On eigenvalues of a high-dimensional Kendall’s rank correlation matrix with dependence

Abstract

This paper investigates limiting spectral distribution of a high-dimensional Kendall’s rank correlation matrix. The underlying population is allowed to have general dependence structure. The result no longer follows the generalized Marc̆enko-Pastur law, which is brand new. It’s the first result on rank correlation matrices with dependence. As applications, we study the Kendall’s rank correlation matrix for multivariate normal distributions with a general covariance matrix. From these results, we further gain insights on Kendall’s rank correlation matrix and its connections with the sample covariance/correlation matrix.

keywords:

[class=MSC2020]keywords:

, 111All authors contributed equally to this work and Cheng () is the corresponding author., and

1 Introduction

Covariance and correlation matrices play a vital role in multivariate statistical analysis because they provide the most direct way to characterize the relation between different variables. Many statistical estimation or inference methods involve the covariance or correlation matrix, such as principal component analysis, multivariate analysis of variance, factor analysis, etc. In high-dimensional data analysis, studying the eigenvalues and eigenvectors of such covariance/correlation matrices are fundamental problems.

In random matrix theory, sample covariance matrix has been thoroughly studied in the past decades. For an Hermitian matrix , the Empirical Spectral Distribution (ESD) of is defined as

where are eigenvalues of and is the indicator function. If converges to a deterministic distribution function , then is called the Limiting Spectral Distribution (LSD) of . Marc̆enko and Pastur (1967) first derived the LSD of the sample covariance matrix. Further, Bai and Silverstein (2004) studied the Central Limit Theorem (CLT) for its Linear Spectral Statistics (LSSs) defined as

where is a function on . As we know, many important statistics in multivariate analysis can be expressed through ESD, for example,

and

Generally, LSD describes the first-order limits of these LSSs and CLT then characterizes their second-order asymptotics. The two are the analogs of Law of Large Numbers and Central Limit Theorem in classical probability theory, respectively. As applications, CLT for LSSs provides an important tool for many hypothesis testing problems in multivariate analysis with diverging data dimension, e.g., Bai et al. (2009) derived the distribution of the likelihood ratio test for high-dimensional data. Both LSD and CLT for LSSs study the global law of the empirical eigenvalues. Another fundamental problem is the local law (Knowles and Yin, 2017), e.g., the asymptotic behaviors of the smallest and largest eigenvalues. The well-known Bai-Yin law (Bai and Yin, 1993) derived the limits of the extreme eigenvalues. Johnstone (2001) further established the Tracy-Widom law for the largest eigenvalues, which plays a fundamental role in principal component analysis. For more comprehensive overview on this topic, one is referred to Bai and Silverstein (2010).

In practice, data normalization is a standard procedure and after that, we are actually dealing with the sample correlation matrix (El Karoui, 2009). Parallel to the study of the sample covariance matrix, Jiang (2004) first obtained the LSD of Pearson-type sample correlation matrix and Gao et al. (2017) developed the CLT for its LSSs. Bao, Pan and Zhou (2012) established the Tracy-Widom law for its extreme eigenvalues and Pillai and Yin (2012) extended the result to general cases. However, due to the complex structure of the sample correlation matrix, most results only consider the case that sample data has independent components so that its population covariance matrix is diagonal and then the correlation matrix is identity. From the perspective of applications, the independence assumption is however too strong so that such results have very limited applicability (El Karoui, 2009). On the other hand, for general dependent or correlated data, little work (e.g., El Karoui, 2009; Morales-Jimenez et al., 2021) has been done on the sample correlation matrix. As far as the CLT for LSSs, the existing works include Mestre and Vallet (2017) that considered the case for Gaussian distributions and Zheng et al. (2019) studied the trace moments.

For the sample covariance/correlation matrix, due to the congenital sensitivity of Pearson-type correlation, finite fourth order or even higher order moments of the data distribution are usually required to guarantee the convergence of the limiting distributions. However, most of the results applicable to light-tailed distributions cannot be directly extended to heavy-tailed cases, e.g., Heiny and Yao (2020) explored the spectral behavior of Pearson-type correlations for heavy-tail distributions where the story becomes completely different.

As a remedy for dealing with heavy-tailed data samples, some non-parametric correlation matrix, such as Kendall’s and Spearman’s , have received considerable attention in recent years. Kendall’s and Spearman’s are rank-based and thus there’s no need to impose any moment restrictions on the underlying distribution. What is more, classical theory on non-parametric statistics shows that only partial information will be lost while robustness can be retained if we only use the ranks of the data. In random matrix theory, Bai and Zhou (2008) first derived the LSD of Spearman’s rank correlation matrix, which turns out to be the same as the standard Marc̆enko-Pastur law. For the Kendall’s , Bandeira, Lodhia and Rigollet (2017) proved that its LSD is an affine transformation of the standard Marc̆enko-Pastur law. For the CLT for LSSs, Bao et al. (2015) considered Spearman’s rank correlation matrix and Li, Wang and Li (2021) studied Kendall’s rank correlation matrix. The Tracy-Widom law for the extreme eigenvalues of the two matrices can be found in Bao (2019a) and Bao (2019b), respectively. However, all these asymptotic results are for data sample with independent components, i.e., all components are independent. To the best of our knowledge, there are no available results on such rank correlation matrices when the underlying distribution has general dependent structure. We summarize the developments of the sample covariance matrix, sample correlation matrix, Kendall’s and Spearman’s in Table 1.1.

