323The economic state variable is assumed to be observable, and it follows from (5.1) that the client’s risk aversion reacts instantaneously to a change in economic conditions. In reality, the economic state may be hidden, and its value can only be inferred probabilistically. We expect that extending the model to such a setting would not have a qualitative effect on our results. Namely, the extended model would capture the fact that, throughout the business cycle, the client is on average less willing to invest in the risky asset when the market Sharpe ratio is high. For these investors, a robo-advisor which caters to the client’s wishes would construct a risk aversion process such that . By contrast, a robo-advisor which goes against the client’s wishes would construct a risk aversion process such that , i.e., invest more in the risky asset when the economy is in a state of contraction and the return per unit risk is high.

The remainder of the section proceeds as follows. In Section 5.3.1, we analyze the Sharpe ratio achieved by the optimal investment strategy and its dependence on the parameter . In Section 5.3.2, we analyze numerically the dependence of the client’s terminal wealth distribution on and discuss how the robo-advisor should balance the client’s risk preferences with the opportunity to improve the portfolio’s investment performance.

5.3.1 Sharpe Ratio of Optimal Investment Strategy

The Sharpe ratio of the strategy (5.10) is defined as

| (5.11) |

where and are the long-run242424We compute the “long-run” Sharpe ratio of the strategy , which is independent of the initial economic state, . mean and volatility of the excess returns achieved by :

We recall that is the return of the strategy , between times and , and that is the risk-free rate. In Lemma C.2 we show that the Sharpe ratio (5.11) can be explicitly computed.

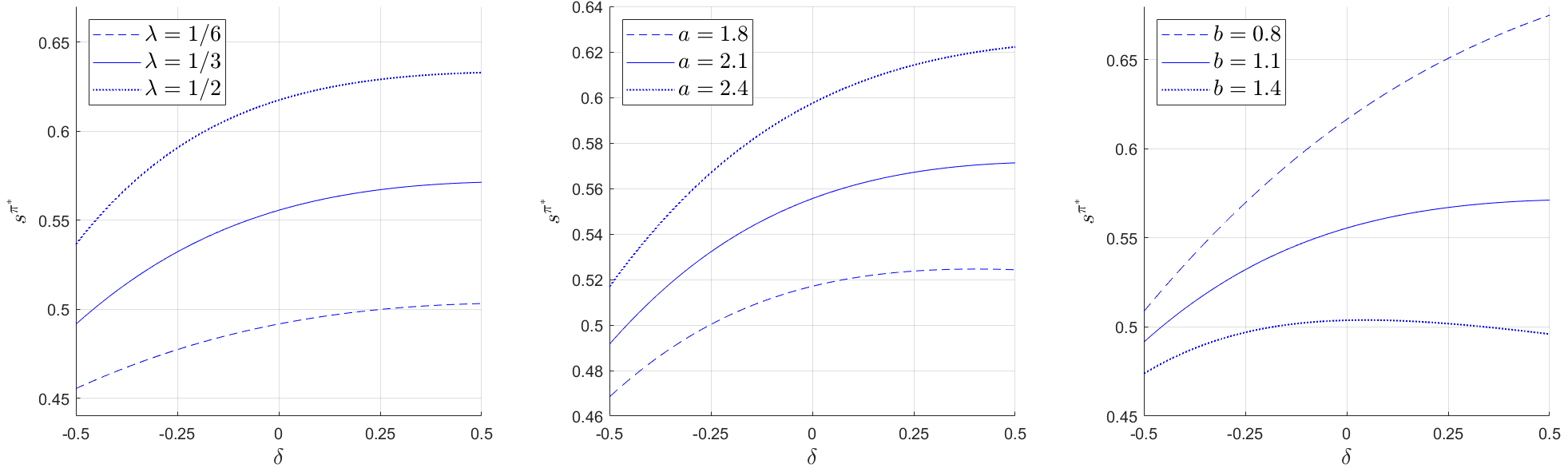

Figure 4 indicates that, for a fixed value of , the portfolio’s Sharpe ratio is increasing in the stationary probability of the recessionary state (). Formally, , and also equals the long-run proportion of time spent in the recessionary state. Additionally, the Sharpe ratio is increasing in , which is the relative change in mean excess returns between the two states, and decreasing in , which is the relative change in the return volatility. These monotonicity properties turn out to hold under mild conditions (see Lemma C.3).

Furthermore, Figure 4 shows that the Sharpe ratio (C.5) is generally increasing in , i.e., it is higher if a larger amount of wealth is invested in the risky asset when the economy is in a state of recession and, thus, the market Sharpe ratio is high. However, as the third panel shows, there may be situations when a larger value of may result in a smaller Sharpe ratio.

