On Unbiased Simulations of Stochastic Bridges Conditioned on Extrema

Abstract

Stochastic bridges are commonly used to impute missing data with a lower sampling rate to generate data with a higher sampling rate, while preserving key properties of the dynamics involved in an unbiased way. While the generation of Brownian bridges and Ornstein-Uhlenbeck bridges is well understood, unbiased generation of such stochastic bridges subject to a given extremum has been less explored in the literature. After a review of known results, we compare two algorithms for generating Brown-ian bridges constrained to a given extremum, one of which generalizes to other diffusions. We further apply this to generate unbiased Ornstein-Uhlenbeck bridges and unconstrained processes, both constrained to a given extremum, along with more tractable numerical approximations of these algorithms. Finally, we consider the case of drift and applications to geometric Brownian motions.

1 Background

Stochastic bridges find applications in a wide range of domains from finance to climatology. It is often necessary to interpolate insufficiently frequent time series data stochastically while preserving as much as possible of the dynamics underlying the original data. A natural question then is how to construct a stochastic bridge, i.e., a stochastic process whose end points are known a priori. These have been used for studying spectral statistics of polarization mode dispersion [S2], modeling fermions trapped in a trap [DMS], modeling animal movement patterns [BSAW], valuing financial securities [CMO] and improving the performance of quasi-Monte Carlo methods for high dimensional problems in computational finance [LW] [K]. Sometimes, there is a further need to generate a bridge subject to additional constraints, such as a given mean (see [M]), or on an extremum. For example, a scenario generator may wish to consider worst-case scenarios where an asset attains a given lowest value to test how a financial instrument would behave under certain unfavorable market conditions, or we may wish to interpolate simulated thermodynamic scenarios where the temperature reaches a certain maximum.

This paper will provide tools for industry to go beyond simple Brownian bridges to allow for some features of more realistic dynamics including drift, geometric Brownian motion and mean reversion, for use in stress tests that condition on extreme values of an asset. For example, the generation of geometric Brownian bridges subject to extrema may be used for the valuation of barrier options whose barrier event has not yet been breached. The algorithms presented in this paper could also be used by banks for data quality remediation problems in VaR models where input time series data is sparse.

We first show how to generate Wiener processes subject to bridge and/or extremum conditions in an unbiased (i.e., measure-preserving) way, and then provide and compare two methods for generating such processes subject to both bridge and extremum conditions. Our first method is much more rapid, while the second generalizes more broadly. We will then consider mean-reverting dynamics by extending this problem to Ornstein-Uhlenbeck processes. Finally, we consider Wiener processes with drift, and geometric Brownian motions, which underlie the Black-Scholes pricing model.

We now introduce some preliminaries. First, we slightly abuse terminology by allowing a Wiener process to start at an arbitrary initial value . A Brownian bridge is a Wiener process over conditioned on . An Ornstein-Uhlenbeck (OU) process is a simple mean-reverting stochastic process given by the SDE

| (1) |

for some standard Wiener process . Then is the mean and is the mean reversion rate. An Ornstein-Uhlenbeck bridge is an OU process over a closed interval conditioned on the values at the endpoints.

In section (2) we provide two unbiased constructions of Wiener bridges conditioned on extrema. In section (3) we generalize the second of the methods in section (2) to construct OU bridges conditioned on an extremum, and discuss the numerical and computational concerns and reasonable approximations involved. In section (4) we consider how to construct an open-ended (i.e., non-bridge) Ornstein-Uhlenbeck process constrained on an extremum. In section (5) we consider the case of Wiener processes with drift, or equivalently geometric Brownian motions.

First, we discuss those problems already addressed in the literature (1-5), and then those which we address in this paper (6-9).

-

1.

For the sake of completeness, a Wiener process without bridge or extremum conditions has a trivial construction. Computationally, the Euler-Maruyama method may be used, successively incrementing by , where .

-

2.

An OU process without bridge or extremum conditions may be constructed from a Wiener process directly via equation 1. Computationally, the Euler-Maruyama method may be used.

-

3.

