Efficient Estimation for Generalized Linear Models on a Distributed System with Nonrandomly Distributed Data

Feifei Wang1,2, Danyang Huang1,2, Yingqiu Zhu1, and Hansheng Wang3

1 Center for Applied Statistics, Renmin University of China, Beijing, China;

2 School of Statistics, Renmin University of China, Beijing, China;

3 Guanghua School of Management, Peking University, Beijing, China.

Abstract

Distributed systems have been widely used in practice to accomplish data analysis tasks of huge scales. In this work, we target on the estimation problem of generalized linear models on a distributed system with nonrandomly distributed data. We develop a Pseudo-Newton-Raphson algorithm for efficient estimation. In this algorithm, we first obtain a pilot estimator based on a small random sample collected from different Workers. Then conduct one-step updating based on the computed derivatives of log-likelihood functions in each Worker at the pilot estimator. The final one-step estimator is proved to be statistically efficient as the global estimator, even with nonrandomly distributed data. In addition, it is computationally efficient, in terms of both communication cost and storage usage. Based on the one-step estimator, we also develop a likelihood ratio test for hypothesis testing. The theoretical properties of the one-step estimator and the corresponding likelihood ratio test are investigated. The finite sample performances are assessed through simulations. Finally, an American Airline dataset is analyzed on a Spark cluster for illustration purpose.

KEY WORDS: Distributed System; Generalized Linear Models; Likelihood Ratio Test; Newton-Raphson Algorithm.

1. Introduction

With the rapid development of technology, massive data are often encountered in both scientific fields and daily life (Gopal and Yang, 2013; Battey et al., 2015). In many cases, such a huge dataset is usually hard to be efficiently dealt by one single computer, but needs a large set of connected computers, which are referred to as a distributed system (Duchi et al., 2014). Here, we consider a standard “master-and-worker” architecture for distributed systems, which is the most popularly used type in practice (e.g., Hadoop, Spark, etc). Under this architecture, a computer serves as the Master, while all the other computers serve as Workers. The analysis task of a huge dataset is then divided into pieces, each of which is solved by one Worker. Therefore, the use of distributed systems enable us to accomplish data analysis tasks of huge scales (Andrews, 2000; Gopal and Yang, 2013; Battey et al., 2015).

In distributed systems, two problems are often worth of consideration. The first one is communication cost, which refers to the wall-clock time from inter-computer communication. In a standard “master-and-worker” distributed system, inter-computer communication is only allowed between the Master and the Workers. Therefore, the communication cost among different Workers is often expensive (Duchi et al., 2014; Fan et al., 2017; Jordan et al., 2018). The second problem which needs consideration is the storage limitation. For example, the popular distributed system Apache Spark uses resilient distributed dataset (RDD) as its foundation, which requires data and intermediate results to be cached in memory during computation (Zaharia et al., 2010, 2012; Gu and Li, 2013). This feature enables Spark to speed up the computational time, but have to pay for the high memory cost of RDDs (Gu and Li, 2013; Chand et al., 2017). Therefore, how to improve the memory usage in distributed computing is also a problem of interest.

Except for the communication cost and memory usage, another important issue is the distribution of data on a distributed system. In an ideal situation, the massive data should be randomly distributed on different Workers (Zhang et al., 2012). Consequently, any statistics computed from a single Worker should be a consistent estimate for its global counterpart. However, this is seldom the case in practice. Actually, practitioners usually store a huge dataset in a way convenient for operation. For example, the data might be distributed on different Workers by location or time. As a consequence, the observed distribution of data is different across Workers, and thus the resulting statistics calculated on different Workers could be seriously biased for its global counterpart. If this is the case, the final estimate, summarizing from those computed on different Workers, would be questionable.

In this work, we target on the estimation problem of generalized linear models (GLM) on a distributed system, and try to achieve the following goals: reduce the communication cost, increase the memory efficiency, and consider the nonrandomly distributed nature of data. The generalized linear model is a broad class of models that generalize the linear regression to allow for various types of response and have wide applications (McCullagh and Nelder, 1989a; Dobson and Barnett, 2008; Fahrmeir and Tutz, 2013). To estimate GLM on a distributed system, the commonly used Newton-Raphson algorithm cannot be applied directly, due to the communication and memory cost in multiple iterations.

To address this problem, researchers have developed a number of effective solutions. One popular method is the so-called one-shot estimate (or mixture average, Mcdonald et al. 2009; Zinkevich et al. 2010; Zhang et al. 2012). The idea of this method is to conduct the estimation of GLM on each Worker to obtain a local estimate, and the final global estimate computed by the Master is a simple average of the local ones. It is communication-efficient, but may lead to inconsistent global estimate when the data is nonrandomly distributed in different Workers. In addition, it could not obtain the best statistical estimation efficiency in many cases (Shamir et al., 2014; Jordan et al., 2018). To improve the estimation efficiency, iterative algorithms, which need multiple rounds of communications, have been proposed (Boyd et al., 2011; Shamir et al., 2014; Wang et al., 2017; Jordan et al., 2018).