In Lemma C.3, we derive the following characterization for the monotonicity of the Sharpe ratio with respect to ,

| (5.12) |

Whether or not the condition above is satisfied depends on the values of and , which determine the difference in market Sharpe ratios between the two economic states. In particular, consider the case where the allocation is the same in both economic states, i.e., . For a fixed , it can be observed from (5.12) that there exists a threshold that needs to exceed for the condition to be satisfied. In other words, for the portfolio’s Sharpe ratio to increase with additional investment during recessions, the market Sharpe ratio needs to be sufficiently high in such an economic state. The reason for why a marginally higher market Sharpe ratio may be insufficient is that larger market returns in an economic state increase both the numerator and the denominator of the Sharpe ratio, because the “between-state” standard deviation of returns is then higher. We refer to the discussion following Lemma C.3 for additional details.

Condition (5.12) is generally satisfied for empirically plausible parameter values. That is, the portfolio’s Sharpe ratio increases if more wealth is allocated to the risky asset when the market Sharpe ratio is high. However, Figure 4 indicates that the gain is modest, and that the Sharpe ratio decreases more when the allocation to the risky asset is decreased, compared to how much it increases when the allocation to the risky asset is increased by the same amount. In Appendix C, we show that is concave in a neighborhood of , namely,

| (5.13) |

This confirms that in order to maintain a satisfactory Sharpe ratio, it is more important not to reduce the risky asset allocation in a state of recession than to increase it.

5.3.2 Wealth Distribution and Cyclicality of Risk Aversion

The portfolio’s Sharpe ratio is determined by the first two moments of its returns, which may not be sufficient to characterize the entire return distribution. Therefore, comparing portfolios in terms of their Sharpe ratios therefore leaves out the impact of higher return moments. This is especially relevant in the presence of multiple economic states, given that the unconditional return distribution is then leptokurtic and skewed.

We use numerical simulations to estimate the terminal distribution of the client’s wealth, for different values of the parameter . We assume monthly portfolio rebalancing (a time step of one month) and set the transition matrix of the state variable to

| (5.18) |

These transition probabilities are based on empirical values reported in Chauvet and Hamilton (2006), who also show that a regime switching model captures well the economic state transitions described by the NBER’s business cycle chronology. These values show that, on average, economic expansions last longer than contractions.

We set the state-dependent return parameters in accordance with Tang and Whitelaw (2011), who report historical averages for changes in the mean and volatility of stock market returns, as well as for changes in the market Sharpe ratio, between the peak of the business cycle and the subsequent trough. Specifically, we set the annual risk-free rate, mean and volatility of market returns to