| Sample covariance | Sample correlation | Kendall’s | Spearman’s | |

| Independent case () | ||||

| LSD | Marc̆enko and Pastur (1967) | Jiang (2004) | Bandeira, Lodhia and Rigollet (2017) | Bai and Zhou (2008) |

| CLT for LSSs | Bai and Silverstein (2004) | Gao et al. (2017) | Li, Wang and Li (2021) | Bao et al. (2015) |

| Tracy-Widom | Johnstone (2001) | Bao, Pan and Zhou (2012) | Bao (2019b) | Bao (2019a) |

| Dependent case (general ) | ||||

| LSD | Marc̆enko and Pastur (1967) | El Karoui (2009) | ||

| CLT for LSSs | Bai and Silverstein (2004) | Mestre and Vallet (2017) | ||

| Tracy-Widom | Féral and Péché (2009) | |||

As can be seen from Table 1.1, the asymptotic behaviors of the eigenvalues of the rank correlation matrices under general dependent structure is still unclear. In this paper, we take the first step to fill this gap and focus on Kendall’s rank correlation matrix with high-dimensional correlated data. Specifically, for data sample , we define the sign vector

where denotes the sign function and the sample Kendall’s rank correlation matrix (Kendall, 1938)

| (1.1) |

Our goal is to study the spectral properties of when have a general dependent structure. This is a problem of its own significant interest in random matrix theory. To study Kendall’s rank correlation matrix with dependence, LSD is the cornerstone for further derivations of CLT for LSSs (Bai and Silverstein, 2004) and local laws including the asymptotic distribution of extreme eigenvalues (Knowles and Yin, 2017). It’s also a key step to solve many high-dimensional statistical problems with heavy-tailed observations. Taking high-dimensional independent test as an example, many test statistics based on covariance/correlation matrices have been proposed to test complete independence among the components of ; see Schott (2005), Bao et al. (2015), Gao et al. (2017), Leung and Drton (2018), Bao (2019b), Li, Wang and Li (2021) etc. In particular, Leung and Drton (2018) and Li, Wang and Li (2021) considered test statistics that based on linear functions of the eigenvalues of Kendall’s , e.g., and . However, the test power is still unclear since the limiting properties of Kendall’s (also Spearman’s ) under general dependent alternatives remain largely unknown.

To answer such questions, in this paper, we take the first step to derive the limiting spectral distribution of under the asymptotic regime where and . One major challenge is the nonlinear dependent structure among the sign-based summands of . Hence, we apply the Hoeffding decomposition to to locate the leading terms. In this way, we obtain the equation which the Stieltjes transform of the limiting spectral distribution of satisfies. It’s a brand new distribution which relies heavily on both the covariance and conditional covariance structure of . As illustration, we study the normal distribution where the Kendall’s rank correlation has a specific relation with the Pearson’s correlation and then we derive explicit LSDs for some cases with common dependent structure. Simulation experiments also lend full support to the accuracy of our theoretical results.

The rest of the paper is organized as follows. Section 2 introduces some preliminary knowledge on Kendall’s rank correlation matrix and Hoeffding decomposition. Section 3 contains our main results on the LSD of Kendall’s rank correlation matrix for correlated data. Section 4 considers the Gaussian distributions and Section 5 collects all the numerical experiments. Proofs of the main results are given in the Appendix.

2 Background on Kendall’s rank correlation matrix

2.1 Kendall’s rank correlation matrix

From the definition of Kendall’s rank correlation matrix (1.1), we can write

which looks similar with the sample covariance matrix. To be specific, the sample covariance matrix of the data sample can be written as an U-statistic of order two, i.e.,

| (2.1) |

Despite this similarity in their forms, the inner structure of the two matrices does not follow the same pattern. The sign function introduces non-linear correlation into the matrix and it is nontrivial to analyze such correlation even for binary random variables. For example, Esscher (1924) spent a lot of efforts to derive the variance of Kendall’s rank correlation for bi-normal distributions. As can be seen from Childs (1967), it is already quite complicated to calculate the integral of sign function over fourth order even for normal distribution. Thus, for high-dimensional Kendall’s rank correlation matrix, it is very challenging to study its asymptotic properties.

One appealing property of Kendall’s rank correlation is that it is monotonically invariant (Weihs, Drton and Meinshausen, 2018).

Proposition 2.1 (Monotonic Invariance).

For any strictly increasing monotonic functions , is invariant for monotonic component transformation

The reason is that Kendall’s rank correlation is rank-based and the monotonic transformation does not change the order statistics. One special case is that for any linear transformation of the data

their corresponding Kendall’s rank correlations remain unchanged. That is, Kendall’s is a correlation matrix which is invariant to the location and scale. More importantly, for any distribution, Kendall’s rank correlation always exists and this fact makes it an important tool to characterize data with heavy tails.

In previous works on Kendall’s rank correlation matrix for high-dimensional data (e.g., Bandeira, Lodhia and Rigollet 2017, Leung and Drton 2018, Bao 2019b, Li, Wang and Li 2021), they assumed that all the components were independent with absolutely continuous density. By the monotonic invariance, we can always transform each component into a standard normal distribution and all components are still independent. Thus, it can be formulated as that are independent and identically distributed (i.i.d.) from a standard multivariate normal distribution , from which we can see that these results are very limited. In this work, we consider more general cases where the data components are allowed to have dependence.

2.2 Hoeffding decomposition

In this part, to deal with the nonlinear dependent structure of high-dimensional Kendall’s rank correlation matrix, we apply Hoeffding decomposition to find out the leading terms. Specifically, denote as the conditional expectation of given ,

| (2.2) |

the Hoeffding decomposition for can be written as,

| (2.3) |

where

Throughout this paper, we assume that are i.i.d. from a population with absolutely continuous density. Then, we have

and the covariance matrices of and exist. Specially, we denote

| (2.4) |

2.3 Preliminary results

With the Hoeffding decomposition of described in (2.3), the Kendall’s rank correlation matrix can be decomposed accordingly,

| (2.5) |

where

and . In particular, is the sample covariance matrix formed by i.i.d. random vectors , see the illustration in (2.1).

Our first result is to show that the error terms and can be controlled so that the dominant contribution in terms of the LSD of is from . As a result, we define the following matrix

| (2.6) |

Throughout the paper, we use and to denote the common spectral norm and Frobenius norm of a matrix, respectively.

Proposition 2.2.

Assume for some universal constant and

then we have

where is the Levy distance between two distributions.

Remark 2.3.