All these methods have been proven practically useful, but under one critical assumption, i.e., the data is randomly distributed on different Workers. However, as we mentioned before, this is seldom the case in practice. In fact, practitioners often find the local estimates received from different Workers are quite different from each other. This can be viewed as a strong evidence that the data distributed on different Workers might be quite different. As a consequence, the local estimates may not be consistent, thus leads to questionable global estimate in one-shot method. Then, how to obtain an efficient estimate for GLM on a distributed system with nonrandomly distributed data becomes a problem of interest.

To address this issue, we develop here a Pseudo-Newton-Raphson algorithm for an efficient estimation of generalized linear models on a distributed system with nonrandomly distributed data. Specifically, in the first step, we collect a random sample of small size from different Workers in the distributed system. The MLE is calculated as a pilot estimate based on this sample, which is -consistent and requires small memory usage. In the second step, we broadcast the pilot estimate to each Worker, and then calculate the first and second order derivatives of the log-likelihood function in each Worker at the point . Then, the computed derivatives in each Worker is received by the Master with little communication cost, since they are finite dimensional vectors or matrices. Finally, the Master combines the received derivatives to compute a global estimate, and conducts one-step updating (e.g., the Newton-Raphson type) with as the initial estimate. This leads to the final estimate .

It is noteworthy that, the above updating method only requires two rounds of Master-and-Worker communication, and the transferred data are all of small sizes. Therefore, this method is computationally efficient, in terms of both communication cost and storage usage. In addition, we prove that the final estimate shares the same asymptotic covariance as the global MLE as long as , which suggests it is also statistically efficient. Based on the final estimate, we also develop a likelihood ratio test for hypothesis testing on a distributed system with nonrandomly distributed data.

The rest of this paper is organized as follows. Section 2 introduces the efficient estimation for GLM and the corresponding likelihood ratio test. Section 3 presents a number of simulation studies to demonstrate the finite sample performances of our proposed estimator and the likelihood ratio test. Section 4 illustrates the application of our method using the Airline dataset (http://stat-computing.org/dataexpo/2009/). Section 5 concludes the paper with a brief discussion.

2. Efficient Estimation for Generalized Linear Models

2.1. Maximum Likelihood Estimation

Consider a sample with observations. For each observation , we collect a response and a -dimensional covariate vector . We assume that s are independent and identically distributed. Suppose that the sample size is large and the data are stored on a distributed system with local Workers. Define , and further define to be the set of sample indices stored on the -th Worker with . Then we have for , , and .

We define the generalized linear models according to the previous literature (Nelder and Wedderburn, 1972; Wedderburn, 1974; McCullagh, 2019). Define the expectation of to be . And is referred to as the canonical parameter, which is some function of . We assume that the distribution of is in an exponential family, whose log-likelihood could be spelled out as,

where is a nuisance parameter, and and are some specific functions. Define to be the linear predictor based on the covariate vector, where is a -dimensional unknown parameter. If we define , then a canonical link relates the linear predictor to the expected value . For example, for logistic regression, the canonical link could be ; for poisson regression, the canonical link is .

The unknown parameter is often estimated by the maximum likelihood estimator (MLE), which is denoted as . It could be obtained by maximizing the log-likelihood function , namely,

where some constants are ignored. Since there is no general closed-form solution to MLE, it could be obtained by Newton’s method.

Remark 1. Specifically, define is a function which satisfies , so that is the variance of when the scale factor is unity. For the sake of notation simplification, we assume that throughout the article. The results could be similarly generalized for the cases where .

Next we consider the theoretical properties of the estimator . Under certain conditions, it has been shown that is -consistent and asymptotically normal (McCullagh and Nelder, 1989b). We further define , which is a positive definite matrix, then we have,

| (2.1) |

where is a zero vector, and is the true parameter. See Nelder and Wedderburn (1972); Wedderburn (1974); McCullagh (2019) for more technical details.

2.2. One-Step Estimation

The one-step estimation consists of two steps. In the first step, a sample of small size is randomly selected from different Workers as a pilot sample. It is assumed that is much smaller than , which is but as . Specifically, let be the indices selected from in the -th Worker by simple random sampling without replacement, and . Thus the pilot sample could be denoted as . Since the pilot sample size is much smaller than , the communication cost in transferring the pilot sample from different Workers to the Master is practically acceptable. Then a pilot estimator could be obtained on the Master based on the pilot sample, which is denoted as,

| (2.2) |

where is the log-likelihood function based on the pilot sample. It is remarkable that is a function of . Specifically, the pilot sample is obtained in a completely random manner. Thus is consistent regardless of how the data are distributed on different Workers. However, is statistically inefficient because it is -consistent.