A Brownian bridge may be constructed as follows: Given a Wiener process with variance and such that , we set

Then is a Brownian bridge on from to , also with variance . Furthermore, the induced mapping has the correct measure, that is, the construction of is unbiased provided the simulation of is unbiased. Equivalently, the SDE for such a Brownian bridge is given by

(2) with initial condition .

-

4.

An OU bridge may be constructed as follows: Given a Brownian bridge with variance over such that , set and simulate the SDE

(3) Then is an OU bridge with variance between and . See [C] for details.

-

5.

An open-ended (i.e. non-bridge) Wiener process conditioned on an extremum may be constructed as follows. To simulate a Wiener process over an interval starting at and conditioned on a maximum , we follow the solution for the equivalent dual case (i.e., for the minimum) in [BPR], following results in [BCP]. First, assume without loss of generality that . Construct a Brownian bridge from to over the same interval . Then, find , the first time this bridge hits . Take the first portion of this process up to , and append potentially repeated reflections as follows:

This selects as an unbiased Brownian motion starting at 0 with maximum on the same interval (and no condition at ). To construct this for an arbitrary initial point , simply construct

-

6.

We discuss an algorithm that constructs an open-ended OU process conditioned on an extremum in section (4).

-

7.

We demonstrate how to construct a Brownian bridge conditioned on an extremum in section (2), in two different ways, and compare the results.

-

8.

We discuss an algorithm that constructs an OU bridge conditioned on an extremum in section (3).

-

9.

We discuss an algorithm that constructs an open-ended Brownian process with positive drift (or equivalently a growing geometric Brownian motion) constrained on an extremum in section (5). The case for bridges with drift follows immediately from case 7 above.

2 Wiener Bridges Conditioned on Extrema

Without loss of generality, consider the space of Brownian bridges on , with variance , , conditioned on a maximum . We construct a generator for such processes, unbiased according to the standard measure (induced from the Wiener measure), in two different ways.

2.1 Method 1: Construction via Brownian Meanders

By [I], a ‘standard’ Wiener meander over with and may be constructed from three standard Wiener bridges over from 0 to 0 as follows:

| (4) |

Note that this is a 3-dimensional Bessel process with drift. Furthermore, this construction is unbiased according to the standard measure.

Remark 2.0.1.

Note that with the notation above, from the scaling property of Wiener processes and checking the values at the endpoints, it follows that

is a Wiener process with variance , and values at and at , with the measure of a conditional Wiener process preserved.

By [AC], we note that the joint density of the minimum and location of the minimum of a Brownian bridge with variance 1 from to over is

|

|

and the density of the minimum alone is

so that the conditional density is, for ,

| (5) |

This only depends on through . Wiener processes with initial value and standard variation transform positively and affinely to standard Wiener processes via , so this transformation preserves location of maximum and minimum. This transformation scales all random increments by , so is an isomorphism at the level of measure, and the probability density for the location of the maximum and minimum is preserved.

The minimum of a standard Brownian process is exactly the maximum of its negative, so negating in the above formula and setting , we find after scaling by that, for ,

| (6) |

This presents the following algorithm:

Input.

Output:

Proposition 1.

Steps 1-5 above generate an unbiased Brownian bridge over from to with variance and maximum .

Proof.

Since Wiener processes have stationary independent increments by definition, the selections of the location of the maximum and unscaled meanders are independent, so that in the Wiener measure we have (suppressing the conditions ):

Each factor was generated according to its law. The scaling preserves the independence and ensures Brownian meanders of the correct variance, maximum and endpoints, so the resulting process is an unbiased Brownian bridge. ∎