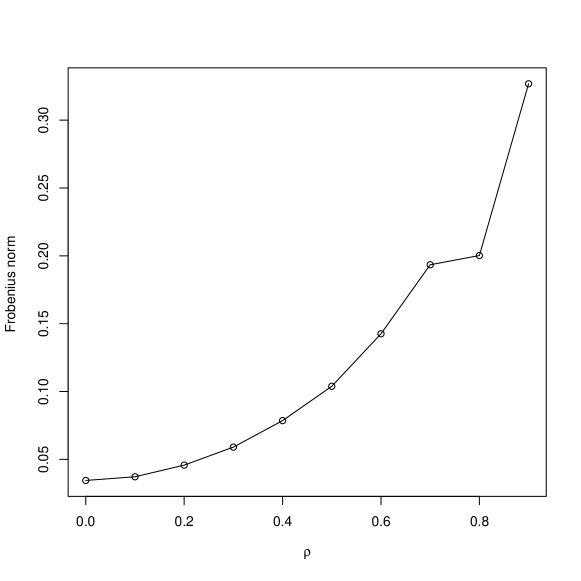

The assumptions on and are to avoid too strong dependence among the components of the data. In random matrix theory, it is a regular condition to assume that the norm of the population covariance matrix is uniformly bounded, e.g., Condition 3 in Bai and Zhou (2008). Here, this condition is also required for bounding the difference between and . To show that such condition is necessary, we conduct a toy example in the following. Specifically, we generate data sample where is a matrix with and . For this case,

which is unbounded for any . Figure 1 presents the distance versus the increasing , and from which we can see that is necessary for bounding the difference between and .

Noting that are i.i.d. random vectors with covariance matrix and

Proposition 2.2 shows that part of Kendall’s rank correlation matrix has similar fluctuations as the usual sample covariance matrix with population covariance matrix and the other part is concentrated on the deterministic matrix . This phenomenon is an analogy of Hoeffding decomposition for the classical U-statistics. By implementing the Hoeffding decomposition for the random vector , we then transfer the study of the LSD of to the study of the LSD of .

3 Limiting spectral distribution of

In this section, we present the LSD of the Kendall’s rank correlation matrix . We first introduce the concept of Stieltjes transform, which is an important tool in random matrix theory. Letting be a finite measure on , its Stieltjes transform is defined as

where denotes the upper complex plane. We can also obtain from by the inversion formula. For any two continuity points of , we have

| (3.1) |

where is the imaginary part of a complex number and is the imaginary unit.

For Kendall’s rank correlation matrix, Bandeira, Lodhia and Rigollet (2017) derived the LSD when the observations are i.i.d. random vectors and the components are also independent with absolutely continuous density. They show that as , , the ESD of such Kendall’s rank converges in probability to an affine transformation of the standard Marenko-Pastur law with parameter , which has an explicit form whose density function is given by

where and . The corresponding Stieltjes transform is the unique solution to the following equation

| (3.2) |

To illustrate the challenges of Kendall’s rank correlation matrix in random matrix theory, we consider the ranking of the data

where each column are the rank of the raw data . For i.i.d. sample , each column of the ranking matrix follows the uniform distribution on the set of all permutations of . While the rows of the raw data matrix are independent, the ranking matrix dose not have independent rows anymore. For the special case where the columns of the raw data are also independent (e.g., Bandeira, Lodhia and Rigollet 2017, Leung and Drton 2018, Bao 2019b, Li, Wang and Li 2021), the columns of the ranking matrix will be independent. Then, the raw data is actually with i.i.d entries which has very limited applications. If the columns of the raw data are dependent, e.g., there is a covariance structure among components, both the rows and the columns of the ranking matrix are dependent. From the perspective of random matrix theory, analyzing such matrices is very challenging.

We first provide a general result as follows and then study the case for Gaussian distribution in the next section.

Theorem 3.1.

For i.i.d. continuous data sample , assume that

-

(A)

as ,

(3.3) where is any deterministic matrix with bounded spectral norm;

-

(B)

for some universal constant , also the solution to the following equation exists

(3.4) -

(C)

such that .

Then, in probability, the empirical spectral distribution converges weakly to a limiting spectral distribution whose Stieltjes transform is given by

| (3.5) |

Recall the dominating matrix in (2.6), which has the same LSD as the following matrix

| (3.6) |

The first part is the type of a sample covariance matrix corresponding to the data sample with population covariance matrix . However, the components within are nonlinearly correlated and thus can not be written in the form of independent components model such that . For those weakly dependent data sample, Bai and Zhou (2008) proved that under certain conditions, the LSD of the sample covariance matrix still follows the generalized Marc̆enko-Pastur law. One of the crucial conditions is that the variance of the quadratic forms is relatively small (see Theorem 1.1 in Bai and Zhou 2008), i.e.,

which is actually the second part of our assumption (A). Under this condition, the LSD of the first part remains the same as the generalized Marc̆enko-Pastur law corresponding to the population covariance matrix .

On the other hand, the LSD of Hermitian matrix of the type has been studied in Silverstein and Bai (1995) where is assumed to be an random matrix with i.i.d. standardized entries, is a diagonal matrix having an LSD, is an Hermitian matrix and the three matrices are independent. Under certain conditions, Silverstein and Bai (1995) proved that the LSD of is a shift of the LSD of . Intuitively, this is because the population version of equals , which shares the same eigenvectors as the matrix . However, in our case, the population version of the first parts in (3.6) equals , whose eigenvectors might be different from the ones of . Therefore, we can not directly apply the results in Silverstein and Bai (1995). Using the terminology of matrix subordination (Kargin, 2015), the limiting Stieltjes transform of is subordinated to the limiting Stieltjes transform of . Roughly, our result is the same as the model . Our Theorem 3.1 shows that both the eigenvalues and eigenvectors of the two matrices, and , will contribute to the LSD of . Thus, it’s a brand new LSD for covariance/correlation matrix.

Technically, the assumption (B) is a new condition and in Appendix, we prove the uniqueness of or if it exists. Here we make some discussions on this condition. If , the equation (3.4) will be

which means that the limiting Stieltjes transform of exists and we solve the above equation to get . The Stieltjes transform of the LSD is then

and then we can get

where the right hand side is exactly the limiting Stieltjes transform of . Thus, our result under the special case is consistent with the one in Bai and Zhou (2008). Now we consider another special case that . From (3.4) and (3.5), we can get

which yields

This result is consistent with the one in Silverstein and Bai (1995) when .

In summary, our new LSD extends the results in Silverstein and Bai (1995) and Bai and Zhou (2008). For general and , it is challenging to study the limits of (3.4). One special case is that and are simultaneously diagonalizable and Toeplitz matrix is such an example, which will be studied in the next section.