Recall that is obtained based on the whole sample. It could be expressed that,

| (2.3) |

where , . See Appendix A for more details. Then, to further improve the efficiency of the estimator, we replace in (2.3) with to obtain , i.e., . This leads to the one-step estimator as , which is

| (2.4) |

This one-step estimator is in the similar spirit as classical one-step estimator (Shao, 2003; Zou and Li, 2008). However, the key difference is that the pilot estimator in our one-step estimator is -consistent. As a consequence, the asymptotic properties of the final estimator are more difficult to be studied than the traditional one-step estimator. Moreover, we are able to prove that the one-step estimator has the same asymptotic covariance as the MLE under certain conditions.

To establish the statistical properties of the one-step estimator, the following conditions are needed.

-

(C1)

The pilot sample size satisfies that and .

-

(C2)

Assume , and to be a positive definite matrix.

-

(C3)

Assume there exists a function , such that for any , , where is a constant. And assume that in the neighbourhood of the true parameter , we have for ,

Condition (C1) considers the relationship between and . It is assumed that is . Condition (C2) and (C3) are typical assumptions of the MLE method for GLM. With the condition satisfied, we have the following theorem.

Theorem 1.

Assume the conditions (C1)–(C3) hold, then we have

See Appendix B for detailed proof of Theorem 1. From the theorem, we could conclude that has the same asymptotic properties as . Precisely, the difference between and is . However, the computational cost of obtaining global MLE is much higher than that of the one-step estimator, since the former needs multiple iterations, which will lead to inevitable higher communication cost.

2.3. Likelihood Ratio Test

In this section, we consider the hypothesis testing on a distributed system with nonrandomly distributed data. The likelihood ratio test is one of the useful tools in hypothesis testing. Traditionally, suppose we would like to test the null hypothesis,

Under the null hypothesis, we could obtain the maximum likelihood estimator for . Thus, the likelihood ratio could be defined as,

| (2.5) |

where is the likelihood function for . Then it could be proved that asymptotically follows a distribution (Van der Vaart, 2000; McCullagh, 2019).

However, as we have mentioned above, the maximum likelihood estimator is hard to obtain for massive data on a distributed system. Thus under the null hypothesis, we consider to use the one-step estimator as an approximate. As a results, a new test statistic based on one-step estimation could be constructed as,

| (2.6) |

It is remarkable that, although the forms of (2.5) and (2.6) are almost the same, the difference of used estimators will lead to totally different computational cost. Furthermore, we have the following theorem.

Theorem 2.

Under conditions (C1)–(C3), asymptotically follows a distribution.

See Appendix C for detailed proof of Theorem 2. By the theorem, we could see that has the same asymptotic distribution as . In the next section, we will illustrate both the performance of and .

Remark. If we would like to test part of the parameters of , the test statistics by one-step method could be similarly established. For example, we assume is a subvector of with . We assume that and could be written as . The null hypothesis is H and the alternative one is H. Under the alternative hypothesis, we could estimate by its one-step estimator . Then define . Thus the test statistics could be constructed as It could be proved that asymptotically follows a distribution.

3. Simulation Studies

In this section, we would first investigate the finite sample performance of the proposed one-step estimator in Section 3.1 to 3.3. Then, we study the performance of the likelihood ratio test using one-step estimator in Section 3.4.

3.1. Simulation Design

To demonstrate the finite sample performance of the one-step estimator, we present a variety of simulation studies. Assume the whole dataset contain observations, and be stored in Workers. Here, different sample sizes and number of Workers would be considered, i.e., and . We then generate each observation and () under certain generalized linear regression models. For illustration purpose, we take two classical models as examples, i.e., the logistic regression and poisson regression. The specific settings for these two examples are given as follows.

Example 1. (Logistic Regression) The logistic regression deals with analytical tasks with binary responses. In this example, we consider exogenous covariates . Each covariate is generated from a standard norm distribution . The corresponding coefficients for are set to be . We then generate the response from a Bernoulli distribution with the probability given as,

Example 2. (Poisson Regression) The poisson regression is used to model count responses. We also consider exogenous covariates in this example, each of which is generated from a uniform distribution . The corresponding coefficients . Then, the response is generated from a Poisson distribution given as

To verify the performance of the one-step estimator, we consider two settings of storing strategies in each example.

Case 1. (Randomly Distributed) In this case, the data are randomly distributed across the Workers.

Case 2. (Nonandomly Distributed) To make the whole dataset nonrandomly distributed across the Workers, we conduct the following process. Define as the summation of covariates. Given , define as the th order statistics, i.e, . Then, we store the -th observation in the -th Worker, where . By this way, the storing place of each observation is related to its covariates, and thus the whole dataset is distributed nonrandomly.