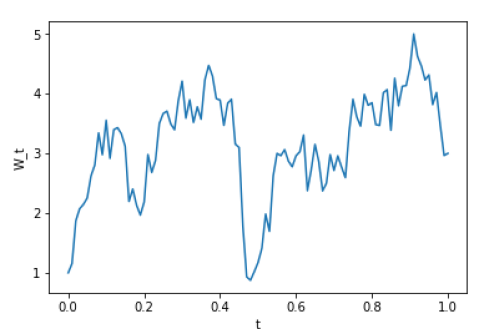

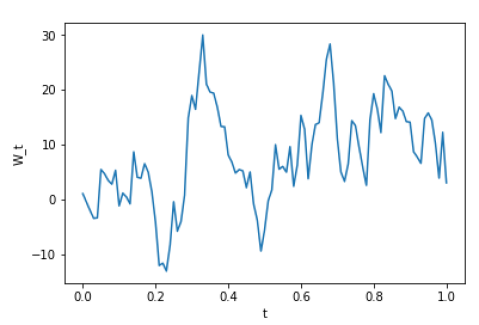

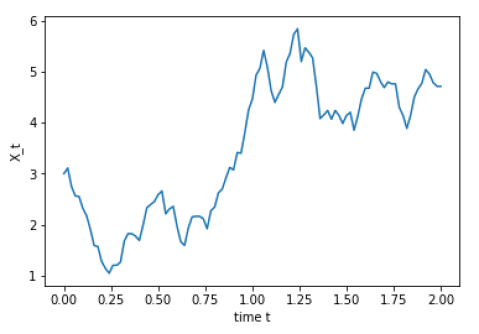

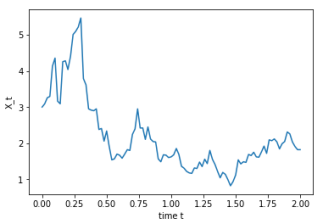

We illustrate a few examples from a Python implementation of 1 below. First we generate Wiener bridges on from to conditioned on a maximum of 5, with :

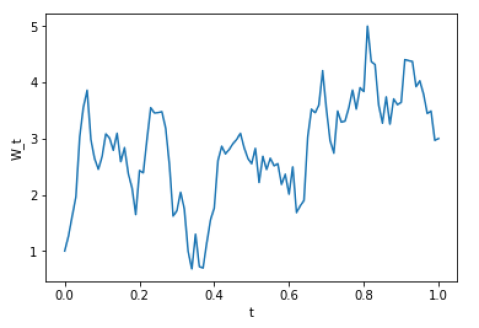

We then run this algorithm to generate Brownian bridges on from to conditioned on a maximum of 5, with :

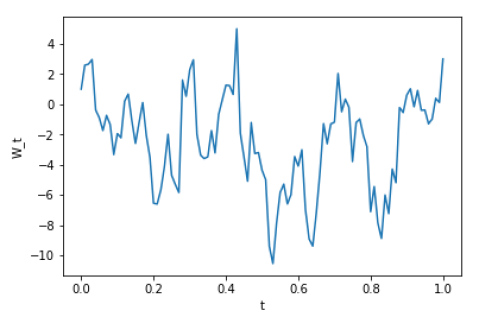

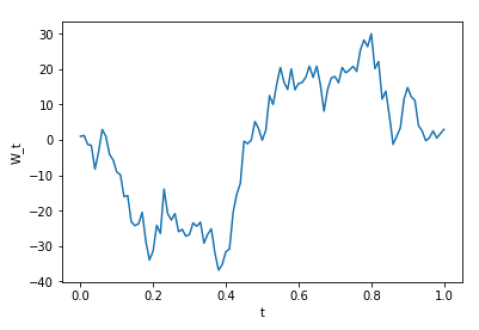

As a final example, we run the algorithm to generate Brownian bridges on from to conditioned on a maximum of 30, with :

As expected, the process is forced far below the initial and final values, having high volatility but being constrained from above (but not below).

2.2 Method 2: Construction via Bayesian Increments

2.2.1 Procedure

We consider the full joint density of the maximum and location of the maximum as provided in [AC], to simulate the Brownian motion from with volatility conditioned on and , without bias.

First, consider and assume the standard measure. We start with , , and successively increment by . As we proceed there are two cases:

-

1.

The process has not yet achieved its maximum. That is, we assume for all . We consider a discrete time increment and wish to find the probability density of . By Bayes’ Law we have, density-wise,

(7) Here the condition pertains to every factor but may be suppressed since has independent and stationary increments.