4 Gaussian ensemble

As mentioned in the introduction, the Pearson correlation matrix has been thoroughly studied in random matrix theory. Generally, there is no explicit relation between Kendall’s correlation and Pearson correlation; see Kendall (1949) for more details. A special ensemble is Gaussian distribution where Kendall’s correlation has a monotonic correspondence with Pearson correlation. This neat relation is presented in the following lemma which is called Grothendieck’s Identity in mathematical community.

Lemma 4.1 (Grothendieck’s Identity).

Consider a bi-variate normal distribution:

where . We have

Assume where is a correlation matrix, by Lemma 4.1, we can show that

| (4.1) |

Thus, for Gaussian distribution, Kendall’s rank correlation matrix is determined by the Pearson’s correlation matrix .

In this section, we consider the LSD of for Gaussian ensembles from which can shed new light on Kendall’s correlation matrix and also its connections with the sample covariance/correlation matrix.

Proposition 4.2.

Remark 4.3.

It is noted that although we consider the Gaussian ensemble, the results actually cover a wider range of distributions, which is called non-paranormal distribution (Liu, Lafferty and Wasserman, 2009) due to the monotonic invariance of Kendall’s rank correlation matrix. To be specific, a random vector is said to have a non-paranormal distribution if there exist monotone functions such that .

The proof of Proposition 4.2 is to check the assumption (3.3) for Gaussian distribution. Specially, for the normal distribution or non-paranormal distribution, we can calculate the variance of explicitly which is based on the classical results in Esscher (1924) and control the variance of the quadratic form using Poincaré inequality. Hence, Assumption (A) holds for Gaussian distribution and the detailed proof is presented in Appendix. Next, we consider some examples to illustrate the result.

4.1 Independent case

A very special case is the standard multivariate normal distribution, i.e., . By the monotonic invariance of Kendall’s rank correlation matrix, it is equivalent to the independent case considered by Bandeira, Lodhia and Rigollet (2017), Leung and Drton (2018), Bao (2019b), and Li, Wang and Li (2021).

When , we know . Intuitively, the matrix given in (3.6) reduces to a standard sample covariance matrix corresponding to the population covariance matrix and the deterministic matrix . This explains that its LSD is . As an illustration of our main theorems, we demonstrate this result using our Theorem 3.1 and Proposition 4.2 in the following.

4.2 MA(1) model

Next, we consider an MA(1) model with population correlation matrix as follows,

where . The eigenvalues of are given by

and the corresponding eigenvectors are

A detailed calculation of the eigenvalues and eigenvectors can be found in Lemma 1 of Wang, Jin and Miao (2011). It is noted that the eigenvectors of do not depend on the correlation parameter . Thus, and share the same eigenvectors and we can derive the two limits of Theorem 3.1 as follows.

Proposition 4.4.

Assume that . Then the Stieltjes transform of the LSD of satisfies

| (4.2) |

Here and satisfies

| (4.3) |

where

4.3 Toeplitz structure

Last but not least, we consider a more general case that the population correlation matrix has a Toeplitz structure

| (4.4) |

where the correlations are absolutely summable

| (4.5) |

Define the function

whose Fourier series are exactly . Szegö Theorem (Gray, 2006) shows that the eigenvalues of can be approximated by

For the limit in (3.4), which involves two Toeplitz matrices, we can not apply Szegö Theorem directly. However, a Toeplitz matrix can be approximated by a circulant matrix (Gray, 2006, Lemma 11) whose eigenvectors are universal for its entries. By Theorems 11 and 12 of Gray (2006), under some mild conditions, we have the following limit.

Proposition 4.5.

The absolutely summable condition (4.5) and the bound for guarantee the existence of the Fourier functions and . By solving (3.4) using the limit (4.6) in Proposition 4.5, we can theoretically derive the . For the limit (3.5) in Theorem 3.1, Szegö Theorem can yields the result directly. In summary, we can obtain the Stieltjes transform of the LSD of when samples are from the Toeplitz covariance matrix model as follows.

Proposition 4.6.

Assume that where is a Toeplitz matrix (4.4). Then the Stieltjes transform of the LSD of satisfies

where

5 Simulation

In this section, simulation experiments are conducted to examine the finite sample performance of eigenvalues of Kendall’s sample correlation matrix when the data sample follows different dependence structure. We generate sample data , draw the histogram of eigenvalues of the Kendall sample correlation matrix and compare with their theoretical densities. Specifically, we consider four types of covariance matrix :

-

(I)

Independent case: ;

-

(II)

Factor mode: , where , , thus , where ;

-

(III)

MA(1) model: all the diagonal entries of are 1, both upper and lower subdiagonal entries are , others are zero;

-

(IV)

General Toeplitz matrix with for .

Here the population covariance matrix and correlation matrix are the same in Model (I), (III) and (IV).

Model (I):

As for the independent case, we consider three types of sample correlation matrices, Pearson , Spearman and Kendall . Specifically, for our data sample , , both and are

matrices where and are the Spearman and

Pearson correlation of the -th and -th row of with

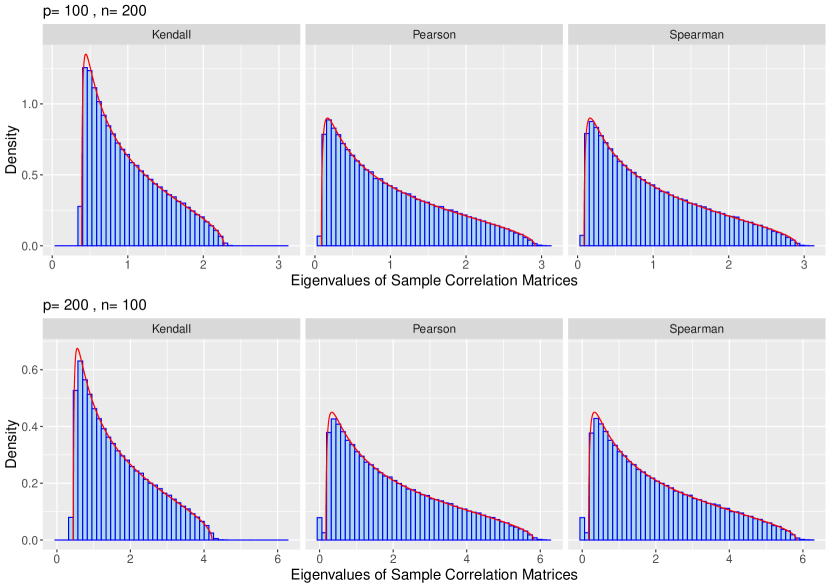

here is the rank of among . From Jiang (2004) and Bai and Zhou (2008), we know that the LSD of and are both standard Marc̆enko-Pastur law while the LSD of is an affine transformation of Marc̆enko-Pastur law (Bandeira, Lodhia and Rigollet, 2017). Thus we list the histogram of eigenvalues of all three types of sample correlation matrices under different combinations of and compare with their corresponding limiting densities in Figure 2. It can be seen from Figure 2 that all the histograms conform to their theoretical limits, which fully supports our theoretical results in the independent case.