With the pairwise combinations of different examples and cases, we have four simulation scenarios in total. They are, respectively, Logistic Random, Logistic Nonrandom, Poisson Random, and Poisson Nonrandom. In each scenario, we repeat the experiment for times.

3.2. Performance Measurement

For a reliable evaluation, we take different measures for comparison. For the randomly distributed case, we compare our proposed one-step estimator with: (a) the global (GO) estimator based on the whole sample, (b) the one-shot (OS) estimator, and (c) the communication-efficient surrogate likelihood (CSL) estimator (Jordan et al., 2018). In the meanwhile, we also report the results for the pilot estimator. For the nonrandomly distributed case, we omit the CSL estimator, since its inference algorithm does not work well with nonrandomly distributed data. In addition, given the pilot sample size would definitely influence the performance of the one-step estimator, we consider different sizes of the pilot sample. Specifically, define as the pilot percentage and we take for illustration.

For one particular method (i.e., GO, OS, CSL, Pilot, and One-Step), we define as the estimator in the -th replication. Then, to evaluate the estimation efficiency of each estimator, we define the root mean squared error (RMSE) for , i.e., . Finally, we compute the averaged RMSE of all covariates as the final performance measure, i.e., .

3.3. Simulation Results

Table 1 presents the simulation results for estimation performance under the logistic regression for randomly, and nonrandomly distributed cases, respectively. The corresponding results under the poisson regression have similar patterns, which are shown in Table 2. From the simulation results in randomly distributed cases, we can draw the following conclusions. First, when data are randomly distributed, both the one-shot estimator and CSL estimator can achieve similar estimation performance with the global one. Also, these three estimators are -consistent, in the sense that the ARMSE values are close to zero as . Second, the ARMSE values of both pilot estimator and one-step estimator decrease as the pilot percentage or sample size increase. This finding verifies that the pilot estimator and one-step estimator are -consistent, in accordance with Theorem 1. Third, although the pilot estimator does not work well when compared with the global one, the one-step estimator performs much better. It can achieve similar ARMSE with the global estimator under a small pilot percentage when is large. In fact, Theorem 1 shows that when , the one-step estimator is statistically efficient as the global one. Last, in the randomly distributed case, the estimation performance of different estimators are not related with the number of Workers.

Then, we focus on the simulation results in nonrandomly distributed cases shown in Table 1 and Table 2. It is notable that, when data are nonrandomly distributed across different Workers, the story of one-shot estimator has totally changed. Specifically, the ARMSE of one-shot estimator is much larger than the global one. In addition, when the number of Workers increases, the data distributed on each Worker become more heterogenous, and the resulted one-shot estimator performs worse. On the contrary, the estimation performance of one-step estimator is similarly with that in the randomly distributed case. This suggests that the statistical efficiency of one-step estimator remains comparable with that of the global one.

3.4. Simulation for Likelihood Ratio Tests

In this subsection, we demonstrate the finite sample performance of likelihood ratio test using one-step estimator. Assume the whole dataset contain observations, which are stored in Workers. The examples of logistic regression and poisson regression are both considered, for randomly distributed and nonrandomly distributed cases. For illustration purpose, we only consider two covariates , where and is independently and identically generated from a uniform distribution . The corresponding coefficients for are and . In the logistic regression, we set , and the null hypothesis is versus the alternative one . In the poisson regression, we set and also test whether equals zero or not.

For each hypothesis testing problem, we conduct a variety of likelihood ratio tests using: (a) the global estimator, (b) the one-shot estimator, (c) the pilot estimator, and (d) the one-step estimator. For GO, Pilot and One-Step estimators, we first obtain and under and , respectively. Then the likelihood ratio test is applied. Under Theorem 2, the test statistics follows a distribution. For the one-shot estimator, we first use observations stored on the -th Worker to obtain and under and , respectively. Then, we summarize the information from all Workers and calculate the test statistic as . It can be easily derived that follows a distribution.

To evaluate the testing performance, we set the significance level . Define as the test statistics ( GO, OS, Pilot, One-Step) in the -th replication for , where is the number of replications. Then, define an indicator measure for using global, pilot and one-step estimators, and for using one-shot estimator. For a total of replications, we can calculate the empirical rejection probability as . Therefore, the ERP is the empirical size under the null hypothesis , while it is the empirical power under the alternative hypothesis . The empirical size and power provide overall measures for assessing the performance of the likelihood ratio test.

Simulation results for likelihood ratio tests under the logistic regression and poisson regression are shown in Table 3 and Table 4, respectively. We find that, all likelihood ratio tests control the size very well, which are around the nominal level 5%. However, they perform differently in empirical power. Specifically, the likelihood ratio tests using global estimator and one-step estimator result in similar empirical power, which are the best of all. The bad performance for likelihood ratio test using pilot estimator is mainly due to its smaller sample size . As for the OS method, it has obtained lower empirical power than tests using global estimator and one-step estimator. The performance of OS method is even worse than the pilot estimator when data are nonrandomly distributed among Workers. Finally, we find the pilot percentage does not affect the empirical size and power much for test using one-step estimator. This finding implies that a small pilot percentage is enough in practice for conducting likelihood ratio test using one-step estimator.