For the remaining two factors, given the density of the minimum of a Brownian bridge as found in [AC], the symmetry of Wiener processes allows us to find the density of the maximum of a Brownian bridge by negating and :

(8) Briefly suppressing the condition , we consider whether the (almost surely unique) maximum is attained between or , and further note that

We integrate to find

(9) Remark 2.0.2.

As ,

and

like , and so both are dominated as by the remaining factors in the full quotient, which take the form

Thus, for the purposes of computation, as we can take the maximum over instead of for the numerator, simplifying the expression in implementation when is very small. In this paper we keep the full expression.

This gives us an SDE in the first case, as in the algorithm we can select at random from this distribution:

-

2.

The process has achieved its maximum already. In this case we do not require the maximum to be attained on (in fact, it almost surely is not), and just require that is bounded from above by there, so that we have

which we can find explicitly from equation 9.

-

3.

Endpoint. Until now we have assumed that the had an interval of nonzero length to its right. Finally, after incrementing through all but the last value, we must set .

The whole procedure follows similarly for minima. However, there are numerical considerations beyond those for the usual bounds and stepsizes in numerical integration. For example, to ensure that truncation error does not hinder the pre-extremum/post-extremum bifurcation in the algorithm, we set a range of acceptable closeness to the extremum when we check whether the extremum has been attained. When incrementing, we should also set a range of possible increments to select from, weighted by the correct probabilities.

2.2.2 Rectification

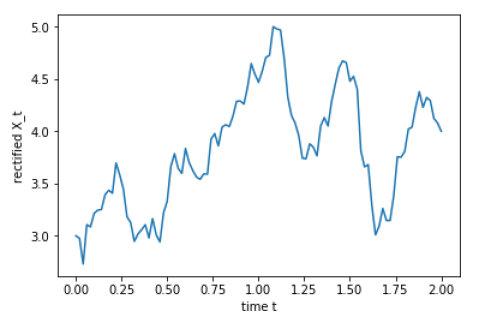

After approximating a Wiener process meeting the conditions in an unbiased way, a simple rectification of the conditions as follows is justifiable for practical purposes. That is, given a range of acceptable closeness to the maximum, , to ensure that the error does not hinder the pre-extremum/post-extremum bifurcation in the algorithm in this subsection, we scale the final process as follows.

Let be the actual maximum of the numerically generated bridge. First we adjust to ensure the maximum is attained exactly (rather than within ) by postcomposing with

Denote the new right-hand end point by . Then, to adjust the final value back to , we replace only that section of the bridge after the maximum by its postcomposition with

Then we have traded one error for another: we have slightly adjusted the dynamics, which may be viewed as having a slight effect on , but the more visible endpoints and maximum are held to exactly.

2.2.3 Implementation

We present the algorithm below, which may be applied to more general processes.

Input. dynamical parameters,

Output. A time vector , approximating the bridge with given dynamics over from to constrained to the maximum .

The choice of may be decided case by case. In general, one approach might be to find when the cumulative probability of the minimum (without constraint to a maximum)

which in turn can be found directly from the probBound function by considering the dual case of the process . In the case of the Brownian bridge constrained to a maximum from to at a given , we have

Solving for , we find

the only one of the two solutions less than . It would also be possible to compute a new at each step over the interval , but this is slightly more computationally expensive and relies on previous simulations rather than taking account of .