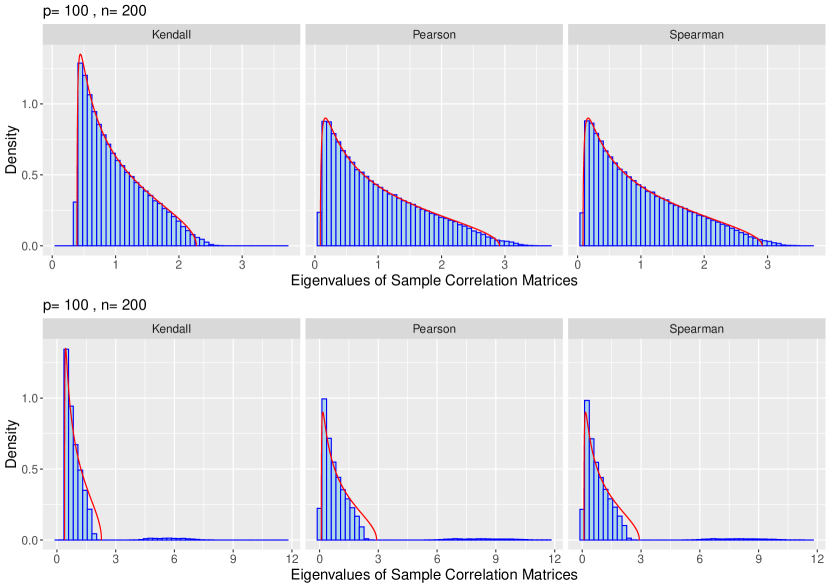

Model (II):

The second case is the factor model or the spiked model, i.e., the population covariance matrix is

where . For the related correlation matrix , we have

where . Noting,

and for any , we have

and

Thus, when

the LSD is still an affine transformation of Marc̆enko-Pastur law (Bandeira, Lodhia and Rigollet, 2017). If the term is large, the result violates the affine transformation of Marc̆enko-Pastur law. To demonstrate these results, we consider two covariance matrices:

where and . Figure 3 shows the results which are consistent with our analysis.

Model (III):

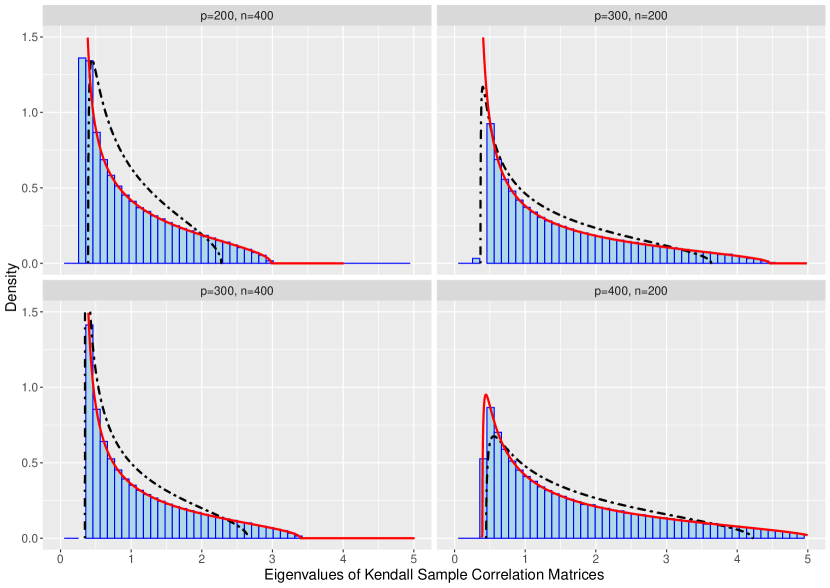

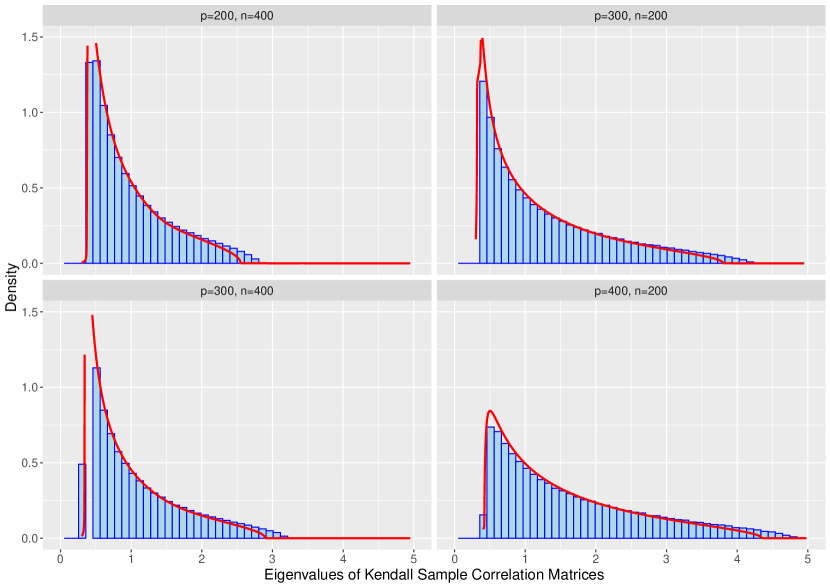

As for MA(1) model, we focus on the spectral behavior of since little is known about and in the dependent case. Similarly, we generate data sample where follows MA(1) model (III) with . The LSD are derived using Proposition 4.4 and the inversion formula (3.1). Then the histogram of eigenvalues of under different combinations of are compared with their corresponding limiting densities in Figure 4. It can be seen from Figure 4 that the LSDs under MA(1) model are different from the independent case. All empirical histograms conform to our theoretical limits, which proves the accuracy of our theory.