4. Real Data Analysis

For illustration purpose, we elaborate the application of our proposed method on an American Airline dataset. This is a public dataset, which can be downloaded from http://stat-computing.org/dataexpo/2009/. It contains flight arrival and departure information for all commercial flights from 1987 to 2007 in America. There are a total of nearly 120 million records and take up 12GB on a hard drive. Each record contains information such as the delayed status, the actual and scheduled departure or arrival time, the flying distance, and so on. We place this dataset on a Spark-on-YARN cluster, which is set up on Aliyun Cloud Server, a industrial-level service for distributed systems (https://www.aliyun.com/product/emapreduce). The Spark system consists of one Master and seven Workers. For convenience, all records in every three years are stored in one Worker.

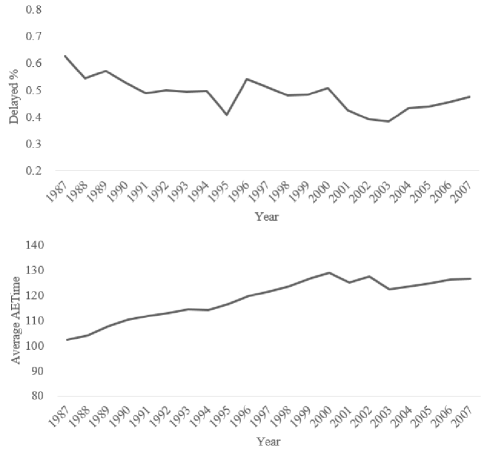

The research goal of this dataset is to investigate factors that can influence the delayed status of flight. To this end, we take “Delayed”, indicating whether the flight is delayed or not, as the response, and consider four continuous variables as covariates for illustration purpose. The detailed information of each variable is shown in Table 5. To investigate the nonrandomly distributed nature of this dataset, Figure 1 presents the delayed percentages of flights and the average of actual elapsed time in each year from 1987 to 2007. It is obvious that, the two variables behave differently in different years. The delayed percentages of flights in most years vary between 0.4 to 0.6. We can also observe a decreasing trend in the delayed percentages. On the contrary, the averages of actual elapsed time are rising continuously. These findings imply the data stored by every three years have the nonrandomly distributed issue.

To address this issue, we establish a logistic regression and use the proposed one-step method for estimation. The pilot percentage is set as 0.001. For comparison purpose, we also obtain the global estimator and the one-shot estimator based on the whole dataset. The likelihood ratio tests are then applied to investigate the significance for each estimator. Finally, we compute the log-likelihood of each method to evaluate the model performance.

Table 6 presents the detailed regression results under the global method, one-shot method and one-step method. It is notable that, in different methods, the p.values of all covariates are smaller than 0.001, suggesting their significant influences to the response. In general, the one-step estimates are more similar with the global ones, especially for the covariates “ActualElapsedTime” and “Distance”. As for the model fitting performance evaluated by log-likelihood, the global method has achieved the highest log-likelihood, indicating its best performance of all. It is followed by the one-step method, which is lower than the global method, but much higher than the one-shot method. All these findings verify the better performance of one-step method in handling nonrandomly distributed data.

5. CONCLUDING REMARKS

In this work, we develop a Pseudo-Newton-Raphson algorithm for an efficient estimation of GLM on a distributed system with nonrandomly distributed data. By only using two rounds of Master-and-Worker communication, this algorithm is computationally efficient in both communication cost and storage usage. The final one-step estimator is also proved as statistically efficient as the global estimator under some technical conditions. Based on the one-step estimator, a likelihood ratio test for hypothesis testing is also developed. The performances of the estimator and the corresponding likelihood ratio test are elaborated by both simulation studies and a real American airline dataset.

To conclude this work, we consider some directions for future study. First, the covariates in large-scale datasets are typically of high dimensionality. Then how to conduct feature selection based on the Pseudo-Newton-Raphson algorithm is worth of consideration. Second, in the first step, we have to collect a sample of size from Workers to the Master. To further reduce the communication cost in transferring data, some sufficient statistics are worth of investigation. Last, the proposed one-step method can be further extended to solve model estimation problems using Newton-Raphson algorithms.

Appendices

Appendix A. Basic Matrices and The Estimation Procedure

Define and to be the first and second order derivatives of respectively. By Theorem 2 in Wedderburn (1974), we have . Furthermore, it could be proved that,

where the denotes the expectation given the covariates . It could be calculated that,

Thus it could be verified that,

| (A.1) |

By Taylor expansion, . We replace with in (A.1) and obtain (2.3).