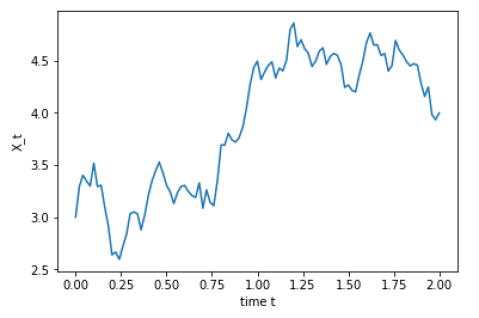

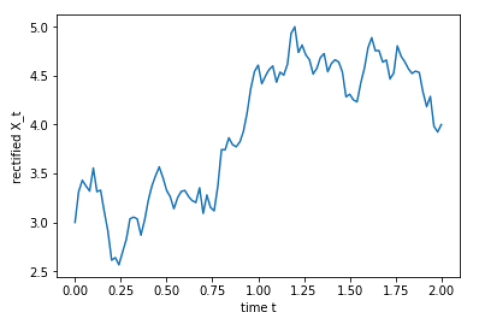

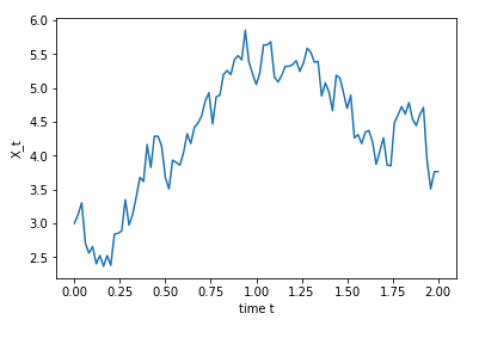

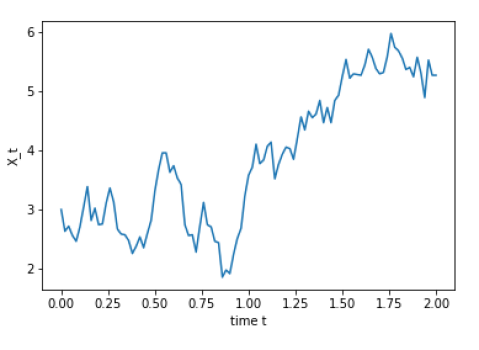

Below we show corresponding unrectified and rectified examples of Wiener bridges generated under method 2 (construction by Bayesian increments) over the time interval from 3 to 4 with standard deviation , conditioned on maximum . We take and , with the number of possible increments from which to make the density-weighted selection at each increment.

We note that the results indeed generate bridges subject to the maximal condition, the apparent variance behaves as expected, and the difference between corresponding unrectified and rectified bridges is minor upon inspection.

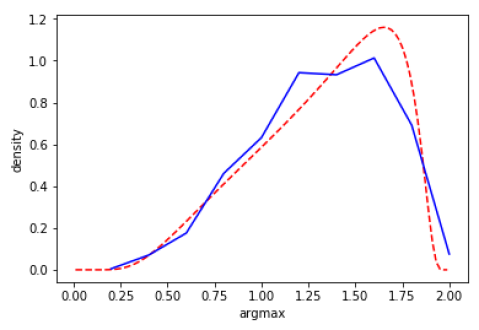

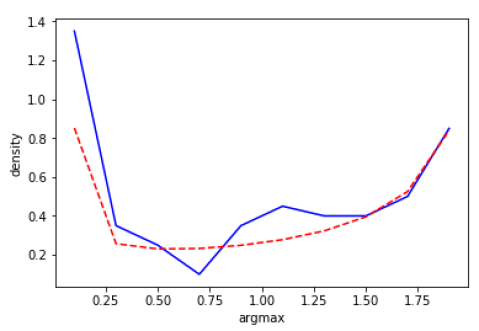

To test that the numerical generation is reliable, we may verify that the distribution of the argmax also follows the result from [AC]:

These visibly agree quite closely. We conclude the fit is good and the simulation is successful for the choices made for these numerical parameters.

We note that for the same parameters, Method 1 (construction via Brownian meanders) took 0.004 seconds to generate the bridge and Method 2 (construction via Bayesian increments) took 10.14 seconds using a 2.6GHz Intel Core i5-7300U CPU. Both methods are linear in the number of timesteps. Clearly the method using meanders is much faster, but the method of Bayesian increments is more generalizable whenever the unconditioned SDE and the density of the extremum are known.

3 Ornstein-Uhlenbeck bridges conditioned on extrema

We seek a construction of an OU-process from to with volatility conditioned on and , without bias. Again, consider and assume the standard measure.

We note that it is possible to run through algorithm 2 as before, provided we have the density for a given increment in an unconstrained OU bridge, and the density of the maximum of a general OU bridge. The solution of the latter is a difficult problem, and unfortunately one convergent solution we discuss requires multiple nested loops to compute. Even with a more easily computable approximation, both Python and C++ implementations are still impractically slow on a 2.6GHz Intel CPU. Analysis of results using a GPU are pending further research.