Model (IV):

As an illustration for the general Toeplitz matrix, we consider a band Toeplitz matrix with two parameters, i.e.,

Noting

we have

and then

The assumption (3.3) is

and Proposition 4.5 yields

| (5.1) |

where

Solving (5.1) to get , the Stieltjes transform of the LSD (3.5) is

where

Figure 5 shows the results with and again, we can see that the empirical histogram conforms to our theoretical result.

Acknowledgments

We thank the Editor, an Associate Editor, and anonymous reviewers for their insightful comments. Zeng Li’s research is partially supported by National Natural Science Foundation of China (NSFC) (No. 12031005 and No. 12101292). Cheng Wang’s research is supported by NSFC (No. 12031005) and NSF of Shanghai (21ZR1432900). Qinwen Wang’s research is partially supported by the NSFC (No. 12171099).

Appendix

This Appendix contains all supporting lemmas and proofs.

A1 Proof of Proposition 2.2

The following results show that and are concentrated on their population means, respectively.

Lemma A1.1.

Under the assumption of Proposition 2.2,

Lemma A1.2.

Under the assumption of Proposition2.2,

Equipped with these two results, we are now ready to prove Proposition 2.2. By the Corollary A.41 of Bai and Silverstein (2010),

which yields

The proof is completed.

A1.1 Proof of Lemma A1.1

Writing the kernel function

we have

For the kernel function, we have the following properties.

-

•

For the mean parts,

-

•

For the Frobenius norm of the kernel function, we have

Since

and , we have

which yields

-

•

For the the Frobenius norm of the conditional mean, we have

which yields

Putting together the pieces, we conclude that

The proof is completed.

A1.2 Proof of Lemma A1.2

Recalling

we have

For the first term, we have

which yields . For the second term, we have

and

Finally, we have

The proof is completed.

A2 Proof of Theorem 3.1

According to Proposition 2.2, it suffices to study the LSD of the following matrix .

| (A.1) |

Let be the Stieltjes transform of , then the convergence of can be determined in three steps:

A2.1 Almost sure convergence of

Denote

Let be expectation and be conditional expectation given . From the martingale decomposition and the identity

| (A.2) |

we have

Since

forms a bounded martingale difference sequence. Hence for any ,

| (A.3) |

which implies , almost surely.

A2.2 Convergence of

Denote

| (A.4) |

Starting from the identity

then take trace on both sides and by (A.2), we have

| (A.5) | ||||

| (A.6) |

where

We decompose

where

For the term , we have

| (A.7) |

then its contribution to (A2.2) can be bounded as

For the term , we have

| (A.8) |

For the term , we have the first part bounded by

So we have

According to Lemma A3.2 and Lemma A3.3,

which gives

| (A.9) |

Combining (A2.2), (A2.2), (A.8) and (A.9), we have

| (A.10) |

where is the limit of .

A2.3 The uniqueness of the solution

We only have to show that the solution to (3.4), if exists, is unique in . Now suppose we have two solutions to (3.4) for a common , then we can obtain

If , then

where is defined as

By the Cauchy-Schwarz inequality, we have

| (A.12) |

On the other hand, denote the eigen-decomposition of by

Then, we have

which yields

Then taking the imaginary part in (3.4), we have

Since , the above inequality yields that

which leads to a contradiction with (A2.3). This contradiction proves that and hence equation (3.4) has at most one solution in . The proof of this theorem is then complete.

A3 Proof of Proposition 4.2

The proof is checking the assumptions 3.3 for normal distribution which are summarized in Lemmas A3.2 and A3.3. Before proceeding, we need the following variance result for Kendall’s correlation.

Lemma A3.1 (Esscher 1924).

Consider a multivariate normal distribution

where , we have

| (A.1) |

Lemma A3.2.

Assuming , we have

| (A.2) |

Proof of Lemma A3.2.

For the covariance part, we have

and Grothendieck’s Identity shows that for any bi-variate normal vector ,

Thus,

For ,

and

For the enlarged random vector, we have

and thus

Next, we derive the explicit result for . Since

and for any ,

then by Lemma A3.1,

The proof is completed. ∎

Lemma A3.3.

Let where , then for any non-random matrix , we have

Proof of Lemma A3.3.

For , we define a function

Direct calculations can show that

where . When , by Gaussian Poincaré inequality, we have

The proof is completed. ∎

A4 Proof of Proposition 4.4

We consider a more general matrix

whose eigenvalues are

and the corresponding eigenvectors are

Then,

where the limit is due to Szegö theorem (Gray, 2006) and the integral can be calculated through the residue theorem from complex analysis.

For , we have

and

Thus,

This yields

and

The proof is completed.

References

- Bai and Silverstein (2004) {barticle}[author] \bauthor\bsnmBai, \bfnmZD\binitsZ. and \bauthor\bsnmSilverstein, \bfnmJack W\binitsJ. W. (\byear2004). \btitleCLT for linear spectral statistics of large-dimensional sample covariance matrices. \bjournalThe Annals of Probability \bvolume32 \bpages553–605. \endbibitem

- Bai and Silverstein (2010) {bbook}[author] \bauthor\bsnmBai, \bfnmZhidong\binitsZ. and \bauthor\bsnmSilverstein, \bfnmJack W\binitsJ. W. (\byear2010). \btitleSpectral analysis of large dimensional random matrices \bvolume20. \bpublisherSpringer. \endbibitem

- Bai and Yin (1993) {barticle}[author] \bauthor\bsnmBai, \bfnmZD\binitsZ. and \bauthor\bsnmYin, \bfnmYQ\binitsY. (\byear1993). \btitleLimit of the Smallest Eigenvalue of a Large Dimensional Sample Covariance Matrix. \bjournalAnnals of Probability \bvolume21 \bpages1275–1294. \endbibitem