Appendix B. Proof of Theorem 1

To prove the theorem, it is sufficient to show that . Based on (2.3) and (2.4), it could be verified that, , where

First, we consider . Define is the th element of , which is the first order derivative of with respect to . It is remarkable that . Then we conduct Taylor expansion on with respect to at point and one could obtained, , where, is the th element of . It could be verified that , where

By central limit theorem, is . Thus . Since , thus it could be verified that .

Second, we prove that is . Furthermore, we define and . Since the dimension of the matrix is fixed to be , it is sufficient to show that each of its element to be . Consider . It could be verified that and . Thus it is sufficient to show that each element of is . Define . Thus we have, . As a result, by Law of Large Numbers, it could be concluded that . Thus, we have . Then, by Central Limit Theorem, . Thus . And . This completes the proof of the theorem.

Appendix C. Proof of Theorem 2

In this section, we prove Theorem 2 in a more general case. Assume that we would like to test the null hypothesis H versus the alternative one H. Thus we could obtain the MLEs under both the null hypothesis and the alternative one, which are defined as and respectively. Let , where is the MLE of under the alternative hypothesis. Furthermore, we define Similarly we could define We are going to prove that asymptotically follows a distribution, where is the degree of freedom. It is remarkable that Theorem 2 is a special case of this conclusion.

We only need to prove that . It could be expressed that, , and . Thus we only need to prove that,

| (A.2) | |||||

| (A.3) |

By the proof of Theorem 1, we have . Similarly, it could be verified that . Since the proof of (A.2) and (A.2), we only prove (A.2). By Taylor expansion, we have

where is between and . Since , we have . Define . Thus,

where . Since , and . Thus . Since , we have . As a result, . Together with , we have . This completes the proof.

References

- Andrews (2000) Andrews, G. R. (2000), Foundations of multithreaded, parallel, and distributed programming, vol. 11, Addison-Wesley Reading.

- Battey et al. (2015) Battey, H., Fan, J., Liu, H., Lu, J., and Zhu, Z. (2015), “Distributed estimation and inference with statistical guarantees,” arXiv preprint arXiv:1509.05457.

- Boyd et al. (2011) Boyd, S., Parikh, N., Chu, E., Peleato, B., Eckstein, J., et al. (2011), “Distributed optimization and statistical learning via the alternating direction method of multipliers,” Foundations and Trends® in Machine learning, 3, 1–122.

- Chand et al. (2017) Chand, M., Shakya, C., Saggu, G. S., Saha, D., Shreshtha, I. K., and Saxena, A. (2017), “Analysis of big data using apache spark,” in 4th International conference on computing for sustainable global development. BVICAM.

- Dobson and Barnett (2008) Dobson, A. J. and Barnett, A. G. (2008), An introduction to generalized linear models, Chapman and Hall/CRC.

- Duchi et al. (2014) Duchi, J. C., Jordan, M. I., Wainwright, M. J., and Zhang, Y. (2014), “Optimality guarantees for distributed statistical estimation,” arXiv preprint arXiv:1405.0782.

- Fahrmeir and Tutz (2013) Fahrmeir, L. and Tutz, G. (2013), Multivariate statistical modelling based on generalized linear models, Springer Science & Business Media.

- Fan et al. (2017) Fan, J., Wang, D., Wang, K., and Zhu, Z. (2017), “Distributed estimation of principal eigenspaces,” arXiv preprint arXiv:1702.06488.

- Gopal and Yang (2013) Gopal, S. and Yang, Y. (2013), “Distributed training of large-scale logistic models,” in International Conference on Machine Learning, pp. 289–297.

- Gu and Li (2013) Gu, L. and Li, H. (2013), “Memory or time: Performance evaluation for iterative operation on hadoop and spark,” in 2013 IEEE 10th International Conference on High Performance Computing and Communications & 2013 IEEE International Conference on Embedded and Ubiquitous Computing, IEEE, pp. 721–727.

- Jordan et al. (2018) Jordan, M. I., Lee, J. D., and Yang, Y. (2018), “Communication-efficient distributed statistical inference,” Journal of the American Statistical Association, 1–14.

- McCullagh (2019) McCullagh, P. (2019), Generalized linear models, Routledge.

- McCullagh and Nelder (1989a) McCullagh, P. and Nelder, J. A. (1989a), Generalized linear models, London: Chapman & Hall.

- McCullagh and Nelder (1989b) — (1989b), Generalized Linear Models, no. 37 in Monograph on Statistics and Applied Probability, Chapman & Hall,.

- Mcdonald et al. (2009) Mcdonald, R., Mohri, M., Silberman, N., Walker, D., and Mann, G. S. (2009), “Efficient large-scale distributed training of conditional maximum entropy models,” in Advances in Neural Information Processing Systems, pp. 1231–1239.