| (5.19) |

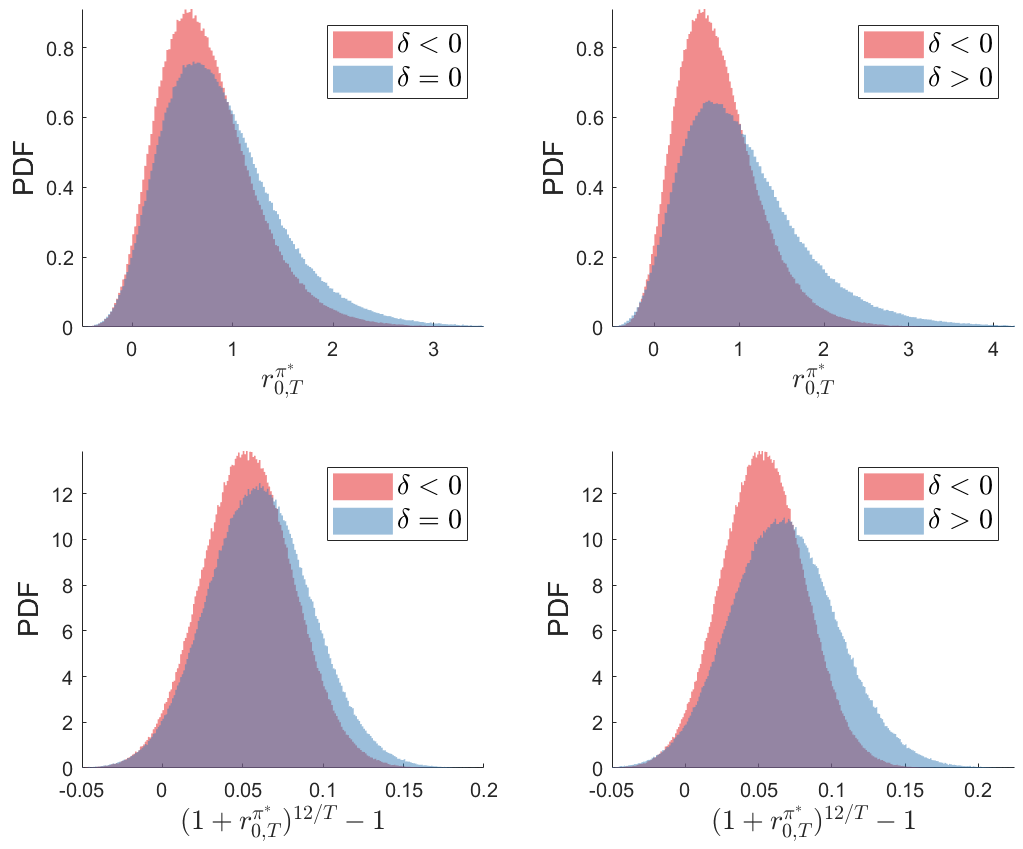

Figure 5 shows the simulated distribution of the return of the optimal investment strategy at maturity, and the corresponding annualized rate of return. It is evident from the figure that the skewness and kurtosis are higher when the risky asset allocation is maintained or increased in a state of recession, and that in those cases, the return upside is considerably higher, with a limited additional downside risk. The same pattern is observed from the summary statistics of the simulations, reported in Table 1.

The above findings indicate that both the Sharpe ratio and the terminal wealth achieved by the strategy defined in (5.10) are higher if , compared to the case . In other words, the investment benefits are greater if the risky asset allocation is maintained or increased during recessions (). The question thus arises of how far the robo-advisor can reach “against the will” of a client whose risk preferences are countercylical and thus consistent with the case .

While higher expected returns will be obtained in the long run, the client may suffer from adverse market moves in the short run, and may not have an adequate understanding of the long-term benefits. In a state of recession, with worsening economic outlook and risk aversion rising, the client may be particularly sensitive to what can be perceived as an investment mistake of the robo-advisor. The importance of this dilemma faced by robo-advisors is emphasized by Rossi and Utkus (2019a), who show empirically that algorithm aversion, i.e., the tendency of individuals to prefer a human forecaster over an algorithm, and to more quickly lose confidence in an algorithm than in a human after observing them make the same mistake (Dietvorst et al. (2015)), is one of the main obstacles for the adoption of robo-advising.

Our analysis suggests that a good middle ground for the robo-advisor is to encourage the client to simply maintain a fixed portfolio composition, which is consistent with the long-term investing principle of riding out business cycles. To that end, the robo-advisor may present statistics such as those reported in Table 1 and Figure 5 to the client. Thus, the client may observe that, over time, higher returns can be earned with limited additional risk by maintaining exposure to the risky asset during recessions instead of reducing it.252525In the context our model, this amounts to “changing” the client’s risk aversion process from such that , to . We recall that is the risk aversion process implied by the strategy given in (5.10). This behavior would also be consistent with that of most robo-advising firms. Namely, modifying the portfolio allocation based on economic conditions is a form of active management and, in general, robo-advising firms which focus on long-term investing do not engage in such market timing.262626One of the claimed benefits of robo-advising is that by managing the portfolio on the client’s behalf, the client is helped to resist the temptation of attempting to time the market. The robo-advising firms Betterment and Wealthfront also mention empirical work, such as the Dalbar’s annual Quantitative Analysis of Investors report, which shows that investors who try to time the market tend to perform much worse than a “buy-and-hold” investor, and that the average investor significantly underperforms a broad stock market index. Rather, they urge clients to stay the course through changing market conditions, in order to reap the benefits of long-term investing.

| Mean | SD | Skewness | Kurtosis | 90% VaR | 95% VaR | 99% VaR | |

|---|---|---|---|---|---|---|---|

| 0.740 | 0.485 | 0.838 | 4.257 | -0.179 | -0.067 | 0.117 | |

| 0.881 | 0.589 | 0.970 | 4.712 | -0.213 | -0.085 | 0.118 | |

| 1.036 | 0.735 | 1.231 | 5.934 | -0.233 | -0.091 | 0.134 | |

| 0.053 | 0.029 | 0.066 | 3.011 | -0.017 | -0.006 | 0.012 | |

| 0.061 | 0.032 | 0.092 | 3.016 | -0.019 | -0.008 | 0.012 | |

| 0.068 | 0.037 | 0.162 | 3.089 | -0.021 | -0.009 | 0.014 |

6 Concluding Remarks

The past decade has witnessed the rapid emergence of robo-advisors, which are online platforms allowing clients to interact directly with automated investment algorithms. Recent literature has provided empirical evidence on the characteristics of those investors who are more likely to switch to robo-advising, and how robo-advising tools affect the portfolio composition of investors.