- Bai and Zhou (2008) {barticle}[author] \bauthor\bsnmBai, \bfnmZhidong\binitsZ. and \bauthor\bsnmZhou, \bfnmWang\binitsW. (\byear2008). \btitleLarge sample covariance matrices without independence structures in columns. \bjournalStatistica Sinica \bpages425–442. \endbibitem

- Bai et al. (2009) {barticle}[author] \bauthor\bsnmBai, \bfnmZhidong\binitsZ., \bauthor\bsnmJiang, \bfnmDandan\binitsD., \bauthor\bsnmYao, \bfnmJian-Feng\binitsJ.-F. and \bauthor\bsnmZheng, \bfnmShurong\binitsS. (\byear2009). \btitleCorrections to LRT on large-dimensional covariance matrix by RMT. \bjournalThe Annals of Statistics \bvolume37 \bpages3822–3840. \endbibitem

- Bandeira, Lodhia and Rigollet (2017) {barticle}[author] \bauthor\bsnmBandeira, \bfnmAfonso S\binitsA. S., \bauthor\bsnmLodhia, \bfnmAsad\binitsA. and \bauthor\bsnmRigollet, \bfnmPhilippe\binitsP. (\byear2017). \btitleMarcenko-Pastur law for Kendall’s tau. \bjournalElectronic Communications in Probability \bvolume22. \endbibitem

- Bao (2019a) {barticle}[author] \bauthor\bsnmBao, \bfnmZhigang\binitsZ. (\byear2019a). \btitleTracy–Widom limit for Spearman’s rho. \bjournalPreprint. \endbibitem

- Bao (2019b) {barticle}[author] \bauthor\bsnmBao, \bfnmZhigang\binitsZ. (\byear2019b). \btitleTracy–Widom limit for Kendall’s tau. \bjournalAnnals of Statistics \bvolume47 \bpages3504–3532. \endbibitem

- Bao, Pan and Zhou (2012) {barticle}[author] \bauthor\bsnmBao, \bfnmZhigang\binitsZ., \bauthor\bsnmPan, \bfnmGuangming\binitsG. and \bauthor\bsnmZhou, \bfnmWang\binitsW. (\byear2012). \btitleTracy-Widom law for the extreme eigenvalues of sample correlation matrices. \bjournalElectronic Journal of Probability \bvolume17 \bpages1–32. \endbibitem

- Bao et al. (2015) {barticle}[author] \bauthor\bsnmBao, \bfnmZhigang\binitsZ., \bauthor\bsnmLin, \bfnmLiang-Ching\binitsL.-C., \bauthor\bsnmPan, \bfnmGuangming\binitsG. and \bauthor\bsnmZhou, \bfnmWang\binitsW. (\byear2015). \btitleSpectral statistics of large dimensional Spearman’s rank correlation matrix and its application. \bjournalAnnals of Statistics \bvolume43 \bpages2588 – 2623. \endbibitem

- Childs (1967) {barticle}[author] \bauthor\bsnmChilds, \bfnmDonald R\binitsD. R. (\byear1967). \btitleReduction of the multivariate normal integral to characteristic form. \bjournalBiometrika \bvolume54 \bpages293–300. \endbibitem

- El Karoui (2009) {barticle}[author] \bauthor\bsnmEl Karoui, \bfnmNoureddine\binitsN. (\byear2009). \btitleConcentration of measure and spectra of random matrices: Applications to correlation matrices, elliptical distributions and beyond. \bjournalThe Annals of Applied Probability \bvolume19 \bpages2362–2405. \endbibitem

- Esscher (1924) {barticle}[author] \bauthor\bsnmEsscher, \bfnmFredrick\binitsF. (\byear1924). \btitleOn a method of determining correlation from the ranks of the variates. \bjournalScandinavian Actuarial Journal \bvolume1924 \bpages201–219. \endbibitem

- Féral and Péché (2009) {barticle}[author] \bauthor\bsnmFéral, \bfnmDelphine\binitsD. and \bauthor\bsnmPéché, \bfnmSandrine\binitsS. (\byear2009). \btitleThe largest eigenvalues of sample covariance matrices for a spiked population: diagonal case. \bjournalJournal of Mathematical Physics \bvolume50 \bpages073302. \endbibitem

- Gao et al. (2017) {barticle}[author] \bauthor\bsnmGao, \bfnmJiti\binitsJ., \bauthor\bsnmHan, \bfnmXiao\binitsX., \bauthor\bsnmPan, \bfnmGuangming\binitsG. and \bauthor\bsnmYang, \bfnmYanrong\binitsY. (\byear2017). \btitleHigh dimensional correlation matrices: The central limit theorem and its applications. \bjournalJournal of the Royal Statistical Society, Series B \bvolume79 \bpages677–693. \endbibitem

- Gray (2006) {barticle}[author] \bauthor\bsnmGray, \bfnmRobert M\binitsR. M. (\byear2006). \btitleToeplitz and circulant matrices: a review. \bjournalFoundations and Trends in Communications and Information Theory \bvolume2 \bpages155–240. \endbibitem

- Heiny and Yao (2020) {barticle}[author] \bauthor\bsnmHeiny, \bfnmJohannes\binitsJ. and \bauthor\bsnmYao, \bfnmJianfeng\binitsJ. (\byear2020). \btitleLimiting distributions for eigenvalues of sample correlation matrices from heavy-tailed populations. \bjournalarXiv preprint arXiv:2003.03857. \endbibitem

- Jiang (2004) {barticle}[author] \bauthor\bsnmJiang, \bfnmTiefeng\binitsT. (\byear2004). \btitleThe limiting distributions of eigenvalues of sample correlation matrices. \bjournalSankhyā: The Indian Journal of Statistics \bvolume66 \bpages35–48. \endbibitem

- Johnstone (2001) {barticle}[author] \bauthor\bsnmJohnstone, \bfnmIain M\binitsI. M. (\byear2001). \btitleOn the distribution of the largest eigenvalue in principal components analysis. \bjournalAnnals of Statistics \bvolume29 \bpages295–327. \endbibitem

- Kargin (2015) {barticle}[author] \bauthor\bsnmKargin, \bfnmVladislav\binitsV. (\byear2015). \btitleSubordination for the sum of two random matrices. \bjournalThe Annals of Probability \bvolume43 \bpages2119–2150. \endbibitem