- Nelder and Wedderburn (1972) Nelder, J. A. and Wedderburn, R. W. (1972), “Generalized linear models,” Journal of the Royal Statistical Society: Series A (General), 135(3), 370–384.

- Shamir et al. (2014) Shamir, O., Srebro, N., and Zhang, T. (2014), “Communication-efficient distributed optimization using an approximate newton-type method,” in International conference on machine learning.

- Shao (2003) Shao, J. (2003), Mathematical Statistics, Springer Texts in Statistics. Springer New York.

- Van der Vaart (2000) Van der Vaart, A. W. (2000), Asymptotic statistics, Cambridge university press.

- Wang et al. (2017) Wang, J., Kolar, M., Srebro, N., and Zhang, T. (2017), “Efficient distributed learning with sparsity,” in Proceedings of the 34th International Conference on Machine Learning-Volume 70, JMLR. org, pp. 3636–3645.

- Wedderburn (1974) Wedderburn, R. W. (1974), “Quasi-likelihood functions, generalized linear models, and the Gauss Newton method,” Biometrika, 61(3), 439–447.

- Zaharia et al. (2012) Zaharia, M., Chowdhury, M., Das, T., Dave, A., Ma, J., McCauley, M., Franklin, M. J., Shenker, S., and Stoica, I. (2012), “Resilient distributed datasets: A fault-tolerant abstraction for in-memory cluster computing,” in Proceedings of the 9th USENIX conference on Networked Systems Design and Implementation, USENIX Association, pp. 2–2.

- Zaharia et al. (2010) Zaharia, M., Chowdhury, M., Franklin, M. J., Shenker, S., and Stoica, I. (2010), “Spark: Cluster computing with working sets.” HotCloud, 10, 95.

- Zhang et al. (2012) Zhang, Y., Wainwright, M. J., and Duchi, J. C. (2012), “Communication-efficient algorithms for statistical optimization,” in Advances in Neural Information Processing Systems, pp. 1502–1510.

- Zinkevich et al. (2010) Zinkevich, M., Weimer, M., Li, L., and Smola, A. J. (2010), “Parallelized stochastic gradient descent,” in Advances in neural information processing systems, pp. 2595–2603.

- Zou and Li (2008) Zou, H. and Li, R. (2008), “One-step sparse estimates in nonconcave penalized likelihood models,” Annals of Statistics, 36(4), 1509 C1533.

[b] Random Nonrandom GO OS CSL Pilot One-Step GO OS Pilot One-Step 2 5 0.034 0.034 0.034 0.147 0.049 0.034 0.049 0.156 0.050 10 0.112 0.039 0.108 0.037 20 0.078 0.033 0.075 0.034 5 5 0.035 0.036 0.035 0.167 0.061 0.035 0.184 0.159 0.053 10 0.112 0.039 0.107 0.038 20 0.078 0.035 0.077 0.034 10 5 0.035 0.038 0.035 0.161 0.053 0.034 6.096 0.16 0.065 10 0.107 0.039 0.105 0.038 20 0.076 0.034 0.081 0.034 2 5 0.024 0.024 0.024 0.111 0.031 0.025 0.034 0.112 0.030 10 0.079 0.024 0.078 0.025 20 0.055 0.024 0.055 0.025 5 5 0.024 0.025 0.024 0.107 0.031 0.025 0.118 0.11 0.029 10 0.076 0.026 0.075 0.025 20 0.055 0.024 0.054 0.024 10 5 0.025 0.026 0.025 0.107 0.030 0.024 0.777 0.112 0.032 10 0.080 0.025 0.078 0.026 20 0.053 0.025 0.049 0.024 2 5 0.011 0.011 0.011 0.050 0.011 0.010 0.015 0.048 0.011 10 0.034 0.011 0.033 0.011 20 0.023 0.011 0.024 0.010 5 5 0.011 0.011 0.011 0.048 0.011 0.011 0.052 0.049 0.012 10 0.034 0.011 0.033 0.011 20 0.022 0.011 0.024 0.011 10 5 0.011 0.011 0.011 0.049 0.011 0.011 0.133 0.05 0.011 10 0.032 0.011 0.035 0.011 20 0.025 0.011 0.024 0.010