Here and elsewhere, we note that the location of an extremum for any diffusion process is almost surely unique (see [KS]).

We find in the unconditioned OU bridge case that

that is

We find from [CFS] that for a general linear diffusion we have the joint probability density form

where is the scale function, is the speed measure for the unconditioned OU process, and is the density of the hitting time of at for a process with the same dynamics starting at . Our and are given, so we normalize this by

to find the conditional probability density.

For linear diffusions with Markov processes given by

we have

where

The Markov generator of the OU process is

Therefore, given we set the process to start at time 0, we may take

The hitting time does not have a known easily tractable “analytic” solution but may be efficiently given as the limit of a sequence given by Lipton and Kaushansky (2017) [LK] based on a method found in Linz [L], or approximated by other methods detailed further below.

Lipton and Kaushansky proceed by transforming the hitting time problem to a system of equations whose solution depends on the solution to Volterra equations. In particular, they first normalize the OU process to a simpler OU process

with the same initial value, and then demonstrate that the hitting time -density of a thus normalized OU process starting at hitting and evaluated at , is

for , and where is the solution to a Volterra-type integral equation of the second kind,

Thus to find the required density, it remains to solve for above.

We define

the kernel of this integral operator.

Lipton and Kaushansky propose a “block by block” method based on a method found in [L], based on quadratic interpolation, as follows.

First, define the following functions

For faster implementation, these evaluate to

Further, define

Then for timesteps , and a desired stepsize , set , repeat the following steps for to :

-

1.

For , compute .

-

2.

Solve the following system of equations for and append them to the list of known :

Explicitly, at each stage we set

Then we have

Then as , pointwise on , .

All functions and operations used to find the incremental probability density are continuous, and thus it follows that algorithm 2 simulates an unbiased OU process with the given bridge and extremum conditions.

For implementation purposes, we set by solving for

numerically by minimizing

given by the methods in this subsection, and where the dynamics of are given by parameters .

We may cut down on computation time by using an approximation of the hitting time found in [LK] from first-order truncation of the governing Volterra equation to an Abel equation and solving via Laplace transforms. This does not formally converge to the correct result, but greatly decreases computation time, and holds for . Since the values of in this context are within the range of the increment , we make this assumption. We set

where and

As before, after approximating an OU process meeting the conditions in an unbiased way, applying the same simple rectification in the algorithms may be justifiable for practical purposes, if the maximum is desired to be reached on one of the actual numerical increments. In this case, such rectification trades errors the constraint variables () for errors in the dynamical variables , in different ways on either side of the actual maximum.

4 Open-Ended Ornstein-Uhlenbeck processes conditioned on extrema

The case of open-ended OU processes conditioned on extrema (without loss of generality, a maximum ) proceeds mostly as in algorithm 2, except that we do not specify a last value after the loop, and pMaxLeft and pBoundLeft are computed quite differently from pMaxRight and pBoundRight. In particular, pMaxLeft and pBoundLeft are computed using the density and distribution formulae for the bridge case as in section 3 (since for these we condition on the endpoints of the interval ), while pMaxRight and pBoundRight are computed using the density and distribution for the open-ended case (since we no longer have the condition ).

The density of the increment of the unconstrained open-ended OU process is given by

and

where the right-hand side is as in section 3.

may again be solved for numerically, as in section 3. In actual implementation, the last value cannot be given as , and the incremental process assumes an interval of positive length between and . For this one point we set for simplicity.

5 Brownian motion with drift and geometric Brown-ian motion conditioned on extrema

We consider the case of drift and geometric Brownian motion, particularly important in quantitative finanace as it underlies the Black-Scholes model. The case for bridges is in fact trivial, since a Brownian motion with drift constrained to bridge conditions is in fact independent of its drift. To see this, consider a Brownian motion with drift on from to , and add a drift . Then by the SDE (equation 2) we have

which is exactly the same as the original SDE in . Therefore, the problem of constructing a Brownian bridge with drift to a given extremum is already solved in (3). A geometric Brownian bridge on from to with maximum and drift (with all necessarily positive) is then precisely (and in law) given by where is a Brownian bridge on from to with maximum .