- Kendall (1938) {barticle}[author] \bauthor\bsnmKendall, \bfnmMaurice G\binitsM. G. (\byear1938). \btitleA new measure of rank correlation. \bjournalBiometrika \bvolume30 \bpages81–93. \endbibitem

- Kendall (1949) {barticle}[author] \bauthor\bsnmKendall, \bfnmMaurice G\binitsM. G. (\byear1949). \btitleRank and product-moment correlation. \bjournalBiometrika \bpages177–193. \endbibitem

- Knowles and Yin (2017) {barticle}[author] \bauthor\bsnmKnowles, \bfnmAntti\binitsA. and \bauthor\bsnmYin, \bfnmJun\binitsJ. (\byear2017). \btitleAnisotropic local laws for random matrices. \bjournalProbability Theory and Related Fields \bvolume169 \bpages257–352. \endbibitem

- Leung and Drton (2018) {barticle}[author] \bauthor\bsnmLeung, \bfnmDennis\binitsD. and \bauthor\bsnmDrton, \bfnmMathias\binitsM. (\byear2018). \btitleTesting independence in high dimensions with sums of rank correlations. \bjournalAnnals of Statistics \bvolume46 \bpages280–307. \endbibitem

- Li, Wang and Li (2021) {barticle}[author] \bauthor\bsnmLi, \bfnmZeng\binitsZ., \bauthor\bsnmWang, \bfnmQinwen\binitsQ. and \bauthor\bsnmLi, \bfnmRunze\binitsR. (\byear2021). \btitleCentral limit theorem for linear spectral statistics of large dimensional Kendall’s rank correlation matrices and its applications. \bjournalAnnals of Statistics \bvolume49 \bpages1569 – 1593. \endbibitem

- Liu, Lafferty and Wasserman (2009) {barticle}[author] \bauthor\bsnmLiu, \bfnmHan\binitsH., \bauthor\bsnmLafferty, \bfnmJohn\binitsJ. and \bauthor\bsnmWasserman, \bfnmLarry\binitsL. (\byear2009). \btitleThe nonparanormal: Semiparametric estimation of high dimensional undirected graphs. \bjournalJournal of Machine Learning Research \bvolume10. \endbibitem

- Marc̆enko and Pastur (1967) {barticle}[author] \bauthor\bsnmMarc̆enko, \bfnmVladimir A\binitsV. A. and \bauthor\bsnmPastur, \bfnmLeonid Andreevich\binitsL. A. (\byear1967). \btitleDistribution of eigenvalues for some sets of random matrices. \bjournalMathematics of the USSR-Sbornik \bvolume1 \bpages457. \endbibitem

- Mestre and Vallet (2017) {barticle}[author] \bauthor\bsnmMestre, \bfnmXavier\binitsX. and \bauthor\bsnmVallet, \bfnmPascal\binitsP. (\byear2017). \btitleCorrelation tests and linear spectral statistics of the sample correlation matrix. \bjournalIEEE Transactions on Information Theory \bvolume63 \bpages4585–4618. \endbibitem

- Morales-Jimenez et al. (2021) {barticle}[author] \bauthor\bsnmMorales-Jimenez, \bfnmDavid\binitsD., \bauthor\bsnmJohnstone, \bfnmIain M\binitsI. M., \bauthor\bsnmMcKay, \bfnmMatthew R\binitsM. R. and \bauthor\bsnmYang, \bfnmJeha\binitsJ. (\byear2021). \btitleAsymptotics of eigenstructure of sample correlation matrices for high-dimensional spiked models. \bjournalStatistica Sinica \bvolume31 \bpages571. \endbibitem

- Pillai and Yin (2012) {barticle}[author] \bauthor\bsnmPillai, \bfnmNatesh S\binitsN. S. and \bauthor\bsnmYin, \bfnmJun\binitsJ. (\byear2012). \btitleEdge universality of correlation matrices. \bjournalAnnals of Statistics \bvolume40 \bpages1737–1763. \endbibitem

- Schott (2005) {barticle}[author] \bauthor\bsnmSchott, \bfnmJames R\binitsJ. R. (\byear2005). \btitleTesting for complete independence in high dimensions. \bjournalBiometrika \bvolume92 \bpages951–956. \endbibitem

- Silverstein and Bai (1995) {barticle}[author] \bauthor\bsnmSilverstein, \bfnmJack W\binitsJ. W. and \bauthor\bsnmBai, \bfnmZD\binitsZ. (\byear1995). \btitleOn the empirical distribution of eigenvalues of a class of large dimensional random matrices. \bjournalJournal of Multivariate Analysis \bvolume54 \bpages175–192. \endbibitem

- Wang, Jin and Miao (2011) {barticle}[author] \bauthor\bsnmWang, \bfnmCheng\binitsC., \bauthor\bsnmJin, \bfnmBaisuo\binitsB. and \bauthor\bsnmMiao, \bfnmBaiqi\binitsB. (\byear2011). \btitleOn limiting spectral distribution of large sample covariance matrices by VARMA (p, q). \bjournalJournal of Time Series Analysis \bvolume32 \bpages539–546. \endbibitem

- Weihs, Drton and Meinshausen (2018) {barticle}[author] \bauthor\bsnmWeihs, \bfnmLuca\binitsL., \bauthor\bsnmDrton, \bfnmMathias\binitsM. and \bauthor\bsnmMeinshausen, \bfnmNicolai\binitsN. (\byear2018). \btitleSymmetric rank covariances: a generalized framework for nonparametric measures of dependence. \bjournalBiometrika \bvolume105 \bpages547–562. \endbibitem

- Zheng et al. (2019) {barticle}[author] \bauthor\bsnmZheng, \bfnmShurong\binitsS., \bauthor\bsnmCheng, \bfnmGuanghui\binitsG., \bauthor\bsnmGuo, \bfnmJianhua\binitsJ. and \bauthor\bsnmZhu, \bfnmHongtu\binitsH. (\byear2019). \btitleTest for high-dimensional correlation matrices. \bjournalAnnals of Statistics \bvolume47 \bpages2887–2921. \endbibitem