[b] Random Nonrandom GO OS CSL Pilot One-Step GO OS Pilot One-Step 2 5 0.037 0.037 0.037 0.175 0.038 0.035 0.049 0.166 0.037 10 0.121 0.037 0.115 0.036 20 0.084 0.037 0.085 0.036 5 5 0.037 0.037 0.037 0.165 0.038 0.035 0.127 0.169 0.037 10 0.112 0.038 0.115 0.036 20 0.083 0.037 0.082 0.035 10 5 0.037 0.037 0.037 0.167 0.038 0.035 0.266 0.159 0.037 10 0.116 0.037 0.117 0.036 20 0.084 0.037 0.083 0.035 2 5 0.026 0.026 0.026 0.128 0.027 0.026 0.038 0.118 0.027 10 0.083 0.026 0.080 0.026 20 0.063 0.026 0.058 0.026 5 5 0.026 0.026 0.026 0.117 0.027 0.026 0.084 0.117 0.027 10 0.083 0.026 0.084 0.026 20 0.058 0.026 0.057 0.026 10 5 0.026 0.026 0.026 0.118 0.027 0.026 0.19 0.119 0.027 10 0.081 0.026 0.088 0.026 20 0.059 0.026 0.060 0.026 2 5 0.012 0.012 0.012 0.053 0.012 0.011 0.016 0.052 0.011 10 0.037 0.012 0.038 0.011 20 0.027 0.012 0.027 0.011 5 5 0.012 0.012 0.012 0.050 0.012 0.011 0.039 0.051 0.011 10 0.037 0.012 0.034 0.011 20 0.026 0.012 0.027 0.011 10 5 0.012 0.012 0.012 0.052 0.012 0.011 0.073 0.053 0.011 10 0.036 0.012 0.037 0.011 20 0.025 0.012 0.025 0.011

[b] Storing Strategy Size Power GO OS pilot% Pilot One-step GO OS pilot% Pilot One-step Random 10,000 0.052 0.054 5 0.050 0.052 0.408 0.226 5 0.050 0.408 10 0.046 0.052 10 0.084 0.408 20 0.052 0.052 20 0.104 0.408 20,000 0.048 0.046 5 0.040 0.048 0.704 0.422 5 0.094 0.702 10 0.060 0.048 10 0.116 0.702 20 0.044 0.048 20 0.208 0.704 50,000 0.051 0.05 5 0.046 0.051 0.950 0.846 5 0.134 0.950 10 0.054 0.051 10 0.236 0.950 20 0.054 0.051 20 0.410 0.950 Nonrandom 10,000 0.051 0.054 5 0.040 0.051 0.388 0.056 5 0.080 0.386 10 0.056 0.051 10 0.084 0.388 20 0.054 0.051 20 0.134 0.388 20,000 0.048 0.052 5 0.052 0.048 0.690 0.062 5 0.060 0.690 10 0.052 0.048 10 0.094 0.690 20 0.048 0.048 20 0.184 0.690 50,000 0.052 0.048 5 0.056 0.052 0.966 0.072 5 0.118 0.966 10 0.056 0.052 10 0.252 0.966 20 0.054 0.052 20 0.388 0.966

[b] Storing Strategy Size Power GO OS pilot% Pilot One-step GO OS pilot% Pilot One-step Random 10000 0.054 0.056 5 0.042 0.054 0.454 0.280 5 0.070 0.452 10 0.052 0.054 10 0.100 0.454 20 0.042 0.054 20 0.126 0.454 20000 0.052 0.054 5 0.054 0.052 0.786 0.504 5 0.108 0.784 10 0.052 0.052 10 0.154 0.786 20 0.048 0.052 20 0.220 0.786 50000 0.048 0.046 5 0.046 0.048 0.984 0.886 5 0.138 0.984 10 0.048 0.048 10 0.286 0.984 20 0.052 0.048 20 0.476 0.984 Nonrandom 10000 0.054 0.056 5 0.046 0.054 0.478 0.050 5 0.076 0.470 10 0.055 0.054 10 0.082 0.478 20 0.055 0.054 20 0.142 0.478 20000 0.052 0.052 5 0.052 0.052 0.774 0.062 5 0.086 0.770 10 0.054 0.052 10 0.110 0.774 20 0.048 0.052 20 0.206 0.774 50000 0.049 0.046 5 0.052 0.049 0.982 0.076 5 0.152 0.982 10 0.050 0.049 10 0.266 0.982 20 0.050 0.049 20 0.432 0.982

[b] Variable Description Mean SD Response Delayed Whether the flight is delayed or not, 1 for Yes; 0 for No. Yes: 48.07%; No: 51.93% Covariates DepTime Actual departure time 1349.69 476.92 CRSArrTime Scheduled arrival time 1490.84 493.65 ElapsedTime Actual elapsed time 119.70 68.49 Distance Distance between the origin and destination (in miles) 701.45 551.29

[b] Global One-Shot One-Step Intercept -3.440*** -2.982*** -2.813*** DepTime (100) 0.096*** 0.066*** 0.069*** CRSArrTime (100) -0.028*** -0.018*** -0.019*** ActualElapsedTime 0.058*** 0.066*** 0.059*** Distance (100) -0.683*** -0.782*** -0.699*** Log-likelihood -19083793.2 -19703781.7 -19451071.1

-

1

*** indicates the p.value smaller than 0.001