Our construction of an open-ended Brownian motion with given variance and drift (and correspondingly an open-ended geometric Brownian motion) constrained to a given maximum over relies again on a Bayesian incremental method. If we assume an initial value , a volatility , drift coefficient , then the transformation induces an initial value 0, a drift coefficient and a maximum . The problem is thus equivalent to simulating a Brownian motion with drift and volatility 1, constrained to a maximum over with initial value 0, which we assume without loss of generality.

The density of the maximum of such a Brownian motion with drift may be found in [BO], from an application of Girsanov’s theorem:

| (10) |

Integrating and setting the value at infinity to 1, we find that the probability that is bounded by on is

| (11) |

The unconditioned density of an increment after a given increment is given directly from the defining SDE by

| (12) |

As in section 4, we follow algorithm 2 with the exception that pMaxLeft and pBoundLeft are computed as for the bridge process over from to (recalling that these are independent of and are the same as in section 2.2), and pMaxRight and pBoundRight are given for the open-ended case. That is, we define pBoundLeft from equation 9, pBoundRight from equation 11, pMaxLeft from equation 8, pMaxRight by equation 10, and DensityIncrementUnconstrained from equation 12.

In our implementation, we find numerically by solving for

We use a Brent solver to minimize

As in section 4, the last value cannot be given by a predefined value , and the incremental process assumes an interval of positive length between and . For this one point, we assume for simplicity that .