In this work, we build a novel framework that incorporates important features of modern robo-advising systems. In this framework, a robo-advisor undertakes the task of optimally investing a client’s wealth. The client has a risk profile that changes in response to market returns, economic conditions, and idiosyncratic events, and to which the robo-advisor’s investment performance criterion dynamically adapts. We derive and analyze optimal investment strategies, and highlight the role of risk aversion process in driving the intertemporal hedging demand.

The frequency of interaction between the client and robo-advisor determines the level of portfolio personalization, which is defined in terms of how accurately the robo-advisor is able to track the client’s risk profile. We show that there exists an optimal interaction frequency, which maximizes portfolio personalization by striking a balance between receiving information from the client in a timely manner, and mitigating the effect of the client’s behavioral biases.

We quantify how the Sharpe ratio of the optimal investment strategy depends on the allocation of wealth within economic regimes, and study the potential gains achieved by a robo-advisor’s strategy during periods of high market Sharpe ratio. The implementation of this strategy may require the robo-advisor to go against the client’s wishes, because both the client’s risk aversion and the market Sharpe ratio tend to be countercyclical. We show that by simply rebalancing the portfolio to maintain constant weights throughout the business cycle, the portfolio’s Sharpe ratio is close to being optimal. We also show that the portfolio return distribution is significantly improved relative to the situation where the investment in the risky asset is reduced during periods of economic contractions.

Our framework can be extended and further aligned to the practices of modern robo-advising systems. Indeed, the market model can be allowed to include multiple tradable assets and portfolio rebalanced only if the portfolio weights have drifted significantly from the target weights, due to price moves of the underlying securities. Robo-advisors generally use such threshold updating rules to rebalance their portfolios (Beketov et al. (2018)), while minimizing expense ratios and maximizing tax efficiency. Furthermore, the regime switching model can be generalized to make the economic state variable hidden, in line with the fact that economic conditions are typically not transparently observed, or observed with a lag. If the state variable is hidden, then the robo-advisor runs the risk of not acting in the client’s best interest by making investment decisions based on misclassified economic conditions. Finally, one may account for noise in the information communicated by the client. As the level of noise is expected to increase with the frequency of interaction, this would act as a further incentive to reduce interaction with the client.

Herein, market returns are assumed to be conditionally independent of economic state transitions. Nevertheless, these transitions are commonly associated with significant market moves, in particular when the economy enters a recession.272727This is also the case in the consumption-based asset pricing frameworks which generate countercyclical variation in risk aversion, such as Campbell and Cochrane (1999). In their framework, a worsening economic outlook leads to an increase in risk aversion, and investors demand higher reward for carrying risk, which in turn leads to a fall in stock prices. Such market moves would effectively result in the client “buying high” and “selling low”, and thus exacerbate the adverse effects of comonotonicity between risk aversion and the market Sharpe ratio. This would further incentivize the robo-advisor to act against the client’s wishes, e.g., if a market drop is likely to happen following a change in economic conditions, the portfolio’s market exposure could be adjusted to account for the probability of a near term market drop.282828Portfolio allocation under regime switching is widely studied. Related to our work, Tang and Whitelaw (2011) show how simple market timing strategies can exploit the fact that Sharpe ratios are countercyclical, and Coudert and Gex (2008) show that risk aversion indices published by financial institutions are good leading indicators of stock market crises. Kritzman et al. (2012) show how a Markov switching model can be used to avoid large portfolio losses related to “event regimes”, during which asset return dynamics start deviating from their past levels and the market risk premium is low.

Appendix A Properties of Optimal Investment Strategy

A.1 Computation of Optimal Investment Strategy

In the following proposition, we provide a characterization of the optimal investment strategy given in Proposition 4.1, which depends on recursively computable expressions.

Proposition A.1.

The optimal allocation in Proposition 4.1 admits the representation

| (A.1) |

for any , where

| (A.2) | ||||

The sequences and satisfy the recursions

| (A.3) | ||||

with , for all .

The quantities and in Proposition A.1 are the first and second moments of the future value of one dollar invested optimally between time and the terminal date , conditionally on . That is,

| (A.4) |

with the simple return defined in (3.6). Because both and are independent of the wealth at time , it follows from (3.8) that the value function at time is also independent of , and given by

| (A.5) |

Finally, Proposition A.1 shows that the optimal proportion of wealth allocated to the risky asset, , is also independent of the wealth variable.

The expected values in (A.2) admit integral representations, which in turn can be used to compute the expected values in (A.3). Next, we provide such a representation for , both in the general case and in the specific case described in Section 5.1.

Lemma A.2.

-

(a)

Assume that given , the random variable admits a generalized probability density function, . Then,

where , and is such that , , , and . The value of is determined by the triplet . If , then , while if , is determined by .

-

(b)

For the model in Section 5.1, i.e., where the risk aversion process is given by (5.3) and the interaction times are of the form , for some , we have