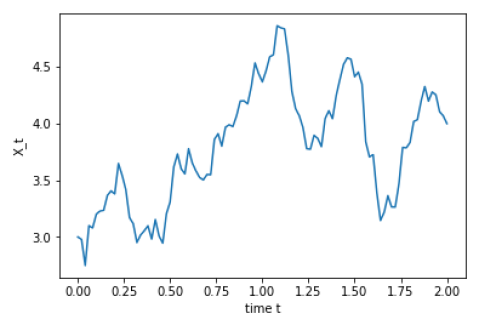

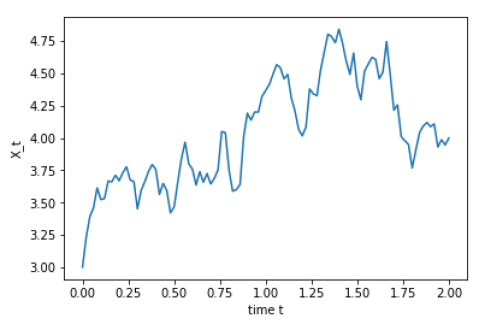

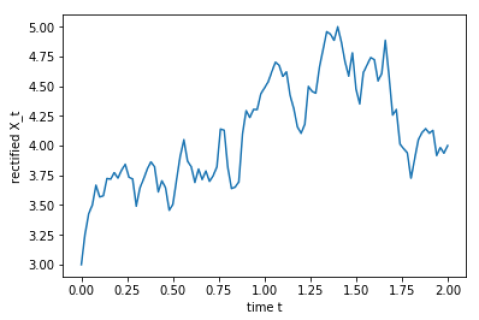

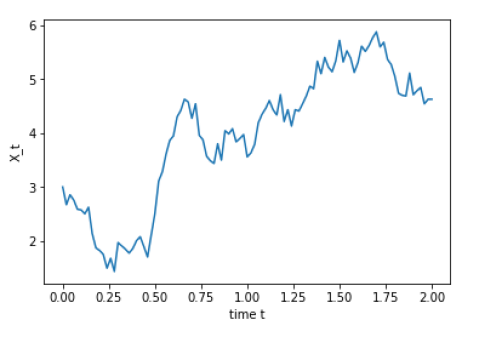

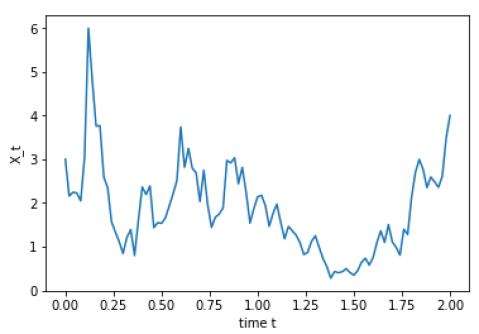

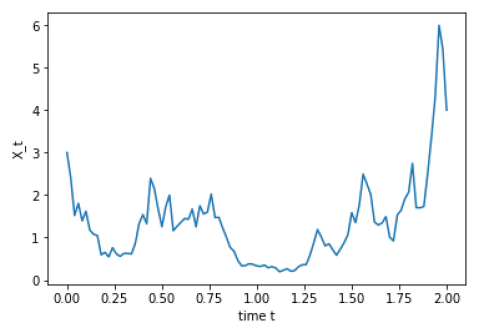

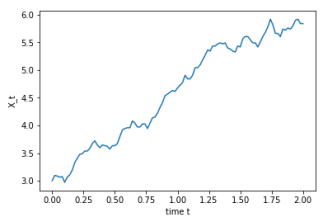

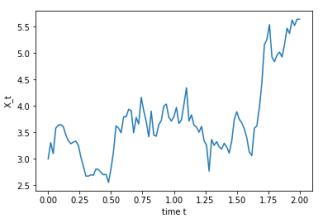

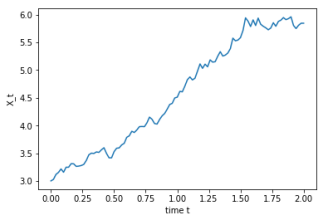

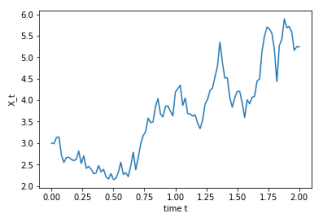

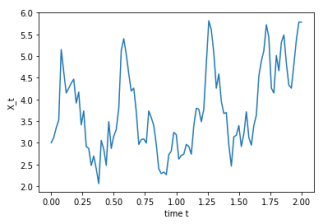

We used our implementation to simulate Wiener processes over starting at 3 with drift and volatility . Numerically, we set , , , and . We show examples below.

Note that we did not rectify the maximum value. The plots show expected behavior. Mean computation time was 21.69 seconds despite the decrease in from 10000 to 1000. Setting to 10000, the mean computation time was 169.47 seconds.111using a 2.6GHz Intel Core i5-7300U CPU The density of the location of the maximum (unconstrained on the maximum value) is found in [KS] to be

| (13) |

This density is the same for in our case.

We see similar distributions for 10 bins, after randomly generating the maximum according to equation 10. We plot both the experimental and theoretical densities for 10 bins below.

These appear to agree fairly closely. We conclude that the fit is good and the simulation is successful for the choices made for these numerical parameters.

Finally, we exponentiate to illustrate the case for geometric Brownian motion, which we take over , starting at 3, conditioned on a maximum of 6. For the bridge case, we simulate the logarithm with the method of 2.1, and assume a value of 4 at , volatility 2 and exponential drift coefficient 1. We simulate 100 timesteps.

For the open-ended case we simulate 100 timesteps with and . First we take drift coefficient 0.2, with volatility 0.1 and 1 respectively:

The simulation meets the maximum condition and the behavior of the simulation as volatility increases as expected.

Increasing the drift coefficient to 0.5, retaining volatility over the same range:

This construction lends itself to several applications. If the underlying of an option is known to have attained a given maximum, but the current payoff of the option is not known, its value can be estimated by Monte Carlo simulation over geometric Brownian bridge (i.e., Black-Scholes) scenarios conditioned on a given extremum. Barrier option pricing in particular is sensitive to this condition. We will save these applications for a later paper.

DECLARATION OF INTEREST

The authors alone are responsible for the content and writing of this paper. The information and views expressed by the authors are their own and not necessarily those of Ernst & Young LLP or other member firms of the global EY organization.